The Layman’s Guide to Accounting, Part 2

The Layman’s Guide to Accounting, Part 2

The Three Accounting Statements

The Layman’s Guide series is a series of short articles going over particular aspects and principles of fields normally considered complicated or too academic for the average person. Emphasizing the principles and ideas that an average person may encounter in their daily life, while tying them together to the discipline as a whole, The Layman’s Guides are intended to be both a reference and an introduction. It is in essence what I wish I had when I was younger, a series of articles explaining key principles of a profession that allow one to begin exploring the field more holistically. In this second part of The Layman’s Guide into Accounting, we get into the three accounting statements that are central to the profession. If you missed the first part, it’s here, and you’ll want to read that to understand this.

Temporary and Permanent Accounts

In the last part, I made a distinction between temporary and permanent accounts. Temporary accounts are accounts that are meant to record transactions of a certain type during a certain period, before being “closed” to a temporary account. Temporary accounts allow for more accurate and detailed record-keeping without clogging up the permanent accounts with entries and making them difficult to trace. Revenues and expenses are the most common temporary accounts, because they are where the advantages of temporary accounts shine – of all types of transactions, sales and purchases are the most frequent and most varied of transactions

Permanent accounts, by contrast, are accounts of record whose importance is not in their flow, but in their stock. This is particularly important in items like cash, inventory, and owner’s equity – all things you don’t want to run out of, or in debt, which you don’t want to have too much of. While these are affected by all the accounting entity’s activities, these balances are more often of interest as matters of record and planning, so they are updated less frequently than temporary accounts.

While the line between these two accounts is blurred by modern computerized accounting systems, it is an important distinction that will help you understand the differing treatment of different accounts later.

Easy analogies for temporary and permanent accounts are below:

Computers – Temporary accounts – Random Access Memory (RAM), built for frequent reading and writing: Permanent accounts – Read-Only Memory (ROM), built to maintain a long-term record.Restaurants – Temporary accounts – Quick-service restaurant focusing on volume and thin profit margins: Permanent accounts – Steakhouse or Sit-down restaurant focusing on fewer customers with higher profit margins.Logistics – Temporary accounts – individual delivery riders and vans moving goods to and from warehouses: Permanent accounts – high-volume transport in the form of container trucks, trains, or cargo ships.The Three Accounting Statements

The three central accounting statements are the balance sheet, the income statement, and the cash flow statement. More formally, they are called the statement of financial position, the profit and loss statement, and the cash flow statement. They are defined as follows:

Statement of Financial Position: a snapshot at a certain date (usually the end of the financial year) of all the accounting entity’s assets, liabilities, and equity accounts. More colloquially called a balance sheet in accordance with the fundamental accounting equation from the first part – Assets = Liabilities + Equity, or Things = Things Owed + Things Owned.

Statement of Profit and Loss: A recording of transactions affecting profit and loss over the past financial year, or whatever accounting period, of all the accounting entity’s typical business activities[1]. More colloquially called the income statement, the statement of profit and loss tallies up all the business activities that affect profit and loss and lists them. As we previously discussed revenues and expenses being composed of a large number of temporary accounts, one can view the income statement as a statement summarizing the closure of all of those temporary accounts to equity.Statement of Cash Flows: A recording of transactions affecting cash over the past financial year, or whatever accounting period. The cash flow statement tallies up all the business activities that affect cash – which are usually mediated through temporary accounts. Much like the statement of profit and loss, one can view it as a closure of all the temporary accounts involving cash. Often, this statement is prepared via deductions and modifications to the statement of profit and loss.We can see here that there are actually only two statements – the statement of position, or the balance sheet, which involves listing the permanent accounts’ balances at a certain date for record and comparison, and the statements of flows, the income and cash flow statements, which list the balances of temporary accounts for a certain period, which are then closed to the corresponding permanent accounts.

Each statement has something to say about the health of the company, and we’ll be tackling them in their own sections below. I’ll also show you how to construct your own simple statement, based on the convention seller’s example from the previous part’s section on entries.

The Income Statement

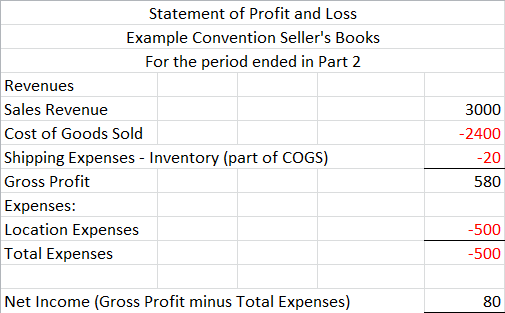

To draw up an income statement, you need to know exactly what goes into it. While that’s defined much more formally in the International Financial Reporting Standards (Generally Accepted Accounting Principles for the United States), the long and short of it is that the income statement summarizes all transactions in the normal course of business that result in a profit or loss, without being direct modifications to owner’s equity. Most often, these transactions are the sales and purchases of the accounting entity, resulting respectively in revenues and expenses. The following entries will be used in the preparation of the income statement:

Dr. Location Expenses $500/Cr. Cash $500

Dr. Cash $2,500/Cr. Sales Revenue $2,500

Dr. Cost of Goods Sold $2,000/Cr. Merchandise Inventory $2,000.

From the succeeding section on Accrual and Cash Bases:

Dr. Accounts Receivable $500/Cr. Sales Revenue $500

Dr. Cost of Goods Sold $400/Cr. Merchandise Inventory $400.

Dr. Shipping Expenses – Inventory $20/Cr. Cash $20.

For our purposes, the temporary accounts involved are Sales Revenue (all sales), Cost of Goods Sold (Price paid for sold goods), Location Expenses (expenses involved in setting up a stall), and Shipping Expenses[2] (expenses paid to ship inventory). Income, or profits, is revenues minus costs – or, in this case, sales revenue minus all the other temporary accounts, which account for costs. Therefore, our income statement would look like this:

As you can see, we simply totaled up all the entries based on their effects on profit and loss, and then wrote an entry closing them to the equity account used to close profit and loss – Retained Earnings. The entry looks like this:

Dr. Net Income $80/Cr. Retained Earnings $80

Retained Earnings’ role is to separate outside investment in the business (people funding it) from the business’ ability to make money and invest in itself (the business funding itself). Directly crediting owner’s equity or shareholder’s equity would cause a problem, in that the value of their investment, and, in the case of sole proprietorships or partnerships, how much in drawings they can withdraw, would change, despite their legal rights staying the same. Retained Earnings sidesteps that by putting “the business’ investments in itself” under a different account.

While this is important, none of this will tell you how close you are to insolvency or bankruptcy. For that, we have the statement of cash flows.

The Statement of Cash Flows

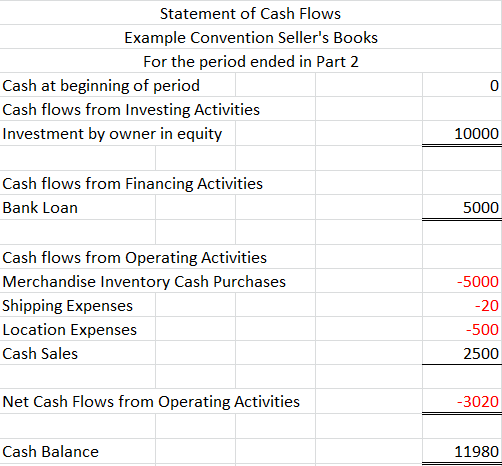

The cash flow statement is a much broader statement than the income statement, taking into account not only business operations, but also loans and investments in the accounting entity. As such, it is often split into three parts – the operating, investing, and financing cash flows, each of which corresponds to cash from business operations, cash from equity infusion, and cash from borrowings. We will focus on the operating cash flow, as investing and financing are often tallied separately. There are two methods of deriving the statement of operating cash flows – the direct method, and the indirect method, both of which I will demonstrate here. The direct method sis called direct, because it directly tackles the problem by tallying and summarizing all entries to cash. The entries we will use to prepare the direct method are used below:

Dr. Cash $10,000/Cr. Owner’s Equity $10,000

Dr. Cash $5,000/Cr. Loans Payable $5,000

Dr. Merchandise Inventory $5,000/Cr. Cash $5,000

Dr. Location Expenses $500/Cr. Cash $500

Dr. Cash $2,500/Cr. Sales Revenue $2,500

Dr. Shipping Expenses $20/Cr. Cash $20.

Dr. Cash $500/Cr. Accounts Receivable $500

Something that should immediately jump out at you is that not all of these flows are of the same type. Your $10,000 dollars in was an investment and the $5,000 borrowed a loan, and the rest of the cash flows are business transactions. These will go into the investing and financing cash flows, respectively. The rest, however, are business activities – which go into the operating cash flow. Via the direct method, we simply do as we did with the income statement, and total up all the entries opposite cash, like so:

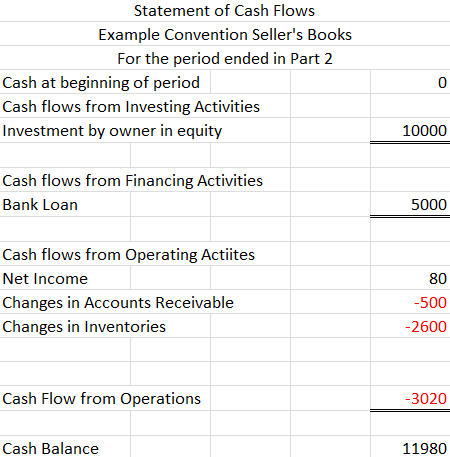

Note that we followed a process much like the one from the income statement. Begrudging, as any reasonable person would, doing the same work twice, the accountant comes up with an idea – why don’t we just take net income and adjust it to the cash basis? We have the entries, after all, so we know which transactions are cash but aren’t on the income statement. I demonstrate this below:

Unlike the direct method for preparing cash flow statements, the indirect method relies on changes in accounts not covered by the income statement. While generally accurate, these two methods do not always tally, since the changes in account balances of Accounts Receivable, Inventory, and other assets do not always reflect cash transactions. The indirect method has an important advantage, however - the work is already partially done by the income statement, so most cash flow statements are prepared with this method. No sense in doing the work twice.

The Balance Sheet

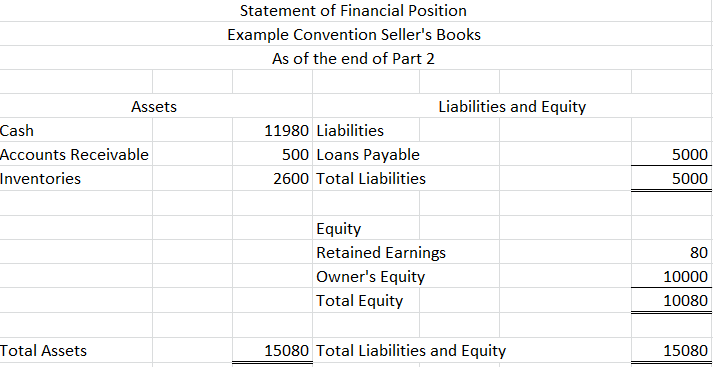

The statement of financial position, or the balance sheet, tallies all the permanent accounts at a certain period of time, after having changes between the last period and the current period reflected in the income statement. These are divided into assets, liabilities, and equity – the former two divided further into current and non-current. Current assets are assets that can be converted into cash within a year, while current liabilities are those that fall due within the year. Conversely, non-current assets are those that cannot be converted to cash into a year, while non-current liabilities are liabilities that do not fall due within the year. These are totaled up in the balance sheet, as seen below:

You can immediately see where the term “balance sheet” comes from – assets should equal the same amount as liabilities and equity, therefore balancing. Unique among the financial statements, the balance sheet is at a certain date, rather than being for a period. Though we don’t have any non-current assets or non-current liabilities here, if we did, they would appear under the assets and liabilities sections of the balance sheet.

The Statement of Changes in Owner’s Equity

There is actually a fourth financial statement – the statement of changes in owner’s equity. This statement summarizes the changes in owner’s equity that occur due to operations. We won’t cover this in detail, because most of the accounts you’ll find here involve valuation reserves, foreign exchange losses, and other more difficult topics. The statement is most important, however, in partnerships. Unlike sole proprietorships where there is only one owner or corporations where retained earnings are properties of the business, the equity investments of individual partners must be kept separate in order to maintain the records of how much of the partnership’s money they have claim to, recorded as their share of owner’s equity. Let’s have an example below:

Gandalf, Frodo, Aragorn, Gimli, and Legolas form a partnership to run an armored car service named the Fellowship of the Bling. Each partner other than Gimli invests $10,000, with Gimli investing $20,000 because he has plenty of inheritance. They agree to divide profits pro rata – in accordance with their contribution to the partnership. Over the past year, the Fellowship of the Bling rakes in $100,000 in net income, which goes not to retained earnings, but to the individual partners’ balances.In order to do this, we start by having their shares of Owner’s Equity be equal to their investment in the partnership and their proportion of the total investment of $60,000. The four partners who invested $10,000 are therefore entitled to 1/6th of the profits, and Gimli to 2/6th for his outsized contribution. 1/6th of $100,000 is equal to 16,666.67 (rounded up to 2 decimals), leading to entries looking like the following:

Dr. Net Income (remember that Net Income is a credit account)/Cr. Gandalf/Frodo/Aragorn/Legolas’ Share $16,666.67

Dr. Net Income/Cr. Gimli’s Share $33,335.34.

A comparison of their equity at the beginning and end of the year is shown:

Four partners go from $10,000 to $26,666.67

Gimli goes from $20,000 to $53,335.34.

This is important, because if any partner decides to call in their equity and make drawings from the partnership, a record needs to be kept to make sure they don’t draw more than they have earned. In this case, if any of the four partners tried to withdraw $30,000, the partnership can point to their owner’s equity and say – “we don’t owe you $30,000, only $26,666.67”.

The equivalent of this for a corporation would be share buybacks – if a corporation buys back its shares at a particular price, it would be the same as cashing you out at a certain amount. The key difference, however, is that shares in corporations can be traded, while shares in partnerships are personal. Therefore, the only way to get money out of a partnership as a partner, besides any salary you might earn, is based on drawings.

This is a simple example that doesn’t seem to justify the effort put in, but remember that many other methods of distributing income between partners exist. Bonuses paid out to partners every year, splits independent from the level of investment, and so on can complicate the distribution of equity, making it an important statement once the business becomes more complex – but not when it’s just starting.

Once you start making money, controlling how it is distributed becomes just as, if not more important than the fact you made it.

Conclusion

That concludes Part 2 of The Layman’s Guide to Accounting. For Part 3, I’m thinking of either doing personal finance or reading financial statements for investment. While the former is more practical for some, the latter as a skill may be more in-demand.

Let me know which you prefer.

[1] Non-business activities changing owner’s equity such as valuation reserves, income over book value from share of sales, dividends, drawings from shares in sole proprietorships or partnerships, or an increase in those investments, are detailed in the Statement of Changes in Equity.

[2] Strictly speaking, we should capitalize Shipping Expenses as part of Cost of Goods Sold, as the inventory could not be delivered if the shipping was not paid, making the shipping expense a direct part of Cost of Goods Sold. This will be important when interpreting the financial statements, but it makes for a clearer demonstration.