12/11 – 12/15 Biotech Moonshots Update

12/11 – 12/15 Biotech Moonshots Update

Profiting From $20-for-$1 Biotechs

The biotech bear market from February 2021 through October 2023 created some dramatically underpriced stocks. There is free money lying on the sidewalk, just waiting for you to pick it up.

Dear Biotechies:

As we come to the end of the year, company news flow shrinks sharply. They enter a blackout period when they can't buy back stock and don't want to comment on how their December quarter is going, unless it is much better or much worse than what they've said previously. With the companies mum, brokerage firm conferences stop.

At the same time, Wall Street gets ready for the annual tsunami of pension fund cash from corporations – yes, that's still a thing – by buying stocks before their customers can. All eyes turn to bigger news, primarily economic. Since last Thursday we've gotten November payrolls, the November Consumer Price Index, and a Fed meeting – all good news for stocks. Let's dig in...

November Payrolls

Payrolls added 199,000 versus the +180,000 forecast and +150,000 in October as striking auto workers and Hollywood actors came back to the workforce. September and October were revised down again – for the 11th straight month - but this time by only about 36,000. The Bureau of Labor Statistics models may finally have caught up with reality.

The unemployment rate dropped from 3.9% in October to 3.7% while the worker participation rate increased slightly from 62.7% to 62.8%. Annual wage inflation, which the Fed watches closely, held steady at 4% in November.

The message to the Fed and the markets was the economy is not falling apart but also not wildly overheating. Soft landing, anyone?

November Inflation

The headline year-over-year Consumer Price Index declined to 3.1% and the core (ex-food and energy) came in at 4.0%, both as expected. The entire rise of the Core CPI was due to cars and housing.

h/t @fundstrat

If Shelter was 0%, both the headline and core month-over-month CPI would be way negative . But Shelter shouldn't be zero, it actually should be negative to match real rent deflation in November. In other words, we already have deflation in November but it is masked by the badly lagging Shelter cost data. Chairman Powell knows this and that the services figures are distorted by car-related services. Powell explicitly acknowledged that non-housing service disinflation progress has become significant.

The November CPI shows why the Fed could cut rates, but the shelter component is still giving them an alibi to keep rates high. As I've been saying, “high (but not higher) for longer.”

The Fed

Chairman Powell, December 1: “It would be premature to … speculate on when policy might ease.”

Chairman Powell, December 13: Rate cuts are something that “begins to come into view” and “clearly is a topic of discussion.”

Is this an election-year rate cut projection? I don't think Powell cares about elections, the level of the stock market, or anything but inflation as measured by the core Personal Consumption Expenditures Index and the value of the dollar relative to other currencies.

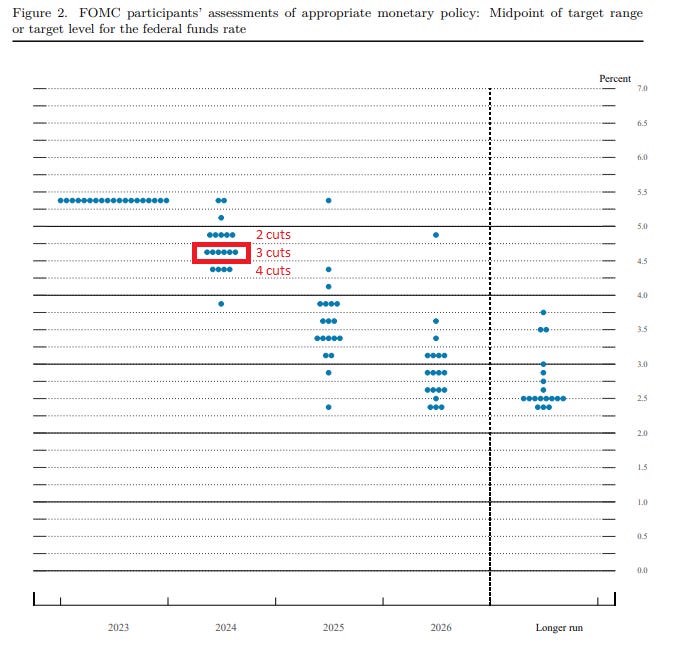

So on Wednesday, as I expected, the FOMC held rates steady at a 22-year high, extending the pause, and retained a weak tightening bias in the statement. They now expect inflation to fall to 2.4% next year - down from 2.5% forecast in September - and drop further to 2.2% by 2025.

The Dot Plot shows a median projection of three rate cuts in 2024. One FOMC member expects six rate cuts in 2024, four see four cuts, six project three cuts, five see two cuts, one thinks one cut, and two expect no cuts. That is the most confused “year ahead” FOMC we've seen in years.

h/t @NickTimiraos

After the dovish FOMC meeting, Fed Funds Futures are now pricing SIX rate cuts in 2024. That's a total reduction of 150 basis points to a range of 3.75% to 4.00% that is expected to begin in March. I think that's nuts, but so much for the Dot Plot suggesting three cuts and the futures market caring at all.

As I see it, real interest rates – the amount by which they exceed inflation - are the highest in this cycle while Quantitative Tightening continues. What else could Powell want? He loves sounding dovish when he isn't – it keeps Senator Warren and her ilk off his back. As he said about the last mile of getting inflation down: “We kind of assume it will get harder from here, but so far it hasn't.”

Powell made it clear the Fed wouldn’t wait until inflation gets all the way down to 2% to start cutting.

"It would be too late," he said. "You would want to be reducing restriction on the economy before you get to 2%…so you don’t overshoot."

Personal Consumption Expenditures Index

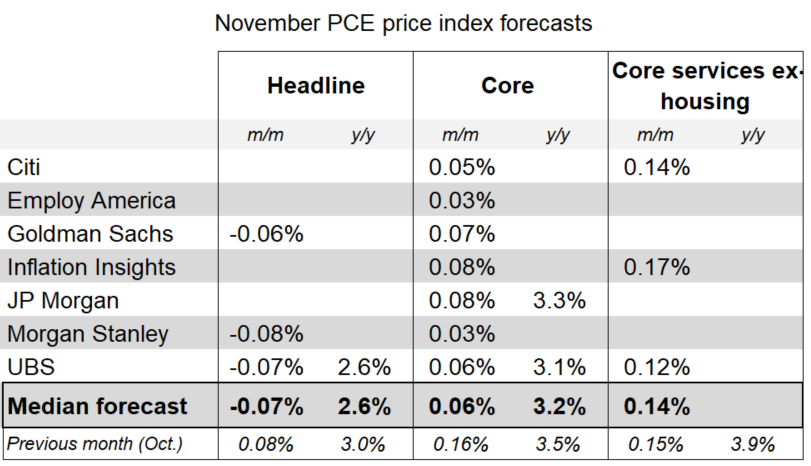

The Fed’s favored inflation measure — the core Personal Consumption Expenditures index — was 3.5% for October, down from 3.7% in September and 4.3% in June. The November PCE announcement comes December 22. Based on the November CPI and PPI, headline PCE inflation likely declined last month. Core PCE inflation is projected to have been a very mild 0.06% in November. This could lower the 12-month core PCE index to 3.1%. The 6-month annualized rate would fall to 1.9%, below the Fed's target.

h/t @NickTimiraos

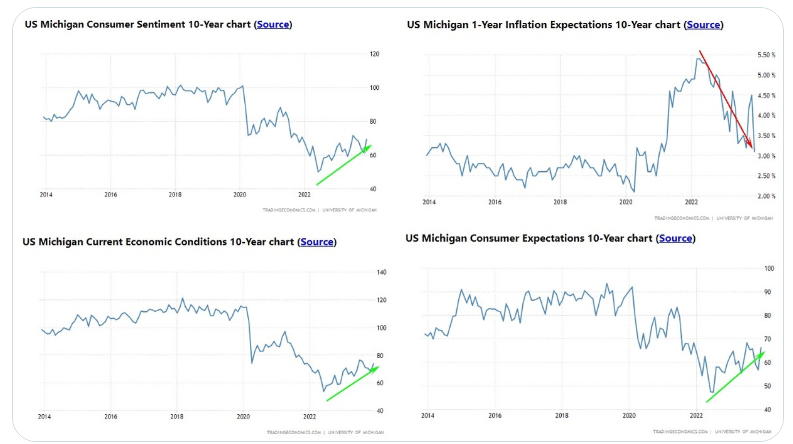

The news of lower inflation and a strong economy is being met with more optimism from the market now. We have not seen this before in this cycle – fear of the Fed after every bit of good news has been replaced by hope for a stronger economy. The latest University of Michigan consumer sentiment survey showed consumers expect inflation to sit at 3.1% in a year, a big decrease from last month's expectation of 4.5%. That's the lowest since March 2021 and only slightly above the 2.3% to 3.0% range seen in the two years before the pandemic. Expectations for long-run inflation fell to 2.8%, down from November's 3.2%, which was the highest reading since 2011.

h/t @OphirGottlieb

Market Outlook

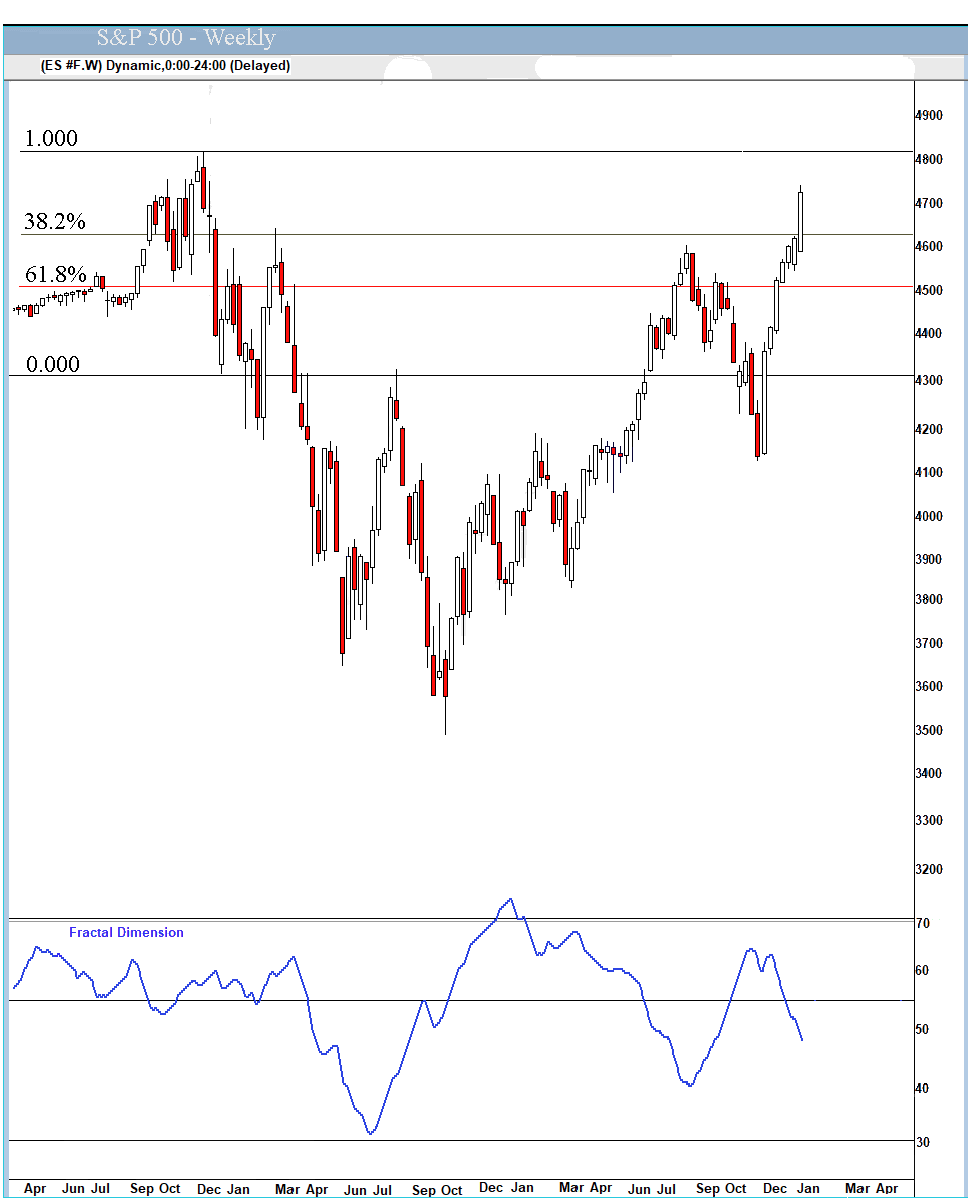

The stock market has been up for seven straight weeks. After the Fed meeting on Wednesday, Powell's press conference unleashed historic devastation on the net-short hedge funds. There were margin calls galore into the close. The venerable Dow Jones Industrial Average closed at a new all-time high as it surpassed 37,000 for the first time ever. The S&P 500 added 2.9% since last Thursday and is up 22.9% year-to-date. Not bad!

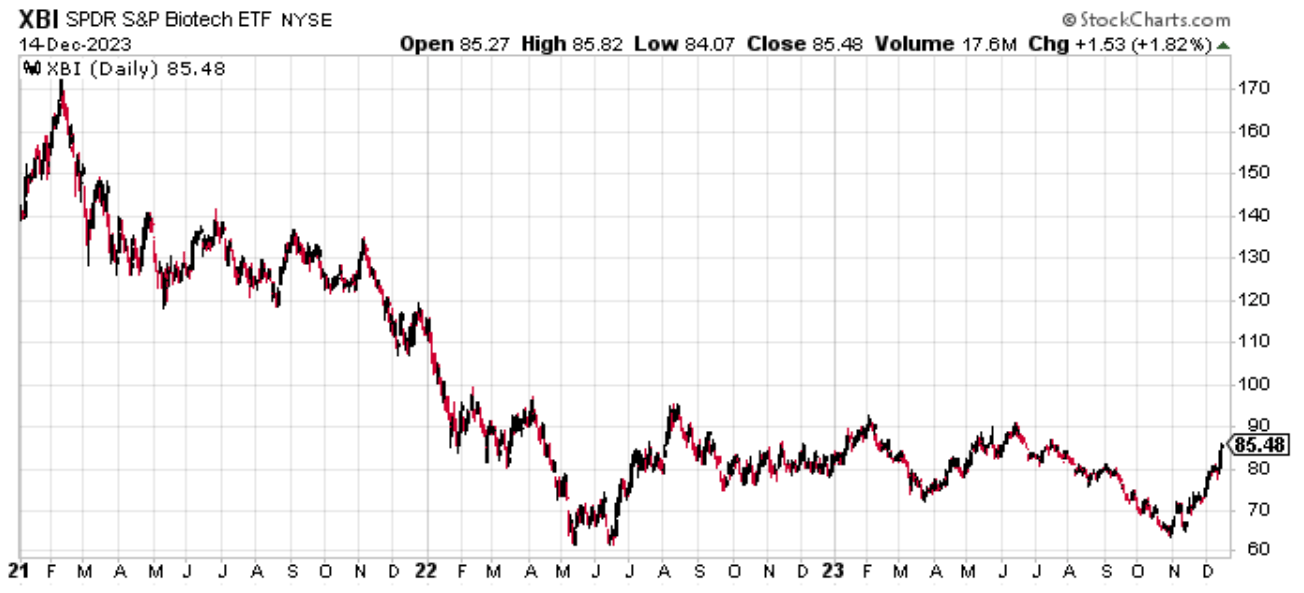

The Nasdaq Composite also gained 2.9% and is up a stunning 41.0% for the year. Thank you, AI! The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 6.2% to tell the world the biotech bear is over (see chart below). It is only up 3.0% year-to-date, but it's on a roll. The small-cap Russell 2000 soared 7.1% to close over 2,000 and is up 13.6% in 2023. 2024 should be much better.

The fractal dimension signaled a new uptrend a few weeks ago and nailed it. We probably have six to eight more up weeks before the inevitable next consolidation.

Economy

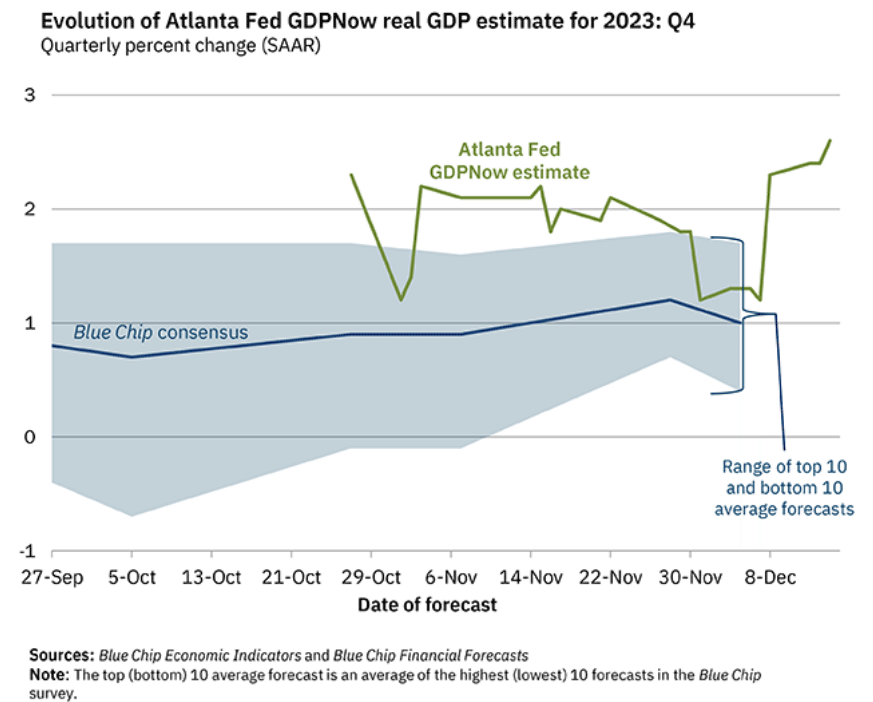

Yesterday morning, the Atlanta Fed's GDPNow model increased its forecast for December quarter real GDP to +2.6% due to big increases in personal consumption expenditures growth, domestic investment growth, and government spending growth.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies' websites so you can listen to them.

Thursday, December 21

September quarter GDP - 8:30am – Third estimate

Winter Solstice - 10:27pm

Friday, December 22

Personal Consumption Expenditures Index - 8:30am

The 2 ¾-year biotech bear market ended with a bang on October 27. Next, the strength in the XBI will spread down to the smaller companies. Now is the time to get onboard!

Biotech Focus

PWC said mergers and acquisitions across the pharmaceuticals and lifesciences sector will reach a “healthy” level in 2024, with deals totaling $225 billion to $275 billion. Channelcheck wrote “Biotech Dealmaking Heats Up as Private Capital Charges Back In.” They said:

“A wave of multibillion dollar buyouts has swept the beaten-down biotech sector in recent months, marking a potential turning point for an industry hammered throughout 2022 – 2023. With valuations of public companies still depressed, flush private investors have stepped up acquisitions of promising drug developers to bolster pipelines for the long-term. And in a bullish sign for the strategic direction of the space, therapeutics targeting high unmet needs and novel modalities remain key areas of focus amid dealmaking...

“Gene therapy remains one especially alluring area for dealmaking despite lofty price tags. These ultra-rare disease medicines come with cure potential that commands premium sales and reimbursement pricing power.

“Recognizing the imperative to bulk up gene therapy capabilities, Pfizer ponied up $5.4 billion to reinforce its genetic medicines pipeline through the acquisition of French outfit Vivet Therapeutics. The move added Vivet’s promising gene therapy for Wilson disease, along with manufacturing strengths across multiple delivery mechanisms...

“Beyond M&A from strategic acquirers, private equity firms have swooped in to capitalize on depressed biotech valuations. The robust dry powder levels built up during the boom years leave private investors eager to allocate while achieving advantageous cost bases.

“Among notable deals, Angel Pond Capital teamed up with life science investor OrbiMed to take gene therapy biotech Generate Biomedicines private for $478 million. The transaction represented a 130% premium to ensure locking up Generate’s base editing technologies believed to be capable of correcting over 75% of known point mutations...

“The fresh upswing in biotech M&A follows a wave of dip buying from some the world’s largest asset managers in shares of industry leaders like Vertex Pharmaceuticals and Regeneron Pharmaceuticals. Warren Buffett’s Berkshire Hathaway has been particularly aggressive, stepping in to purchase stakes in key biopharma bluechips...

“With fundamentals stabilizing and access to capital normalizing, the environment for biopharma dealmaking has markedly improved. Expect the momentum to carry through 2024 as drug developers position through M&A for the next, post-pandemic leg higher while private capital readily supports compelling technologies at discounted prices. The long-term health of the biotech ecosystem depends on transactions advancing today’s high-potential assets, and the industry appears to have emerged from its lull ready to strike the necessary deals.”

Biotech Moonshots Portfolio Update

This was another excellent week for the portfolio as it jumped another 16.1%. There's enough clinical and other data coming to drive our performance much higher in 2023 and 2024. Let's dig in...