($GAW.L) Games Workshop

HISTORY & OPERATIONS

Games Workshop is the largest and mostly respected miniatures company in the world, with brands like Warhammer, Warhammer 40,000 and IP licensing for exploiting The Lord of the Rings saga into tabletop battle games.

The entirety of its production is located in Nottingham (UK), where not only hobby miniatures are developed, but also books, all sorts of manuals (painting guides, rulebooks, etc.) and different scope accessories which contribute to enhance and enrich the culture surrounding its fantasy world.

The company sells these miniature soldiers, which are painted and collected by customers engaging afterwards in tabletop battle games at Game Workshop stores or official tournaments with other fellow fans, building a strong community and fostering social interaction.

It is a vertically integrated business, which allows it to maintain control over every aspect of design, manufacture and distribution of its leisure products.

As the management has repeatedly indicated, this is an industry where customers seek to have the best quality miniatures and, consequently, they are willing to pay a high price for it.

Games Workshop is a manufacturer, not a retailer. They make things.

Nonetheless, they have outlets in retail locations (Game Workshop stores) which act as the frontline of the company by helping customers in getting initiated to this world. Since the company historically has relied strongly on how these stores (typically single-managed locations, meaning there is only one person taking care of the shop) performance, the selection process is hard and thus tough to rapidly penetrate new countries and/or cultures by means of this system. The owners of the stores (who Games Workshop refers to as Stockists) have to be very passionate about the company’s products.

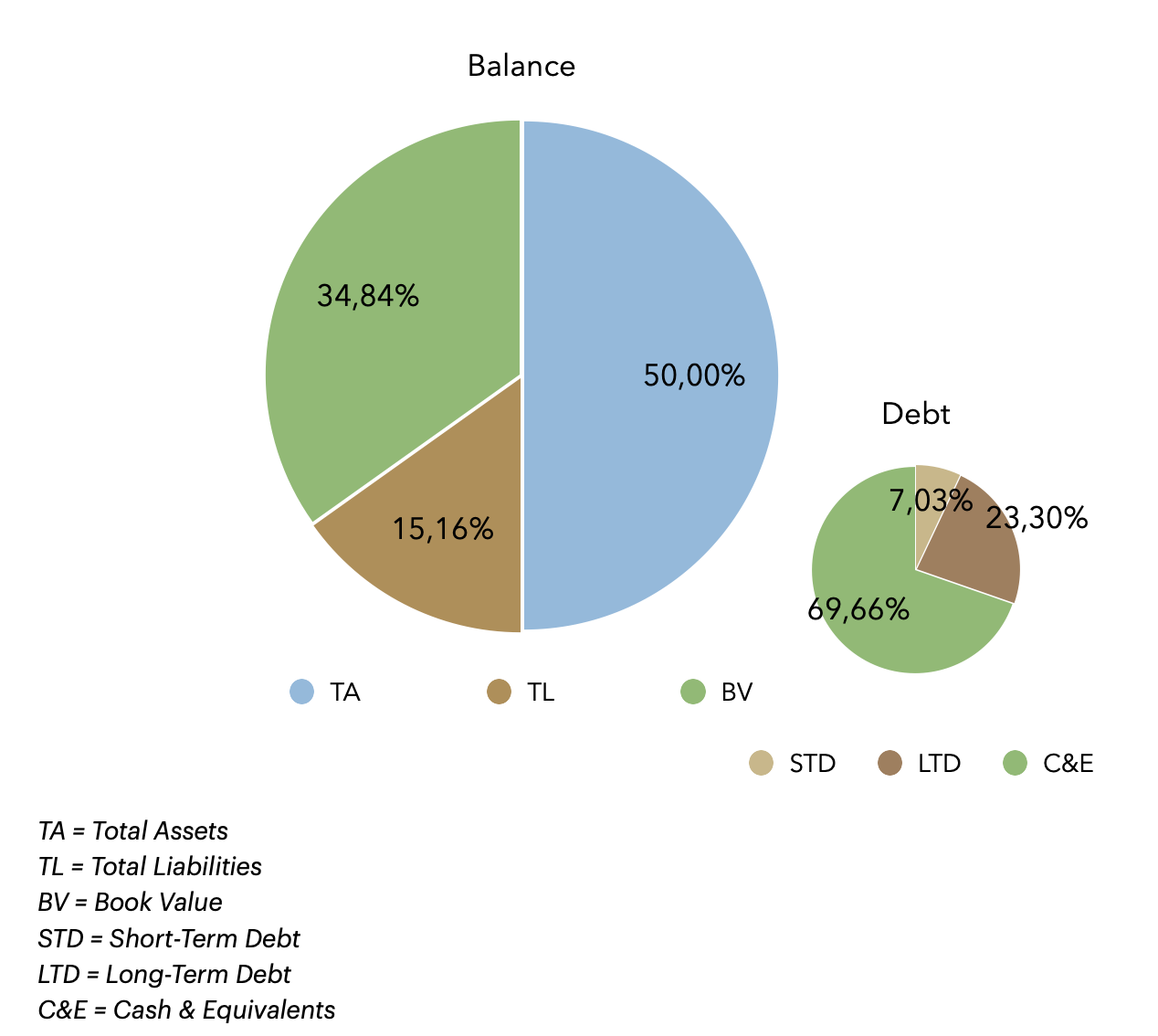

Overall, Games Workshop carries on its operations without any leverage, bearing a negative net debt of (£41.0M) in an industry which could be thought as somewhat capital intensive.

As management puts it:

"We don’t spend money on things we don’t need, like expensive offices or prime rent shopping locations or advertising that speaks to the mass market and not our small band of loyal followers. We only invest where it makes a positive improvement to our business model, such as in tooling to make better plastic miniatures, in opening more Game Workshop stores to improve our customer service and in fit-for-purpose systems to make our processes more efficient and reliable.

And when we make an investment, we measure its impact to ensure that it delivers an improved return on capital for our owners.”

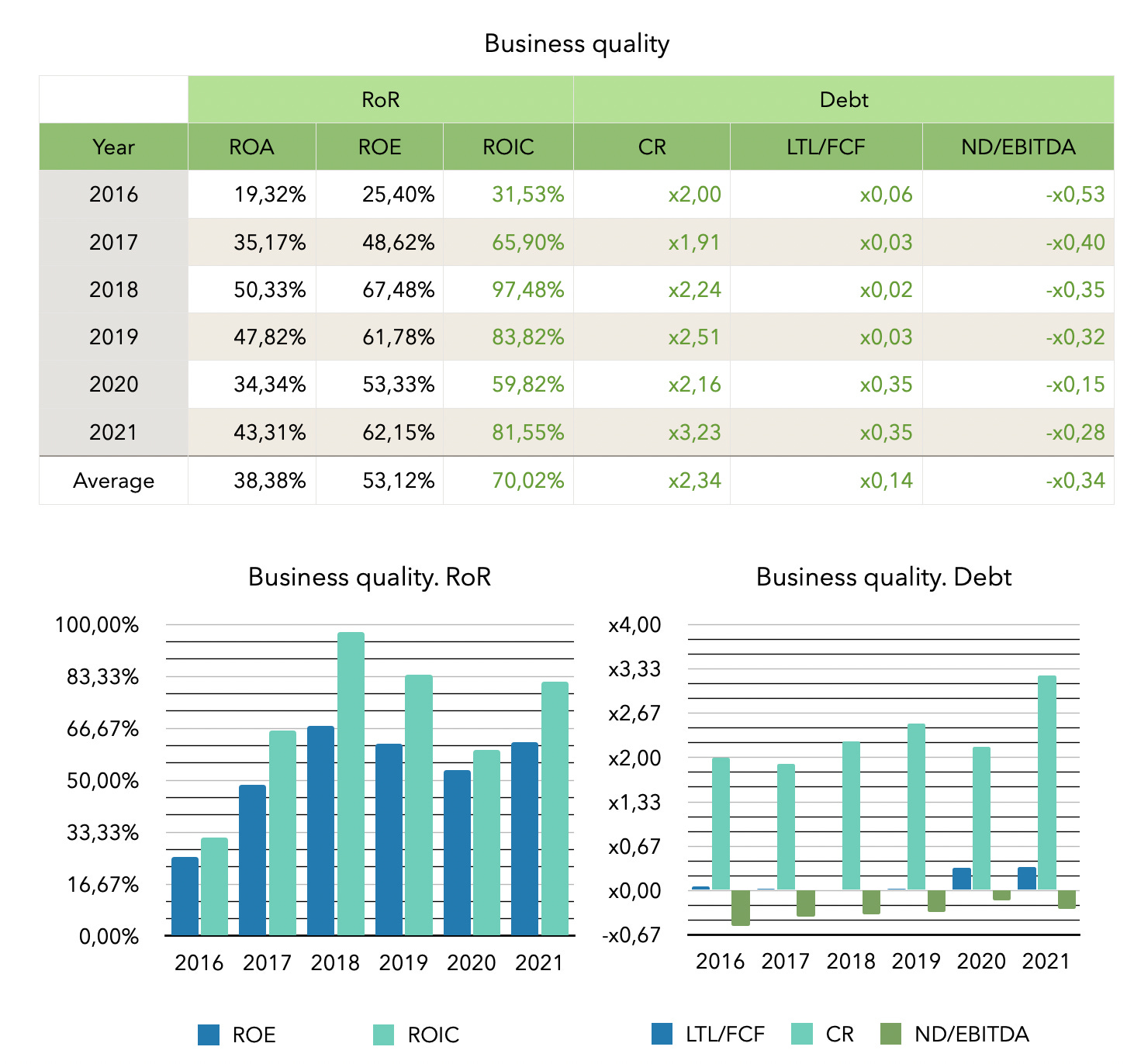

Interestingly enough, indeed it looks like the returns on capital employed and equity of Games Workshop range consistently between 50.0% and 85.0% (now that is a very persuasive war hammer!).

SEGMENTS

We can differentiate 3 main business segments (4 really, but we will get to that): Trade, Online and Retail.

Let’s jump into the audited most recent annual data -FY2021- (although the fiscal year ends in May, so we will have soon the financials for FY2022):

Trade:

The Trade segment is the main one, accounting for £194.8M of revenues (55.2%), with a 39.0% growth YoY.

Games Workshop sells its products to third party retailers under closely controlled terms and conditions, aiming to reach those areas where Stockists are not present yet or it is not economically profitable for the company to open new stores.

The transactions are controlled by telesales departments located in Nottingham, Sydney, Tokyo, Shanghai, Singapore, Hong Kong and Kuala Lumpur. The final sales to consumers are done either at the third party stores or through their online platforms.

In 2021, there were 5,400 independent retailers (versus 4,900 in 2020) spread across 73 different countries.

Online:

The Online segment is the second one (by size), accounting for £87.7M of revenues (24.8%), with a 70.0% growth YoY.

It consists of every sale made via Games Workshop’s website, directly to consumer. Every store has its own online platform, from which online sales are also available.

All the website stores are managed from Nottingham HQ.

Retail:

The Retail business segment accounted for £70.7M of revenues (20.0%).

This segment comprises all sales made directly to consumers by the Games Workshop stores, which only offer Games Workshop’s products. These stores are where the majority of new consumers and hobbyists are recruited.

The stores do not offer the complete range of the company’s products, only starter sets, new releases and the appropriated extended range.

In 2021, there were 523 stores in 23 different countries, from which 406 are single-staff stores and the remaining 117 multi-staff stores are constantly reviewed to ensure they remain profitable. If not, Games Workshop’ converts them into single-staff stores.

The fourth business segment, which has only been relatively recently initiated (since Kevin Rountree began as CEO in 2015) is:

Licensing:

Games Workshop started granting licenses to a number of carefully chosen partners. This is allowing the company to broaden the exposure of the Warhammer brand worldwide, while generating additional income.

The majority of this income comes from computer game sales in North America, the UK and Continental Europe.

In 2021, 9 new games were launched, while another 15 are currently under development. Further out, more large scale projects are in early stages as well.

In the media and entertainment sector, at the end of FY2021 the amount of contracts totalled 125.

This business area is experimenting a significant growth, having Games Workshop ranked 66th in the “Top 150 Global Licensors 2020” list.

Breaking the sales by geographic segments, we appreciate that the main driver for the £353.2M of total revenues was North America (£145.5M), followed by Europe -excluding UK- (£82.1M), UK (£80.5), Australia and New Zealand (£26.1M), Asia (£12.1M) and rest of the world (remaining £6.9M).

Since the manufacturing, research and development is concentrated in Nottingham, the capital expenditures in other countries than the UK is somewhat negligible (UK CAPEX amounts to 84.8% of the total expenditures on PP&E).

We observe a similar behaviour for Game Workshop’s assets (British assets valued at £100.0M whereas the rest of the world amounts to only £27.2M).

Management

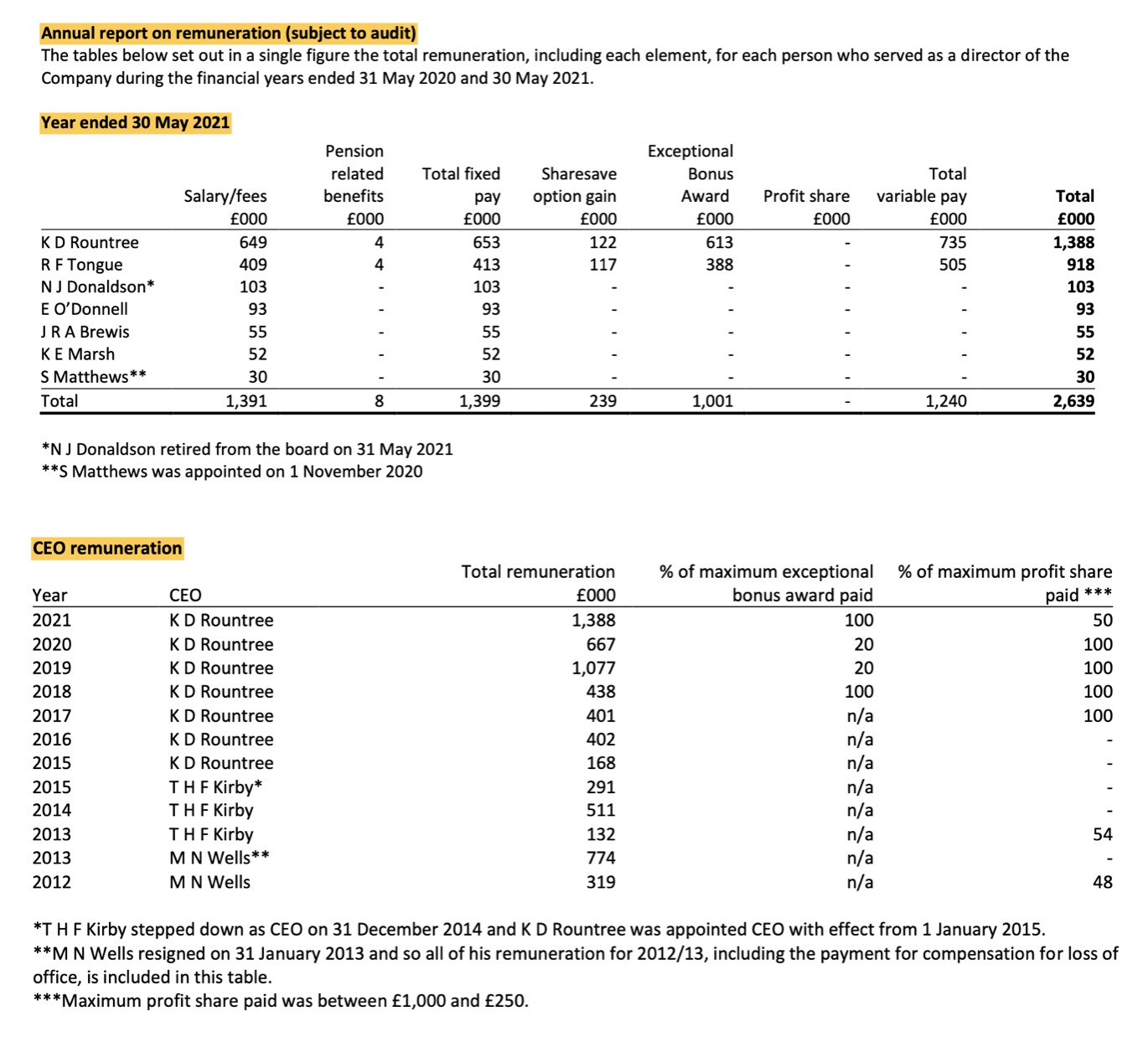

Kevin Rountree (CEO) stepped into the company in 1998 as assistant group accountant. He then had various management roles within Games Workshop, and being appointed as CFO in 2008. In 2011, his title was changed to COO as he took responsibility of managing the Group’s service centres globally. In January 1st, 2015, he became CEO.

R. F. Tongue (CFO) joined Games Workshop in 1996 as group tax manager. She then was appointed CFO in January 1st, 2015.

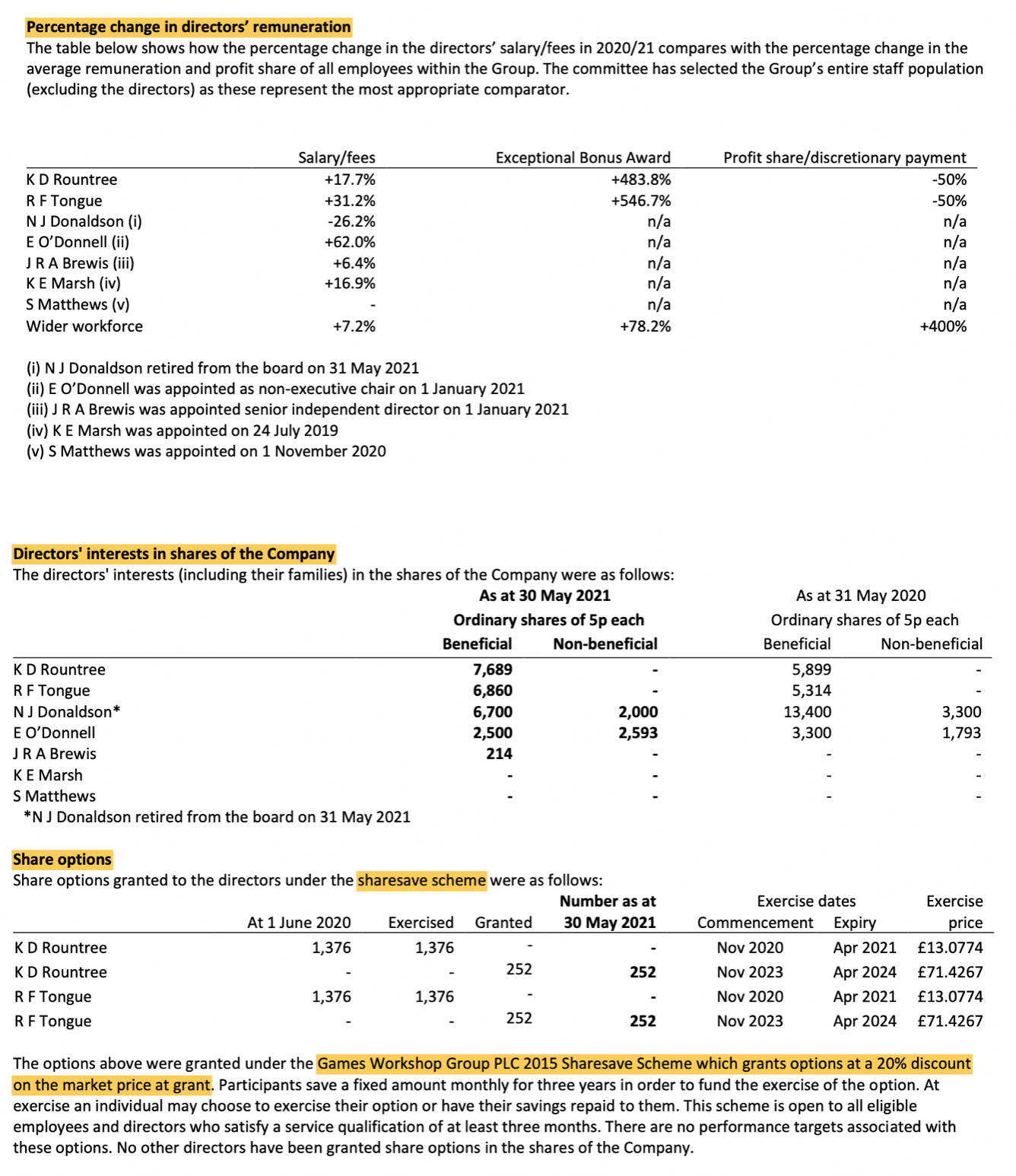

As stated in the remuneration report, after benchmarking the executive directors salaries in comparison with those of other comparable companies, it was agreed to increase K. Rountree annual base salary from £525.000 to £675.000, and R. F. Tongue from £300.000 to £450.000. Also, the Exceptional Bonus Award increased from 100.0% the annual base salary to 150.0%, payable in cash with the condition that, at least, 67.0% (previously 50.0%) of it must be invested in shares of the company at market price, which must be held for a minimum period of 3 years (previously 2 years).

The variable pay was changed bearing in mind all stakeholders’ interests. Therefore, it depends on performance indicators as sales growth, gross and operating margins, profits and profits per share, cash generation and dividends paid throughout the year.

Kevin Rountree has established a flat structure, in which people with senior responsibility report directly to him.

To bring extra focus, this senior team is split in 6 major parts: product design and IP creation, manufacturing and supply chain, sales, digital and marketing, operations and support and IP exploitation.

“We believe shareholder value is created, primarily, by not destroying it. We have no intention to acquire other companies, nor to dispose any of whose we own.

We return our surplus cash to our owners and try to do so in ever increasing amounts. A working cash buffer of three months’ worth of working capital requirement has been set aside along with six months’ worth of future capital spend and tax payments before deciding how much cash is truly surplus for the purpose of declaring dividends.”

“Our core strategy is unchanged. […] The key elements are:

Make the best fantasy miniatures.

Engage and inspire our customers.

Sell our products globally, profitably.

Make decisions with long term success in mind.”

Under Kevin, Games Workshop is focusing on the phrase “More Warhammer. More often”, meaning the management’s focus is on providing more new products with each release and fostering the IP licensing business segment.

To bring all Warhammer knowledge together, the company is developing “My Warhammer” site.

“It is worth noting that historically the launch year of a new Warhammer 40,000 edition is normally the financial high point… until the next edition of Warhammer 40,000.”

Management’s intentions for coming years is to steadily increase revenue growth whilst maintaining and improving gross and operating margins via the 3 sales channels, increasing the Warhammer brand presence in all large countries, paying special attention to China and the rest of Asia -not significant contributors to the company’s performance yet-.

VALUATION

Games Workshop holds a very strong position in the leisure products sector, more specifically in the fantasy miniatures subindustry, where quality is the single most important factor by innovating with new editions of its starred Warhammer 40,000 series being released every 3 years.

BUSINESS QUALITY

The company has maintained high returns on capital for the last decade (specially after Kevin stepped into CEO in 2015), with ROEs ranging between 50.0% and 62.0% and ROICs between 50.0% and 80.0%.

It is a conservatively managed business, with low debt and high Current Ratios:

The strategy adopted by Rountree seems to be working splendidly so far, achieving high levels of operating leverage whilst fostering organic growth. This comes as a consequence of the expansion of the Online segment (5 years CAGR of 70.0%) and the IP licensing.

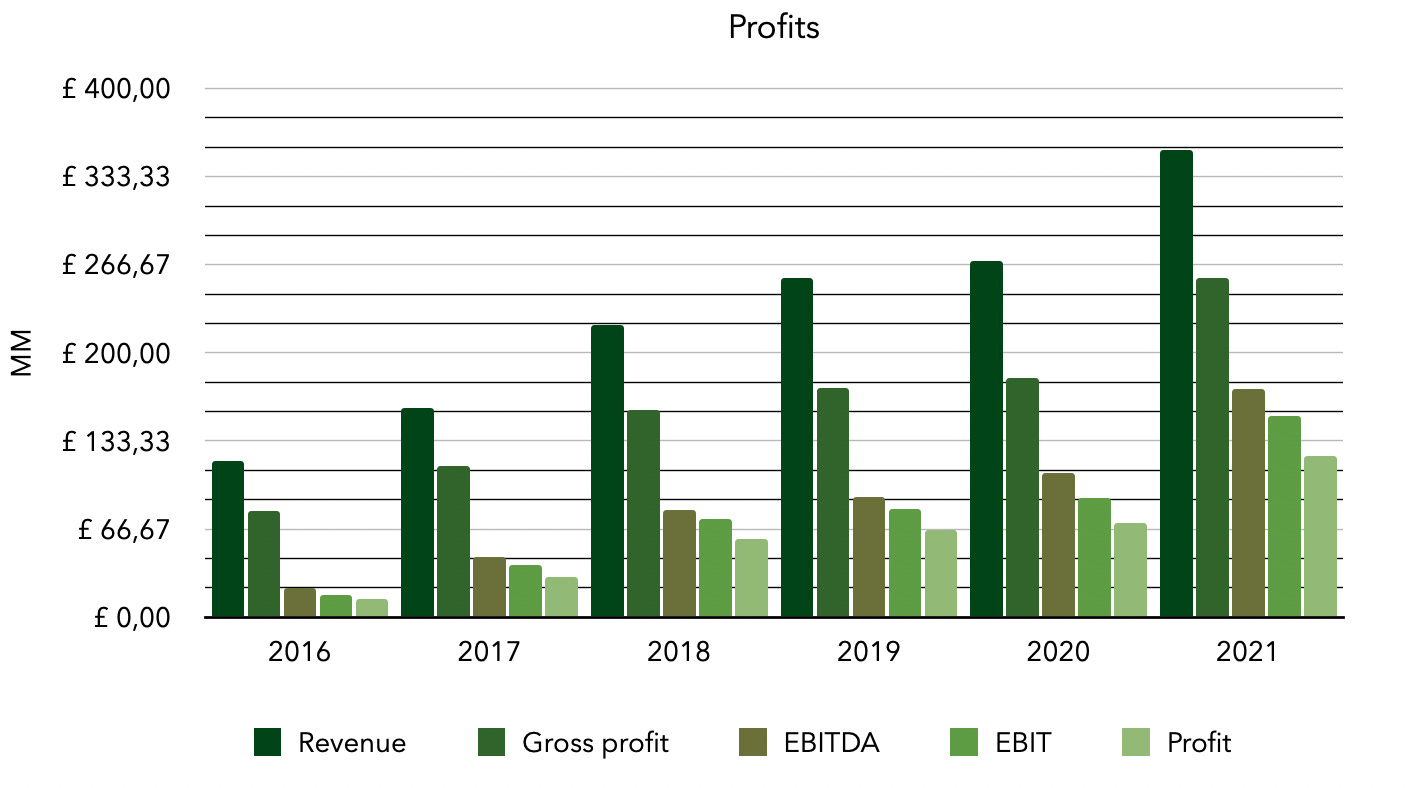

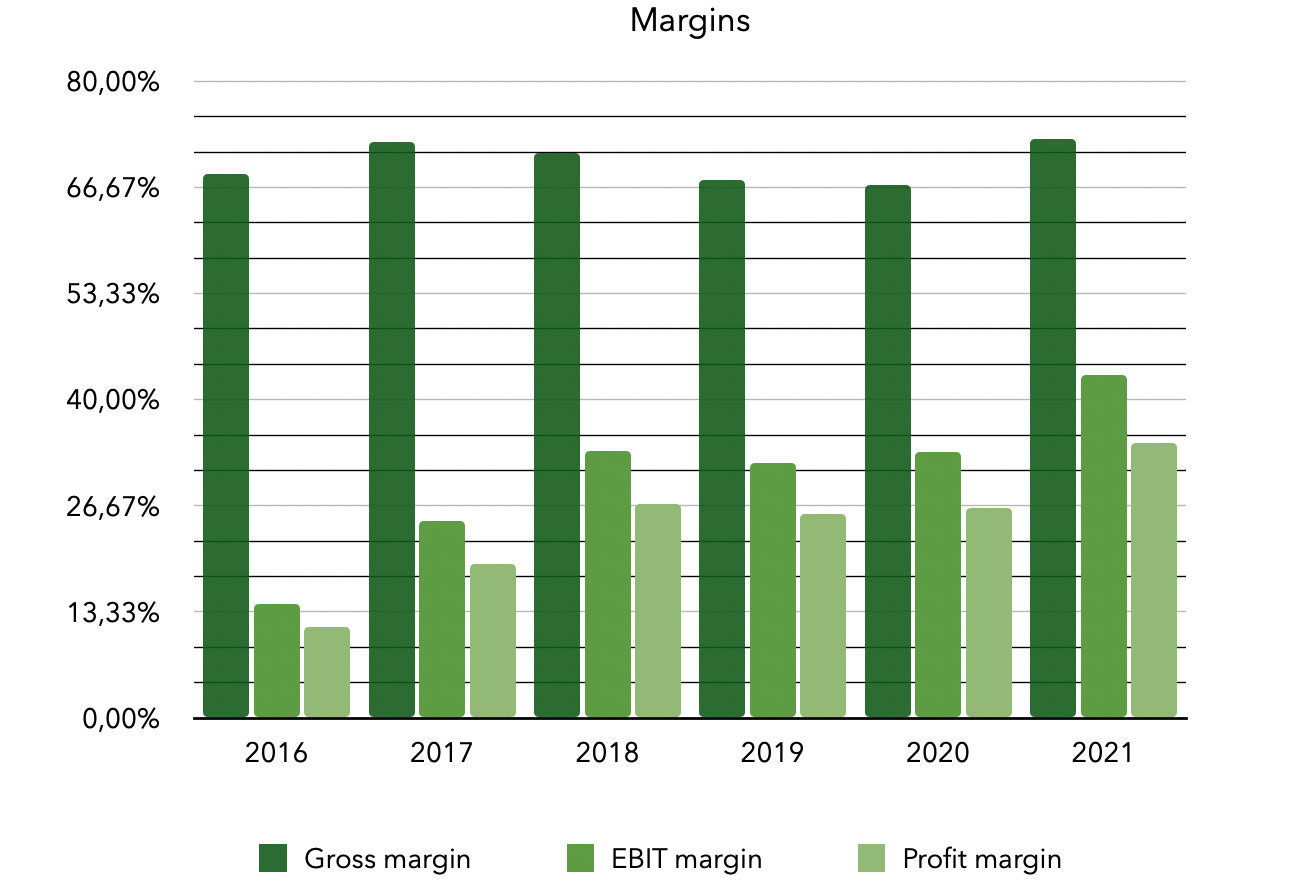

The charts below show the evolution of the Group’s organic growth and gross, EBITDA, EBIT and profit margins since 2016, when Kevin took over as executive director:

This is being achieved with an almost flat share count (only increasing due to the share-save program) and stock compensation options.

The fully diluted share count has increased from 32.15M in FY2016 to 32.93M in FY2021, which represents a net issuance rate of 0.48% CAGR.

The margins expansion, in combination with organic growth and flat share count have exploded EPS to an astonishing 5 year CAGR of 54.57%, while most of the Games Workshop’s Retail stores were forcedly closed amidst the pandemic.

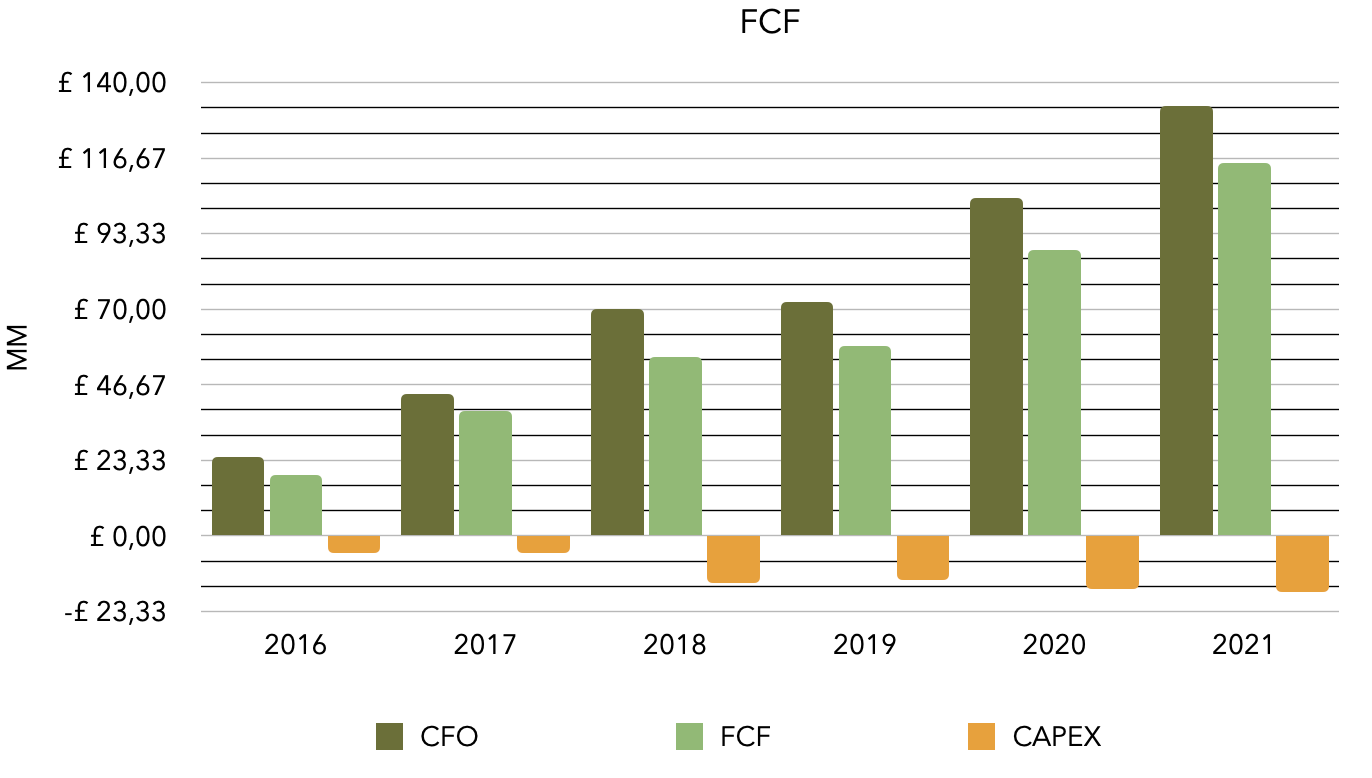

But how efficient is Games Workshop in converting those EPS into actual cash?

By taking the FCF of FY2021 and comparing it to the bottom line, we get a cash conversion rate of 94.5%, averaging 111.2% during the last 5 years. This indicates that the business is very efficient in generating actual cash (out of every £10 of net income, £9.45 are available for the company to pay down debt -almost non-existent-, make acquisitions -management refuse M&A strategies- and return value to shareholders, either via dividends or share repurchases).

Warren Buffett indicates in his 1970s letters that, on inflationary periods, the winner businesses are those with pricing power (seems to be the case for Games Workshop) and that do not need to reinvest most of the cash generated to sustain their operations.

Games Workshop’s capital expenditures amount, on average, to 17.1% of CFO (meaning out of every £10 generated by the normal operations of the company, only £1.7 needs to be reinvested to keep the business running).

The chart below shows the FY2021 financial position:

PROSPECTS

Current price of $GAW.L: £76.4/share.

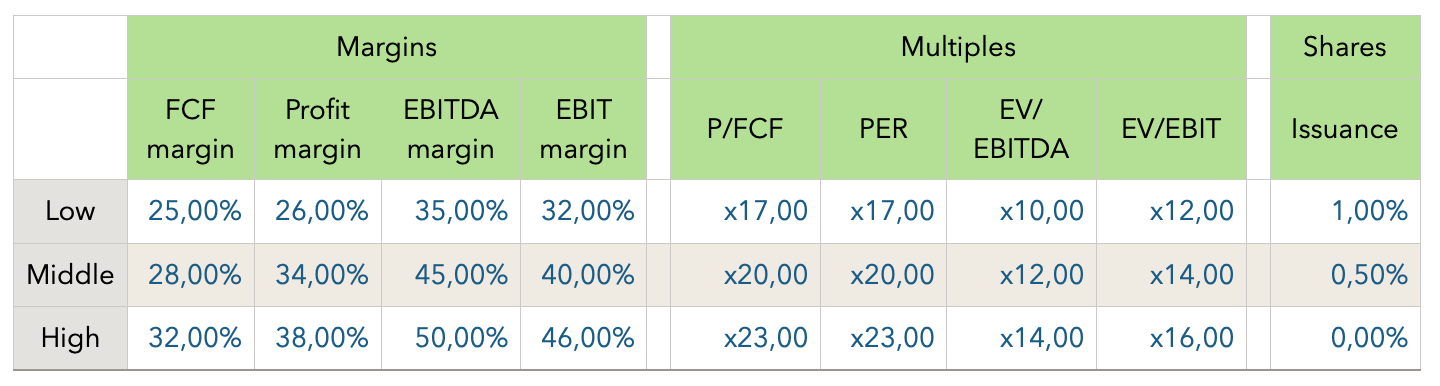

For the valuation model, we use 3 study cases (low, middle, and high). For each of these cases we try to estimate the value the business could have in 2026 based on multiples via P/FCF, PER, EV/EBITDA and EV/EBIT. The following assumptions are made:

Since 2016:

FCF margins are increasing, starting in 16.0% and ending in 32.6%.

Profit margins are increasing, starting in 11.4% and ending in 34.5%.

EBITDA margins are increasing, starting in 18.8% and ending in 48.8%.

EBIT margins are increasing, starting in 14.3% and ending in 43.1%.

Revenue CAGR of 24.5%.

FCF CAGR of 43.5%.

Net income CAGR of 55.3%.

EBITDA CAGR of 50.7%.

EBIT CAGR of 55.2%.

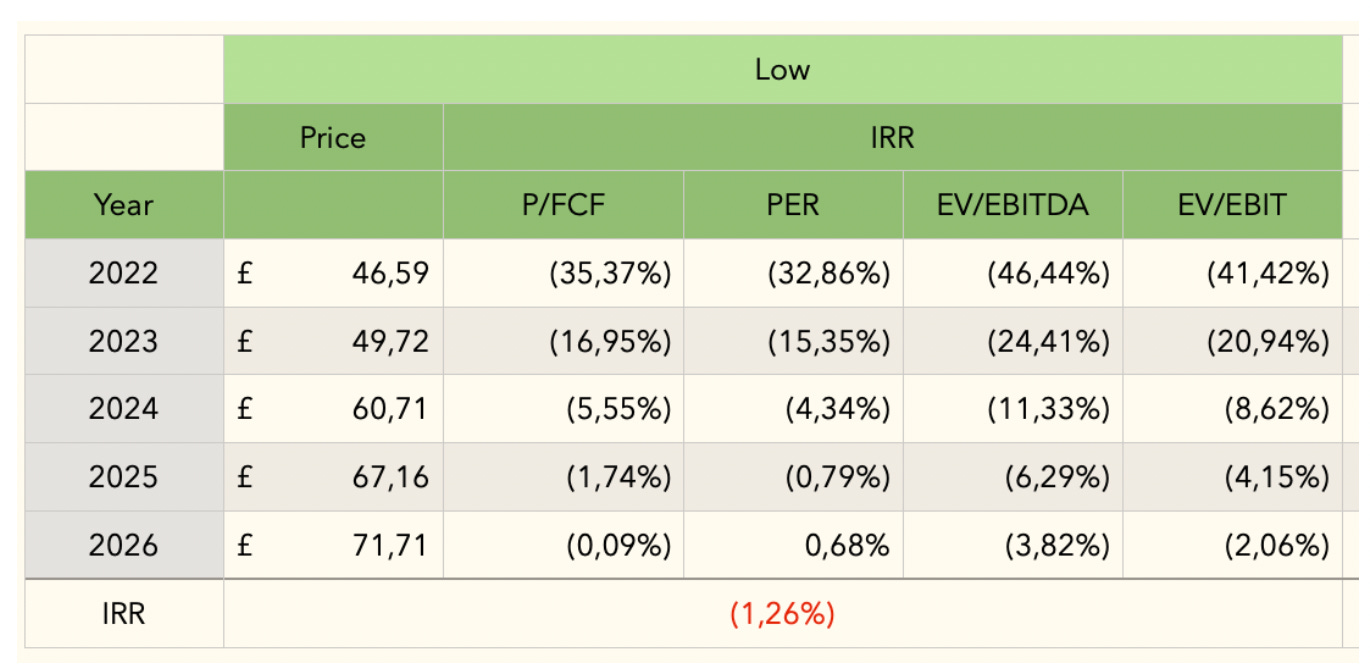

Low case

A revenue growth for the next 5 years of 11.5% CAGR is projected.

This takes us to CAGRs of 4.6% (FCF), 4.3% (EPS), 3.3% (EBITDA) and 4.0% (EBIT).

With the multiple and margins from the assumptions table above, the IRR for this case looks like this:

The Price column indicates the expected value per share on each year. The 4 IRR columns on the right, the expected annualised return.

It is important to note that this case implies a multiple contraction to x17.0 P/FCF, x17.0 PER, x10.0 EV/EBITDA and x12.0 EV/EBIT (from last 5 year averages of x35.0 P/FCF, x24.0 PER, x16.0 EV/EBITDA and x27.0 EV/EBIT), a revenue growth slowed down to 11.5% CAGR (last 5 year CAGR was 24.5%), annual share issuance rate of 1.0% (last 5 year CAGR was 0.5%) and margins contraction to 25.0% FCF, 26.0% net income, 35.0% EBITDA and 32.0% EBIT (from 32.6% FCF, 34.5% profits, 48.8% EBITDA and 43.1% EBIT).

Expected result for the Low study case:

-1.3% IRR 5 years

Middle case

A revenue growth for the next 5 years of 14.5% CAGR is projected.

Expected return for the Middle study case:

9.8% IRR 5 years

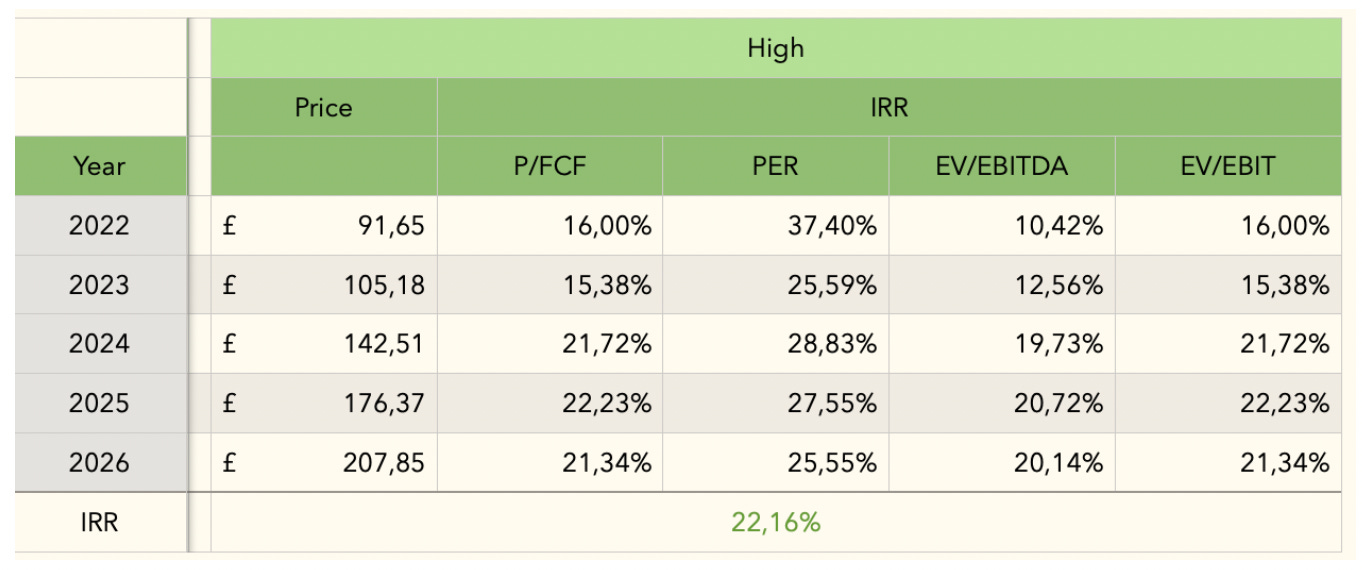

High case

A revenue growth of 20.4% CAGR is projected.

Expected return for the High study case:

22.2% IRR 5 years