#25 Geoeconomics in Geopolitics

#25 Geoeconomics in Geopolitics

US Capital imperfections - China Socialism efficiency

I] INTRODUCTION

A multidimensional approach to solidify its sole hegemonic power - within an imperial hubris - the U.S. attempts through tariffs, financial and technology sanctions, political provocations to - and military maneuvers near - Taiwan and an encirclement of China, whilst threatening to ban Huawei and Tik Tok: now is a time to dissect the imperfections of a capitalist economy when competing with a state-run socialist model like China.

The U.S. cannot dismember a civilisation state; it tries, therefore, to damage China’s economy upon goading her to voluntarily commit economic suicide by implementing policies that will damage the country. Deeply-funded resources are used to spread false news regarding China’s economy:

“The economic model that took the country from poverty to great-power status seems broken, and everywhere are signs of distress“, Aug. 20, 2023 wsj

OR

Xi’s Age of Stagnation : The Great Walling-Off of China, Foreign Affairs, Sept/Oct ‘23

Another concurrent goal is to persuade Third World economies not to learn from China’s economic success — because any acknowledgement of the practicality that China’s socialist economy is more efficient and successful than capitalism would be a devastating ideological blow to the U.S.’s rule-base assumptive international order.

Arguing that capital enhancement is economic efficiency of capitalism – but ignoring super-exploitation in the continuance capital accumulation nor indicating the extracted value from labour (see Storm, May 2023, Labour exploitation and Capital accumulation factors; Storm, August 2023, Dependency and super-exploitation) - has U.S. perpetuated a claim of the “inefficiency of socialism”. That an alternative but efficiency economy integral to the socialist character of China’s economy is often debased.

Similarly, that an alternative politico-economic praxis can serve to re-orient the Madani Malaysia model narrative nuances, is ignored, too, (Storm,May 2023 and June 2023), especially when state of a nation under the clutch of IMF neoliberal policies is neoimperialism, (Storm, May 2023, Economic growth, retarded development).

We shall be applying John Ross main arguments, supported by data points from the World Bank’s World Development Indicators, U.S. Bureau Economic Analysis, and China National Bureau of Statistics – to show that Socialist China’s investment is much more efficient in creating growth than in capitalist countries such as the U.S.

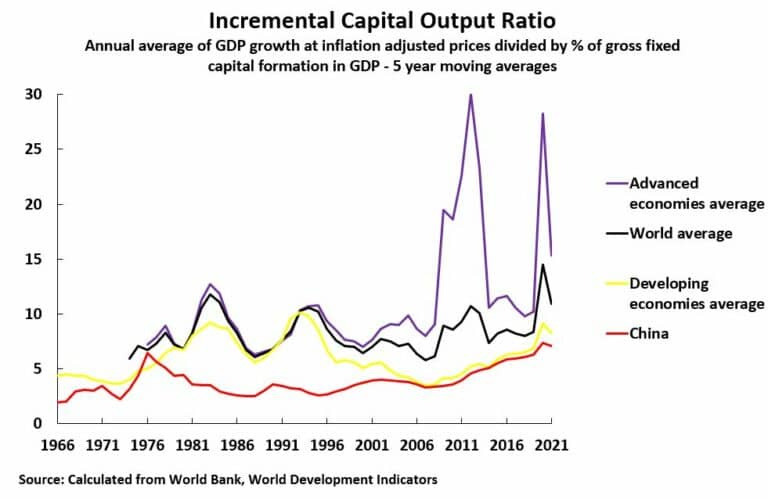

II] INCREMENTAL CAPITAL OUTPUT RATIO ( ICOR )

The factual situation regarding efficiency of fixed investment in generating economic growth is shown in the Table below — which portrays the world’s 20 largest economies ICORs (where Incremental Capital Output Ratio – is the additional unit of capital investment needed to produce an additional unit of output, generating subsequent increase in the gross domestic product of a nation).

If the Eurozone as a whole is also included with South Africa, so as to include all BRICS countries, then the Table shows the ICORs for these economic regions account for 83.9% of world GDP, that is, for all economies which have a major impact on world growth.

Taking a five-year average (thus avoiding short-term business cycle shifts), China had to invest 7.1% of GDP to generate 1% of annual GDP growth. This is characterised by China’s investment extremely low ICOR comparing with other countries. This aspect indicated China’s extremely high efficiency in generating economic growth; she was the second best out of the world’s 20 largest economies.

In particular, China’s ICOR of 7.1 was more efficient than the US’s 10.0, the Eurozone’s 22.4, Germany’s 30.3, the U.K.’s 70.1 — not to mention Japan’s negative ICOR number: an economy which contracted despite its investment.

III] Comparing to the emerging and developing countries:

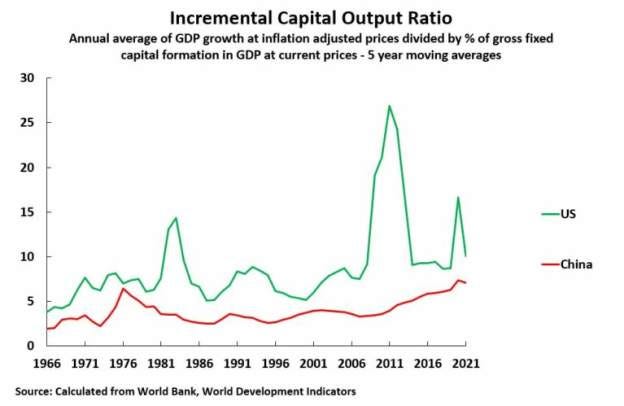

IV] Comparison with the U.S.

Comparisons conducted between China and the U.S., the ICORs for the two countries are shown in Chart 4.

As indicative, China outperforms the U.S. in the efficiency of investment in generating growth in all periods.

How has China’s efficiency of investment in producing economic growth changed relative to other current economies at a similar stage of development.

The factual factor is clear.

China’s efficiency of investment in terms of international comparisons is extremely high — in particular, superior to the U.S. Europe and Japan, as well as compared to other developing countries.

Therefore, after elaborating upon the above situational circumstances, and after having established the factual events, a reasonable question to enquire lays on why is China’s investment so efficient?

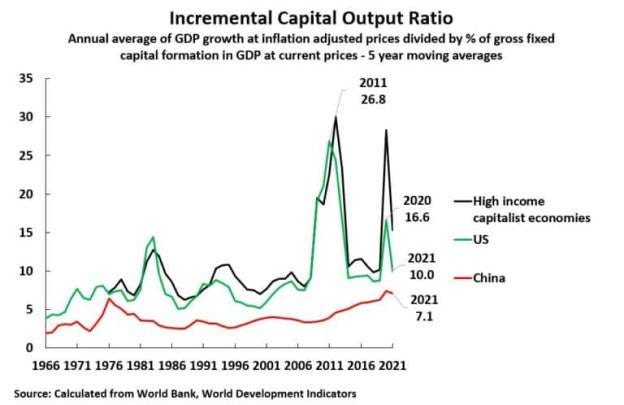

V] SOCIALISM IS EFFICIENCY

It is clear that the main reason for China’s very high efficiency of investment is due to the socialist character of its economy (Boer 2021) with an anti-crisis macro-economic strength. This fundamental process in ICOR can be discerned from Chart 5 below that shows the worsening of U.S. ICOR indicating the efficiency of its investment was not a smooth process at all.

There are two specific periods of huge deterioration that they affected average efficiency of US investment over the entire period. These were a more than doubling of ICOR to 26.8 in the period leading to 2011 following the international financial crisis, and a rise to 16.8 in the period leading to 2020 in association with the Covid induced recession.

In short, economic crises led to a sharp worsening of U.S. ICOR, to a severe fall in her domestic investment.

To illustrate clearly the long-term cumulative effects of such crises, and to smooth out the extreme short-term spikes, Chart 6 shows a longer term, 10-year, average for U.S. and China’s ICOR. The long-term cumulative worsening of U.S. ICOR under the impact of its successive economic crises is clear. In short, the fall in the efficiency of U.S. capital investment was particularly associated with capital crises in the U.S. economy.

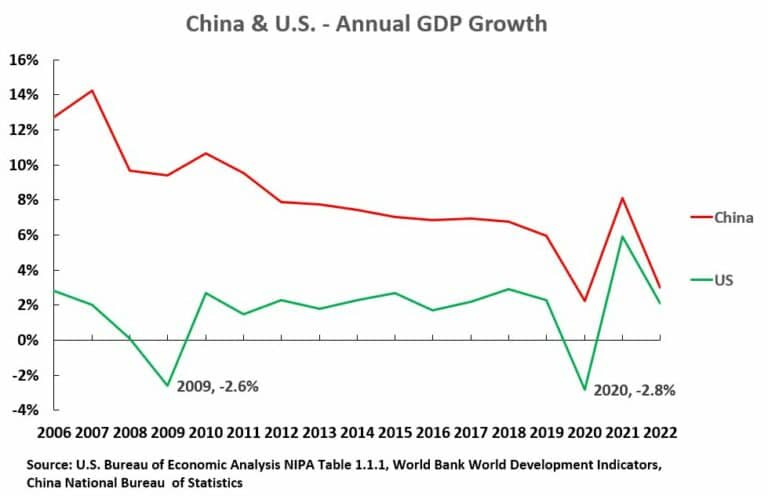

A) America economic slowdown and rising ICOR

This process of economic slowing is shown in Chart 7. The U.S. went through two sharp recessions with negative growth — economic contraction of 2.6% in 2009 and of 2.8% in 2020.

The contraction of the U.S. economy in crisis years sharply slowed its average growth rate and therefore raised its ICOR.

Consequently, the U.S.’s much weaker anti-crisis macro-economic capacity than China explains the superiority of China in efficiency of investment compared to the U.S. and is the primary explanation for the deterioration of U.S. ICOR — that is, for the worsening of the efficiency of U.S. investment.

B) The fall in US investment

Consumption is at a higher GDP percentage than fixed investment in the U.S. As an instant, in 2007, on the eve of the international financial crisis, consumption was 82.5% of U.S. GDP compared to 22.3% for fixed investment.

These fluctuations in the U.S. investment economy are so much more violent than the fluctuations in consumption which create its recessions. This may easily be seen by looking at the following fact:

Between 2007 and 2009, the latter being the worse year of the U.S. recession created by the international financial crisis (or sometimes known as the Great Financial Crisis {GFC'07}) , then overall U.S. GDP declined by 2.5% adjusting for inflation. The inflation adjusted fall in U.S. household consumption, which accounts for 82% of total U.S. consumption, was 1.5%.

However, the inflation-adjusted fall in U.S. private fixed investment, which accounts for 82% of U.S. fixed investment, was at 27.6% — almost twenty times as severe as the fall in consumption.

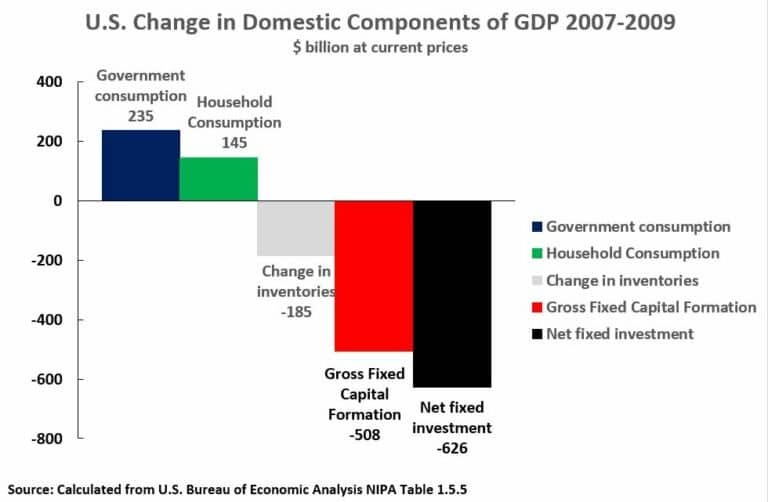

Chart 8 shows that, in current prices, between 2007 and 2009 U.S. household consumption rose by $145 billion and U.S. government consumption by $235 billion — a total rise in consumption of $380 billion. However, it must be emphasised that this increase in consumption was more than offset by $508 billion fall in gross fixed capital formation. That is, the post-international financial crisis recession was overwhelmingly created by the fall in investment, not in consumption.

Moreover, depreciation of fixed capital during this period was $119 billion. Consequently, the fall in U.S. net fixed investment was even worse than that of gross fixed investment — a decline of $626 billion. Therefore by 2009, the U.S. capital stock was lower than in 2007, lowering U.S. potential for long term growth.

Summarising,

The U.S. recession after 2007, and therefore the worsening in U.S. ICOR, was due to the fall in U.S. fixed investment during the international financial crisis after 2007.

The US capitalism economy means its dynamic is determined by decisions of private capitalists. If these capitalists decide not to invest the economy goes into a tailspin into a recession (producing an increase in ICOR).

In short, there is no equivalent U.S. state sector sufficient to offset this. Private ownership of all the main means of production in the American national economy only ensues and ensures weakness in the U.S. macro-economic crisis mechanisms.

B) China’s anti-crisis macro-economic mechanisms

In contrast to the U.S., the Chart 9 shows what occurred in China in 2007-09, even when faced with the international financial crisis.

In 2007 to 2009 China’s GDP, in inflation adjusted terms, rose by 20.0%. At the same time, China’s gross fixed capital investment rose more rapidly than any other major component of GDP — increasing by $890 billion, compared to $511 billion for household consumption and $233 billion for government consumption. China’s fixed capital depreciation in this period was $356 billion.

Therefore, China’s net fixed investment rose by $534 billion. China’s capital stock was significantly greater in 2009 than in 2007, increasing its potential for long term growth – in direct contrast to the U.S. trend, and a contradiction to US capitalism mode.

In summary,

That China’s large state-owned sector gave it much stronger macro-economic anti-crisis mechanisms than the U.S. capitalism mode.

That China suffered no decline in output in any year during the international financial crisis.

That the strength of China’s state sector, by preventing a fall in investment, which prevented recession and ensured China’s superior ICOR to the U.S.

That China’s fixed investment did not fall is because of being a socialist economy with a large state sector and state-owned banks which entirely dominate its financial system.

That the macro-economic strength given to China by its state sector thereby ensured the high overall efficiency of China’s investment in generating growth.

C) The Covid and China Investment

A reason that China’s overall investment could remain high was also due to the large size of China’s state sector.

To be precise in making a comparison to the U.S., in 2022 only 16%, less than one sixth, of U.S. fixed investment was in the state sector, accounting for only 3.4% of GDP.

Given this extremely small size of the U.S. state sector even a very high percentage increase in U.S. state investment would be unable to prevent overall U.S. fixed investment from falling. Indeed, to offset a 10% decline in private investment U.S. state investment would have to pump up by 50%. In comparison, China’s large state sector means it is possible to stabilize China’s investment level with much lower increases in state investment.

In short, China’s large state sector is an extremely powerful anti-crisis mechanism. This, in turn, because it sustains economic growth, prevents the type of severe crisis increases in ICOR seen in capitalist economies such as the U.S.

Chart 10 shows that China’s economy far outperformed the U.S. during the pandemic period. In the three years 2019-2022 China’s GDP grew by 13.3% compared to the U.S.’s 5.2%. That is, during the pandemic China’s economy grew by more than two and a half times as fast at the U.S. capital investment.

D] The stabilizing role of China’s state investment

The reason for the high contribution of fixed investment to China’s GDP growth during the pandemic period is shown in Chart 13 whereby China’s state investment, during a crisis, could be used to offset the decline in private investment.

CONCLUSION

The reason that China’s overall investment could remain high was only due to the large size of China’s state sector. Whereas U.S.A. in 2022 only 16%, less than one sixth, of U.S. fixed investment was in the state sector, accounting for only 3.4% of GDP.

Given the extremely small size of the U.S. state sector, even a high percentage increase in U.S. state investment would be unable to prevent overall U.S. fixed investment from falling. Indeed, to offset a 10% decline in private investment U.S. state investment would have to pump up by 50%. In comparison, China’s large state sector means it is possible to stabilize China’s investment level with much lower increases in state investment.

China’s large state sector, therefore, has a powerful effect in keeping China’s ICOR down and maintaining a high level of investment - and economic growth - efficiency.

An indepth, and wider, discussion on Capital Imperfections and Socialism efficiency economic model can be found HERE -with additional references, graphs and cited links.