One fund, One objective & Simplifying investment choices

One fund, One objective & Simplifying investment choices

Thinking about Position Sizing and How I arrived at one fund alone.

For the purpose of simplicity, I am only focusing on Pure Equity investment within this post (excluding Equity arbitrage/ equity balanced fund, etc).

How many equity funds do you own. A typical investor must be carrying about 7-10 equity funds on an average, whereas few even may have upward of 20 funds+. Very rarely you will find someone to be investing in 1-2 equity mutual funds.

Why?? I am sure you have heard a lot of these reasons

Large Cap, Mid Cap, Small Cap, Satellite portfolio, Thematic fund, NFO, international funds. 350 Different funds, I don’t know what to choose.

My Advisor asked me to pick 2 funds from each category. A perfect potpourri you know.

This fund performed well this year/ This fund is not performing, hence stopped SIP in X and Started in Y

Twitter talks about this fund

All financial wellness apps suggest a portfolio of few funds

I have SIP running in different funds for different goals (Makes My Mental allocation easy)

Diversification is something I read is important in equity investing

But international is where returns are, I need international diversification. Fund added

My friend invests in this

I like the IT/ digital theme fund ( Shh.. they show the highest return on last one year in all APPs)

So and so forth, the investors have numerous reasons for adding various funds from various fund houses and then managing/ hopping one from another/ disappointment and celebrations over fund performances and whatnot.

And all of this when your equity allocation may not be even 50%. An average Indian portfolio may not be 70% equity but more tilting towards 25%.

This is one of the biggest dichotomies of Indian Investors. Given that chances of Equity returns to be far higher than gold/real estate is far more, yet the average allocation to equity would be sub-optimal and on top of it, so much of time is spent buying various funds trying to maximize returns.

Refer to various examples of allocation and expected returns from your portfolio if you have to arrive at 10% CAGR.

The example below is 100 Rs invested for 20 years with various allocation/return assumptions. (Excluding rental/dividend/taxations)

Now unless your equity position is not the highest (assuming Equity returns are far higher than other asset classes), your return from equity has to go upward of 12% to achieve a meaningful cagr of 10%.

Lesson: Take a portfolio view and set up what you wish to achieve from your portfolio component. If you are too little invested in equity, then you will need more returns, and mixing and matching various funds may not even yield that for you. On the other side, if you are 75% in equity, then perhaps an index giving 11.5% also will help you achieve your goal.

So before you jump into buying various funds, assess where your equity allocation is.

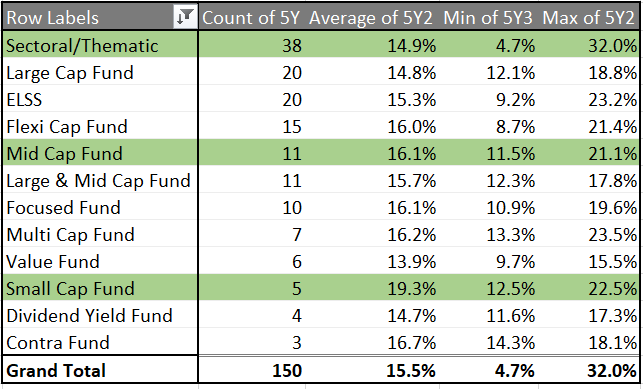

Potpurri of funds: 5-Year Return as of 27th August 2021 (lump sum)

Here is a 5-year return of all kinds of equity funds (Except Fund of fund/index).

Will you put 100% of your money in Sectoral funds or Mid-cap funds of small-cap funds. If you have put 100 Rs in any of these 3 categories with an equal amount in all the funds available in that particular category, you would have made 14.9% (Thematic), 16.1% (MidCap), and 19.3% (Small Cap). Splitting it 33% each also would have given you 16.9% returns with some 92 funds in your portfolio:)

Let’s say you could buy 100% of all funds in equal proportion, then also you would have made 15.5%. Barring Small-cap, all other themes are more or less giving returns equivalent to any other category return. (Avg of all funds in a particular category)

The question is would you have put your 100% of EQUITY MONEY in any of the SINGLE categories of fund (by buying all the funds available in that category in equal split)

Perhaps No!! if your equity portfolio is upward of 50%.

Perhaps yes, if your average Equity weight in the overall portfolio is <=20%. Remember, finding out which fund is equally troublesome, hence you end up buying all the funds in the category.

Another one

Would you put 100% of your equity money in the best performing Sectoral/Midcap/Smallcap fund for the last 5 years, you would have received 32%, 21%, and 21%, but how and where to find that fund:).

Hindsights are easy, hence the present levers to find that funds can not be subjective parameters but only performance indicators.

Enters Risk

It’s very prudent as well evident that none of the investors perhaps will put all his 100% money in one small-cap fund or midcap fund or sectoral fund given, the extreme volatility and gut-wrenching time periods when they underperform/ behave like a roller coaster.

To reduce the risk, the financial advisory provides solutions by doing 2 things.

Your asset allocation. Bring Equity down to 30% and your overall risk, in any case, is mitigated.

Add few large caps, a few mid-caps, few small caps, few international funds and you have reduced volatility.

The choices that I have made to invest in one fund stemmed from the following thoughts with the purpose of REDUCING RISK of the EQUITY component as compared to other Equity Choices.

Should not be a specific cap. Should be a mix of all caps.No Restriction of Capping weightage. (Removes mid-cap only/small-cap only/ sectoral/thematic etc etc ). It gives a fund house to navigate anywhere for opportunities.

Should be investing internationally. Globally diversified option (Reduces the need to buy international funds, whose taxation is treated as debt fund)

Should be value-conscious/able to take the cash calls if the market seems to be heated. (a fund going into cash/waiting for the right time to invest clearly says that every new penny I invest, needs to be assessed on the long-term potential as of today.

Should have skin in the game. It increases my confidence in fund philosophy given they are investing their own money into it.

My Assumption of long-term return from Equity is not 18%. I need 10-12% to reach all my goals. Hence, anything with a higher probability to beat 10%-12% works for me.

Results of Flexi cap in last 5 years

Here is a brief overview of all flexicap funds in the last 5 years

A basket of all flexicap funds would have beaten any other basket of funds (except 100% small-cap)

A flexicap is nothing but an amalgamation of various types of stock caps as per the market situation.

The fund that I have chosen is the Parag Parikh Flexi Cap fund.

My overall equity investment is about 77%. 80% of that is in PPFCF and 20% in ITC.

#One Stock #One fund

The fund meets up all the criteria for me to focus as a single entity and over years as I studied more and more about the fund, I cashed out of all other mutual funds to simplify my equity investments.

My first investment was in this fund in March 2018 and by September 2019, 100% of my equity mutual fund investment shifted to this fund.

A mix of Indian and global stocks (Checked)

Cash Calls in the fund (Checked). This fund generated the number of returns despite being at in CASH level as high as 27% in October 2018.

Skin in the game

Few questions may come up

By being globally diversified, we are not playing the India story? That’s not true.65% is a big enough number to play India's story. Remember stock is stock. Eventually, all an investor cares about is where the 10-12% cagr comes from. Why can't it be “ the best companies of the world with large TAM”. You can choose not to play the GLOBAL diversification part but ignoring companies especially in the DIGITAL space with a market size equivalent to GLOBE, a lot has to go wrong for these companies for your fund to perform real bad

Manager risk: Remember a fund does not stop behaving badly immediately. There is a lot of processes a fund follows, while this risk remains, but diversifying, for this reason, is sometimes quite overplayed.

Diversification with 20-30 stocks versus 80 stocks: Historically, a concentrated portfolio with few winners is what makes a fund perform toward the alpha creation. More important is the size of that bet (POSITION SIZING). For example, AMNZ being 9% is the BET whose 10X in the next ten years will matter more as compared to Mahindra holidays 2% whose 10x in 10 years may not mean too much to a full portfolio. Of course, there will always be some laggards. If the average holding pattern of your fund mirrors the index on an%age basis, then more or less, the returns will be similar largely unless the fund takes a lot of cash calls at the right time.

While I am not recommending anyone to follow the path I have taken but do find out the purpose of every fund in your portfolio and see how it reduces decision making. The same rule applies to DEBT funds.

Active versus passive debate

Guess, I am still convinced that alpha exists in a globally diversified market and a careful selection of 25-30 odd stocks. It's about making fewer mistakes rather than being right more times.

Tweet @crazynaval

Nicely written

Would like your review of PPFAS Conservative hybrid fund.