Temenos AG ($TEMN.SW)

Business overview.

Temenos AG is a Swiss enterprise founded in 1993 and headquartered in Geneva, focused on providing software solutions to banks and financial institutions across more than 150 countries.

As of H1 FY2022, 41 out of the top 50 global banks are existing customers of the company. This number has been steadily expanding from 35 back in FY2014.

Similarly, Tier 1 and 2 banks contribute c.45.0% to the group’s revenues.

Products.

The Temenos’ platform and its products are the leaders in a highly regulated industry, with their flagship being Temenos Transact (core banking applications).

A key feature worth mentioning is that Temenos solutions are independently deployable, although customers gain incremental benefits when integrating them on an end-to-end basis.

Additionally, in recent years the business has introduced a Microservices architecture, splitting each product offering into smaller, independently deployable packages and hence allowing banks to transition to Temenos on a more granular way, reducing switching risks and implementation costs while enabling them to start benefitting from the integration early in the process.

The group offers four main products, each of them focused on providing coverage for a specific set of use cases and functionalities which are available (a) as SaaS, (b) in the cloud or (3) on-premise.

When serviced via (2), Temenos products characterise by being cloud-agnostic, which means they can run in any of the major data-centre providers (including AWS, Azure, Google Cloud, IBM Cloud, Alicloud and Huawei Cloud). This is a feature which derives from the security and reliance concerns of regulators in relation to cloud banking services, as this model is relatively new.

Temenos has been benefitting from strong tailwinds and consumer demand trends for the last decade, where the relevance of a full digitalisation in the banking landscape has been made evident. This is addressed below in ‘Sector’ chapter.

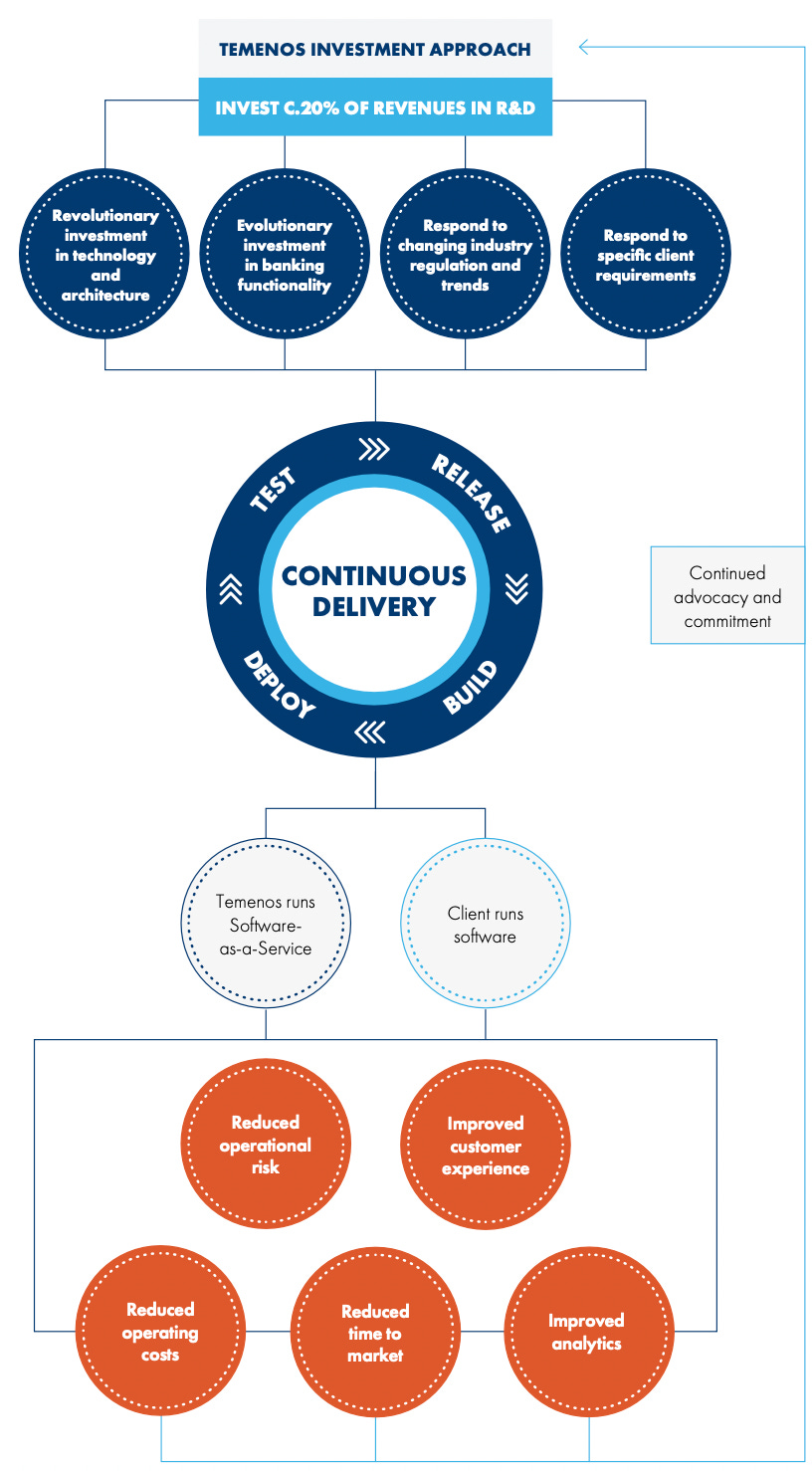

Since 2014, the holding company has maintained a clear, constant vision of key attributes when developing new features and enhancing existing ones on their software. These principles have contributed to elevate flexibility, scalability and profitability in customers’ and own operations.

Temenos products are based on some key design principles which constitute the saint grail in software development and are often interrelated:

Scalability.

Modularity

Openness.

A series of reflections on the implications of these factors is addressed below in ‘Thoughts. Qualitative analysis’ subchapter.

1. Temenos Infinity.

Temenos Infinity is the leading front and middle office software solution in the banking industry, which can be operated no matter the bank office system in place.

It helps banks to engage with their clients -through both digital and physical channels- by running consumer spending analysis, processing transactional data and providing insightful parameters which allow for early detection of customer experience and engagement issues.

The Temenos Infinity platform can be split into three main areas: digital platform, built-in applications and distribution services.

2. Temenos Transact.

Temenos Transact stands out as one of the most complete core banking software solutions in the industry.

At its heart, it allows banks and financial institutions to execute their daily activities and operations in an automated and digitalised way, bearing the associated improvements in operating costs and returns on equity.

According to the company’s information, customers who utilise Temenos Transact in combination with other Temenos offerings achieve cost-income ratios of 26.8% (half the industry average) and increase their ROE up to 29.0% (three times the industry average).

Transact has increased the amount of functionalities and services on a continuous basis, as Temenos spends North than 20.0% of revenues in R&D every year.

One of the most recently implemented (in FY2021) Microservices is Temenos Enterprise Pricing, which enables banks to make the most of Temenos Transact’s pricing capabilities without needing to replace their existing core systems.

3. Temenos Payments.

Designed to provide coverage for ISO 20022, Temenos Payments grants end-to-end management of transactions in an automated way, giving banks full, real-time control over payment operations and integrated customer service experience.

The platform incorporates Explainable AI (XAI) algorithms after the successful integration of Logical Glue back in FY2019 (when it was acquired). The banking industry requires processes to be transparent, this is, to allow for the diagnostics of decision-making processes and typical AI algorithms behave more like black-box systems.

One of the main functionalities embedded into Temenos Payments is the auto-repair Microservice, which increases STP (Straight-Through-Processing) to rates of 97.0% and higher (STP represents the rate of successful transactions completed without requiring manual intervention).

4. Temenos Multifonds.

Temenos Multifonds is specifically oriented to wealth management applications, helping fund administrators, asset managers, insurance companies and pension funds achieve operational efficiency while reducing risks.

As of FY2021, 9 out of the top 15 global fund administrators use Temenos Multifonds for their daily activities.

Services.

Historically, Temenos’ services have consisted of training of digitalisation operators (so called Partners), customer support and maintenance activities.

Nonetheless, for the last decade Temenos has realised about the implications that industry trends like Open Banking would pose to their business and the overall banking sector and, consequently, the company has acted to secure its competitive straight by enhancing not only flagship products but also by developing new platforms and services which (1) place Temenos at the core of the banking industry and (2) ease the future organic growth of the company.

Among Temenos’ service offerings, two stand out as the main pillars for the sustainability of its competitive advantages:

1. Temenos Exchange.

The Temenos Exchange (Temenos MarketPlace before being renamed in FY2021) was launched in FY2015 to allow banks and fintech businesses to benefit from each other.

As the consequences of PSD2 (European directive initiating what would later be known as Open Banking) started to come to effect, traditional banks realised of the relevance that digitalisation would bear to their industry. What this policy entails for the banking landscape is, in simple terms, the obligation to share customer information with third parties when requested by the client.

The PSD2 and its peer policies in other western countries triggered the explosion of fintech enterprises in an attempt to gain market share and disrupt the historically overprotected banking sector.

Nonetheless, the majority of these non-incumbent fintechs soon realised that, although their digital offerings by far excelled in comparison with the traditional banking ones, they lacked a big audience to market their products. Banks and financial institutions were on the opposite side of the spectrum: large customer base but no valuable digital offerings.

Progressively, the latter group’s view on fintech companies has drifted from seeing them as direct competence to partners who they can establish symbiotic business relationships with.

Temenos appreciated this enormous opportunity and is taking advantage of it by (1) marketing the Temenos Exchange platform and (2) introducing an interfacing architecture in their software solutions based on Open APIs.

The Temenos Exchange is a search aggregator where curated fintech companies can offer their products. On the other side, banks and financial institutions can use this service to look for the latest developments and fintech offerings which fit their needs. This allows banks for a fast digitalisation and reduced development and integration times, while enabling fintechs to access a large customer base with minimal marketing expenses.

Temenos publishes their set of Open APIs (Application Programming Interfaces) and offers them as open source code, so any fintech developer may use them to program its solutions.

In essence, an army of already curated fintech companies which are available in the Temenos Exchange develop and market software enhancements which are then easily integrated with Temenos’ native offerings, improving its set of solutions and strengthening its competitive advantage in the banking industry.

2. Temenos Learning Community (TLC).

Temenos’ solutions are integrated at the customers by its Partners.

The Partners are typically digitalisation companies like DXC, Salesforce, Accenture, Capgemini, IBM, Deloitte, Cognizant -to name a few- and so Temenos must ensure that their operators are properly educated and possess the necessary knowledge to integrate its products with other legacy solutions which may be in use at the banks.

This is done via certification processes approved by Temenos after the corresponding Partner has successfully completed a specific set of trainings, depending on the deployment type and scope.

The Temenos’ customer base has grown substantially in recent years -and continues to do so-. Since Temenos strongly relies on its Partner base to cover the required demand for new and existing customers, the company had to find a way to scale its integration and deployment capabilities while reducing associated costs.

The solution finally arrived with the introduction of Temenos Learning Community (TLC) in FY2017, providing digital channels for training, certification, testing, learning and interfacing with other Temenos professionals which can be utilised by its Partners and customers.

The TLC consists of three main applications:

TLC Online:

Cloud-based platform offering hundreds of training modules which are available on a 24/7 basis.

This platform enables customers, Partners and independent consultants to obtain the Temenos Certification.

In FY2021, the number of TLC Online paying subscribers increased by 37.0% over the previous year.TLC Engine:

Cloud-based platform which can be seen as a sandbox where software developers can test their products and operating processes in combination with Temenos products and solutions.

In FY2021, the number of TLC Engine users increased by 50.0% over the previous year.TLC Classroom:

Platform that represents the natural evolution of the traditional Temenos trainings. The main difference with TLC Online is that TLC Classroom accounts for instructor-led-training programs tailored to the client’s specific needs and executed either in a physical or a remote classroom environment.

All three applications are offered freely or via subscription-based contracts for premium content.

Pricing models.

Historically, Temenos offered customers two pricing models for their licensing depending on the deployment type:

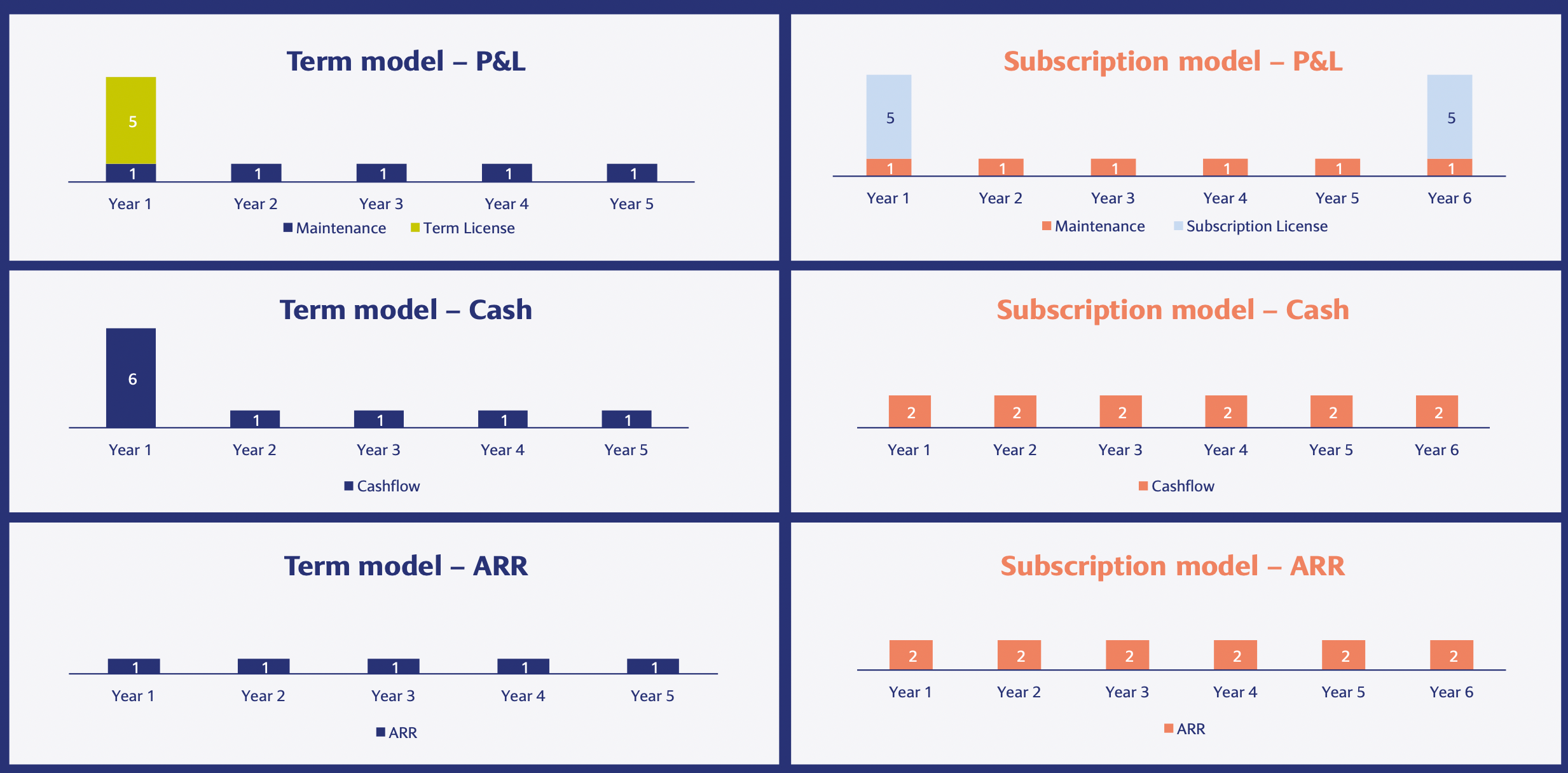

Term-license:

This pricing model is only available to customers for which the deployment is made on-premise, this is, Temenos software runs on the bank’s systems (in-house). The customer then needs to cover all costs related to the installation, operation and maintenance of the hardware and facilities involved.

Typically, the licensing process consists of five year contracts where the principal payment (non-recurring revenue) is made on the first year. Additionally, these agreements include a minor part which is payed on a yearly basis for maintenance services (recurring revenue).

An important KPI for term-license pricing schemes is DSO (Days Sales Outstanding) per annum, which measures the amount of days elapsed, on average, since a sale is competed until the associated revenue is collected.

DSOs have been decreasing at a pace of 10-15 days p.a. since FY2014.Subscription:

A subscription-based pricing model has been historically the way to go for customers who choose to run the software either as SaaS or in the cloud.

Although the duration of these contracts is also five years, the revenue stream is recurring on its entirety. The bank transfers on an annual basis both licensing and maintenance related costs to Temenos.

Additionally, all subscription contracts at Temenos are CPI protected.

This is likely the single most important point around the investment opportunity in Temenos today (August 2022), since the company announced at the end of FY2021 that customers running the Temenos platform on-premise will get the freedom to transition from term-license contracts to subscription-based ones.

As of FY2021, on-premise deployments accounted for 70.3% of total software licensing sales (or 30.2% of total revenues).

More on the implications born by this decision and how banks are reacting so far (H1 of FY2022) is included in ‘Thoughts. Qualitative analysis’ subchapter.

Thoughts.

Qualitative analysis.

As mentioned earlier, some of the best practices and design specifications for efficient programming and software development are:

Scalability.

Modularity.

Openness.

It is pivotal for most programs, applications or software solutions to be scalable, this is, being agnostic to whether one client or a million are using them. When this happens, their set of functionalities are typically based on generic principles which remain unchanged across multiple use cases or verticals.

Once achieved a highly scalable product or service, operating leverage automatically enters the equation when revenues increase.

This is the case for Temenos’ solutions.

Scalable software is often achieved via smaller, generic and modular components which can be reused across the implementation. When properly defined, they may even associate to build bigger and more complete modules which execute more specific tasks.

This is the case for the Microservices included in the Temenos’ offering.

This software architecture enables Temenos, along with its Partners, to deploy the entire platform bit by bit, module by module, in a way which (1) decreases integration downtimes, (2) considerably reduces the risk for a customer when switching its core banking application, (3) allows the bank to run function-specific systems which may be desired to keep internal (due to IP legacy, for instance) and (4) enables the bank to start benefitting from Temenos’ software earlier in the digitalisation chain.

Finally, openness. We live in an interconnected, globalised world and, although the banking sector is probably one of the highest regulated ones (specially after ‘08) and hence not the most eligible to experience major changes, recent drifts in western policies have trended the industry towards what is nowadays known as Open Banking.

With the release of PSD2 in Europe in 2015, Temenos launched its Temenos Exchange platform to ease the access to fintech developments by their customers, creating a symbiotic effect while placing itself at the core of the fintech enhancements in the banking industry.

By adding an Open APIs based architecture to the described Microservices, the result is a highly flexible and easily scalable core of software solutions which benefits from multiple external developments that are integrated with Temenos’ offerings at zero cost.

As the post-PSD2 banking industry matures, Temenos is placed at its core to benefit not only from its traditional offerings but also from fintech developments and bank outsourcing activities.

As of FY2017, the Temenos Learning Community (TLC) has also come to effect, increasing Service margins from 9.7% to 13.1% in FY2021. This is likely to continue as Temenos scales its sales, deployments rate and, consequently, its Partners base.

Some of the more recognisable competitive advantages of the business are:

Network effects:

The Temenos software investment approach forms a virtuous cycle in which its customers (banks and financial institutions, mainly) influence Temenos’ investment decisions (R&D) and therefore benefit from the improved product.

This, in turn, contributes to their success. The customers then advocate for Temenos’ solutions, enabling the company to attract more clients and gain reputation in the industry, continuing the cycle.

These network effects are accentuated by the introduction of the Temenos Exchange, where more fintech developments attract banks to subscribe to the service, which in turn drives up demand and more developers seek to enrich the platform’s offerings.

Switching costs:

Banks and financial institutions base their day-to-day operations on Temenos’ solutions.

The associated costs (specially in subscription-based pricing models) are negligible in relation to the overall value provided by the software. This creates an environment in which taking market share from competitors is extremely difficult, since the downside risk that a bank faces in such situation outweighs (in most cases) the potential benefits of the new system.

On the other hand, Temenos can afford gaining market share more easily than other banking software providers in the industry as a consequence of its Microservices-based, cloud-agnostic offerings, which reduce integration costs and switching risks for new customers.Pricing power:

With the recent drift towards subscription licensing on the on-premise deployments, ARR is expected to grow at c.15.0% CAGR over the next five years.

All subscription contracts at Temenos are CPI protected, so the company is better positioned to take advantage of price increases over the years which, combined with the high switching costs that characterise the core banking software sector, creates a powerful leverage for Temenos’ financials.

In FY2021, term-license revenue accounted for nearly 100.0% of the on-premise software licensing sales, which represented 30.2% of total revenues.

As of Q2 FY2022, this non-recurring revenue stream represents only 51.0% of the on-premise software licensing top line, which seems to indicate that banks are welcoming the new subscription-based pricing model.

This should not be surprising, since Temenos’ customers benefit from this new scheme by (1) facing lower upfront costs (allowing a shift to OPEX from CAPEX and hence making the most of the time value of money), (2) easily scaling based on demand, (3) gaining access to more flexible maintenance possibilities and (4) easier path to SaaS.

At the same time, although the shift to the new subscription-based pricing model for the on-premise deployments will definitely impact the cash inflows in the short term, over the long run it poses high benefits for Temenos by (1) significantly expanding long-term value creation through incremental growth, margin expansion and cash flows, (2) accelerating the drift to a more predictable revenue stream and financial performance (higher weight of ARR on top line), (3) increasing total contract values (TCV), (4) greater upsell opportunities (utilising pricing power) and (5) improving customer retention rates.

The illustration below shows how a drift from a term-license to a subscription-based pricing scheme affects the P&L, cash-flow statement and ARR for a business like Temenos:

Notably, the P&L is not impacted (apart from the renovation of the subscription at contract end) since IFRS demand that revenue from the sale of a product or service is recognised at the start of the contract.

Cash inflows, on the other hand, are annually split across the total duration -five years- of the subscription contract.Since the subscription licensing revenue is considered recurring, as a result ARR accounts not only for Maintenance payments, but also licensing stream.

Scale:

As of Q2 FY2022, 41 out of the top 50 global banks are Temenos’ existing customers. The company operates worldwide, with a special focus on gaining market share and consolidating its strength in the key banking markets: US, Europe and Australia.

The more customers in different regulations using Temenos’ solutions, the more complete its software becomes. This, in turn, elevates the amount of functionalities that customers from different banking systems get, since regulatory trends in the main developed markets gravitate to go hand in hand.

Temenos closely monitors new potential changes from regulators in the markets where their platforms are offered, which allows them to (1) adapt rapidly to these modifications and (2) enable the enhancements to be ready for the future adoption of the same trend in other jurisdictions.

With TLC, Temenos can afford to scale its deployments rate while improving its Service margins, since most of the trainings and certifications take place in an automated, digital manner.Reputation:

The banking industry is one of the most difficult to penetrate sectors due to its highly regulated environment and competitiveness.

Over its 29 years of continuous development and software enhancements, Temenos has built a reputation which protects it from non-incumbent competitors. Once a company possesses a compelling product, most of the contracts are gained on the early stages of the negotiation and being sat at the table at that moment is commonly achieved based on reputation.

To be continued… (at @ConserValue in Twitter).

Will link the complete .pdf over there.

Cheers.