The use of the Treasury, to protect banks from realising losses

The use of the Treasury, to protect banks from realising losses

Understanding The Relationship Between Treasury Bonds, Collateral, and Liquidity in the Financial System

In the world of finance, Treasury bonds and bills play a critical role in providing collateral and ensuring liquidity within the financial system. This article will explore the relationship between Treasury bonds, collateral, and liquidity, with a particular focus on government spending, Basel III regulations, asset allocation, and Tier 1 capital.

By understanding, first, the BIS report on the March 2023 banking crisis highlighted on “Section 1, unrealised interest rate losses on fixed income assets held at amortised cost was

an important driver in the failure of several banks during the recent turmoil. If banks need to sell such securities before their maturity date to meet liquidity needs, unrealised losses on those securities become realised losses and reduce both equity and regulatory capital. Moreover, the large-scale and ad-hoc firesales by some troubled banks to meet large-scale and simultaneous deposit withdrawals may also require reflection on how best to reflect the risks from second-round fire-sales. This, in turn, raises two

issues”.

Second, the solution as highlighted by the BOE, “The global financial crisis has highlighted the need for central banks not to tighten collateral policies in the face of market stress. Such a strategy can provide certainty to counterparties when constructing their funding strategies. Some central banks have found that there are benefits to loosening collateral policies in times of severe stress. An easing of central bank collateral policies may free up market strains on high-quality collateral”.

It is my goal, to use this article to bring together, both reports from the BIS and BOE, and conduct a deep drive into the relationship between Treasury bonds, collateral and liquidity in the financial system. Explaining why I think government spending is possibly strategic, in that it is supplying the financial system with an oversupply of collateral, which is needed to protect it from Commercial Real Estate (CRE) and interest rate risks. The goal is to ensure an efficient amount of liquidity in the financial system, ensuring banks don't have to realise losses on their portfolio and ensure loan to maturity. Which is the main reason for the bull run from October 31st.

Collateral and liquidity explained

The process of how a bank acquires liquidity from central banks involves the use of the Discount Window and reverse repurchase agreements (reverse repos), with collateral playing a vital role in securing the liquidity.

Collateral is essential in the discount window and reverse repo transactions to mitigate the risk for the central bank. The central bank holds the securities as collateral until the reverse repo matures or is terminated. This ensures that the central bank has assets to rely on if the bank fails to fulfil its repurchase obligations. That's know explain exactly what each one is:

1. Discount Window

The Discount Window is a facility provided by central banks where commercial banks can borrow funds directly from the central bank, usually as a last resort. Banks can access this facility to meet their short-term liquidity needs. The borrowing rate at the Discount Window is typically higher than the market rate to discourage banks from relying on it excessively.

To access funds from the Discount Window, a bank submits a request to the central bank, providing information on the amount of liquidity needed and the reasons for the request. The central bank assesses the bank's financial condition and determines whether to provide the requested funds.

In this process, collateral plays a critical role. Banks are required to pledge eligible assets as collateral, which the central bank holds as security against the loan. The eligible collateral can include government securities, high-quality bonds, and other approved assets. The value of the collateral is usually more significant than the borrowed amount to mitigate the risk for the central bank.

2. Reverse Repurchase Agreements (Reverse Repos)

Reverse repos are another tool used by central banks to provide liquidity to banks. In a reverse repo, the central bank temporarily buys securities from banks with an agreement to sell them back at a future date. This essentially allows banks to obtain cash by using their securities as collateral.

To initiate a reverse repo transaction, a bank offers eligible securities to the central bank as collateral. The central bank provides cash to the bank, and the bank agrees to repurchase the securities at a predetermined future date with an agreed-upon interest rate. The difference between the cash received and the repurchase price reflects the interest paid to the central bank.

Basel III

The policy goal of Basel III, specifically concerning capital requirements, is to strengthen the resilience of the global banking system. Basel III aims to address the vulnerabilities exposed during the 2008 financial crisis by establishing more robust capital standards for banks. Again it's important to take two minutes to explain the key objectives of Basel III capital requirements include:

1. Higher Capital Adequacy

Basel III sets higher minimum capital requirements that banks must maintain to support their risk-weighted assets (RWAs). It introduces a common equity Tier 1 capital (AT1) (CET1) capital requirement, which emphasises the highest-quality capital within a bank's capital structure. This higher capital adequacy ensures that banks have a stronger buffer to absorb losses and enhances their ability to maintain solvency during times of financial stress.

2. Risk-Based Capital Standards

Basel III promotes more risk-sensitive capital requirements, aligning the amount of capital banks are required to hold with the underlying risks in their balance sheets. It introduces stricter risk weighting of assets, helping to ensure that banks allocate sufficient capital against riskier assets. This approach encourages banks to assess and manage their risks more effectively, reducing the likelihood of insolvency due to excessive risk-taking.

3. Countercyclical Capital Buffer

Basel III introduces a countercyclical capital buffer (CCyB) requirement, which allows regulators to increase capital requirements during periods of excessive credit growth and economic expansion. The CCyB helps mitigate the buildup of systemic risk and enhances the resilience of banks against economic downturns. Banks are required to maintain an additional buffer of capital that can be deployed to absorb losses and stabilise the financial system during times of crisis.

4. Capital Conservation Buffer

Basel III sets a capital conservation buffer requirement, which requires banks to hold additional capital to ensure they can maintain their capital adequacy levels in times of financial stress. The buffer acts as a cushion to prevent banks from depleting their capital levels and facilitates orderly resolutions without resorting to taxpayer-funded bailouts.

By implementing these capital requirements, Basel III aims to enhance the overall stability and soundness of the banking sector. It reinforces banks' ability to absorb losses, strengthens their capital base, and reduces the likelihood of systemic disruptions that can have significant adverse effects on the global financial system.

Government Spending and Collateral

The Treasury's role in supporting the financial system by supplying it with AT1 capital is an important part of maintaining liquidity and stability.

When the government issues Treasury bonds or bills, financial institutions purchase these securities, effectively lending money to the government. In return, the financial institutions receive Treasury securities, which serve as collateral that can be used to secure funding. This collateral, backed by the full faith and credit of the government, is considered high-quality and low-risk in the financial market.

The issuance of these Treasury securities increases the supply of collateral available in the financial system. This oversupply of collateral ensures an efficient amount of liquidity, as these securities can be used as assets to secure funding and access to liquidity.

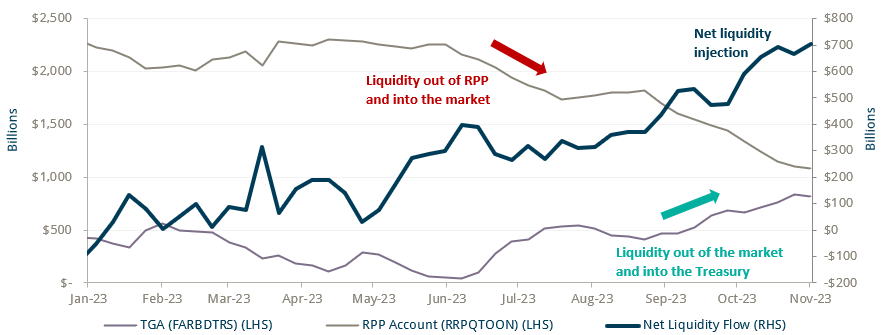

The Treasury's actions in controlling the rate of bill issuance and managing the Treasury General Account (TGA) can impact the amount of liquidity in the financial system. By adjusting the rate at which Treasury bills are issued and determining the level of funds held in the TGA, the Treasury can influence the amount of private liquidity that finds its way into the markets or is set aside for future fiscal expenditure.

Janet Yellen, the Treasury Secretary, has been managing the issuance of Treasury bills and the buildup of the TGA; she can control the flow of private liquidity into the markets. This control allows the Treasury to influence the level of liquidity available to financial institutions and the overall functioning of the financial system. That's now examine and understand the Treasury's strategy.

The Basel Committee's Report on the 2023 Banking Turmoil

The Basel Committee published a report on the 2023 banking turmoil, emphasising the need for a robust design and calibration of global standards for internationally active banks. While Basel III has enhanced banks' resilience, recent turmoil highlighted their vulnerability to rapid changes in market sentiment.

High leverage combined with long-term opaque assets funded with short-term runnable deposits makes banks especially vulnerable to a loss of trust in their long-term solvency.

The BIS report highlights the “issue is whether the treatment of unrealised gains and losses for assets that are held to maturity (HTM) should be similar to those that are held as AFS. One view is that, in times of stress and/or resolution, banks may need to sell or monetise all types of securities – potentially at a discount – including those that were intended to be HTM. As such, regulatory capital might overstate banks’ shock-absorbing capacity if unrealised losses of HTM securities are not adequately reflected.”

The issue for central banks is that the unrealised losses, reduces regulatory not only capital requirements, but it also reduces the ability to access the Discount Window or Reverse Repo facilities, due to lack of collateral, or current market value of that collateral.

Basel III Liquidity Standards and Asset Allocation and Yellen

Janet Yellen's actions and control over the rate of bill issuance and subsequent TGA build can have implications for the market's perception of efficient Additional AT1 collateral, which is relevant for banks' liquidity and potential coverage of underlying problems in their loan books.

The efficient use of AT1 collateral relies on the availability and quality of assets that banks can use to access liquidity. Under Basel III, certain instruments, such as AT1 instruments, can be counted towards a bank's capital buffer and can provide them with access to additional liquidity in times of stress.

By controlling the rate of bill issuance, Janet Yellen has the ability to influence the supply of high-quality liquid assets (HQLAs) available in the market. HQLAs are essential for banks to meet liquidity standards under Basel III. If Yellen increases the rate of bill issuance, it can lead to an increase in the supply of HQLAs, making them more accessible for banks.

In addition, Yellen's control over the TGA build, which is the amount of funds held in the Treasury General Account, can also affect the liquidity available in the market. When the TGA balance is high, it indicates that funds are being held by the government and not actively invested or utilized. If Yellen chooses to reduce the TGA balance by deploying the funds into the market, it can increase the availability of liquidity for banks.

The increased availability of HQLAs and liquidity in the market due to Yellen's actions can enhance the efficiency of AT1 collateral. AT1 instruments can be utilized by banks as a source of liquidity and can help cover any underlying problems in their loan books, including unrealized losses. If there is a heightened supply of HQLAs and liquidity, banks may find it easier to access funding through AT1 instruments when needed, allowing them to address issues in their loan portfolios.

SVB and Signature case study

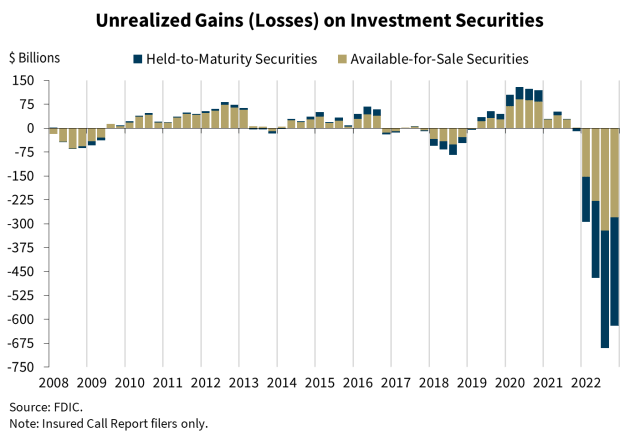

Estimated unrealized gains (losses) on SVBFG's investment portfolio securities

I now want to analyse and explain what the BIS said about the March 2023 banking crisis. The issue highlighted in the context of the SVB and Signature failures is primarily related to risk exposure and the lack of adequate collateral. If these banks had possessed sufficient collateral, they would have been able to access normal interbank funding mechanisms instead of encountering liquidity difficulties. This is clearly highlighted in the % of HTM assets held by SVB, shown in the chart above.

The discount window is designed to offer banks a source of backstop liquidity during times of stress. However, the events of March 2023 demonstrated that there is still a stigma associated with borrowing from the discount window. This means that banks may be hesitant to utilise this facility due to concerns about how it will be perceived by the market, potentially damaging their reputation.

In the case of the regional banks' health concerns in the US, increased depositor withdrawals prompted a surge in borrowing from Federal Home Loan Banks (FHLBs) rather than the discount window. The BIS indicated a lack of preparedness among many banks to use the discount window as a source of backstop liquidity.

To address this issue, explained that in their opinion, it is crucial to ensure that banks have adequate collateral to access normal interbank funding mechanisms instead of relying solely on the discount window. By having sufficient high-quality collateral, banks can maintain market confidence and avoid stigma associated with utilising emergency liquidity facilities. This underscores the importance of effective collateral management and risk assessment within banks.

By, improving operational readiness and agility can also contribute to addressing these challenges. Banks need to proactively assess their liquidity needs and prepare contingency plans well in advance to ensure they can access liquidity promptly when required. This includes having a robust understanding of collateral eligibility, monitoring market conditions, and being proactive in managing risks.

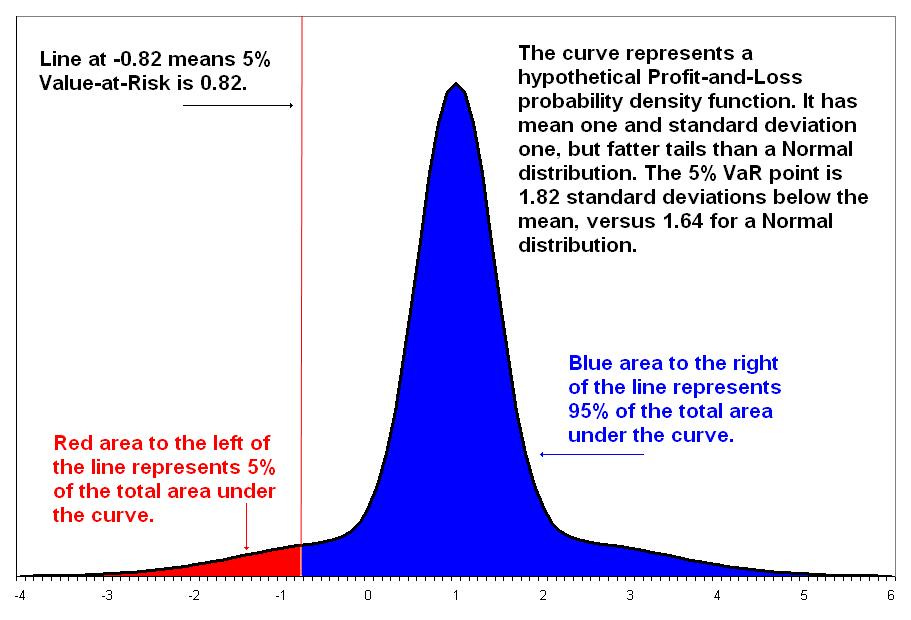

Value-at-Risk

That take a minute to understand risk, by analysing VaR. This is a means of making a statement along the following lines: ‘We are X (which is the blue area of the chart) percent certain that we will not lose more than V dollars (which is the Red area on the chart) in time T’ (which is the line at the bottom of the chart) on an investment or portfolio. Therefore it gives an ability to state the maximum loss that

can be expected over a specific amount of time with a certain degree of probability. For example a ten-day 95% VaR of £200 million would mean that 95 times out of 100 the loss on an investment will not be greater than £200 million over a ten-day period. Hull (2010)

It is important for banks to understand their Value at Risk (VaR) because it provides a measure of the amount of risk they are exposed to on a daily basis. By having a clear understanding of their VaR, banks can assess the potential losses they may face within a certain confidence interval, allowing them to manage and mitigate risks effectively.

Efficient collateral management is crucial for banks to address liquidity risks. By maintaining an appropriate quantity and quality of collateral, banks can protect themselves from potential liquidity issues and having to realise HTM losses on their portfolio. This involves ensuring that they have assets that can be easily converted into cash to cover any unexpected outflows, like AT1 Treasuries bills.

The Central Bank's Role in Collateral Lending

That now analyses how this interbank lending system works and the role of Central Bank's. The interbank lending system revolves around the assessment and perception of risk between banks. At its core, over-the-counter (OTC) interbank lending involves the exchange of liquidity for collateral. Banks evaluate the value and risk associated with the collateral being offered and make adjustments accordingly. In return, the borrowing bank offers an interest rate based on their perception of the collateral's value.

This system holds significant importance because if the Treasury provides an unlimited supply of AT1 Treasuries, where the value and risk are clearly defined, banks can avoid exposing the other elements of their portfolios where the risk is high and potential losses have not yet been fully realised on their balance sheets.

By relying on these well-defined and low-risk Treasury bonds as collateral, banks can mitigate risk and maintain stability in their lending activities. This provides a level of certainty and confidence in the interbank lending system, enabling smooth operations and facilitating the flow of liquidity in the financial markets.

Furthermore, the availability of high-quality Treasury collateral positively influences market dynamics. The presence of central bank eligibility for specific securities can increase their price and reduce their yields, especially during periods of collateral scarcity. Consequently, well-managed collateral policies by central banks can have positive effects on wider market practices, contributing to improved market functioning overall.

The role of Central banks

The chart above highlights the role the Federal Reserve played in the interbank lending system. As you can see, from 1950 to 2008, it was zero, as such we need to understand why?

The Federal Reserve has policies that require collateral from banks when providing them with funds as part of policy operations. This collateral requirement helps mitigate credit risk and ensures that central banks lend to banks in a secured manner as I have already explained. The principle of not lending uncollateralized to counterparties is enshrined in statute to maintain the stability and financial soundness of the banking system.

The principle that the ECB and constituent central banks of the

Eurosystem will never lend uncollateralized to counterparties

in policy operations are enshrined in statute. (Article 18.1 of the Protocol on the Statue of the European System of Central Banks and of the European Central Bank states).

The stability of the Federals balance sheet from 1970 to 2008, with minimal changes, can be attributed to the functioning of market mechanisms. In the 1970s and 1980s the financial system could not be described as healthy, yet banks were able to manage their own liquidity needs by relying on interbank mechanisms and borrowing from each other.

However, in 2008, a financial crisis occurred, and market mechanisms collapsed. This left banks in a precarious situation, with limited access to interbank lending and facing liquidity shortages. As a result, banks turned to the Fed for liquidity support, which required collateral for them to access funds.

In 2008, during the financial crisis, the U.S. government provided support to the Federal Reserve to help stabilise the banking system. The support primarily came from the U.S. Department of the Treasury.

One of the key initiatives introduced was the Troubled Asset Relief Program (TARP). TARP was a program authorised by the Emergency Economic Stabilization Act of 2008, which aimed to stabilise the financial system and promote economic recovery. Under TARP, the Treasury was granted authority to provide financial assistance to troubled financial institutions, including banks, by purchasing their troubled assets or injecting capital into them.

The Treasury provided funds to the Fed through programs such as the Capital Purchase Program (CPP), which allowed the Treasury to purchase equity shares in banks. By injecting capital into banks, the government aimed to strengthen their balance sheets and improve their ability to lend, thereby preventing a collapse in the banking system.

Additionally, the Treasury and the Fed worked together to implement various emergency lending facilities and programs. These initiatives, such as the Term Auction Facility (TAF) and the Commercial Paper Funding Facility (CPFF), aimed to provide liquidity to financial institutions facing funding challenges. The Treasury often provided backstops or guarantees for certain Fed programs, further supporting the banking sector.

Why is this relevant? Because the 2008 GFC exposes two things. First, the Federal Reserve needs support from the Treasury, due to the fact the Federal Reserve has neither the legal authority nor the policy tools to deal with the banking system. Second, the political turmoil created by the bailouts. The next question, is there a risk of another GFC?

Understanding Current Market risks

There is an ongoing concern that banks may be heavily leveraged, which could potentially lead to write-downs on long-dated bonds and adversely affect the commercial real estate (CRE) market, highlighted by the collapse the week of New York Community bank . Furthermore, the actions of policymakers, such as Janet Yellen, may impact political accountability. The question then arises: what will be the future cost of these situations?

Let's consider a hypothetical scenario where Bank of America is rumoured to be applying for chapter 11 bankruptcy. In such a case, if they approached JPMorgan for a $10 billion loan to cover potential customer withdrawals, JPMorgan might consider doing a swap if Bank of America provides the right collateral, such as AT1 Treasuries bills.

By engaging in this swap, Bank of America would, in essence, delay addressing its financial challenges for another week. This temporary respite, however, does not resolve the underlying issues at hand.

The recent situation involving New York Community Bank, where losses of $500 million were incurred on two loans, indicates that there could be larger implications than initially perceived. This raises concerns about the stability of banks facing such losses.

I have written before about collateralized loan obligations (CLOs), which are leveraged loans with maturities typically ranging from 3 to 5 years. Given the collapse in demand caused by COVID-19, it is a huge concern that borrowers may not possess sufficient collateral or fixed income from properties to cover their loan obligations.

Creating a property group within a bank, as seen with institutions like Lloyds and Blackstone, could be one possible solution. By separating properties and treating them as assets instead of liabilities, banks can mitigate losses on their loan books. However, it is important to note that implementing this strategy depends on the bank's ability to manage their overall risks effectively and ensure enough collateral to cover short term stress in the financial system.

In terms of sourcing sufficient and suitable collateral to cover liquidity needs, it seems clear to me, Treasury Secretary Yellen, is pushing this provision onto the taxpayer. The Treasury is currently running a 8% fiscal deficit and bills and paper to cover this spending, is also injecting liquidity into the system and supporting the banks. In this context, using AT1 collateral can help "wash" the system and provide the necessary backing.

Asset Bubbles and Spending Power Erosion

Despite the lingering burden of debt in the financial system after the Global Financial Crisis (GFC), fiscal spending in the US has played a crucial role in managing this debt by providing ample AT 1 capital. This capital enables banks to access necessary liquidity, thus preventing them from facing losses on their balance sheets.

However, it is important to be aware of the potential dangers associated with the emergence of asset bubbles, which began to surface on October 31st. These bubbles have the propensity to erode the spending power of individuals who do not possess assets, contributing to potential economic imbalances.

In recent years, the phenomenon known as the Magnificent Seven (Mag Seven) emerged from the FANG (Facebook, Amazon, Netflix, and Google) stocks, which started in the mid-2000s. This group subsequently evolved into FANGAM with the inclusion of Apple and Microsoft, and eventually transformed into the Mag Seven in 2023, with the removal of Netflix and the addition of Tesla and Nvidia. The collective market capitalization of these companies experienced a staggering increase of $5.1 trillion throughout 2023 and that has continued into 2024.

While shareholders of these assets witnessed a rise in their wealth, the real economy faced inflation as high as 9.1% in the US, outpacing any wage increases and affecting purchasing power negatively.

Therefore, it is crucial to recognize the potential consequences of such discrepancies between asset holders and the broader population. Striving for a more balanced approach, focusing on prudent fiscal policies, responsible financial practices, and technological innovation can help address these challenges and ensure a more sustainable and inclusive economic future.

Conclusion

Treasury bonds hold immense significance in our financial system as a vital source of collateral and liquidity. The oversupply of collateral, stemming from government spending, ensures an efficient amount of liquidity, positively impacting the market. The implementation of Basel III regulations and the maintenance of Tier 1 capital are crucial for upholding financial stability.

Nevertheless, certain risks need careful monitoring, such as asset bubbles and the potential erosion of spending power for non-asset owners. Collateral policies established by central banks have both advantages and drawbacks, and their actions significantly influence market practices.

Currently, the fiscal expansion and erosion of spending power experienced by US citizens are generating political instability. The accumulation of debt since the Global Financial Crisis presents a complex issue with no easy solution. However, achieving stability can be facilitated through the development and expansion of the manufacturing sector, prudent government spending, and technological innovation.

By focusing on these areas, we can foster a more stable and prosperous economy, mitigating the negative consequences of debt accumulation and ensuring the well-being of both the financial system and the public.