Lucid Motors' Struggle to Survive in 2023

Lucid Motors' Struggle to Survive in 2023

$5bn equity raise is needed this year to keep Lucid afloat

While this is a bearish report on Lucid Motors, keep in mind that the Saudi Arabian sovereign wealth fund (PIF) owns a 64% stake in Lucid. But this doesn’t mean they’d buy it out at current prices.

Lucid’s Current Plight

Over-Ambitious Forecasts Pre-Listing: Lucid Motors raised $4.4bn via a SPAC merger in July 2021 with forecasts of selling 250,000 luxury EVs priced at $90,553 by 2026. This is a target so insane that it assumes Lucid would take 27% of the market in that price range, which was only 936,300 units at its 2019 peak.

Prices Much Lower than Expected: Lucid also said in its pre-listing presentation that its EV line-up would be selling at an average price of $109,233 in 2025, yet recent ASP estimates by the company on its order backlog indicate prices are down to $94,118, or 13% lower than expected.

Tesla Took 8 Years to Become Profitable With No Competition: Raw material and logistics costs have risen dramatically since Lucid’s pre-listing roadshow, making its original target of $637m of operating profit in its fifth year after launch (2025) even more far-fetched. It took Tesla 8 years to become profitable without any EV competition at the time.

Production Targets Slashed Twice: Since going public, Lucid has been a disaster. 2022 production targets were slashed last February by 30% to 13,000 and once again in August by 50% to 6,500, due mostly to production glitches and quality issues.

Order Cancellations: In Q3, Lucid saw its order backlog shrink by 3,000 vehicles to 34,000. With a flood of 31 new EVs set to hit the market in 2023 (plus another 18 launched in 2022 going into full production this year), the chances of further order cancelations are high.

Capex Plans Nearly Halved: Lucid also slashed their 2022 capex budget from $2bn to $1.2bn due to “budget timing” and then launched a $600m ATM equity raise in November. This will make 2023/24 capex much higher than expected and crimp free cash flow.

Exodus of Execs: Lucid lost 6 high-profile execs in 2022, mostly those involved in manufacturing operations. Not a good sign when they’re planning to launch a new variant of the Lucid Air line-up in 2023 and ramp up their first SUV by 1H 2024.

High Inventory and Lower Prices

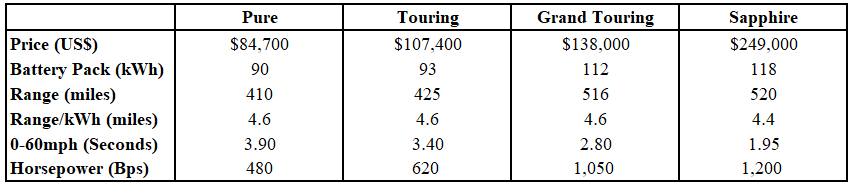

Lucid currently has one model with four variants priced between $87,400 to $249,000 (see Figure-1). So far, the three most expensive models have gone on sale, while many are waiting for the lowest-price “Pure” variant to go on sale at $84,700 in Q2 this year.

Management has stated that most of their backlog consists of orders for the Lucid “Pure”, which will likely lead to lower ASPs than originally planned for 2023. On Lucid’s website, there are currently 22 higher priced Touring and Grand Touring variants on sale for immediate delivery, up from 15 just 4 weeks ago.

Given weaker affordability, there may have been further order cancellations and could explain why Lucid missed Q4 delivery targets of 4,000 units by 52%. Production in Q4 beat expectations by 24% and came in at 3,493 units, causing the stock to spike intraday, but there was no explanation given in Lucid’s press release as to why output exceeded deliveries by 1.8x.

Implied inventory came to 2,936 units, or 114% higher than Q3’s level. If these undelivered cars are in transit, then it’s a not the end of the world, albeit the spike in Inventory should lead to worse than expected Operating Cash Flow.

Figure-1: The Lucid Air Line-Up

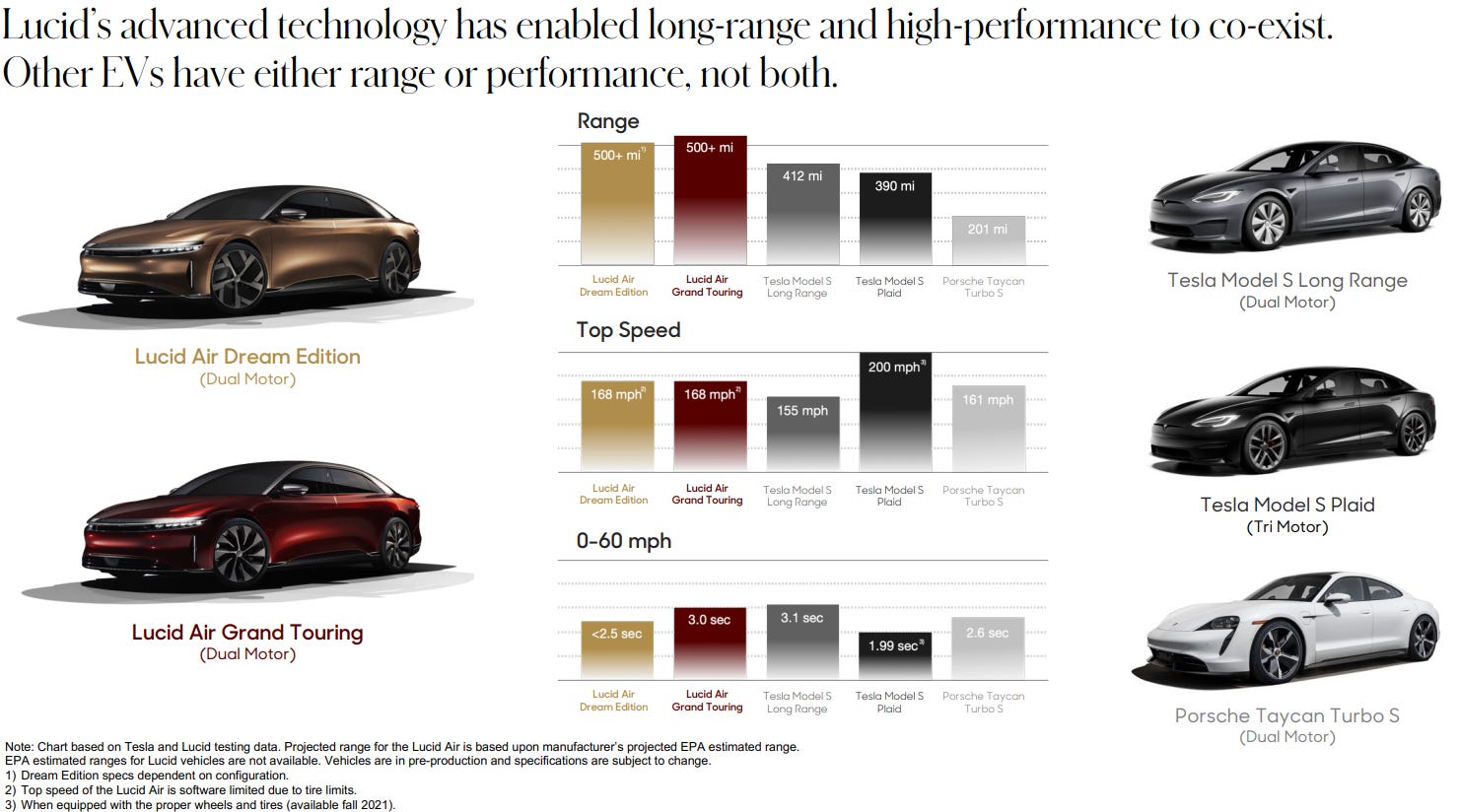

Lucid’s Strengths: Batteries and Motors

The Lucid Air is a great engineering feat in the electric vehicle world, putting Tesla’s drivetrain technology to shame. These are the three main areas of Lucid’s lead in EV technology:

Batteries: Highest battery efficiency due to fewer battery modules, which gives Lucid the longest range on one charge in the industry.

Drivetrain: Lucid’s motors are 40% smaller than rivals. These motors have a power-to-weight ratio of 9 hp/kg (over 3x Tesla’s Model S ratio of 3.2 hp/kg), which is the highest level in the industry.

Fastest Charge Time: Because the Lucid Air uses a 900v battery versus 400v batteries in all other EVs, the Air has the fastest recharging time in the industry at only 20 minutes for 300 miles of range versus 15 minutes for 200 miles of range for the Tesla Model S.

Where Lucid falls short is its software stack, which has been criticized for being “buggy” and still cannot download third-party apps like Apple CarPlay or Android (a big drawback for EV buyers). Lucid scurried to hire new software experts late last year, but the new team (headed by a former Google exec) has yet to fix the problems.

Figure-2: Lucid’s Competitive Edge

Lucid Overstated its Growth Abilities Pre-Listing

In its pre-listing presentation in July 2021, Lucid forecast that the global luxury car segment would grow at a 5% CAGR to 15 million vehicles by 2030, or 12% higher than US car sales in 2022 and 16x peak global luxury car sales of 936,300 vehicles in 2019. This alone should’ve been a red flag for any investor.

Based on these lofty forecast, Lucid projected it could grow its deliveries by a 51% CAGR from 20,000 in 2022 to 537,000 in 2030. Lucid’s 2022 deliveries were only 4,369 and its goal of attaining 537,000 deliveries in 2030 at an average price of $92,781 implies it would’ve reached 57% of the global luxury car market peak in 2019.

Figure-3: Lucid’s Flawed Market Projections & Growth Targets

Lucid faced a class-action lawsuit about false claims on their production outlook, but the case was recently dismissed due to the information in question having been relayed before Lucid’s SPAC merger was even public information. Lucid dodged a bullet, but the fact remains that Lucid lost investors money by overstating their growth capabilities.

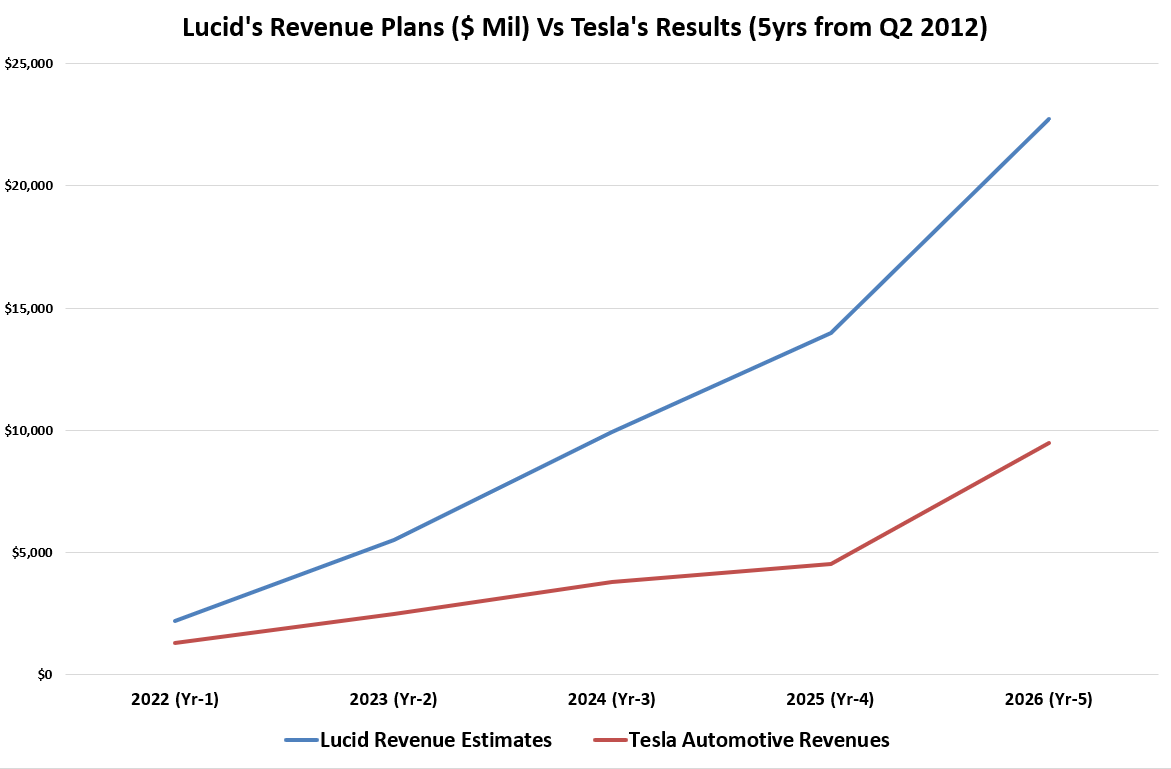

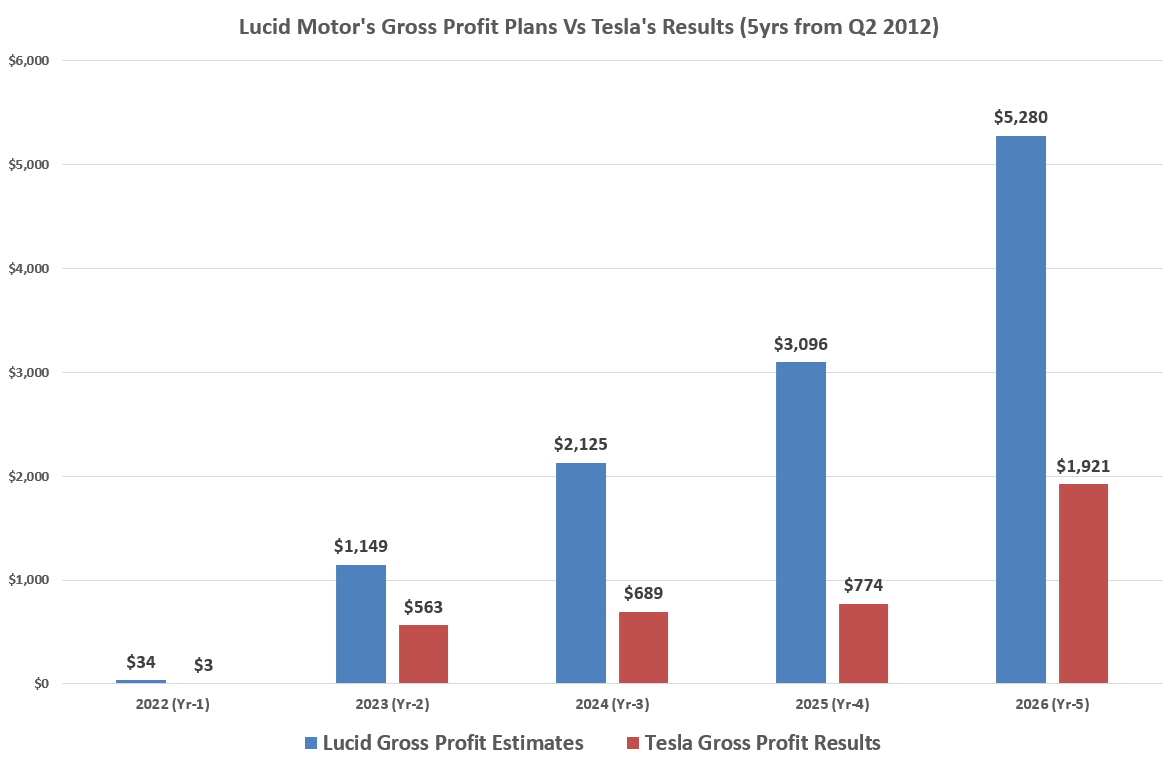

On every metric (deliveries, gross margin, etc.), Lucid has projections in its July 2021 presentation that defy logic when compared to Tesla’s results during its first 5 years since start of production in 2012—a time when there was literally zero competition for Tesla. For reference, the link to Lucid’s July 2021 presentation is here and financial projections start from page 64.

Figures 4 & 5 are just two examples of how unrealistic Lucid’s forecasts are when compared to what happened at Tesla during its first 5 years since 2012 start of production.

Figure-4: Lucid’s Revenue Growth Plans & Tesla’s Results

Figure-5: Lucid’s Gross Profit Plans Versus Tesla’s Results

It took Tesla 8 years to generate its first GAAP net profit in 2020. Lucid is aiming for its first profit in 2025, or 4 years after start of production, amid intense competition and record high raw material costs. Over 31 new EVs are hitting the market in 2023 and another 18 launched in 2022 are going into full production. In the luxury EV sedan segment, there are 6 new models being launched in 2023 and 3 launched last year going into full production this year (the BMW i4 and i7, and Benz’s EQS).

Soaring Lithium Price Will Widen 2023 Losses

Lucid faces a potentially severe cost headwind from surging lithium prices. Assuming Lucid locked into long-term contracts with their battery suppliers (LG Energy Solution and Samsung SDI) 12 months before start of production in Q4 2021, the price of lithium in Q4 2020 was $7.30/Kg on average. The current price of lithium is 837% higher at $68.42/Kg.

These are important points to consider about Lucid’s cost situation amid this spike in the cost of lithium and pricing pressure from Tesla in the US:

Tesla Lowers Prices by 13% on its Model S, a Direct Competitor to Lucid: Lucid was forced to raise prices from 8% to 13% on its 4 variants of the Air in June 2022 due to rising raw material costs. Rivian raised their prices by 18% on average as well.

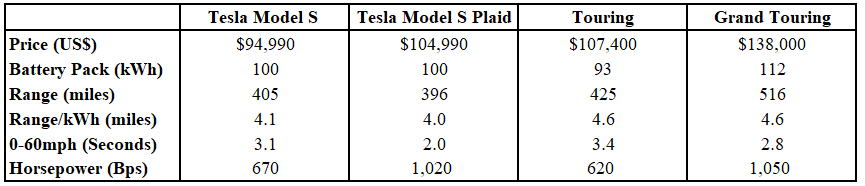

In early January, Tesla lowered the price of its lower-end Model S by 9.5% to $94,990 and its high-end Model S Plaid by 15.4% to $114,990, making them roughly 15% cheaper than Lucid’s Touring and Grand Touring models. While Lucid still has better range, battery efficiency and horsepower, Tesla has clearly put the squeeze on Lucid amid rising raw material costs.

Figure-6: Model S Prices Now are on Average 15% Lower than Lucid

Lucid Faces New Battery Contracts at Much Higher Rates in 2023: Lucid says their battery contracts with LG & Samsung are multi-year contracts with coverage “through 2022” (LG’s contract is reported to expire by 2023), so Lucid found another supplier in Q3 2022, but has yet to disclose the maker. This implies Lucid will be paying higher prices for battery cells in 2023 given the re-set in their contract prices. The lithium price has spiked by 836% since Lucid first signed their contracts with LG and Samsung SDI.

Lithium Price Spike and Tesla Pricing Pressure Implies Larger 2023 Losses: At the January 2020 price of $7.30/Kg for lithium when Lucid likely made its pricing agreements with LG and Samsung SDI, , Lucid’s cost just for battery cells were probably around $600 per vehicle. This has now spiked to $6,970 based on current lithium spot prices. The cell costs have essentially gone from 0.5% of the price of Lucid’s cars to 5.7%.

Current cell costs could be 8.2% of the Lucid Pure, the cheapest variant in Lucid’s line-up which management says makes up the majority of its order backlog. The Lucid Pure will likely see a price hike or lose more money than originally expected if Lucid eats the higher raw material costs.

The Problems With Saudi Arabia’s 64% Stake

Saudi Arabia’s Stake Poses Risks for Both Longs and Shorts: Saudi Arabia’s Public Investment Fund (PIF) owns 63.9% of Lucid’s shares outstanding, making Lucid’s free float only 30.4%. This presents a huge overhang for other Lucid shareholders, as any selling by PIF could cause huge downside in the share price (PIF’s stake amounts to 23 days of average daily trading volume in Lucid).

It also presents a problem for short-sellers, as the short interest in Lucid is high at 27% of the float as of January end. On a 30-day average trading volume basis, the short interest went from 5.5 days of volume at December end to 2.8 days at the end of January.

This is likely because Lucid saw a short squeeze on January 26th on rumors of PIF preparing to fully buy out Lucid. The stock surged by 43% that day and flushed out a lot of shorts. What’s more interesting is that January 26th was only 8 days after the 2-year lock-up period ended for Lucid’s SPAC sponsor, Chruchill Capital, which owns 2.98% of Lucid. There was no statement issued to confirm or deny the rumor, which is unbecoming of a listed company of Lucid’s size.

Saudi Arabia also wants Lucid to build cars at a new factory in King Abdullah Economic City at a cost of $3.4bn for the new plant, though Lucid will receive hefty subsidies for this. Plans are to start production in 2025 and reach 150,000 per year in output by 2027.

The problem is that Saudi Arabia has no parts supply network, so it makes little sense to produce cars there. This is why any cars produced in Saudi Arabia will likely be knock-down kits shipped from Lucid’s Arizona factory to be assembled in Saudi Arabia. The one advantage of having a plant outside of the US is that it allows Lucid to ship cars to China without getting hit by China’s punitive tariffs of 25% on cars imported from the US.

In an odd move—from the perspective of their 63.9% investment in Lucid—PIF recently took a $100m stake in an EV start-up called “Ceer”, which will also be producing EVs in Saudi Arabia. Ceer will have its EVs produced by Foxconn in 2025 with technology licensed from BMW.

Given Foxconn’s manufacturing prowess—it assembles all of Apple’s iPhones, as well as Fisker and Lordstown’s EVs—and BMW’s technology, Ceer could actually take share from Lucid. The first model will be an electric SUV and its launch timing coincides with Lucid’s plan to release its first SUV, the Gravity, in the 1H of 2024.

Earnings Outlook is Grim

Lucid’s Q4 2022 delivery numbers missed again, but by a wider margin than before. Deliveries of 1,932 units in Q4 were 52% below plans of 4,063 units, but the stock rose on the announcement most likely because full-year production of 7,180 units was above Lucid’s plans of 6,000 to 7,000 units. Obviously, no one buying the stock stopped to wonder what the excess inventory would do to free cash flow.

What the market didn’t digest is this: Lucid’s CEO stated on the Q3 2022 earnings call that they were “firmly producing 300 units/week exiting Q3”. However, the Q4 2022 production number of 3,493 equates to only 268/week, which points to some kind of production glitch again all those unsold vehicles are in transit.

2022 Results: Revenues for 2022 should come in at $598m versus consensus of $672m and GAAP net losses should be $1.5bn, which is in line with consensus.

Delivery Growth on Tesla’s Cadence Points to Lower Earnings than the Street: Using the same pace of delivery growth that Tesla had from 2012, Lucid should only see around 20,000 units in 2023 (Street is at 24,000) and 32,000 units in 2024 (Street is at 42,500). If Lucid tracks Tesla’s pace of ramp up, this should lead to revenues of only $4.5bn in 2026 versus consensus estimates of $12bn. Unlike the Street, it seems unlikely that Lucid becomes profitable in 2027. It took Tesla 8 years to become profitable with literally no competition. Consensus estimates believe it will only take Lucid 6 years with tons of competition on the horizon.

Lower Prices and Higher Costs in 2023: As raw materials like lithium spike intensely in 2023, Lucid should see its ASPs drop by at least 27% YoY, leading to higher gross losses. R&D should also weigh on earnings in 2023 as Lucid prepares for the launch of its Gravity SUV in 1H 2024 (Gravity was originally scheduled to go on sale in 2023). This could cause all sorts of problems for Lucid, as they try to ramp production of various versions of the Lucid Air to higher volumes, while rolling out a new model.

Non-Operating Income 1.8x Revenues in 2022 but Gone in 2023: One more important earnings factor for 2023 is the removal of gains booked at the non-operating income level in 2022, which should likely provide a $1.1bn gain versus only $598m in revenues. This is a non-cash line item based on Lucid’s share price: the lower Lucid’s stock goes, the higher this non-cash gain, as it’s based on warrant valuations from the SPAC merger. The valuation gains/losses in Q3 have come down to only 30% of what they were at the start of 2022.

Based on these assumptions, 2023 net losses should nearly triple to -$2.9bn, which is worse than consensus estimates of -$2.2bn. The Street seems to be tracking Lucid’s over-ambitious delivery estimates from the July 2021 presentation package, which have already proven to be woefully wrong.

Cash Burn Increases in 2023: Consensus estimates are quite dovish when it comes to Free Cash Flow, which should come to -$4.1bn in 2022 and -$6.9bn in 2023 (Street estimates are -$3.4bn in 2023 and -$2.8bn in 2023). Lucid should also see higher than expected capex in 2023 and 2024 as they slashed their 2022 spending from $2bn to $1.2bn and said that the $0.8bn would slide into 2023 and 2024.

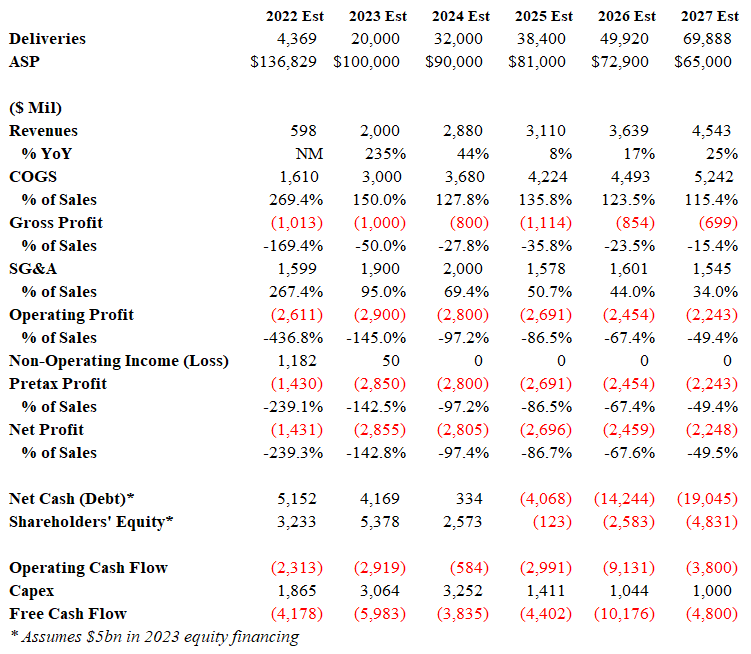

Figure-7: Lucid Earnings Estimates

Valuations—Lucid High Multiples are Second only to Tesla

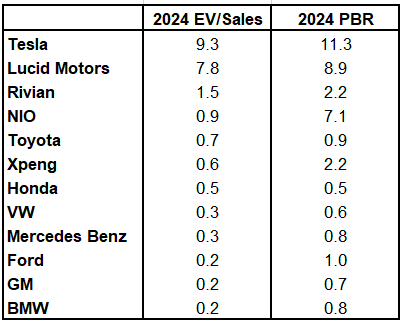

After Tesla, Lucid’s valuations are the highest in the auto industry (see Figure-8). What’s more is that Lucid’s 2023 estimated enterprise value of $22bn is more than twice that of Nissan’s and Subaru’s, 40% more than Renault’s and on par with Honda’s.

Figure-8: Lucid’s 2024 Valuations Versus Rivals

It’s highly doubtful the the Saudi Arabian sovereign wealth fund will buy out Lucid at these prices, especially after they just hedged their Lucid bet by investing in another EV start-up.