Why, With full employment do we all feel poorer?

Why, With full employment do we all feel poorer?

A full economic analysis

I want to use this article to explain the economic landscape of both the 1970s and today, going down the rabbit hole of intriguing parallels and contrasts emerging, revealing the intricate dance between demographics and inflationary pressures. The 1970s witnessed the Baby Boomer generation flooding the labour market, curbing wages but escalating overall demand, culminating in double-digit inflation. Fast forward to today, a reverse correlation unfolds as falling population growth propels labour costs upward, while dwindling labour participation in the United States hovers around 62%. Unsurprisingly, the Baby Boomers, with their sustained demand for goods and services amid a shrinking workforce, paint a unique picture. Although demand remains robust, the scarcity of labour inputs presents a new challenge, akin to the past but with a modern twist, once more fueling potential inflationary trends. This dynamic interplay between shifting demographics and economic forces underscores the complexities shaping our current economic landscape.

1970s Inflation and Baby Boomers

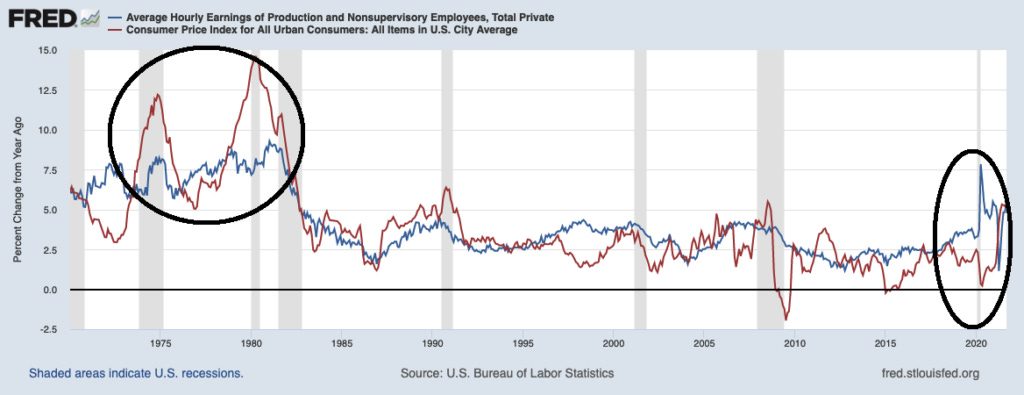

During the 1970s, the Baby Boomer generation, born in the years following World War II, entered the workforce in large numbers. This influx of young workers led to a significant increase in the labour supply, creating a situation where there were more people seeking jobs than there were job opportunities available. This is represented in the chart below, on the left hand side, where unemployment was as high as 15%.

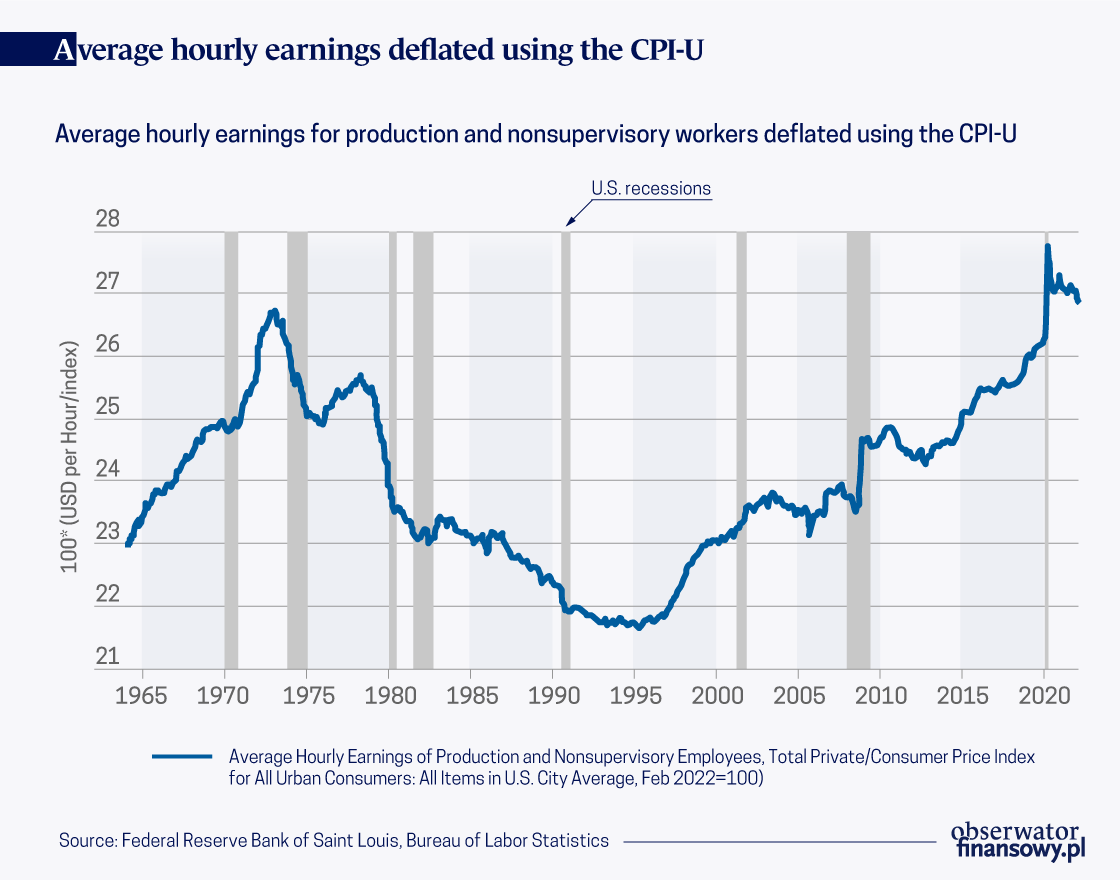

As a result, employers had the upper hand and could afford to offer lower wages due to the abundance of potential employees. Which, again is clearly Highlighted in the chart below, where average hourly Earnings, deflated using the CPI-U, takes a dramatic fall in 1974, and doesn't start recovering from 20 years. But today, hourly earnings are as high as they ever were in the last 60-years.

At the same time, as the Baby Boomers began working and earning incomes, they collectively had greater spending power. This increased demand for goods and services in various sectors of the economy, such as housing, automobiles, and consumer goods. As you can see from the chart above, while wage growth was high due to inflation pressure, CPI clearly outstripped all wage increases.

The combination of abundant labour supply driving down wages and increased overall demand from the Baby Boomer cohort led to a scenario where demand exceeded supply, creating inflationary pressures.

The surge in demand for goods and services from the Baby Boomer generation, who all entered the workforce, got married, bought houses, and purchased cars around the same time, further exacerbated the inflationary trends.

The failure of Arthur Burns.

During Arthur Burns' tenure as Chairman of the Federal Reserve, the Federal Open Market Committee (FOMC) made decisions on key monetary policy measures to address the high inflationary pressures of the 1970s. The FOMC, which is responsible for setting the nation's monetary policy, worked alongside Burns to implement policies aimed at controlling inflation by adjusting interest rates and managing the money supply.

One of the primary tools used by Burns and the FOMC to combat inflation was to raise interest rates. By increasing interest rates, the FOMC sought to reduce demand for goods and services, thereby slowing down economic growth and inflation. However, these efforts were not always successful in curbing the rampant inflation experienced during this period.

The challenges faced by Arthur Burns in controlling inflation and the failing results of his policies during his time as Federal Reserve Chairman have contributed to his reputation among economists and policymakers. His tenure is often associated with the difficulties of combating inflation in a complex economic environment. The legacy of Arthur Burns, is that NO Federal Reserve Chair wants to be known as Arthur Burns because of the difficulties he faced in effectively managing inflation and the lingering criticisms of his tenure.

The Real World Effects of 1970s Inflation

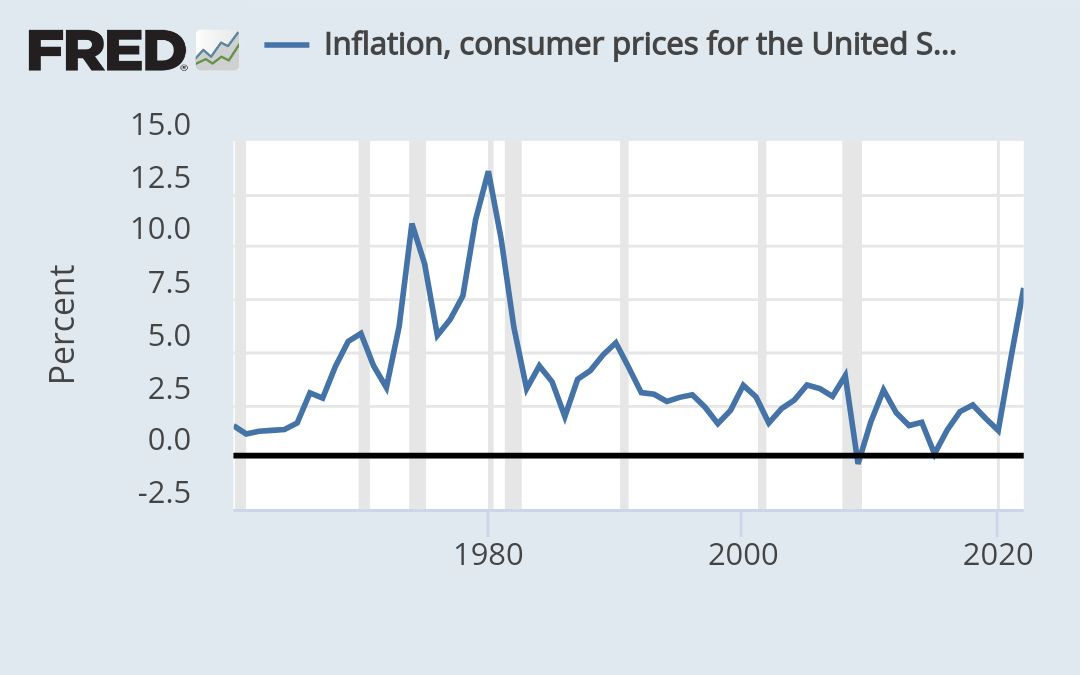

During the 1970s, the United States experienced a significant increase in the Consumer Price Index (CPI), which measures the changes in prices of goods and services typically purchased by consumers. For instance, from 1971 to 1980, the annual average inflation rate surged from around 3% to over 11%, translating to a rapid erosion of consumers' purchasing power.

This erosion of purchasing power meant that consumers needed more money to purchase the same amount of goods and services, leading to a decrease in real incomes. As a result, individuals' standards of living were negatively impacted as their wages could not keep up with the rising cost of living due to high inflation.

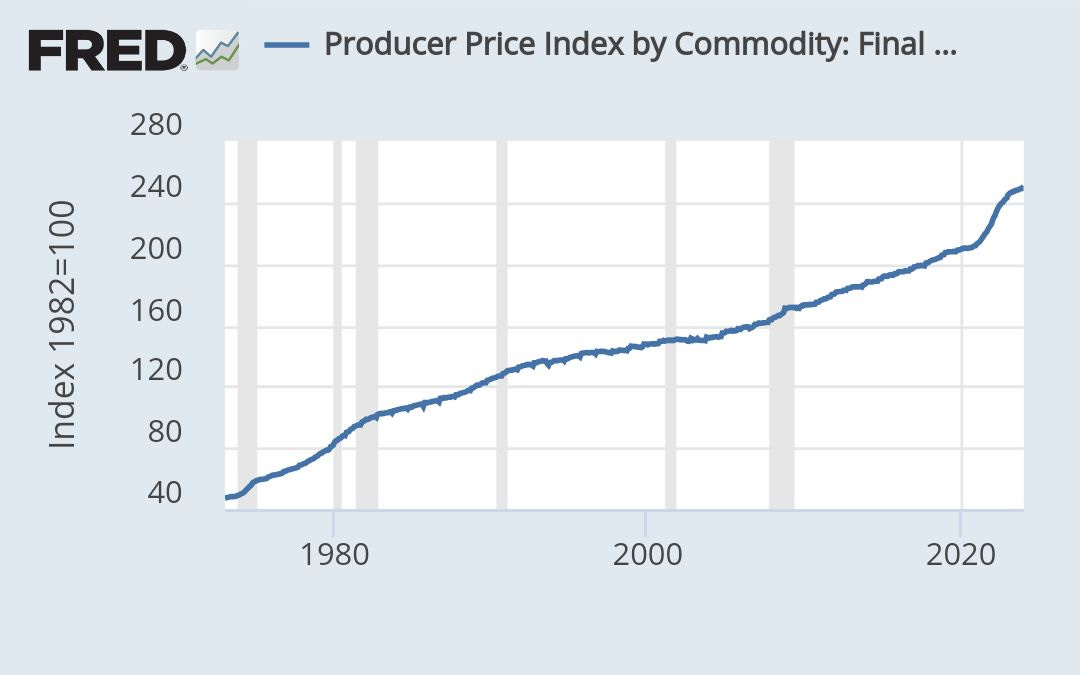

The volatile price levels and cost pressures due to high inflation introduced a significant level of uncertainty for businesses during the 1970s. For example, the Producer Price Index (PPI), which tracks the changes in prices received by domestic producers, also showed sharp increases during this period. In the chart Below while PPI, has risen consistently, during the 1980s and after 2020, there is a clear steepness in the curve, which is a deviation from the norm.

This is important because, if businesses face challenges in predicting future costs and revenue streams amidst fluctuating price levels, this uncertainty influences their investment and planning decisions. Businesses become hesitant to commit to long-term investments or expansion due to the unpredictable economic environment created by high inflation.

In response to the persistent inflationary pressures of the 1970s, the Federal Reserve implemented contractionary monetary policies in the late 1970s. One key indicator of these policies was the increase in the federal funds rate, the benchmark interest rate.

The Federal Reserve's objective was to rein in inflation by tightening monetary conditions, thereby reducing aggregate demand in the economy. However, these contractionary measures also had the unintended consequence of contributing to recession in the early 1980s as economic activity contracted due to the restrictive monetary policy.

Current Demographic Trends

In contrast to the economic landscape of the 1970s, where excess labour supply drove unemployment rates as high as 15%, today's scenario unveils a different dynamic, (as highlighted in the chart above).

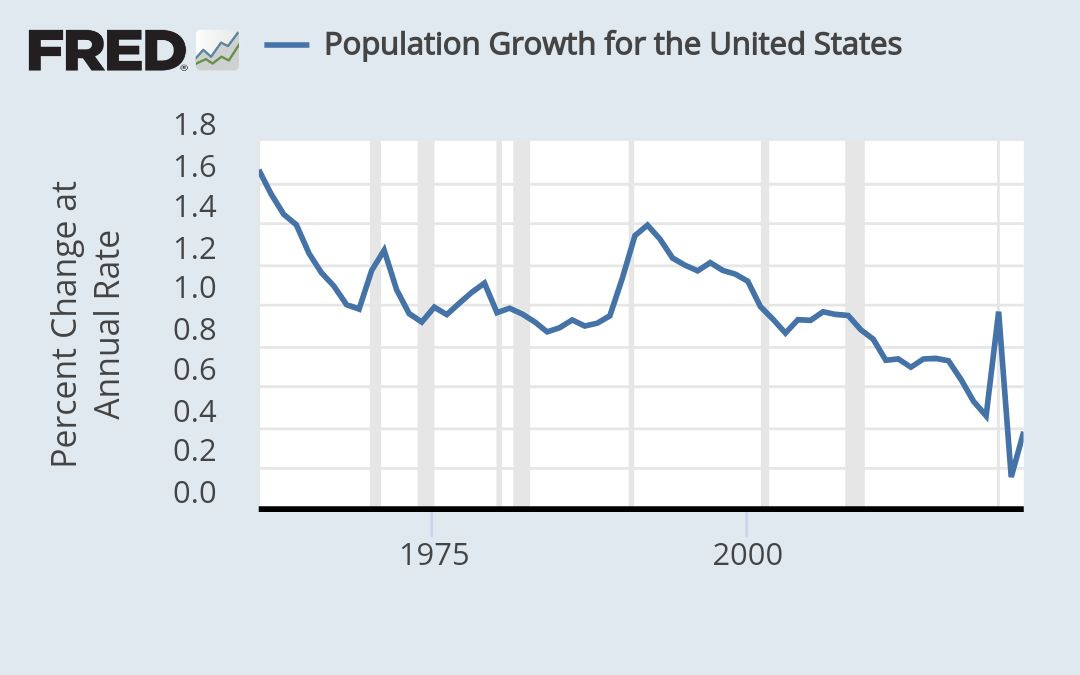

The falling population growth (as highlighted in the chart below)seen in developed nations like the United States is influenced by factors such as declining birth rates, an ageing population, and evolving societal norms. This demographic shift has lead to a reduced workforce and labour pool, posing challenges for employers seeking qualified workers to fill job vacancies.

In the current context, with the unemployment rate resting at a low 3.5%, employers find themselves in a position where they need to offer competitive wages and flexible working arrangements to attract and retain talent. This shift towards hybrid working conditions, accommodating remote work options, is emblematic of the evolving expectations and demands of the modern workforce.

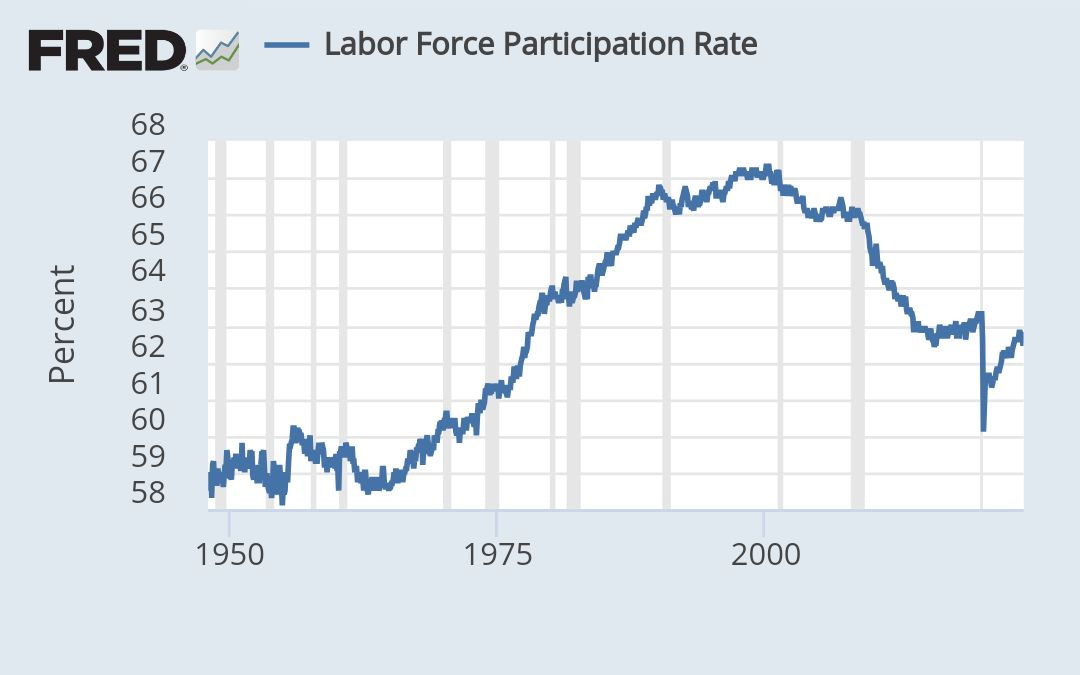

The decreased working-age population today has implications for economic growth and productivity. The limited pool of workers contributing to the economy may result in a slowdown in overall economic activity and innovation, necessitating proactive strategies to address these challenges. As you can see from the chart below, the labour participation rate has fallen by just under 10% in the 2000s, to 62% today. Unlike the 1970s when unemployment Was as high as 22%, the decline today is due to an ageing population.

2024 Inflation

In the current economic environment, high inflation is eroding consumers' purchasing power as evidenced by the Consumer Price Index (CPI) data, showing a notable increase in the cost of goods and services. The annual inflation rate has risen, outpacing wage growth, resulting in a decrease in real incomes for consumers.

Inflation eroding consumers' purchasing power leads to a decline in standards of living, as individuals have to allocate more of their income towards basic necessities, leaving less room for discretionary spending and savings. But this is also having another effect in that it is creating real political instability in the west, as asset prices rise and real wages fall, the gap between rich and poor expands.

Volatile price levels and cost pressures faced by businesses observed through indices such as the Producer Price Index (PPI), reflecting the changes in input costs for producers. While PPI has fallen from its COVID-19 peak, the trend since the turn of the year is higher. The upward trend in input costs, including labour and borrowing costs, is squeezing profit margins for businesses.

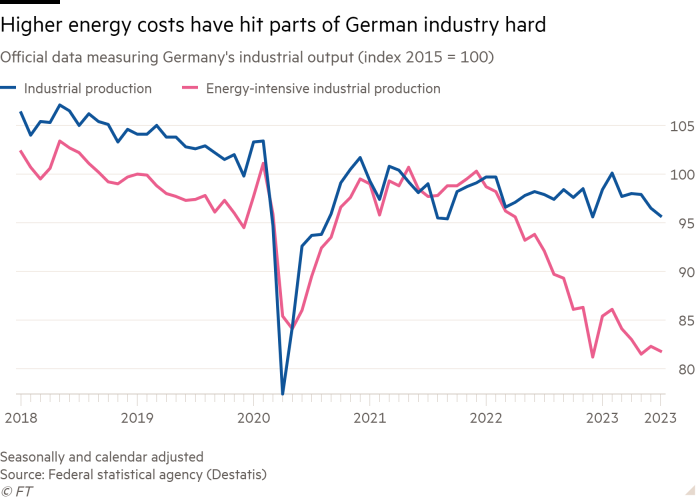

This in turn creates heightened uncertainty stemming from cost pressures that influences businesses' investment and planning decisions. While businesses in the US have not yet shown signs that they are hesitating to expand operations or invest in new projects due to the unpredictable economic environment characterised by rising costs. However, this effect can clearly be seen in Germany. Where German industrial production has shown massive 25% contraction, from its 2018 peak.

The Federal Reserve's response to combat inflation

I have already shown how in the 1970s, the United States faced a challenging period characterised by "sticky" inflation, a phenomenon where prices exhibited resistance to declining even as economic conditions changed. This persistent inflationary environment presented significant difficulties for policymakers, including the then Federal Reserve Chairman Arthur Burns, in adjusting monetary policy effectively to bring inflation under control.

During Arthur Burns' tenure as Chairman these encountered the complexities of addressing sticky inflation, where price levels remained elevated despite efforts to combat rising inflationary pressures. The challenge of navigating an economy plagued by sticky inflation limited the effectiveness of traditional monetary policy tools, leading to a protracted battle against escalating price levels.

Fast forward to the present day, Federal Reserve Chair Jerome Powell faces a comparable dilemma as inflation rates exhibit stickiness, resisting downward adjustments even amidst contractionary monetary policies. Powell's efforts to curb inflation by implementing similar contractionary measures, such as interest rate adjustments and tightening monetary policy, echo the challenges faced by predecessors like Arthur Burns in managing stubborn inflationary trends.

The implications of sticky inflation are far-reaching, impacting not only the ability of policymakers to effectively adjust monetary policy but also influencing economic growth, employment levels, and consumer purchasing power. The delicate balance between combating inflation and sustaining economic activity underscores the importance of monitoring the outcomes of past policy responses while adapting strategies to address the unique characteristics of current inflationary pressures.

As Jerome Powell navigates the complexities of managing sticky inflation in today's economic landscape, drawing insights from historical experiences like those of Arthur Burns in the 1970s can provide valuable lessons on the nuances of addressing persistent inflation dynamics and their implications for monetary policy effectiveness, economic stability, and long-term prosperity. This is why understanding the supply and demand imbalance is so important.

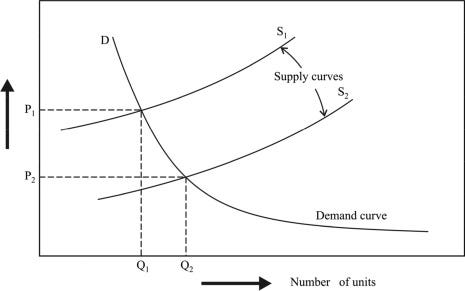

Supply and Demand Imbalance

While demand in the economy may remain relatively steady, the reduction in the supply of labour inputs, shifting from S1 to S2, due to demographic shifts and lower participation rates leads to a supply-demand imbalance. Where firms have to either increase prices from P¹ to P² or increase quantity from Q¹ to Q², this is called electricity supply. The issue there isn't the increase in demand from Baby boomers and the supply of labour in contracting, the result is that the cost of labour rises, contributing to overall inflationary pressures.

Conclusion

The economic landscape of the 1970s and today presents a fascinating tapestry of parallels and contrasts, shedding light on the intricate dance between demographics and inflationary pressures. In the 1970s, the Baby Boomer generation entering the labor market led to a surge in demand but curbed wages, contributing to double-digit inflation. Contrastingly, today's scenario showcases falling population growth propelling labor costs upward, while labor participation rates in the US hover at around 62%, altering the dynamics of inflationary trends.

During Arthur Burns' tenure as Chairman of the Federal Reserve, the complexities of addressing sticky inflation were evident as price levels remained elevated despite efforts to combat rising inflationary pressures. The challenge of navigating an economy plagued by sticky inflation limited the effectiveness of traditional monetary policy tools, leading to a protracted battle against escalating price levels.

Fast forward to the present day, Federal Reserve Chair Jerome Powell is confronted with a similar dilemma as inflation rates exhibit stickiness, resisting downward adjustments despite contractionary monetary policies. Powell's efforts to combat inflation by implementing measures like interest rate adjustments and tightening monetary policy mirror the challenges faced by predecessors such as Arthur Burns in managing stubborn inflationary trends. The shift in today's scenario isn't due to the surge in demand from the Baby Boomer generation but the contraction in the labour supply, which elevates labour costs and contributes to overall inflationary pressures.

This dynamic interplay between shifting demographics and economic forces underscores the complexities shaping our current economic landscape and highlights the ongoing challenges faced by policymakers in managing inflation in a changing world. Which the markets seem briskly unaware.

Thank you

Great summary! https://rarible.com/token/0xb66a603f4cfe17e3d27b87a8bfcad319856518b8:81968064289257990630448839818518672153510570972563018559010431814722589294600