VinFast May Drop Fast

VinFast May Drop Fast

No other carmaker has started up with a bigger "thud" before in history. Fair value may be 95% lower at $2.50

Move Fast and Fall Over

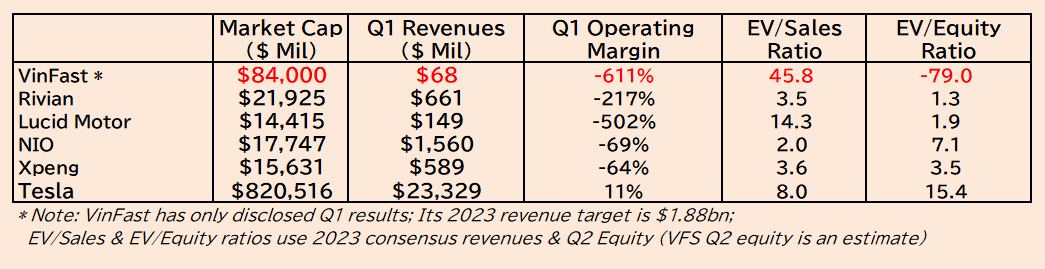

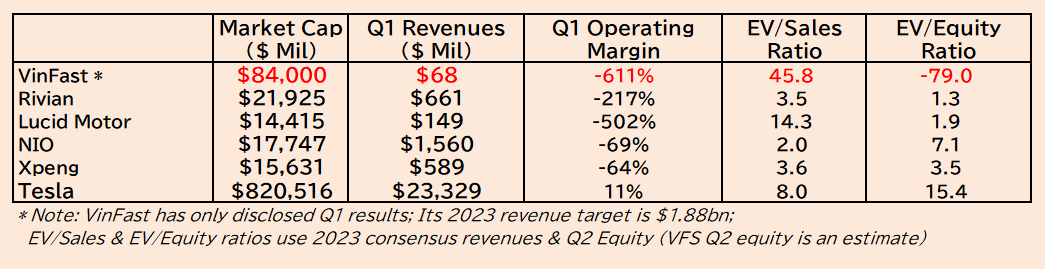

Before I get into what farcical operation VinFast is as an automaker, a gentle reminder about its gargantuan valuation (see Figure-1). At its current market cap of $84 billion, VinFast is now the world’s fourth most highly valued carmaker after Tesla, Toyota and BYD. This is despite the automotive press having skewered VinFast’s flagship model (the VF 8) for quality issues and the fact that it has only shipped 11,300 vehicles in 1H 2023 (Tesla had 881,015 deliveries, Toyota was at 4.67 million and BYD at 1.26 million).

Aside from having such bloated valuations for such low levels of sales, VinFast also sports the largest losses per unit, as is evident from its massive -611% operating loss margin in Q1 (VinFast has yet to disclose its Q2 financials). The average price of VinFast’s cars sold during Q1 was $32,422, while the cost per unit came to a whopping $117,082. This doesn’t include Research & Development expenses, which are booked at SG&A.

Figure-1: Valuations & Margins Among Major EV Start-Ups

Founder Has Pumped Over $9 Billion into VinFast

VinFast is 99.7% owned by Vietnamese entrepreneur Pham Nhat Vuong, who founded Vingroup, a $9.8 billion listed company in Vietnam specializing in real estate development, resorts and education. VinFast was spun out of Vingroup, which ventured into vehicle manufacturing in 2017 and scrapped all of its petrol products for EVs in 2021.

Much of VinFast’s $2.5 billion of net debt is tied to both Vuong and Vingroup affiliated companies. In total since 2017, Vuong and Vingroup have invested over $9 billion to get VinFast rolling. The start-up EV maker will need another $4 billion to complete its new factory in North Carolina, which just broke ground for 150,000 units of annual capacity in 2025 for Phase 1 and double thereafter.

Both VinFast’s CEO and CFO are on the record as saying they hope to capitalize on VinFast’s lofty valuation by raising money within the next six months. Given VinFast’s $84 billion market cap (25% higher than VW, the world’s number two volume car producer), I imagine they’re racing to launch an equity offering as soon as possible.

When top management enthusiastically advertises its intent to finance, the stock would normally drop. But in VinFast’s case, they have one of the smallest floats in the stock market: only 0.31% of its shares outstanding trade publicly. And VinFast is a meme stock now (also with options available as of this week), so management should definitely be lining up an offering.

Small Float of 0.31% Due to Lack of Demand at the Time of Listing

The SPAC merger that allowed VinFast to list in the US was valued at $23 billion, which was 23% higher than the market cap of Rivian, a blue-chip EV start-up backed by Amazon. This caused investors’ jaws to drop and 92% of them sold into the listing. Bloomberg’s Chris Bryant wrote a brilliant piece about the deal and how it required additional capital from the SPAC sponsor, Black Spade Acquisition Co., in order to execute the merger (here).

Incidentally, Black Spade Acquisition Co. is run by Lawrence Ho, a Macau casino resort magnate and son of the late Stanley Ho, aka “The Godfather of Gambling” who had a monopoly on Macau’s gaming industry for 40 years.

Why was an IPO Switched to a SPAC Merger?

It should be noted that VinFast was being advised by some large investment banks on going public via an IPO this year and, in preparation for this, VinFast filed an F-1 with the SEC on December 6, 2022. However, on May 12, 2023, VinFast suddenly announced that they’re listing via a SPAC merger with Black Spade Acquisition Co. No reason was given for the F-1 withdrawal, but there were probably issues of disclosure that Vingroup didn’t like or the due-diligence process was simply too long for them.

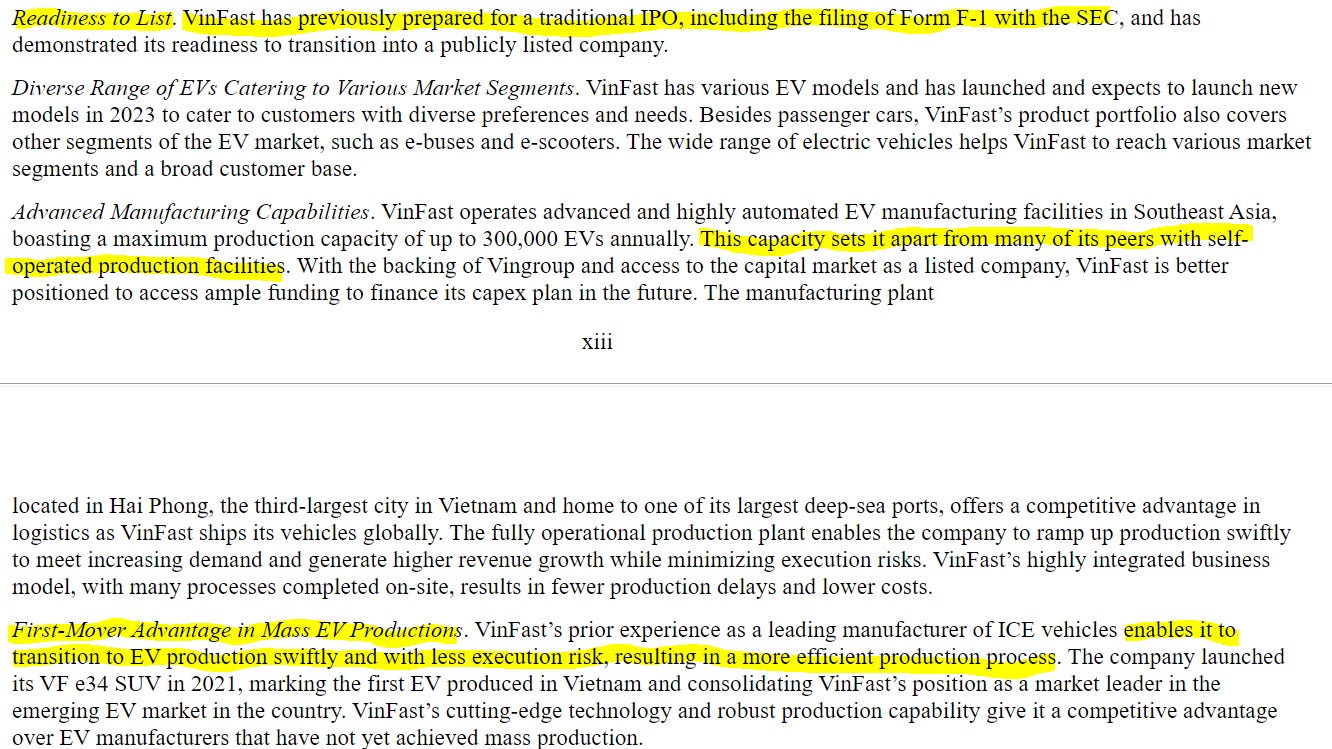

The fact is that VinFast’s founder gunned for the public markets as of May. Figure-2 shows a snippet from that announcement with regards to why a SPAC for VinFast made sense. I’ve highlighted sections of it that didn’t age too well, given VinFast’s current situation.

Figure-2: Reasons Given by VinFast for Being “SPAC-Worthy”

VinFast’s Mistake: Moving Fast & Breaking Yourself

VinFast’s debut in the US was the most disastrous launch of a flagship car in recent automotive history. The carmaker had only been producing cars since 2017, switched over from petrol cars to EVs in 2021 and launched their flagship VF 8 model in the US last year.

Much of their technology has been licensed out from GM and BMW, and they even spent lavishly on design by hiring the highly revered (expensive) Pininfarina, which does a lot of work for Ferrari and other sports car makers.

The problem is that VinFast simply moved too quickly and obviously skipped normal validation procedures used by established carmakers. VinFast is essentially selling cars that should still be in R&D stage while letting the customers find various glitches instead of finding these problems by normal validation procedures on VinFast’s own R&D expense.

It’s also obvious that VinFast thought that what they did in Vietnam would fly in the US as well. This was a fatal misjudgement by “moving too fast”. Hyundai had a fraction of the quality issues in the 20 years it took to establish its brand in the US compared to all the complaints VinFast has received in its first 8 months in America (see below).

The key points about why VinFast is doomed until it can repair its badly damaged brand image in the US are as follows:

Figure-3: VinFast’s Flop in the US: The VF 8 SUV

More Quality Issues than the Average Tesla: The automotive journalists who tested the VF 8 ridiculed VinFast over quality issues ranging from huge interior panel gaps, bad turn signal, too many chimes, bad ride quality, horrible driver-assist system, etc. (this is a must-see 14-minute YouTube video for more details).

So Many Complaints that VinFast Offers Cash Rebates by Category: With the deluge of complaints from customers, VinFast tried to quell the situation by offering cash back, depending on the problem, including $300 if your “vehicle is inoperable”. This program started in June both in Vietnam (where VinFast sells the bulk of its cars at the moment) and also in the US. The below screenshot shows the policies at the time, but it’s no longer on their website, so they either ran out of cash or fixed the quality issues. Good article on this from InsideEVs here.

Order Backlog Nearly Halved in 6 Months: VinFast’s parent company, Vingroup, published that VinFast had an order backlog of 70,000 cars at the end of December 2022 (before VinFast entered a SPAC deal). In VinFast’s latest presentation materials, that backlog is down to 26,000 as of June 2023. If VinFast had sold 44,000 vehicles in 1H 2023, this would be great news. But VinFast only had 11,300 deliveries in 1H 2023, which means that 32,700 (47%) orders were canceled.

VinFast Now Asking US Dealers to Sell its Cars: While VinFast was following the direct sales to customers method that Tesla and other EV start-ups are using, it recently approached various US dealerships to see if they could sell VinFast SUVs. Naturally, this was met with skepticism by US dealers, especially regarding whether VinFast had enough spare parts inventory among other things. The dealer margins in the US for luxury cars are around 10% of the sales price, so this should directly affect profits by a significant amount. VinFast already faces a pricing problem with its line-up, as outlined below. This is a sign of desperation as VinFast likely has over 2,000 units of inventory in the US right now (it’s Q1 global sales were only 1,800).

VinFast Hides its Delivery Numbers: Looking through VinFast’s recently published F-20 financials, unit sales numbers are nowhere to be found. This is a first for me, as a longtime auto analyst. Marklines, an automotive database I use, shows that through July 2023, VinFast has only sold 1,230 of its flagship VF 8 in the US. S&P Global Mobility says that the VF 8 only saw 137 registrations in the US through June. CNBC recently reported that VinFast has already shipped 3,000 cars to the US since December, so inventory must be high. I finally found quarterly delivery numbers in the quarterly presentation materials of Vingroup (VinFast’s parent company), which is odd. Most carmakers emblazon their delivery numbers on the first page of their presentation materials.

2023 Delivery/Revenue Goals Are Unrealistic without Huge Price Cuts: At the May annual shareholders’ meeting for Vingroup—VinFast’s parent company—its founder and CEO stated that VinFast would sell between 40,000 to 50,000 EVs this year and generate $1.88 billion in revenues. As of Q1, however, Vinfast had only generated $0.84 billion of revenues on deliveries of 1,800 vehicles. Vingroup’s Q2 presentation material shows that VinFast saw 9,500 deliveries, implying around $0.35 billion in Q2 revenues (assuming flat pricing with Q1, which is doubtful). This means that VinFast will need to deliver 75% of its full-year target for car sales and 94% of its full-year revenue target during the 2H of 2023. And this is implausible given how weak VinFast’s image is in the US and how overpriced their new models are compared to better-made products from rivals, as explained below.

Expect Deep Price Cuts Soon

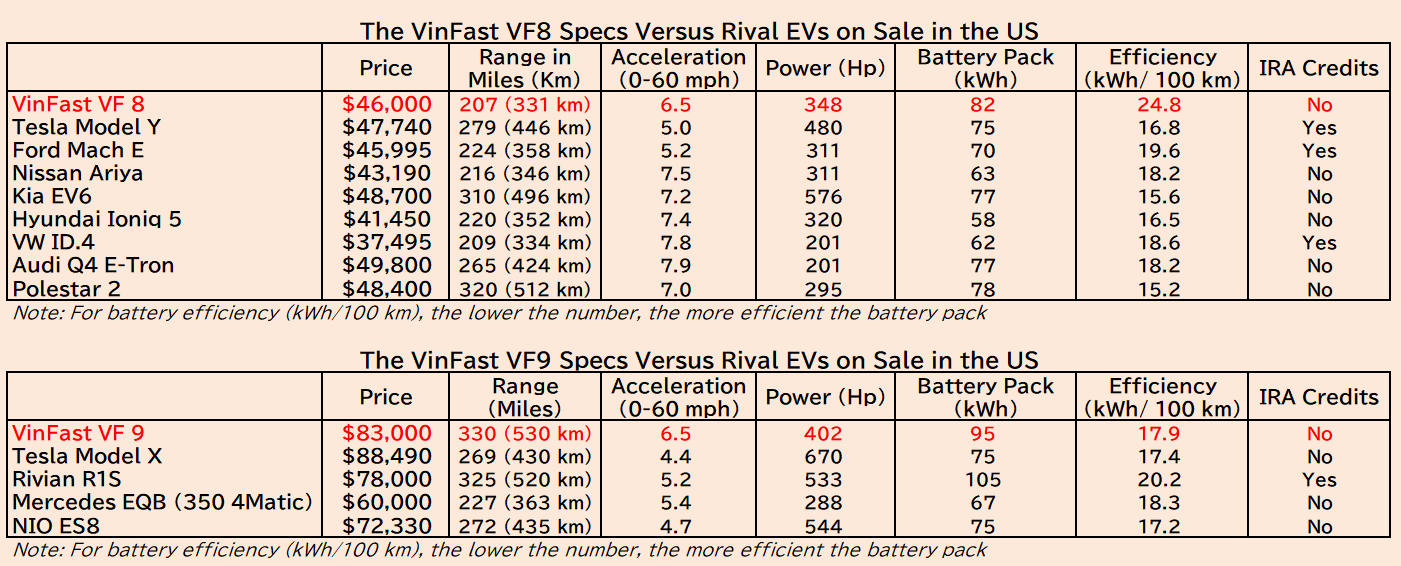

While already behind on its target of 45,000 deliveries in 2023 (only 11,300 cars sold in the 1H of 2023), VinFast is now faced with weak product quality that’s priced in line with better EVs among rivals in the US. Figure-3 shows VinFast’s VF 8 and the upcoming VF 9 (Q4 launch scheduled, but not yet announced). The VF 8 is a compact SUV going against Tesla’s Model Y, while the VF 9 is a three-row large SUV that will compete with Tesla’s Model X and Rivian’s R1S.

The VF 8 has decent acceleration and horsepower compared to its rivals, but battery efficiency, in terms of kWh of energy used per 100 km (the lower, the better), is inferior to rivals. This is why the 207 (331 km) range for the VF 8 is below the average 255 miles (408 km) seen among its rivals.

The VF 9’s EPA range of 330 miles (530 km) is much higher than rival models’ average range of 275 miles (440 km). Battery efficiency is also better than the rivals’ average. But since it has yet to be given to the automotive press for test drives as of now, we have no clue how good the quality will be.

Furthermore, at a price tag of $83,000, VinFast will be challenged to draw customers away from the lower-priced Rivian R1S at $78,000. The Rivian is also eligible for at least $7,500 in IRA credits as it’s made in the US, while the VinFast VF 9 isn’t. This means that VinFast’s VF 9 may need at least a $12,500 (15%) discount in order to even be noticed by potential buyers.

Figure-4: VinFast’s Pricing is Too High vs Rivals

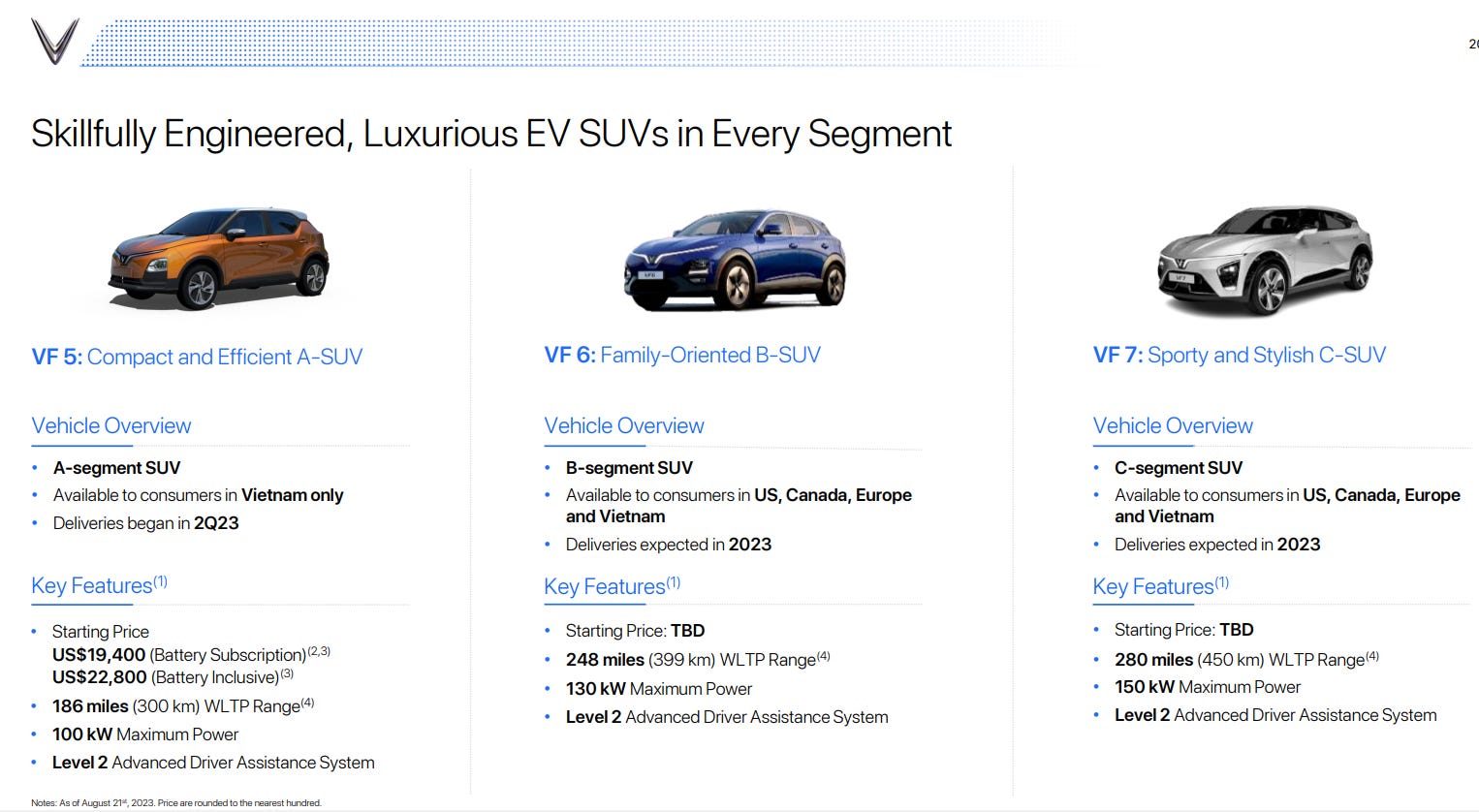

VinFast also plans to launch two more SUVs in the US this year: the VF 6 and the VF 7. Given that there is no news of launch events recently, it’s hard to imagine that they will be on sale this year. The VF 7 actually looks attractive and could sell well at the right price.

Figure-5: Two More Models For the US in 2023

The Downside: Dilution, Insider Selling & More

In the article about VinFast’s SPAC merger by Chris Bryant (see link above), he mentions that there are around 15 million warrants that will soon become exercisable. This is more than twice the 7.2 million float of VinFast at the moment and roughly 1.7x the average daily trading volume since VinFast went public. The founder’s shares (99.69% of total shares outstanding) and those of other large insiders are locked up for 180 days until February 12, 2024 and it’s highly doubtful that Vuong would sell any of his shares.

But the need for capital at VinFast is huge: In Q1, the cash burn at VinFast of $1.1 billion was 14x their revenues of $0.84 billion. Any announcement of an equity offering will surely cause the stock to dive (but given its “meme stock” status, maybe not?) and the company definitely knows this.

If they can issue shares at $20 (roughly 46% below current price) at 10% dilution, VinFast could raise around $4.6 billion. If they dilute by 15% and can sell new shares at $15 (roughly 60% below current price), they could raise $6.9 billion.

Both scenarios wouldn’t cover the downside VinFast faces in terms of $4 billion per year in cash burn and the $2 billion needed to build Phase 1 of its North Carolina plant by 2025.

Fair Value Could be as Low as $2.50 (93% Downside)

Using the valuation table on EV start-ups below (same as Figure-1), here are the main points about EV start-ups:

The average EV/Sales ratio is now 6.3x versus legacy’s 0.7x average

VinFast currently trades at 46x

The average operating loss margin (ex-Tesla) is -213% vs VinFast’s -611% in Q1

Given all of this plus VinFast’s disastrous debut in the US, a 20% discount to the average EV/sales multiple of 6.3x leaves you at 5x for VinFast

On a 5x EV/Sales ratio based on VinFast’s target of $1.88bn in revenues this year, it’s only worth $3.16. But as discussed above, there’s no way this $1.88bn revenue target for 2023 will be achieved based on recent disclosures

On my estimates of only $1bn in revenues, VinFast is worth $2.17, but this doesn’t factor in cash burn

Assuming the best-case scenario of VinFast being able to raise $7 billion this year while the stock price is still elevated, VinFast would still only have around $1.4 billion in equity after 2023 and 2024 cash burn. Based on the current rival average of 5.8x EV/equity and a 20% discount to that at 4.7x, VinFast should trade at $2.23

The average of all of the above points to VinFast fair value at around $2.50. VinFast is currently trading at $35.59

A Warning to VinFast Short Sellers: Mind the Float

The above is by no means investment advice. Please read VinFast’s recent F-20 and let me know what you think. Keep in mind that, with a low float, VinFast could see upside short-squeeze volatility like Lucid Motors. And you’ll get your face ripped off.

Lucid only has a 23% float because 60% of its shares are owned by the sovereign wealth fund of Saudi Arabia, or PIF. This is a risk because PIF could buy out minority shareholders of Lucid before it falls to its fair value of around $2.00 at current pace.

By the same token, if VinFast falls to a certain level where its bondholders get worried, it would be natural for Vingroup or its founder to plow in capital to save it. Given the roughly 500% premium to its options these days, selling long-dated out of the money calls may make the best sense. VinFast is expected to report its first results as a public company on November 9, 2023, according to Bloomberg estimates.

VinFast also has $1 billion of short-term loans due in September and some type of convertible bond triggering date of September 25, 2023.

Trade carefully.

Figure-6: VinFast’s Q1 Earnings Results

Thanks for this article. I think there will be plenty of opportunity to short the stock later, when more shares are available. It's amazing how much money the founder invested. I will follow his story and the stock.

IMHO, Tesla looks next to this one as quite respectable blue-chip company. Just out of curiosity, I have tried to open a short position and according to my broker, there are no shares available. Considering, with whom we are dealing on the other side, I would rather buy a popcorn a watch, what is going to happen that to have my skin in this game.

By no means, this company, given its valuation and its prospects is an ideal deal for a short position. But here is my problem (leaving aside, that there are no shares available to short): it wasn't big deal to orchestrate a "gamma squeeze", which effectively wiped out the TSLAQ community at that time. This company is a "micro-volume", just "beer money" of that owner guy would be enough to do the same here.

It is a nice dream to be able to short this few days ago, but it is just a dream. My 2 cents of course, based just on this article. But I will read comment of anyone who is willing to the F-20 filling :-)