Tesla Q4 2023 Preview: Nobody Cares--Show Me the Guidance

Tesla Q4 2023 Preview: Nobody Cares--Show Me the Guidance

Beware of a relief rally if guidance is in line or "credibly" bullish

The first section below is an outlook for 2024 and how Tesla might guide for it on its earnings call this Wednesday after market close.

After that is a detailed explanation of the assumptions behind my Q4 2023 earnings estimates.

Final thoughts at the end are how I plan to trade Tesla into this turbulent event (not investment advice).

Tesla should see Q4 2023 adjusted EPS of $0.66, which is 11% below consensus estimates of $0.73. Automotive gross margin (excluding regulatory credits) is the key performance metric for Tesla and my estimates of 15.8% are also below consensus estimates of 17.0%. That being said, I have no short position in Tesla ahead of this Wednesday’s earnings call due mainly to technical reasons:

Tesla is down 20.1% in the past 17 trading sessions since December 27th (when it hit a near-term high), while the Magnificent 7 (ex-Tesla) are up by 6.5% on average. Tesla appears to be decoupling from the “Mag-7”—which is a positive sign, given Tesla is just a carmaker—but I’m not quite ready to bet this trend “has legs”.

Figure 1 shows that Tesla only recently began to underperform the Mag-7 and how long bears like me were proven wrong by not having gone with the flow (yet again). But if you’d stuck to your guns and shorted Tesla while being long tech, the returns could’ve been around 35%—only as of the last 3+ weeks.

Figure 1: Tesla Decoupled from the Magnificent-7 on January 3rd

Source: Bloomberg

The main oscillators like RSI and MACD are flashing “oversold”. RSI doesn’t tend to stay at these low levels for long unless the market crashes or Musk decides to not give 2024 guidance (which is not out of the question, in my opinion). Barring that, however, the stock is pretty oversold at these levels and could pop on a “less bad than anticipated” event on Wednesday or drop not as much as the usual 10%-13% on bad results up to now (Q1-Q3 2023 results all saw 10% drops the following day, which were dip-buying opportunities).

Figure 2: Technicals Show Tesla Being Short-Term Oversold

Source: Bloomberg

Any Relief Rally Should Be Short-Lived

Aside from Tesla facing its first earnings decline since becoming profitable in 2020, the following issues will continue to weigh on the stock:

Musk is now a real liability to Tesla shareholders: After he publicly tweeted that he might take Tesla’s AI/Robotics business elsewhere if he wasn’t granted a 25% stake in Tesla (i.e. pay me $60 billion-plus more to stay, or I leave with the “crown jewels”), Tesla shareholders face two prospects: (1) dilution of 10%+ in the future if he gets his bonus award; or (2) a crash in Tesla’s share price if Musk quits Tesla and sells his shares while trying to ramp up, xAI, his “AI” start-up.

No stop to price cuts: In the last 10 days, Tesla has cut prices in China and the EU by around 6%, as well as introducing costly 0% interest rate loans in the US as a “stealth” price cut. In the past 12 months, it was the first official price cut in China, the 3rd cut in the EU, and the 5th cut in the US. I’ve said this ad nauseam, but even some Tesla bulls are opening their eyes: old models stop selling unless fully made over. And, Tesla has no plans for full model changes of the Models 3 and Y, which made up 96% of global deliveries in 2023. Tesla either continues to slash prices and sell below cost, or idle capacity to maintain prices. Both will burn cash. I wrote about it in May regarding Model Y excess capacity (here) and again in June related to China’s need to be propped up due to excess Model Y capacity, globally (here).

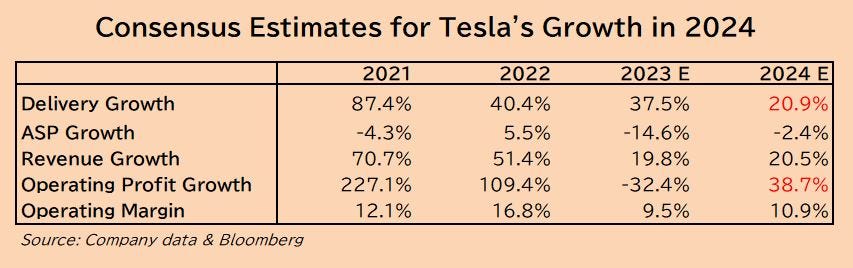

How out of tune consensus still is with reality: Many Tesla bulls have predicted a “bottoming out” of gross margins in 2024 due to an end to the incessant price cuts of 2023. Figure 3 shows consensus estimates of growth in volumes, prices, profits, and margins in 2023 and 2024 versus 2021 and 2022. Note the huge slowdown in volume growth, yet a spike in 2024 estimates for revenues and operating profit growth. Finally, note in Figure 4 how a well-informed Tesla bull admits he didn’t expect Tesla to underperform “legacy carmakers” like Toyota due to further price cuts at Tesla in the past few weeks.

Figure 3: Tesla 2024 Consensus Growth is Unrealistic

Figure 4: Tesla Bull Who Thought Price Cuts Would End Last Year

Beware of Musk pumps on the call and accounting tricks: This time last year, Musk proclaimed that orders exceeded output by two times after Tesla’s 20% price cuts in early January. That pumped the stock 34% in less than 3 weeks, albeit in a rallying tech market. The stakes are even higher now, given Musk’s blackmailing Tesla’s Board to grant him a $60 billion-plus bonus, so it would not be surprising to see some unusual lumpiness in Q4 profits.

Note that Q1 seasonality could lead to cash burn this time: Two surprising things about 2023: (1) how Tesla managed to avoid cash burn despite huge price cuts and fixed cost burdens from their 2 new plants; and (2) how consensus repeatedly overestimated Tesla’s shrunken free-cash flow (FCF) each quarter. Given the removal of subsidies in the EU and the US, as well as the slow seasonality of Q1 each year, it would not be shocking to see negative FCF in Q1 of this year. That’s a decent catalyst in just 3 months from now and would likely shock the fanbase, who up to now, thought that Tesla is the richest carmaker in the world.

2024 Guidance is a crapshoot (also the new CFO isn’t as smooth): If Tesla guides for 2024 deliveries of around 2 million units (consensus is at 2.2 million), the stock might fall but should have a relief rally. Morgan Stanley and Barclays came out with bearish previews implying that Tesla might have to bite the bullet and guide conservatively (lol emoji here). Given that Musk is angling for another $60 billion-plus bonus, I’ll bet that he pumps the stock as much as he can, including the Auto business. My only concern is the new CFO, who probably means well, but had a bad debut on Tesla’s Q3 2023 earnings call last October. Hopefully he’s brushed up on his presentation skills.

Assumptions for $0.66 in Q4 2023 Adj-EPS

The main drivers of my model are average selling prices (ASPs) and cost of goods sold (COGS) per unit. This may seem oversimplified but is actually the most reliable way (for me) to estimate Tesla’s earnings, given their poor disclosure of vehicle sales and earnings by region, as well as positive and negative profit factors which all other carmakers disclose.

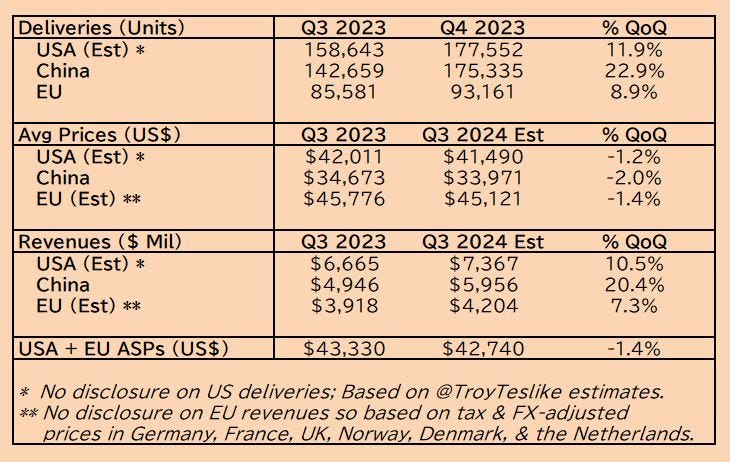

Figure 5 shows my assumptions for ASPs by major region. This is the basis for my ASP estimates for China (which can be calculated based on Tesla disclosures) and “Non-China” which is basically the rest of the world, not disclosed by Tesla on an automotive basis.

US deliveries are estimates because Tesla doesn’t disclose them. They’re based on TroyTeslike’s delivery estimates for Q3 and Q4 2023, as well as price changes at Tesla on its US website.

China deliveries and revenues are actual results from Q3 and estimates based on that for Q4. Tesla has to disclose delivery and revenue data from China, given its large share of Tesla’s earnings.

EU deliveries are public information, but pricing is tricky to track given all the countries in the EU + EFTA + UK. I was only able to find price change data from 6 countries in 2023, highlighted by the ** double asterisk below. Those 6 countries are a good sample and made up 65.8% of Q4 total EU + EFTA + UK deliveries.

Figure 5: Pricing by Region at a Carmaker in Need of Price Cuts

With all of the above, I have global ASPs down 2.8% QoQ to $43,049, which is 2.6% below consensus estimates of $44,205. Please note that there were “new car inventory” offers going on at 10% discounts during Q4, but it’s hard to tell what percentage of global sales they made up. Hence my estimates are conservative on the pricing front, i.e. Q4 ASPs could fall much more than my assumption of -2.8% QoQ.

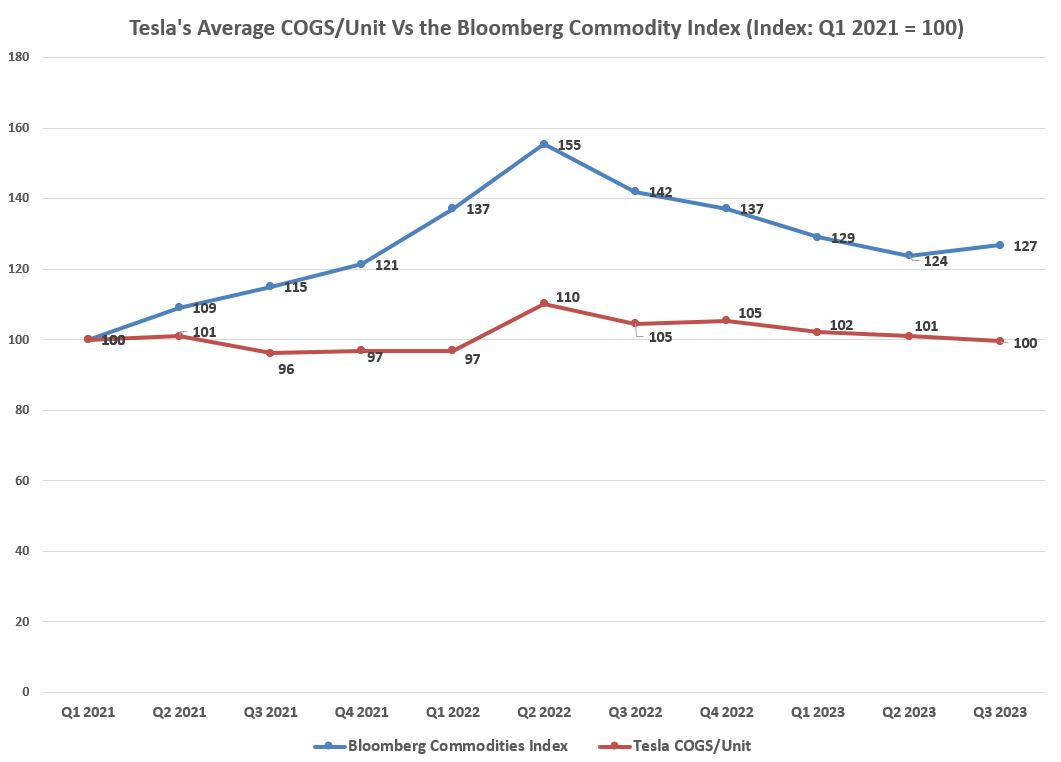

COGS/unit is always a shot in the dark and all I can use here is a basket of commodities that Tesla may or may not buy at spot prices, along with an eye on the lithium and nickel prices which are mostly on a contract basis. The lithium hydroxide (South Korea) price in Q4 has dropped by 59% QoQ and the nickel spot price has dropped by 15% QoQ. These two materials make up a significant portion of the cost of a battery pack.

The lithium content for a Model Y battery pack, alone, has cost as much as $5,046 per car in Q4 2022 based on the spot prices back then. Currently, this has come down to around $900 per Model Y if Tesla were buying at spot prices.

Tesla has said on many quarterly earnings calls—while the lithium price was dropping—that they have little exposure to the spot market, but capitalize where they can (I saw no evidence of dramatically lower lithium prices leading to lower COGS/unit during 2022 and 2023, as Tesla is locked into long-term contracts set at prices similar to current levels). Other commodities that Tesla has to buy in the spot market are charted below in Figure 6, which is the Bloomberg Commodity Index versus Tesla’s Automotive COGS/unit (ex-leases). It looks like Tesla’s costs/unit have withstood a big rise in commodity prices over the past 3 years.

With my thumb in the air, I take down Q4 2023 COGS/unit by 1.5% (compared to -1.4% QoQ in Q3 2023) despite a 14% QoQ rise in volumes in Q4 for the following reasons:

Newly launched Cybertruck and refreshed Model 3 start-up costs should weigh on earnings due to start-up costs and expensing new equipment (although, this is Tesla so it may not hit earnings yet).

“Fixed cost absorption” at the struggling new plants in Austin and Grünheide doesn’t seem to have made much progress in Q4 2023. Capacity utilization at Austin rose from 30% in Q3 to 37% in Q4 according to TroyTeslike’s output estimates (and my estimates of 50,000 units of Cybertruck capacity having come online in Austin). Grünheide fell from 48% in Q3 to 41% in Q4. On a combined basis, both plants saw capacity utilization grow from 35.4% in Q3 to only 36.6% in Q4—an improvement that is likely diluted by Cybertruck start-up costs in Austin and idled production in Grünheide in December.

Much of the mix in Q4 2023 was either low-priced sales in China or Model 3 sales in the EU. This is what is clear when calculating volumes by price according to Q4 deliveries by model in each region.

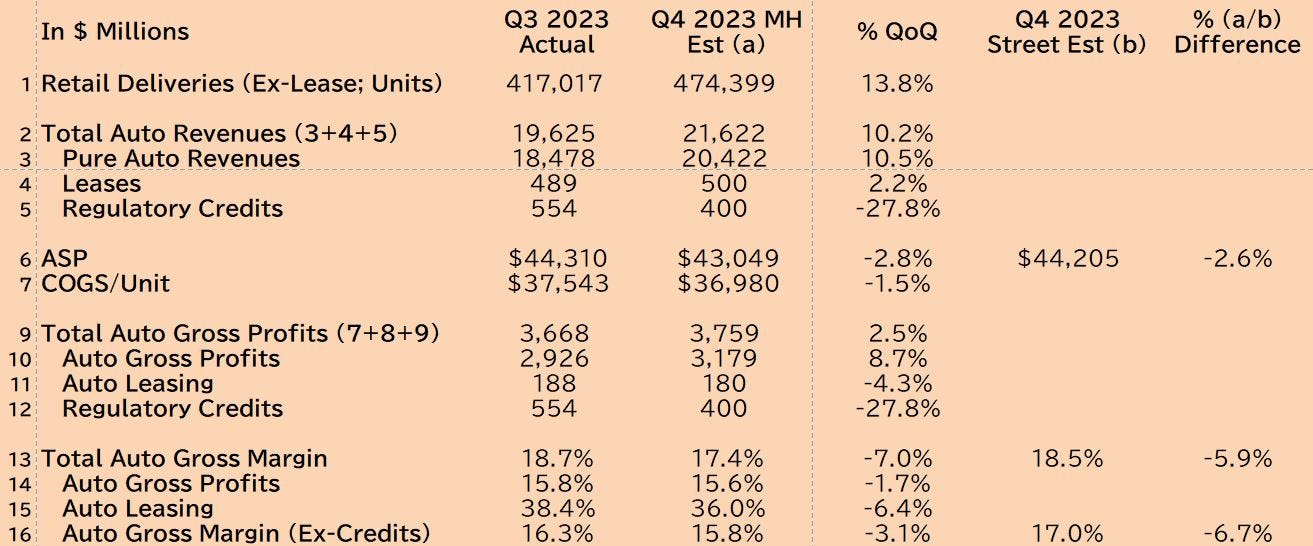

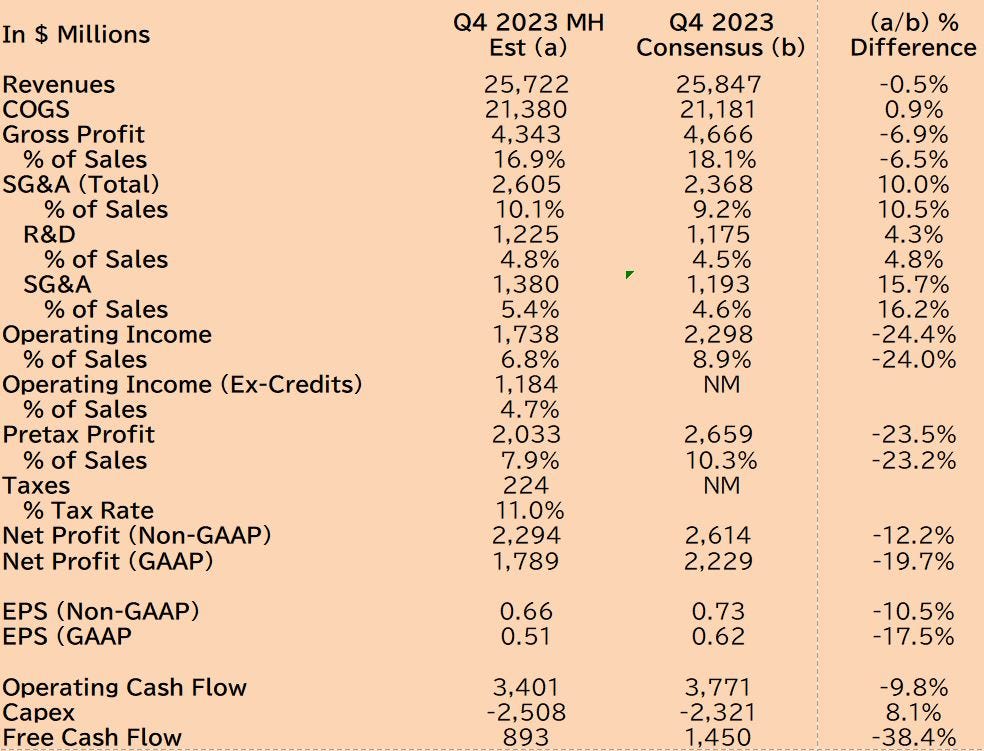

With the above ASP and COGS/unit estimates, the Auto division margins are shown in Figure 7 and the overall P&L is displayed in Figure 8 with comparisons to consensus.

Once again, this time I don’t expect Q4’s results to be that much of a catalyst unless something like the booking of huge regulatory credits pumps EPS up way above consensus, but once stripped out, reveals a large undershoot.

Figure 6: Tesla’s Automotive COGS/Unit vs Commodities

Figure 7: Tesla Q4 Automotive Estimates vs Consensus

Source: Company data & Bloomberg

Figure 8: Tesla Q4 Earnings Estimates vs Consensus

Source: Company data & Bloomberg

Final Thoughts—Sell Into Strength

Tesla is finally being treated like the outcast that it should be among various indexes due to its deteriorating profit margins and decrepit CEO. And yet, its market cap of $664 billion is still over twice that of Toyota’s, which generates double the pretax margins of Tesla and sells 11x Tesla’s annual deliveries.

That being said, I anticipate a short-term relief rally if nothing too untoward is said by Musk on this Wednesday’s earnings call and Q4 results don’t miss more than 15%.

Signs of being oversold somewhat resemble those that flashed in my face in December 2022, when Tesla traded down to $101: the fanboys were at each others’ necks, admitting they were wrong for not having sold a year earlier, while the bears were becoming increasingly vocal by the day (yours truly, included).

This is why I’ll definitely not be short Tesla into the Q4 earnings call. I’ve bought a very tiny position of calls to play the bounce and I may add if Wednesday’s earnings call is positive.

But this is strictly a tactical trade. If anything, my long-term view on Tesla has only become more bearish in the past few weeks in light of Musk’s blackmailing of Tesla’s Board and further price cuts around the world in such a short time frame.

My current 2024 estimates can be summarized as follows (and subject to change after Tesla’s Q4 2023 10-K is released):

1,768,938 deliveries (-2.2% YoY & -19.1% below consensus of 2.187 million).

Gross margin (ex-credits) of 11.7% versus consensus of 18.1% and 17.3% in 2023.

Operating margin of 2.7% versus consensus of 10.7%

Non-GAAP EPS of $1.29 versus $3.80 for consensus

GAAP EPS of $0.72 versus $3.37 for consensus

FCF of -$4.68 billion versus (positive) $8.18 billion for consensus

ROE of only 4.5% versus consensus estimates of 20.3% in 2024.

Using the average of my estimates and that of consensus, Tesla is currently trading at a 2024 PER of 82x and a PBR of 11x. Musk claims that Tesla is an “AI/robotics” company, but it has never disclosed any numbers to back that up. Seeing how badly made Tesla’s cars are, I call “bullshit”. It’s just a pump like their “Full Self-Driving” (FSD) technology has been and it’s no wonder that the Department of Justice has subpoenaed information about FSD.

The car market is turning stale due to problems with affordability. Battery electric vehicle sales were down 25% YoY in the EU last month despite strict mandates for EV adoption. Similar trends are emerging in the US. Hybrid vehicles are growing faster than BEVs and ICE vehicles in China, the EU, and the US. Coincidentally, my favorite pairs trade in this environment is long Toyota and short Tesla, a report on which will be out after results season.

Thanks for reading this far and remember that the above is in no way investment advice.

The Q4 increase in production should reduce COGS per unit by spreading the fixed costs over a larger base. That will probably be enough to offset the lower ASPs and keep gross margins flat.

But Q4 gets a full audit, and there is one component that I think deserves some scrutiny. The potential write down in value of the used car inventory and the effect of lower used car prices on lease returns and resale value guarantees.

Brad, since Musk is hijacking the board on additional comp, wouldn't he try to bring the stock down as much as possible instead of pumping auto business? Can you talk a little bit more about it?

I was thinking that his future comp would be based on the baseline market cap at the time he negotiates vs 5 years out or 10 years out target market cap