For What It’s Worth: The Vietnam War and The Great Recession

For What It’s Worth: The Vietnam War and The Great Recession

The roots of the student loan crisis run deep.

This note was sent to my institutional clients on 6 July 2019. To learn more about institutional subscriptions, simply reply to this email. If you enjoy reading this post, please take the time to like, comment, and subscribe. Do you think the shrinking college premium justifies loan forgiveness?

Demand for labor remains strong and “disappointing” wage growth is the result of data over-aggregation. The “conundrum” that Wall Street has been dealing with is that they are ignoring the concept of a falling college degree premium due to an oversupply of graduates.

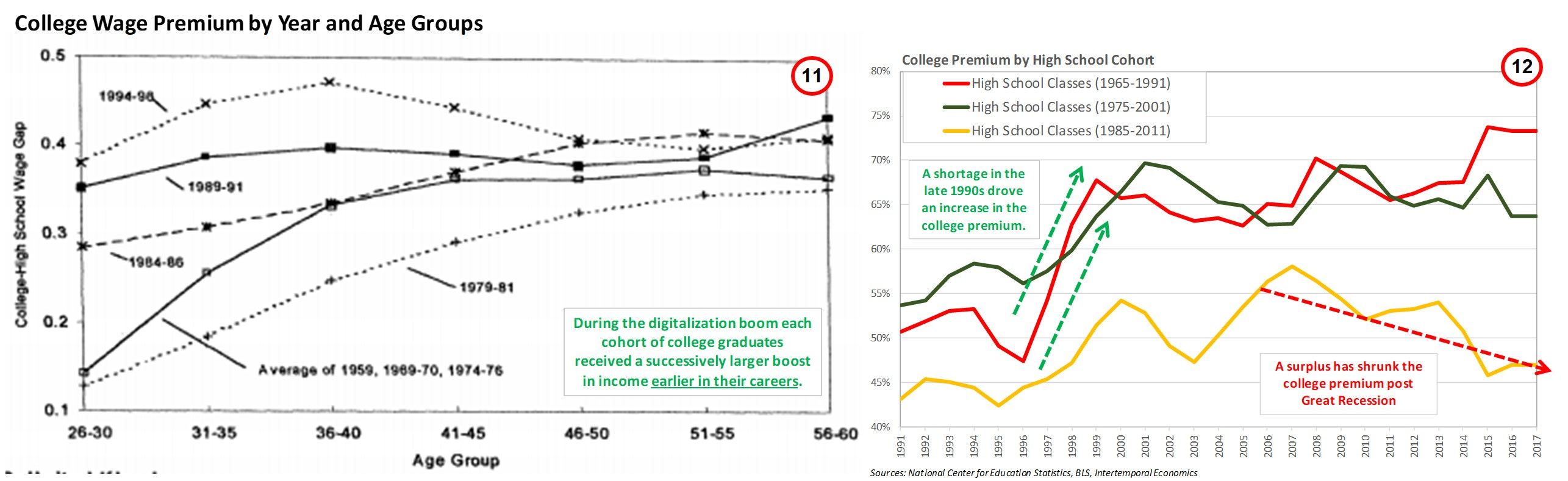

Cohorts who had graduated during the second half of the 1970s experienced low premiums on their college degrees early in their careers but went on to experience very large premiums because college educated workers were relatively scarce when digitalization took place.

I expect by the end of 2019 the shortage of college graduates will become apparent and non-linear wage growth acceleration will continue to broaden.

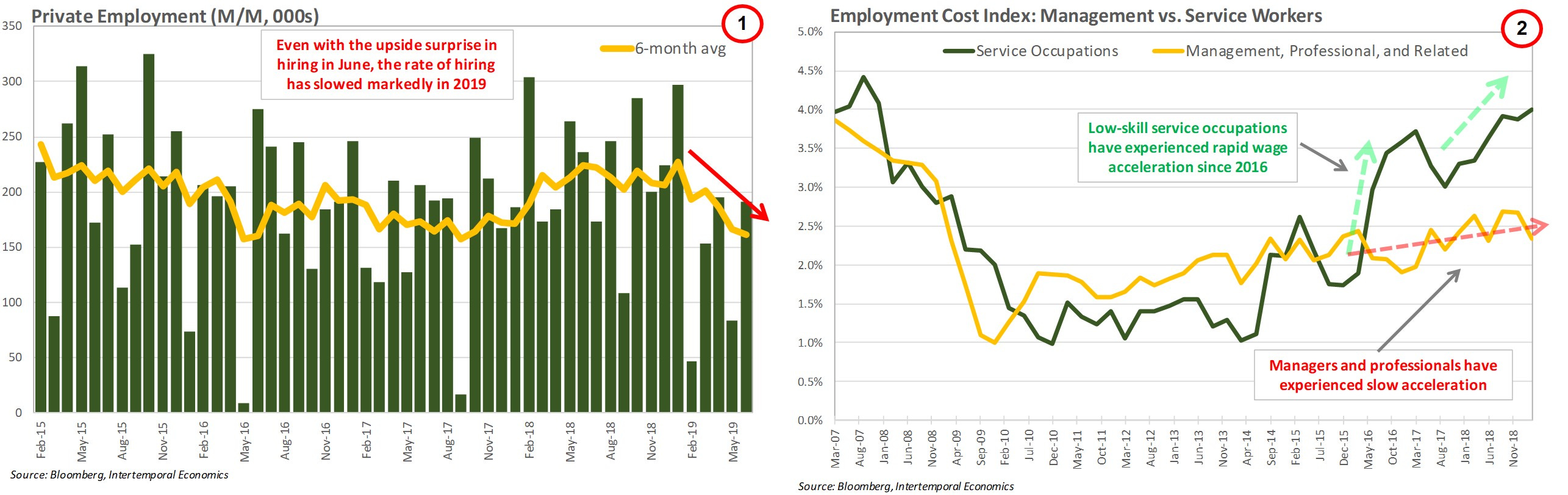

The upside surprise for net employment growth in June was large enough to jolt Wall Street into considering that the slowdown in hiring over the course of 2019 is due to a shortage of workers rather than deteriorating demand for labor (Chart 1). As I have been writing for a year now[1], demand for labor remains strong and “disappointing” wage growth is the result of data over-aggregation. In this writer’s framework labor is not homogenous and, in many cases, there are costly and time-consuming regulatory gates to be passed before a worker can be shifted from one pool of labor to another.

In this writer’s opinion, the “conundrum” that Wall Street has been dealing with is that they are ignoring the concept of a falling college degree premium due to an oversupply of graduates. Indeed, the shortage of unskilled labor is clearly seen in the sudden burst of wage acceleration in service occupations (i.e. retail and restaurants) experienced after Trump’s election (Chart 2).

The labor market should be viewed as multiple pools of labor, some more fungible than others. To understand developments in wage growth we should be looking for the supply and demand factors for skillsets rather than workers. In this note, I will examine the effect that the relative supply of high skill to low skill workers has on wages for highly educated workers. A full analysis of the July payrolls report will soon follow.

The Great Recession and the draft for the Vietnam War share two important characteristics. First, they both increased the incentive to attend college (for men only during Vietnam), regardless of the expected income premium gained from a college degree. Second, they were discrete events rather than secular trends, which creates the risk of a short-sharp effect followed by a reversal.

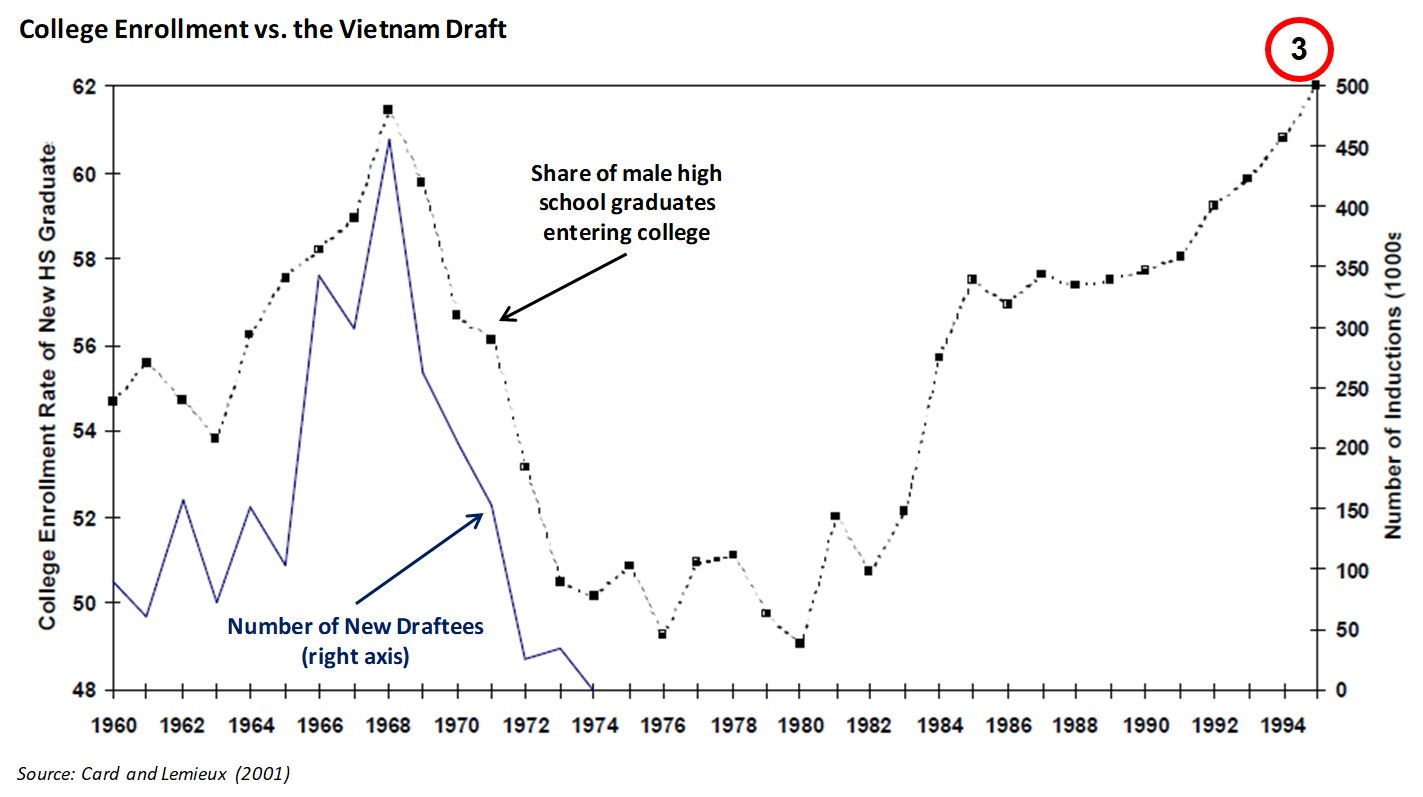

As noted by Card and Lemieux (2001), there is a clear relationship between the college enrollment of male high school graduates and the draft for the Vietnam War (Chart 3). The enrollment rate for men rate accelerates sharply in 1965 and peaks in 1968, in concert with the peak of the draft, before plummeting in the early 1970s. Card and Lemieux found that draft avoidance increased the likelihood of men attending college by 6.5 percentage points, no such effect is visible for women. Enrolling in college was a very effective method of draft avoidance as men from the 1945-1947 birth cohort were only 1/3 as likely to serve in the military if they attended college. Many men without a degree were found unfit for duty, which reinforces the effectiveness of college as a draft avoidance method.

After 1969, the draft was changed to a lottery system where the order of the draft was assigned randomly rather than calling draftees at random as needed. Thus, only men with a low draft number were at serious risk and only for one year. This change significantly reduced the incentive to attend college and, especially, remain enrolled. Dropout rates soared and enrollment rates fell. The draft was ended in 1973 and college enrollment rates for men bottomed out soon after.

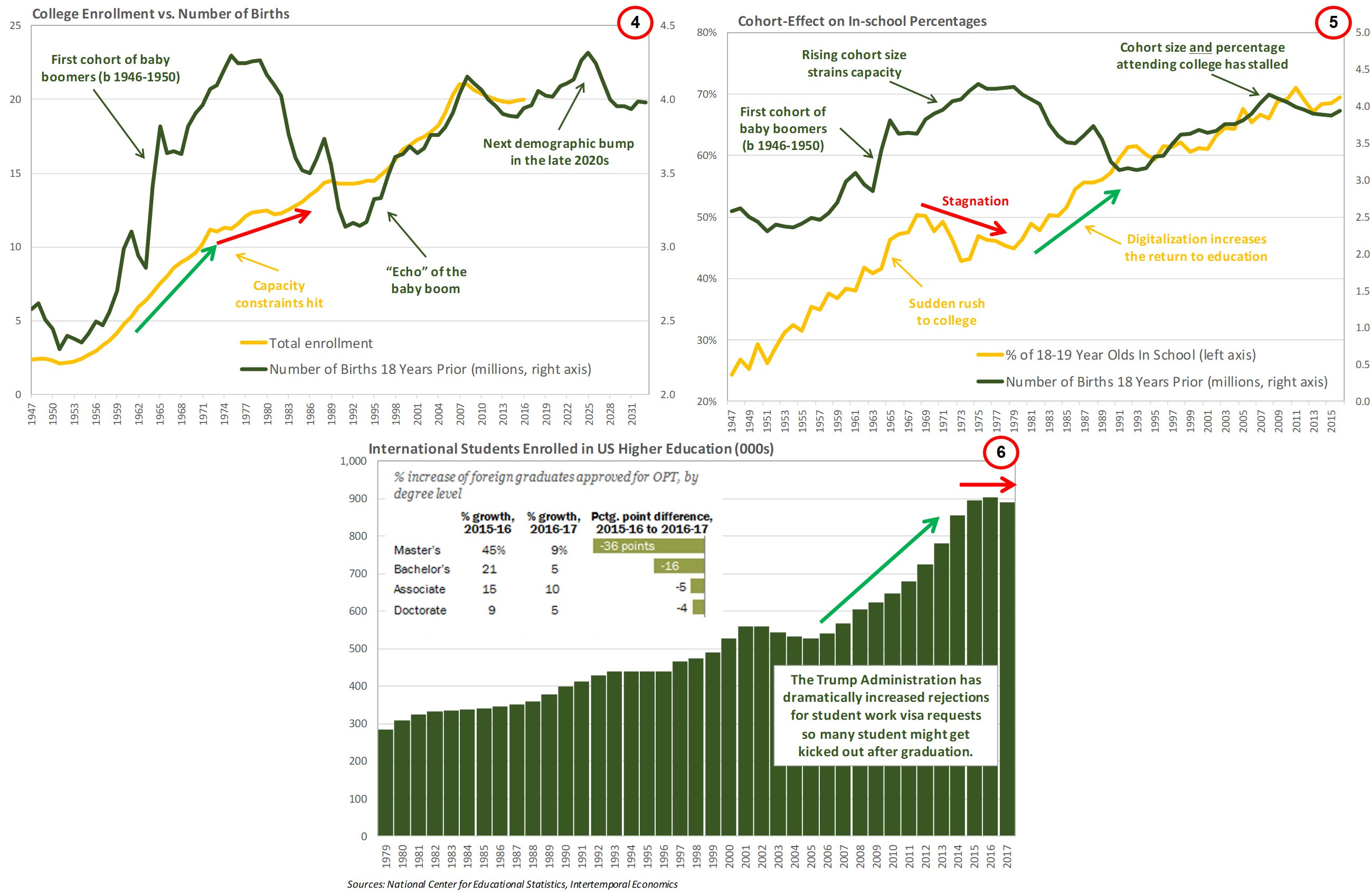

Some of the decline of enrollment rates in the 1970s was the result of payback from the rush to college during Vietnam, but enrollment rates also declined in Canada and Britain. The “kink” in enrollment that occurred in 1973 was a sign of binding capacity constraints in the higher education sector (Chart 4). The Baby Boom was so large that it flooded the higher education system in the 1970s. Enrollment continued rising, but cohort sizes expanded faster than the higher education system could accommodate new students. Indeed, the number of births in 1956 was 27% higher than in 1946. In the 1980s cohort sizes were plummeting, causing enrollment rates to rapidly rebound.

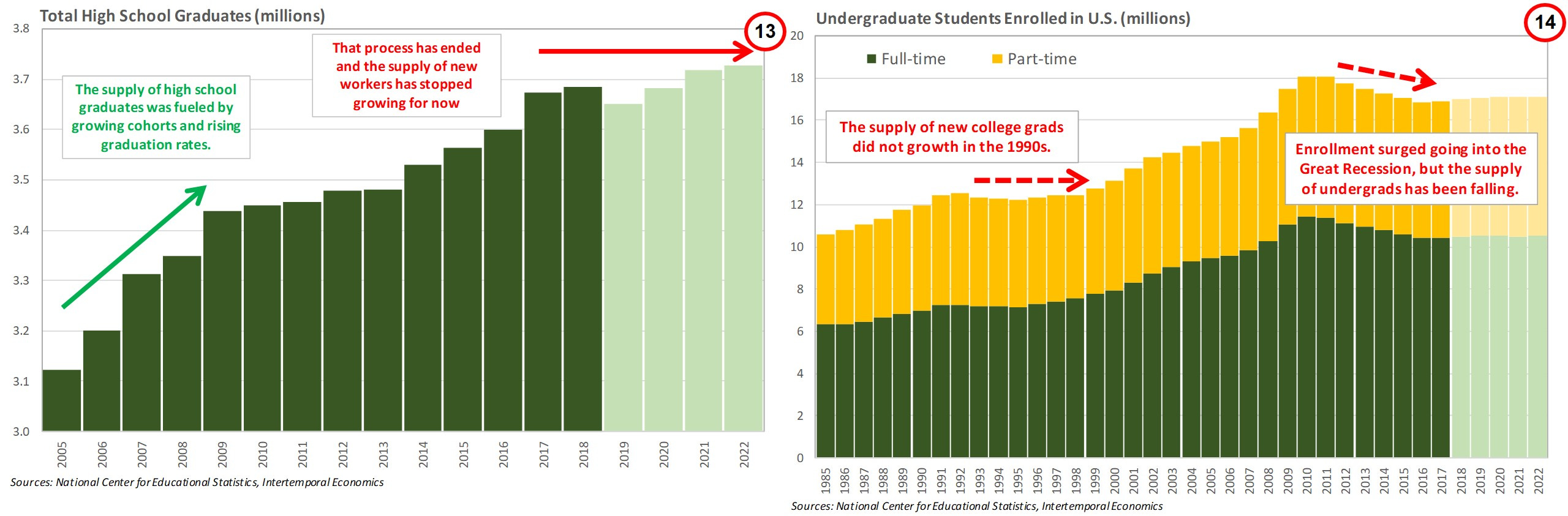

During the late 1990s and 2000s the “echo” of the Baby Boom increased cohort sizes and college enrollment rates for graduating high school seniors continued to rise (Chart 5). However, in 2008 two important changes occurred. First, cohort size began declining as the effects of the “Baby Bust” of the 1970s reaches a second generation. The Census department is predicting another demographic bump of 18-year-olds in the late 2020s so there is a long time before a significant amount of fresh meat gets dumped on the labor market. In addition, college enrollment rates have stalled as the nation reassess the value of a college degree, more on this below. The key point is that in the next five years the US faces smaller cohort sizes and flat to lower college enrollment rates. Indeed, the decline in college enrollment would have been much larger if not for the addition of 300,000 foreign students (Chart 6). The labor market is about to experience a decline in the number of college graduates for the first time since the 1990s.

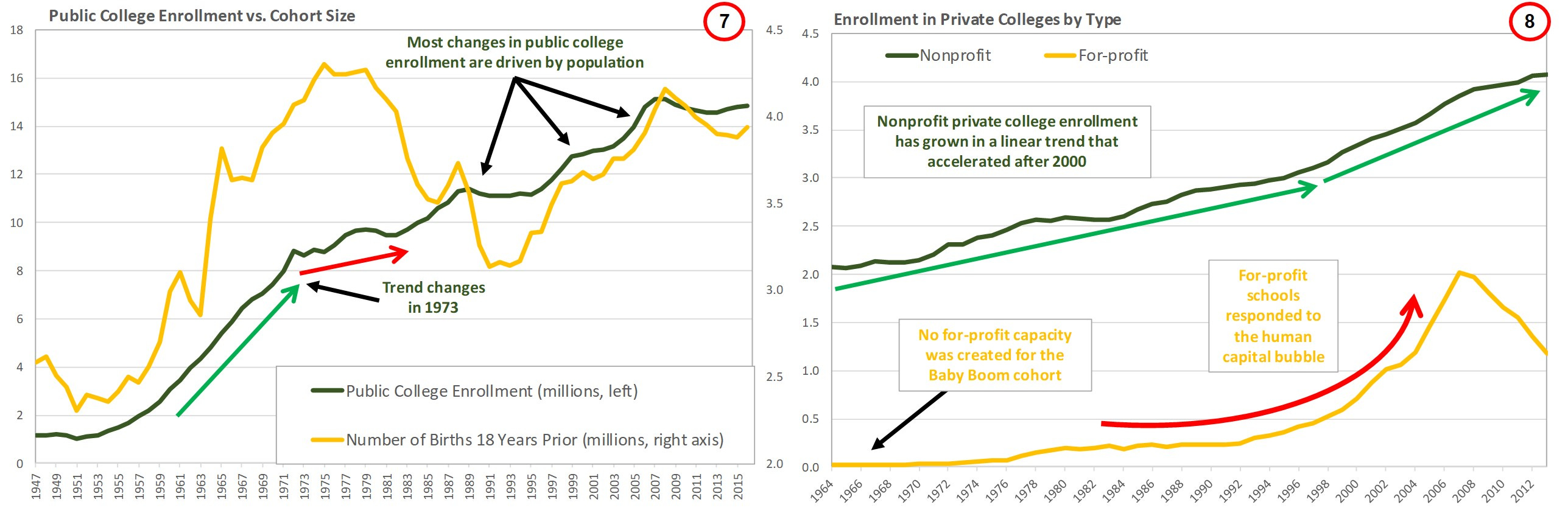

The difference in enrollment trends in the 1970s and 2000s can clearly be seen when enrollment is segmented by the type of institution. Private institutions show no change in trend in 1973, but enrollment in public colleges shows a distinctive “kink” (Charts 7 & 8). The 1973 date is clearly not accidental. Fiscal restraint and declining expectations for future growth (of the economy and thus taxes) reduced the willingness of states and municipalities to fund growth in higher education capacity. The rate of enrollment at private non-profit schools has maintained a linear trend since the 1960s with minor change in trend rates over time.

In contrast, attendance at private for-profit schools grew exponentially starting in the 1990s and running until 2008. Unlike in the 1970s, the growth of for-profit schools meant there was no capacity constraint limited demand for higher education. The reason for the collapse of for-profit private school enrollment is not due to a decline in demand, but rather a collapse of the business model for many “schools”[1]. Back in the “old days” of 2008, the vast majority of student loans were 98% guaranteed by the government and funding was provided by the private sector to students at a mandated interest rate[2]. Part of the business model for for-profit schools was skimming the spread between the mandated interest rate and the rate on AAA-rated secured bonds. Once the willingness of investors to buy asset-backed bonds dried up, funding for student loans was hard to come by and spreads were gone so many for-profit schools went bust.

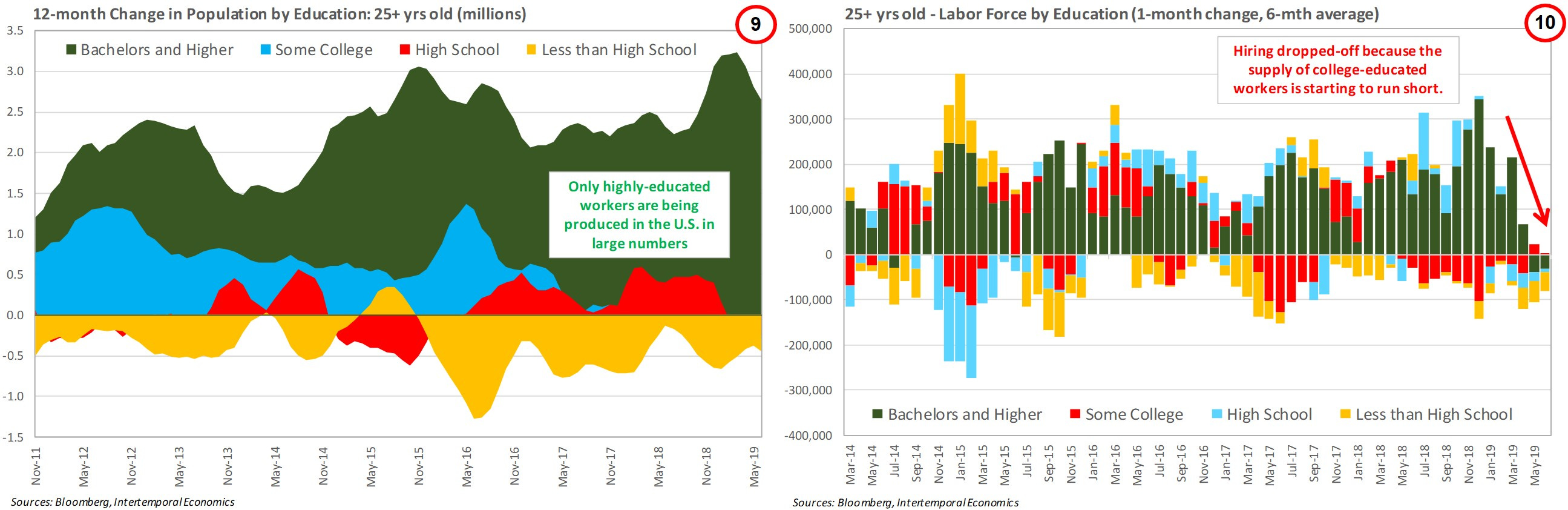

In short, the rapid growth of college graduates during the 2000s combined with the flood of “recession avoiders” created a glut of college graduates in the labor market. As a result, when wages for low-skilled jobs accelerated in 2017, wages for college graduates reacted only weakly. However, over the course of 2019, signs of a shortage in the high-skilled section of labor market have been growing. Notably, the number of prime age workers with a bachelor’s degree or better has stagnated in 2019 (Charts 9 & 10). The pool of excess high-skilled labor is finally drying up.

The implications of a shortage of high-skilled labor can also be found in the aftermath of the Vietnam War and the stagnation of the 1970s. Workers decide whether to enter college based on the college wage premium at the time they graduate high school. In addition, once a person has elected not to attend or has dropped out of college, they are extremely unlikely to go on to graduate later.

In the 1970s, the result of a glut of college graduates and economic malaise was a prolonged decline in the rate of college enrollment by high school graduates. The college premium was low for post 1955 birth cohorts so they attended college at a lower rate than would be expected, given other factors. That low rate of enrollment in the 1970s had significant implications in the 1980s and 1990s as the digitalization of the US economy took place. Two factors stand out.

First, during periods of rapid technological advancement such as the 1980s and 1990s, the college premium expands significantly for younger workers, presumably because their education incorporated training with new technologies (Chart 11). In Chart 12, I have updated the analysis used in Chart 11 using a slightly different methodology. Cohorts who had graduated during the second half of the 1970s experienced low premiums on their college degrees early in their careers but went on to experience very large premiums because college educated workers were relatively scarce at a time when their skills were in very high demand. In contrast, cohorts that graduated in the 2000s, especially those who graduated after 2008, experienced lower and declining wage premiums for their college degrees.

In the post-2008 period the college premium declined and since Trump’s election the premium has shrunk even further as wages for low-skilled occupations have accelerated. This was to be expected given the massive run up in college enrollment during the 2000s and the flight to college during the Great Recession. However, as 2020 approaches, the actuarial tables have turned. Declining cohort size and stagnating college enrollment rates mean the supply of new college graduates will be falling off for the next few years and will not begin rising again until the late 2020s (Charts 13 & 14). The college premium has declined further than it should have and, if labor market conditions remain tight, strong demand for highly educated workers will bring the premium back to historic norms. Since wages are sticky to the downside and overall demand remains strong, the premium will be restored by wage acceleration among high-skill occupations. I expect by the end of 2019 the shortage of college graduates will become apparent and non-linear wage growth acceleration will continue to broaden.

If you enjoy reading this post, please take the time to like, comment, and subscribe. Do you think the shrinking college premium justifies loan forgiveness?

Related Posts

The Political Economics of Student Loan “Forgetfulness”

Wages, Inflation, and the Speed of Adjustment

The Beveridge Curve and the Magic of the Movies

References

Cand, David and Thomas Lemieux, 2001. "Going to College to Avoid the Draft: The Unintended Legacy of the Vietnam War," American Economic Review, American Economic Association, vol. 91(2), pages 97-102, May.

Card, David & Thomas Lemieux, 2001."Dropout and Enrollment Trends in the Postwar Period: What Went Wrong in the 1970s?," NBER Chapters, in: Risky Behavior among Youths: An Economic Analysis, pages 439-482 National Bureau of Economic Research, Inc.

Card, David & Thomas Lemieux, 2001. "Can Falling Supply Explain the Rising Return to College for Younger Men? A Cohort-Based Analysis," The Quarterly Journal of Economics, Oxford University Press, vol. 116(2), pages 705-746.

Douty, H. M. "The Slowdown in Real Wages: A Postwar Perspective." Monthly Labor Review 100, no. 8 (1977): 7-12.

[1] For a detailed discussion on the for-profit student loan scam see my note “The Political Economics of Student Loan Forgetfulness”, 19 March 2019

[2] A provision ending the private funding program was included in the Obamacare legislation to satisfy the hard left who had wanted a publicly owned health insurance provider.