Subservient to Subsidies: Part II

Subservient to Subsidies: Part II

under a financialisation capitalism regime

The concluding part of a two-part series; Part I is available HERE.

3. CONCLUSION

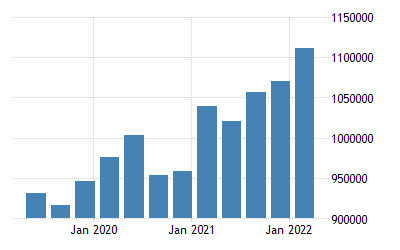

The undeniable fact as to why many bumiputera had not attained parity despite +65 years of neo-liberal-enforced economic development is the existence of a new class of compradore capitalist. According to the UNDP 1997 Human Development Report, and the 2004 United Nations Human Development Report, Malaysia has the highest income disparity between the rich and poor in Southeast Asia, greater than that of Philippines, Thailand, Singapore, Vietnam and Indonesia. From past performance, one can safely say that the future capital-led vehicle on an uneven route ahead is going to be calamity in crisis with government direct and statutory debt going up:

In addition, the economic downturn challenges emerging countries capacity to service their existing debts. Therefore, despite widespread concerns about the current escalation of public debt and its sustainability, we should not lose sight of the potential risk from possible surges of private debt, too.

The Malaysian Federal Government Debt and liabilities rose to RM$1.2569 trillion, or 87.3% of GDP, by end-September 2020 – up 7.5% in the first nine months of that year compared with RM$1.1692 trillion as at end-2019. Indeed, country’s revenue is not rising as fast as the increase in operating expenditure that is more than 95% of revenue since 2008. Assuming the economy is set to expand by 7.5% in nominal terms during 2021 to RM$1,521.3bil, Malaysia’s official debt to GDP and total debt to GDP is expected to rise to 64.1% and 77.9%, respectively.

[It is a fact that governments in high-income developing countries are often unable to issue long-term government securities at a sustainable rate of interest, yet they need to be able to pay off or roll over maturing short-term obligations.

In the case of Malaysia, our total debt service is the sum of principal repayments and interest actually paid in currency, goods, or services on long-term debt, interest paid on short-term debt, and including repayments (repurchases and charges) to the IMF].

With the national household debt-to-Gross Domestic Product (GDP) ratio had already surged to a new peak of 93.3% as at December 2020 from its previous record high of 87.5% in June 2020, according to Bank Negara Malaysia (BNM), Malaysia’s debt-to-GDP ratio could stabilise at 65.5% in 2022, but the outlook for the country’s fiscal policy is highly conditional upon the growth recovery this year. Though current household debt to GDP is at 89% as at December 2021 as compared to 89.6% in June 2021, it remains on the higher end when compared to regional economies such as Singapore (69.7%); Indonesia (17.2%); Philippines (9.9%).

Moody’s assistant VP and analyst Nishad Majmudar said the outlook for Malaysia’s fiscal policy is highly conditional upon a good growth recovery. The political-economic scenario is not that as fortuitous as projected by the Finance Minister. Research For Social Advancement (Refsa) and the Malaysian Institute of Economic Research (MIER) agreed that any stimulus must be at least over RM$90 billion.

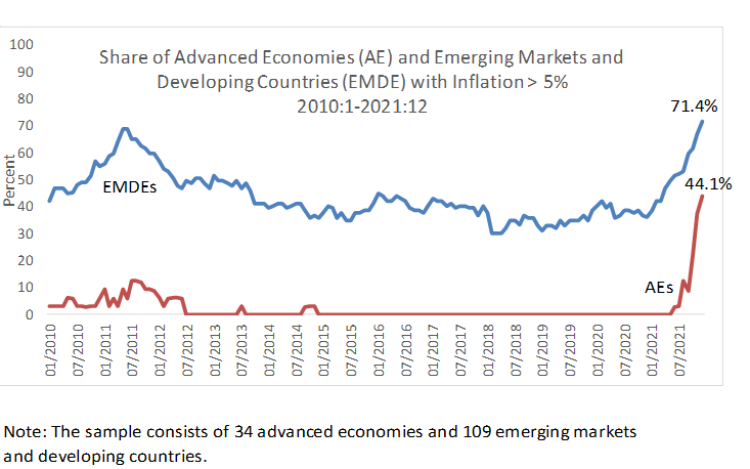

This allocation is a minimal because rising energy prices and supply disruptions have resulted in higher and more broad-based inflation than anticipated, notably in the developed countries in the Global North and many emerging market and developing economies. The IMF World Outlook July 2022 has indicated in its report whereby inflation is leading to acute uncomfortable trend in the emerging markets and developing economies (EMDE):

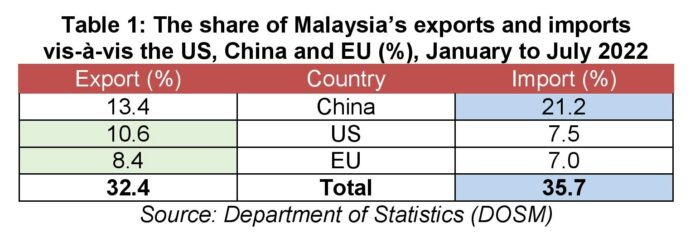

As a country depending on three main trading partners where the US and EU are experiencing profound inflation flights, and China under a supply chain bottleneck,

the resultant depreciation of the Malaysian ringgit is expected. On 26th September, 2022, the ringgit dropped to RM$4.60 to US$ - the value of ringgit is worse than Sept 2015 during the peak of the 1MDB scandal and the 1997 Asian Financial Crisis.

Indeed, the IMF advice is that EMDC would require judicial use of macroprudential tools and making reforms to debt resolution frameworks all the more necessary.

Our tool box is rather limited in the forthcoming Budget 2023 since the restructuring of the national economy was not adequately executed post-Asian Financial Crisis in the 1990s which coincided to follow a program in premature de-industrialisation towards a financialisation capitalism mode. Likewise, the limited economic policies will entail, and only should be offset, by increased taxes and or lower government spending.

The tax rate for the top income bracket in Malaysia is a low 25%, compared to other Asian countries such as Korea (38%) and Thailand (35%).

Howevet, World Bank Group lead economist Richard Record had indicated that Malaysia has already depleted much of its available fiscal space and would emerge from the current covid-19 crisis with a larger burden of debt and contingent liabilities.

This scenario is compounded by contrary to net foreign inflow of RM$6.1 billion in Malaysian equities year-to-date, the local bond market recorded net foreign outflow of RM$3.23 billion. Heightened uncertainty and tightening global financial conditions have contributed to portfolio outflows from domestic bond markets and reduced inflows into the equity market in recent months. By April, 2022, non-resident outflows from domestic bond funds amounted to RM2.2 billion (March 2022: RM4.0 billion), while inflows into the equity market declined from RM3.3 billion in March to RM0.8 billion in April, (World Bank Economic Monitor on Malaysia, June 2022).

It is the expectation that more money one borrows, the harder it is to pay it back and the higher your likelihood of default. The greater risk is that by pumping more money into the economy, the government will fuel further inflation.

Typically, when inflation is high, Bank Negara Malaysia (BNM) will set about undoing these actions by tightening monetary policy, and markets will make you pay with higher bond yields. Boost the economy with borrowed money, and you will see the gains clawed back by higher interest rates. The resulting economic contraction and inflation will erase whatever economic gains through “freebies and free lunches” through subsidies.

Always remembering that subsidies stimulus is a class war waged against the 99 per cent by the elite 1 per cent. Often the money extracted from the working class through inflation is transferred to the rich as subsidies and tax cuts to promote capital accumulation.

Part II of a two-part series; Part I is available HERE.

First published in STORM, 22nd July 2022, by the Collective on GeoEconomics; and, updated with new data herein, reposted under Creative Commons.

RELATED:

INDEBTED THROUGH AND BY NEO-IMPERIALISM

Monopoly Capital: Debt and Stagnation under Financialization Capitalism

Thank you for visiting and reading On Geoeconomics. Subscribe for free to receive new posts & articles: