Tesla Facing Peak EV Adoption--Hybrid Market Share Growth Pushes Down EV Prices

Tesla Facing Peak EV Adoption--Hybrid Market Share Growth Pushes Down EV Prices

Spike in more affordable hybrid sales has eaten up the market share of battery electric vehicles globally

In just under two months, 5 major automotive companies have announced either delays or cancellations of EV investments amounting to over $30 billion. If money talks, then this is a loud cry that the 5-year-old EV boom may have peaked. And the monthly data shows continued deceleration in global EV sales growth through November. The CFO of the Mercedes-Benz Group recently stated what other auto executives were too scared to say about the EV market: “it’s a pretty brutal place…I can hardly imagine the current status quo is fully sustainable for everybody”.

Sales of battery electric vehicles (BEV) in the US surged by 50% YoY in Q3 2023, pushing their share of US car sales to a record high of 7.9%, up from 6.1% the previous year and only 2.1% in Q1 2021.

Despite such stellar growth—which had the subsidy tailwinds from the Inflation Reduction Act (IRA) behind them—there were some seismic shifts among carmakers that had announced bold electrification plans back in 2021.

In October, Tesla, GM, Ford and Honda, alone, delayed or canceled at least $26 billion worth of BEV investments in the US and Mexico due to lower than expected demand. Just yesterday, Panasonic canceled its plans for a battery cell plant in Oklahoma, which was said to have been a $4 billion project. That’s at least $30 billion of BEV capex wiped out in less than two months.

As of November, BEV inventory in the US has risen to 114 days of supply (link here) versus 71 days for the industry (60 days is ideal) and BEV incentives have spiked by 270% YoY to $4,660 per vehicle (link here), which is 85% above the industry average of $2,510 per vehicle.

What’s more is that hybrid electric vehicles (HEVs) and plug-in hybrids (PHEVs) are taking away market share from BEVs in every major car market of the world.

This report focuses on the following topics:

What kind of adjustments in BEV capex and profit outlook were made at major automakers.

Why this deceleration in BEV demand happened just as supply chain constraints eased up earlier this year.

How affordability seems to be the key factor behind hybrid electric vehicles (HEVs) taking away share from higher-priced BEVs (hence Tesla’s 20% drop in profits through Q3 2023).

The Autumn of BEV Discontent

GM scales back BEV output targets & delays new battery plants: In October, GM delayed the opening of its Orion electric pickup truck plant by one year to late 2025 in order “to better manage capital investments while aligning with evolving EV demand.” Guidance for 100,000 units of BEV production in the 2H of 2023 and 400,000 in 2024 was also removed due to growing uncertainty over demand (however, 2025 plans for 1 million BEV sales were maintained). GM also delayed the timelines on the opening of two new battery joint-ventures it had originally planned. In total, GM pushed out around $6.5 billion worth of capex ($4 billion in factory delays and $2.5 billion in canceling its joint-venture with Honda), explaining that it needs more flexible operations given the demand environment.

Ford cuts BEV plans while raising Hybrid outlook: Aside from delaying $12 billion (!) of BEV-related capex, Ford withdrew its 2023-end target of a 600,000 run rate in EV output and halved its 2024 production plans for the F-150 Lightning from 160,000 to 80,000. This comes after Ford announced in September that it would raise production of its V-6 hybrid F-150 output in 2024 to 20% of total production. “The customer is going to decide what the volumes are,” Ford’s CFO said on the Q3 earnings call. “Ford is able to balance production of gas, hybrid and electric vehicles to match the speed of EV adoption in a way that others can’t.” This is exactly what Toyota Motor has been saying since 2020 with regards to why they weren’t rushing the rollout of their own BEVs.

Tesla delays construction of its Mexico plant: On the Q3 earnings call in October, Elon Musk said that plans to build a next-generation EV factory in Mexico were on hold due to economic uncertainty and high interest rates. The initial phase was estimated to be around $5 billion of capex and would be the first plant to make Tesla’s “next-generation” car, with a platform so advanced that they could be profitable on selling a compact EV at $25,000.

Honda & GM canceled plans for joint BEV production: Honda and GM agreed to discontinue their BEV joint venture, which had aimed to sell millions of affordable BEVs worldwide from 2027. The project was said to be worth $5 billion. Both sides were said to have differing views on the timing of development in order to achieve profitability.

VW sees BEV orders halve in Europe & halts 4th battery plant: On VW’s Q3 2023 earnings call, the German carmaker said that its order backlog for BEVs were only 150,000, or half of the level it was a year ago. In November, VW’s CEO announced that there was no longer a need for a fourth battery plant, which was expected to be built in the Czech Republic.

Battery cell suppliers slash forecasts due to weak demand: Both LG Energy Solution (LGES) and Panasonic slashed their estimates for the rest of the year. Panasonic cut its cell production plans by 60% in Japan due to sagging demand for Tesla’s Model S & X, while LGES cut its Q4 2023 revenue growth forecasts from “double digits” to “single digits”. This is mainly due to weakness at its clients in the EU.

Panasonic cancels plans for a 30 GWh plant in Oklahoma: Despite having received $698 million of incentives to build a 30 GWh battery cell plan in Oklahoma, Panasonic turned down the opportunity. A 30 GWh cell plant is enough to supply enough cells for 400,000 to 450,000 BEVs per year, so this is a huge project that just got canceled. The Wall Street Journal cited higher than expected costs as the main reason, but it was more likely due to a large customer scaling back their EV expansion plans in the US.

All of these moves to reduce exposure to the BEV market proved to be prescient: BEV sales growth since then has largely decelerated, despite continued growth for other types of cars. Below are a few examples:

Germany and Norway see BEV sales plunge in November: BEV sales in Germany dropped by 23% YoY and Norway saw its sales plunge by 47% YoY. Combined, the two countries made up 42% of total Eurozone BEV sales in November 2022, but their weight dropped to 29% of total sales this November. Both markets saw a fallback from high levels this time last year due to expiring BEV incentives.

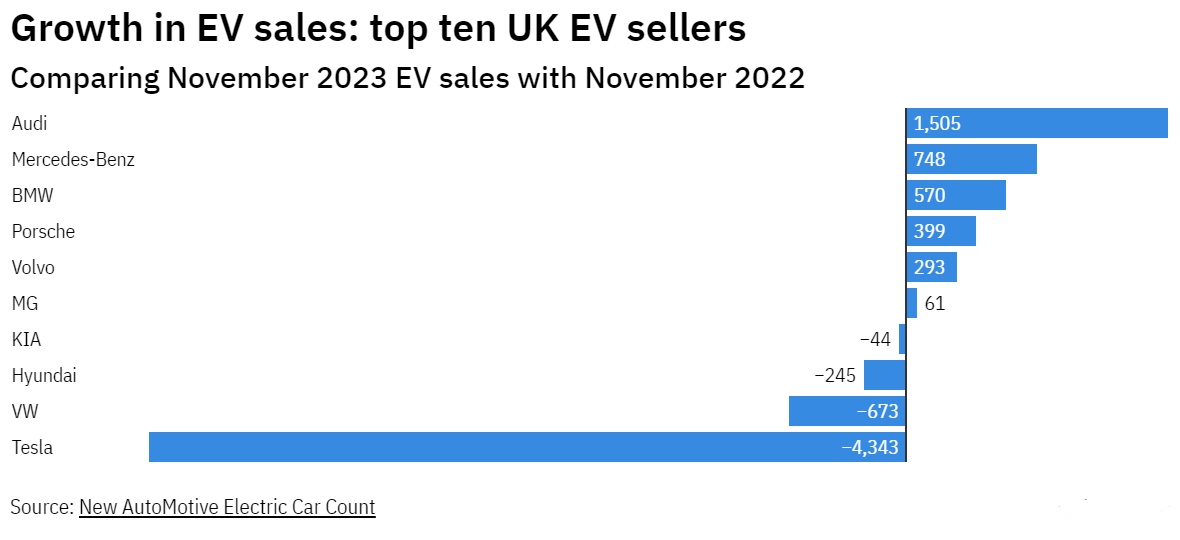

UK BEV sales fall by 17% YoY in November: While the hurdle was high based on strong sales in November 2022, the 17% decline in UK BEV sales was mainly led by a 73% YoY crash in Tesla sales (Tesla dropped by 4,343 units YoY while the entire UK market was down 5,013 units YoY; see figure 1 below). What’s more is that the UK has a zero-emission mandate that calls for 22% of all carmakers’ sales to be made up by BEVs next year. However, only 19 of the 27 carmakers currently have that much of their overall UK sales made up by BEVs. It will be interesting to see how the UK government deals with this issue if BEV demand continues to wane.

Figure 1

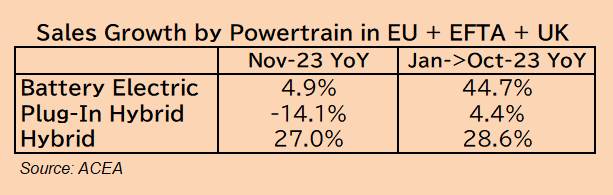

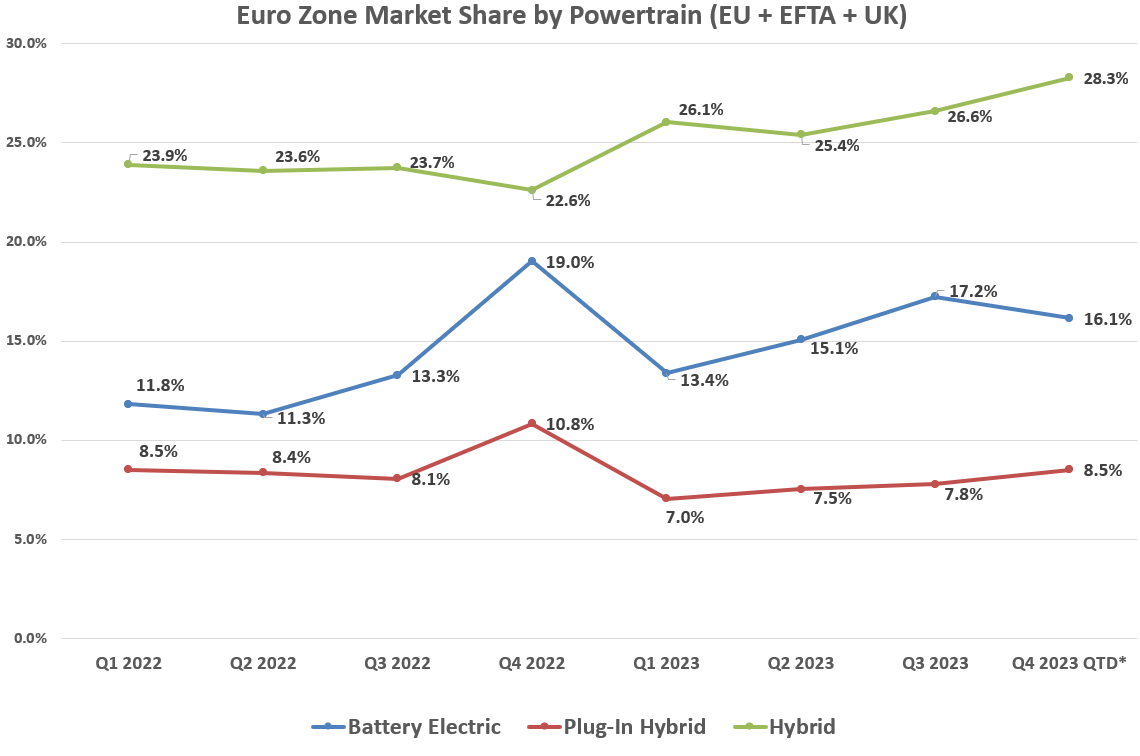

Eurozone sales of BEVs see massive deceleration in growth: While BEV sales in the Eurozone had been growing by 45% YoY through October, things appear to have stalled in November, with only 5% YoY growth. Hybrid vehicle sales clearly appear to be taking share away from BEVs, which points to affordability problems for BEVs (see Figure 2).

Figure 2

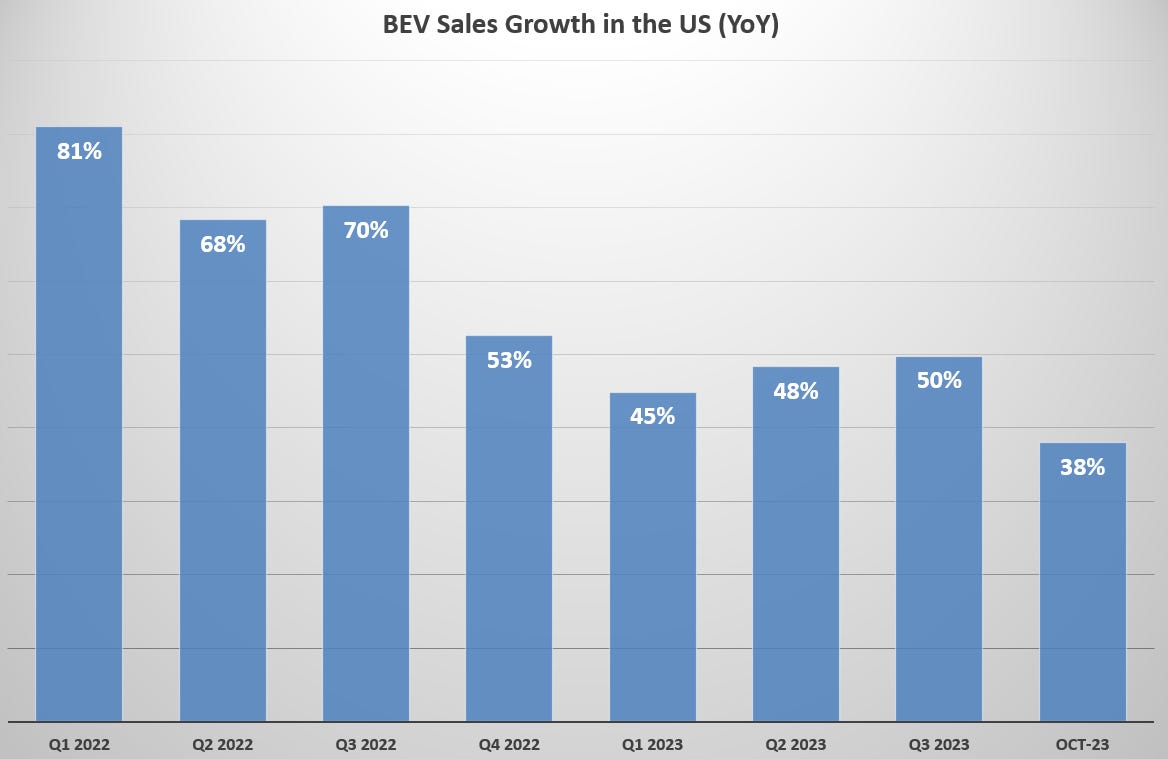

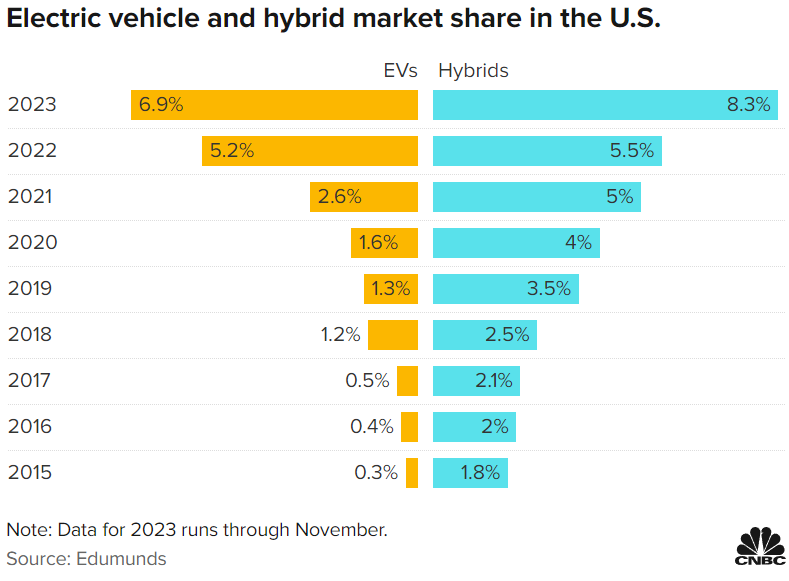

Young BEV market in the US is also seeing growth slow: While October BEV sales growth in the US was 38% YoY, this was much slower than the 50% quarterly growth seen in Q3 (see Figure 3). Also, there were some unsavory things happening behind the scenes: according to Cox Automotive, September BEV inventories were at 97 days’ supply versus the overall industry’s 57 days (60 days is ideal) and this grew to 114 days versus the industry’s 71 days by November.

Figure 3

Source: Cox Automotive for quarterly numbers & Experian for October

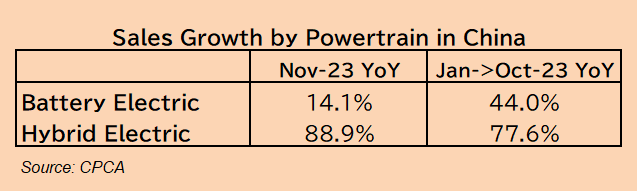

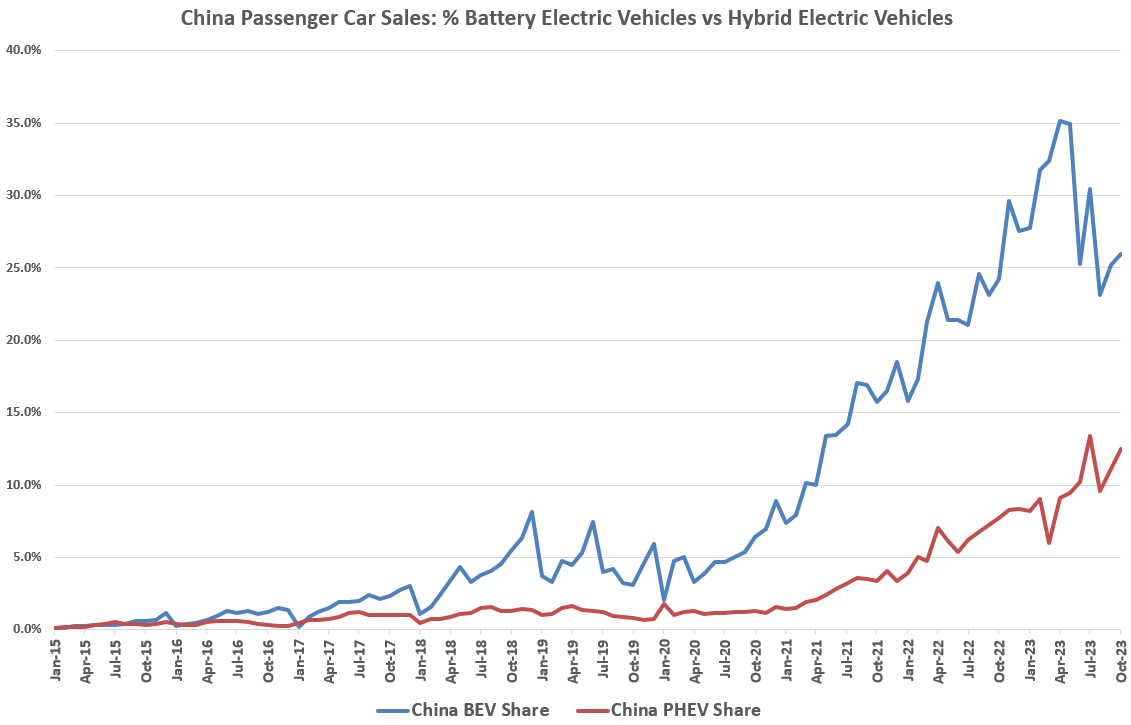

Pace of growth in China slows despite price cuts & incentives: Tesla launched a price war in China in December 2022 and it has only intensified ever since. The year-end promotions being offered now only make things worse, and despite this, BEV sales in November only grew by 14% YoY after seeing 44% YoY growth year to date through October. Note that HEVs are seeing sales surge as they’re 25% cheaper than BEVs (some HEVs are even being sold at a slight discount to gasoline vehicles). Given the economic malaise in China, it’s hard to see this improving in 2024.

Figure 4

Why BEV Demand is Stalling Now

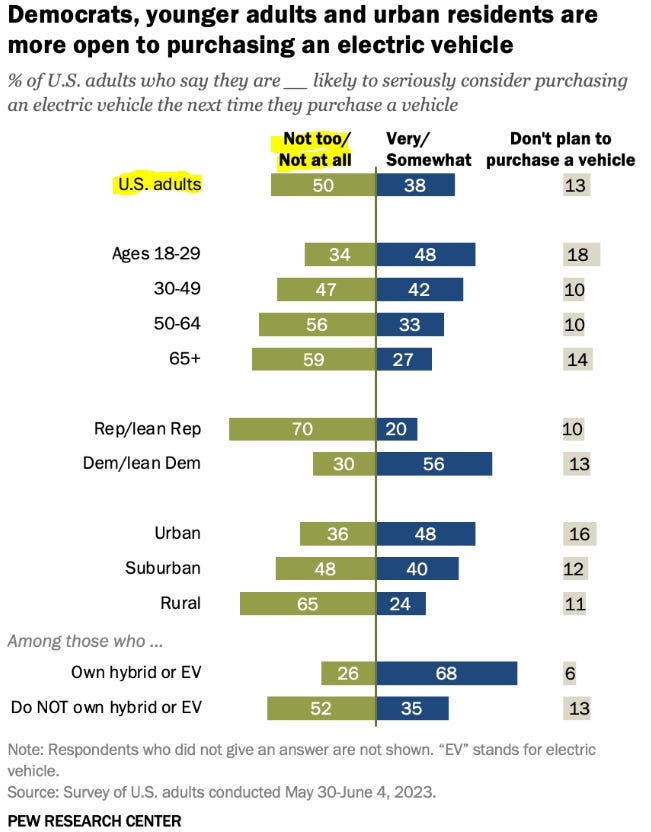

One of the more reasonable causes cited as to why BEV sales growth is waning is that those early adopters who wanted electric vehicles have all bought theirs by now. The rest of potential buyers are waiting on the sidelines.

Figure 5 below has results from a recent Pew Research Center poll which shows that 50% of Americans are either not too likely or not intending to buy a BEV. Also, note that those who are “very or somewhat likely” to buy a BEV dropped from 42% in 2022 to 38% this year.

Figure 5

But there are a few other reasons, which can be outlined as follows:

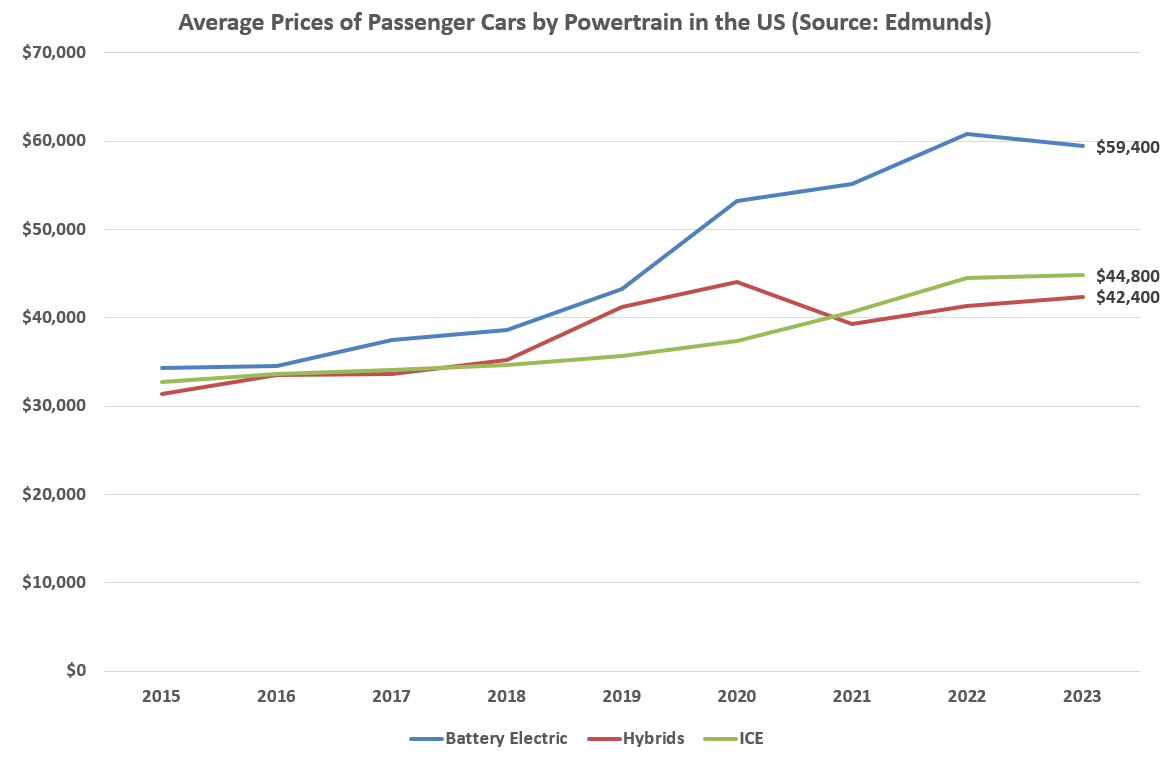

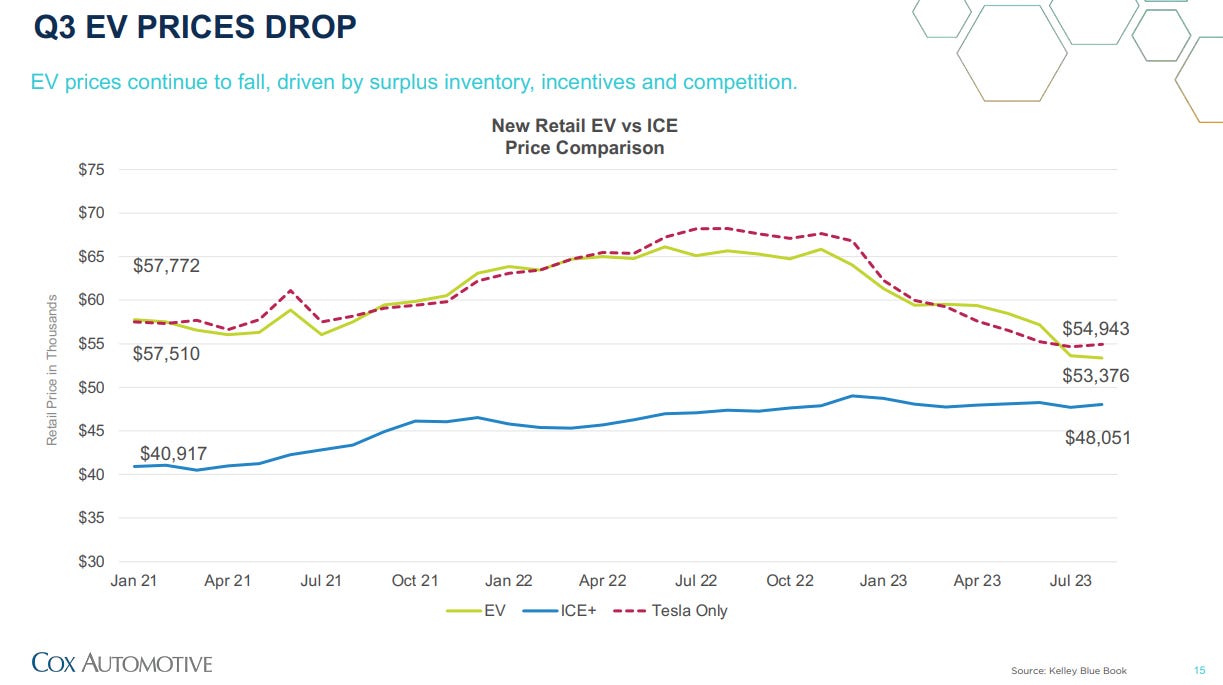

Affordability: Edmunds says that the average price of a BEV in the US is $59,400 as of November, or $17,000 (40.1%) more than a hybrid’s average price and $14,600 (32.6%) more than an ICE vehicle (see Figure 6). Cox Automotive data has slightly different data, saying the average BEV price of $53,345 was $4,098 (8.5%) more than the industry average of $48,247 (see Figure 6). Either way, BEVs are still out of reach for many car buyers, especially those who need financing. Based on the top-ten best selling models in the US and current prices, my estimate is that the average BEV costs around $50,000, or a 25% premium to the $40,000 price of non-electric cars.

Figure 6

Figure 7

Range anxiety is still a problem: Even on routes that have proper charging stations along the way, such as Phoenix to San Diego, the 5 hour 40 minute drive gets extended by nearly an hour to 6 hours 33 minutes, if all runs smoothly. More BEVs on the road is causing larger queues at charging stations these days and many chargers often don’t work (a common complaint among non-Tesla owners). Given the roughly $10,000 average premium in the price of a BEV versus other cars, this is a big inconvenience.

Much lower resale values for BEVs: As of October, a 3-year-old gasoline vehicle was said to hold on to 66% of its original value compared to 73% a year ago, as car prices have fallen. A BEV was found to only maintain 49% of its value compared to 70% in October 2022, as BEV prices have fallen faster than ICE vehicle prices. These are estimates by Black Book, a vehicle appraisal guide that bases its data on 60 used car auctions nationwide in the US. It is owned by Hearst Communications.

Sky-high repair costs are scaring many away: The battery pack of a BEV costs between $15,000 or $22,000 to replace, so if it’s damaged during an accident, the repair costs are so high that most insurance companies scrap the entire vehicle (hence the surging costs of insuring BEVs). Hertz recently paused its purchase of Teslas and other BEVs for its rental fleet, citing low resale values and high repair costs as the main reasons. German car rental giant, Sixt, recently made the same decision.

Hybrids Causing Pain for BEV Makers as Affordability Leads to Huge Market Share Gains

In every major market this year, hybrid electric vehicle (HEV) sales are outpacing growth of BEV sales. Toyota is the world’s largest hybrid maker, with a 59% share of the global market—most of it outside of China. Toyota could put further pressure on BEV sales next year as its HEV sales this year are constrained by battery supply issues (its global share was 79% last year).

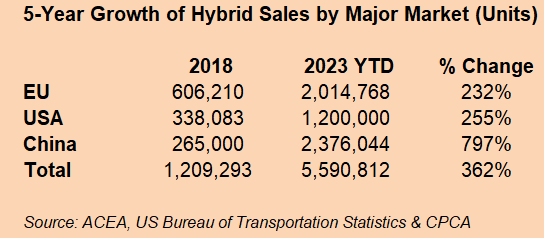

In the past five years, the growth of HEVs in the world’s major markets has been stunning (see Figure 8), with faster growth than BEV sales since 2022. This year, HEVs are outpacing BEV sales growth due to larger supply of cars and the continued affordability gap relative to BEVs (note the year-to-date market growth of HEVs versus BEVs in Figure 9).

Figure 8

Figure 9

Toyota rules the US Hybrid Market, but look out for Ford: Toyota is the main player in the US Hybrid market and, despite battery supply constraints this year, has already seen 25% YoY growth through November to 574,128 vehicles versus the overall market’s growth of 12% YoY to 1,200,000 units.

What’s interesting is Ford’s plans to quadruple their hybrid sales in 2024 after cutting their BEV forecasts. Ford said it plans for its V6 hybrid models to reach 20% of their truck sales in 2024 from only 7% this year (link here). Ford’s hybrid sales have grown faster than its BEV sales this year and are double its BEV sales in terms of volume: hybrids are up 23% YoY to 121,000 vehicles through November at Ford, while BEVs are up only 16% to 62,500 units. Figure 10 shows just how much hybrid sales have outpaced BEVs in the US for the past 8 years. With higher capacity in 2024 at Toyota, this could put much more pressure on BEV prices and volumes.

Figure 10

Europe: Tesla is definitely feeling the heat from hybrid growth: As can be seen in Figure 11, hybrid vehicles like the Toyota Prius are eating away from BEV makers’ market share in the EU.

And while Tesla has grown its sales by 84% year to date through November (versus the 28% growth in hybrid sales), its sales have only grown by 12% in the last 3 months (September through November) versus a surge in hybrid sales by 30% during the same period, most likely due to higher sales by Toyota.

Toyota has a 23% share of the EU hybrid market and is battery supply-constrained this year. Management said on their last earnings call that battery supply is normalizing as of Q4, so 2024 should see higher growth of their hybrid sales. At 23% in fiscal 2022, the EU was Toyota’s largest market for hybrids. This could put further pressure not only on Tesla, but other carmakers highly exposed to the BEV market in the EU like the VW Group, BMW and Benz. It also could throw a spanner into the Chinese makers’ plans to export their excess BEV capacity to the EU, as they’ve been doing this year.

Figure 11

Source: ACEA. * Q4 2023 is data through November.

China’s hybrid market is different: PHEVs & EREVs are crushing BEVs: In China, HEVs mainly consist of plug-in hybrids (PHEVs) and extended-range hybrids (EREV). PHEVs are gasoline cars with a small battery pack that can get around 45 miles (72 km) of range, or enough for trips around town with a gasoline engine for back up when the battery runs out. EREVs run mainly on a larger battery pack, but have a small gasoline engine to regenerate the batteries when they run low.

EREVs are the fastest growing segment of China’s hybrid market, led by Li Auto which has a 14% market share. HEVs in China are 25% cheaper than BEVs on average and receive the same benefits of not owning a gas-only car in China: easy access to license plates (which can take years to receive or cost huge sums of money for gas-only cars) and the freedom to drive anywhere (some provinces bar gas-only cars from out of town and/or forbid them from entering business districts).

As is clear in Figure 12, China’s HEV segment is near its all-time high share of the passenger car market, whereas BEVs peaked out at 35% last summer and seem to be drifting lower. Hence the intense price war in China’s BEV market and the boon for all carmakers in China with high exposure to hybrids, like Li Auto.

Figure 12

Source: CPCA

Closing thoughts: Battery electric may have been a bad idea; Tesla & Others Face Huge Risks

I’m not a tree hugger or get support from Big Oil or carmakers like Toyota. I do believe that we need to reduce carbon emissions henceforth, but not by using taxpayers’ money to fund the sales of expensive BEVs, which spew out much more carbon dioxide in their production process than gasoline cars do.

Toyota says it can produce eight 40-mile plug-in hybrids for every one 320-mile battery electric vehicle and save up to eight times the carbon emitted into the atmosphere.

Until there’s a technological breakthrough that makes BEVs cheaper and drive at least 625 miles (1,000 km) on a 10-minute charge, BEV adoption will remain at recent levels: 8-10% of the US market; 15%-20% of the EU and 30%-35% of China’s market.

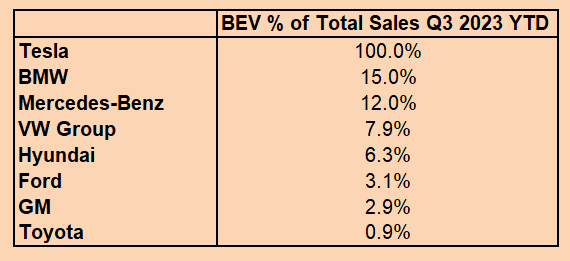

In light of this, highly valued EV stocks like Tesla and more recent EV startups like NIO, Xpeng, Lucid and Rivian may face liquidity risks from 2024. Figure 13 shows the percentage of BEV sales among the big carmakers, but the higher the exposure is not necessarily a sign of worse for earnings. The key is which of the carmakers below face more downside from their investments in BEV capacity. In that sense, the main victims could be Tesla, VW, GM, Ford & Mercedes-Benz (in that order). All have recently seen unexpected earnings downside from lackluster demand for their BEV line-ups. And 2024 could see the beginning of at least a lull in BEV demand.

Figure 13

This is not investment advice. It’s simply an Op-Ed on auto industry trends. Thanks for reading my automotive drabble all year and Happy holidays!

Does TM actually sell BEVs? I saw some controversy over what they call BEVs.

Hybrids are a way of green washing ICE vehicles to make owners feel better about taking carbon sequestered hundreds of millions of years ago and putting it in our skies to greenhouse us.

This article, if true, gives a shameful view of humanity in the recent quarters as people have relaxed and taken their eyes off climate change. 2024 will be a year where consumers remember what we are fighting against and flock to BEVs and Tesla solar.