New Age Tech IPOs Corrected Enough (Nykaa) ?

New Age Tech IPOs Corrected Enough (Nykaa) ?

part -1 Nykaa #stock #share #value

I have been tracking some of the businesses and in almost all of them post-lock-in period the stock prices have started correcting as the insiders and pre-IPO investors started exiting the stocks.

Even after a 40-80 % correction in most of them, they are still pricing in a very optimistic future, Let’s see try to analyze them to see if there is any investment opportunity.

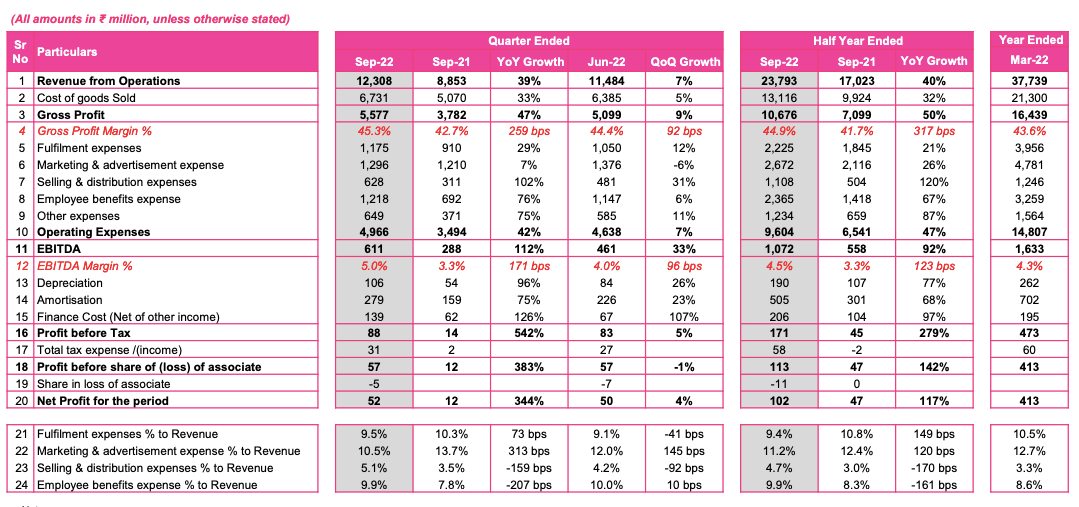

Nykaa -

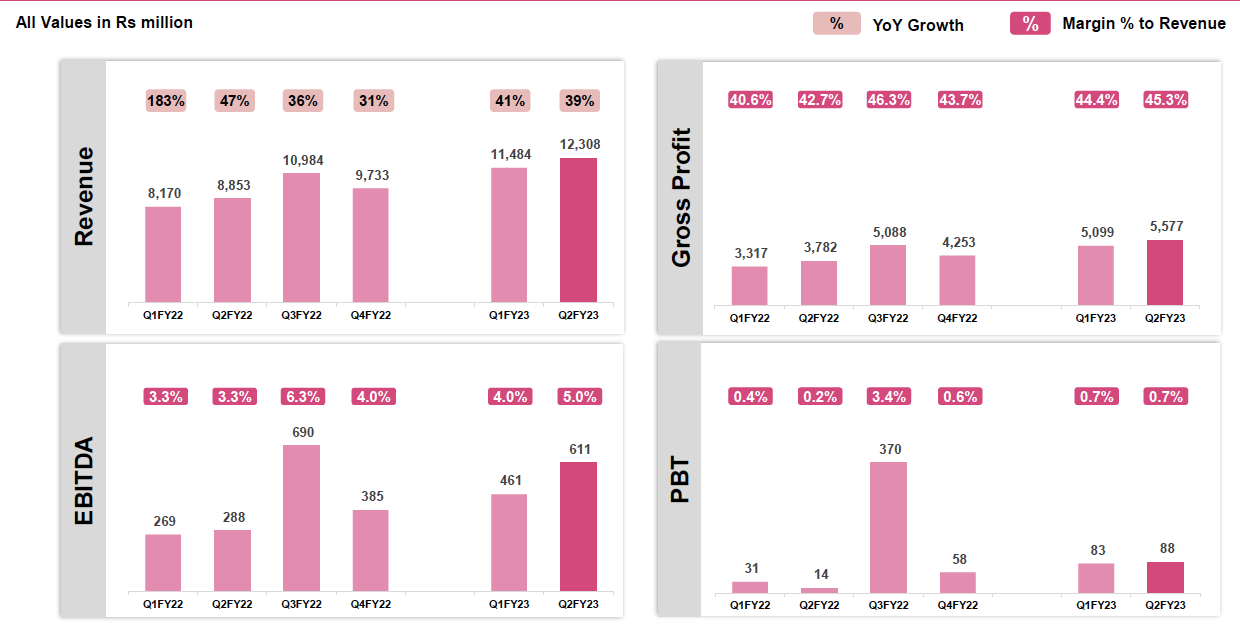

Marker cap ₹ 48,734 Cr & Revenue Rs 4,451

Trading at 11x revenue.

When any business is trading at 11x revenue your intuition says “oh boy it’s trading expensive” you might be right but certain businesses prove your intuition wrong. For example, if you would have bought bajaj finance at 11x 2012 revenue you still would have made a 32% cagr return holding it till today.

You might say no-no, you are comparing apples with oranges Bajaj finance is a high-margin business, whereas retail is a low single-digit margin business comparing the revenue multiple of two is misleading.

Okay, what if I tell you if you would have bought DMART at 11x Revenue in 2012, you would have made a 28% cagr return? It’s a 5-6% net profit margin (NPM) business.

One of the biggest problems with these businesses is there is no doubt about the quality, everyone knows about it but no one knows

when they will reach their full potential (become mature businesses with healthy cash flow / ROE) or how fast they will grow to reach there?

What’s the growth trajectory going to be?

What will be their Net Margin when they will reach there?

and what will be the terminal growth rate?

To be able to really value these companies we have to make some wild assumptions and when you are making wild assumptions about the future ( like I did for MapMyIndia and BBQ Nation ) you probably don’t know what you are doing.

What are the chances anyone can get growth, Steady state margins, and terminal growth right for the next 10-20 years? Especially for these businesses which still don’t have their business model in place. Chances are close to nill but anyways we can always know what markets are pricing in with a fair bit of assumption and try to roughly see if markets are too optimistic or pessimistic. because missing out on future Dmart or Bajaj finance is also not a good idea either just because it’s trading at 11x revenue. (after all its all about betting on odds)

Let’s try to value Nykaa by looking far into the future anyways -

First Assumption -

Net profit margins at terminal growth rate (when business is mature enough)

To value any business we need to know what is the net profit at the end of the day because that is ultimately what going to get distributed to shareholders.

To know the net profit of any business we need to know what net profit margins going to be.

Nykaa is just a retail/trading business at the end of the day, they buy stuff from somebody and sell it to you. In any kind of trading business, your margins are very low if you get a high single digit you are lucky & it’s not sustainable.

Do you know wall mart operates with a 2 to 3% net profit margin?

Do you know the other best retail business in the world (Costco) operates with similar 2 to 3% net profit margins?

Today Dmart enjoying 5-6% net profit margins in their investment-led growth phase which is really commendable.

Ecomm, on the other hand, is an even tougher business than brick and mortar due to higher delivery costs, high employee costs (Tech Engineers are expensive), and high cost of handling returns.

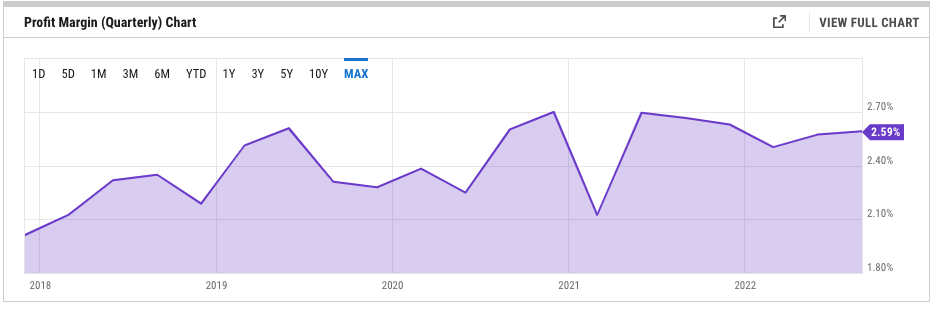

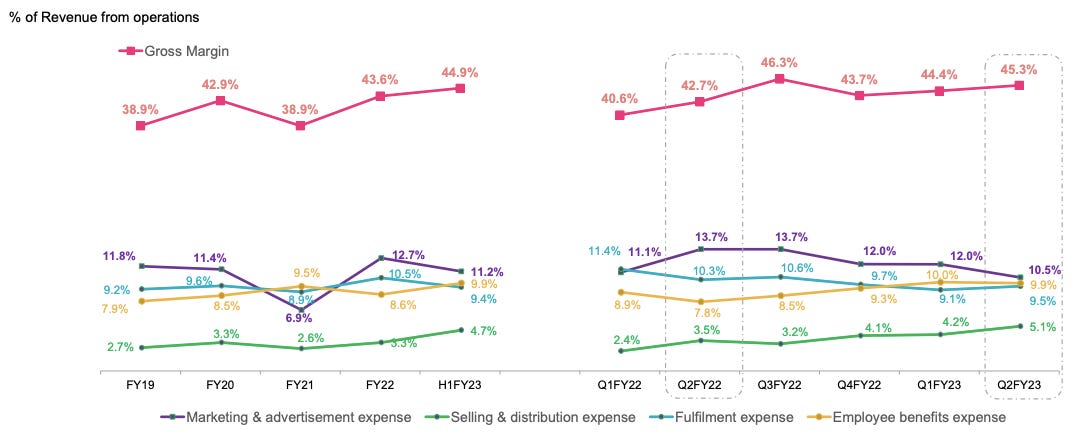

Today Nykaa is doing 40-45% gross profit margin which is inline with other Ecomm players globally such as Amazon, and Alibaba enjoy around 48% profit margins.

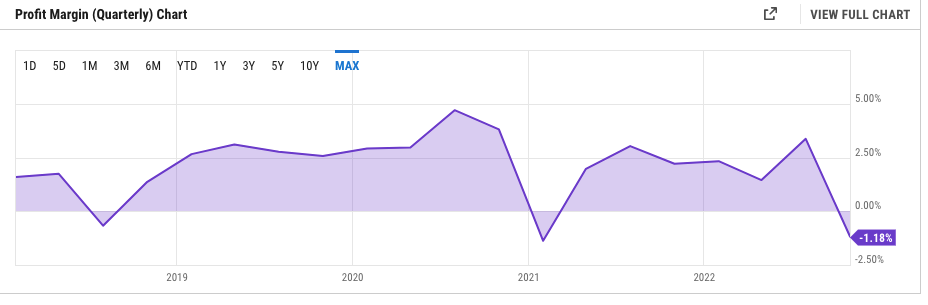

Nykaa is doing about 5% EBITDA margins and about 0.7% Net Margins (before tax).

Today their Net margins are artificially low as they are spending on growth. As you can see they are burning roughly 10-12% of revenue or 23% of gross profits into marketing and advertising

If we just take this expense alone out their EBITDA margins will go up from ~5% (sep -22) to 15% and this is possible maybe 10-15 years from now they may not have to do advertising once they are big enough & enjoying mindshare of all the customer base and if we run through it further they could have ended up doing roughly Rs100 Cr profit (NPM =8%) in Q (sep-22) instead of 5 Cr and if you annualized it its Rs 400 Cr profit which means its trading at ~100x PE btw DMART trades at 111x PE and they burn Rs 0 in marketing and advertising.

because of Nykaa's monopoly and operating at high margin goods Vs Groceries let’s say long-term sustainable net profit margins for Nykaa going to be 7-8% whenever they mature.

let’s say due to its monopoly nature and network effect of business it’s going to trade at 25-30 PE, 20 years from now (reasonable you know) and assume it will grow let’s say 15% cagr for 20 years then Is it trading cheap?

If we take all that into consideration

In Fy 42 they will be doing Rev of Rs 16x4451 = Rs 71216 Cr.

with NPM of 7%, net profits would be Rs 4985 Cr.

At 30x PE the market cap will be = Rs 149553 Cr, Which is just a 6% cagr return from today’s market cap.

Sam - Ohh boy this is too low what if they end up growing at a rate much high than 15%?

Me - Yes that’s possible.

Sam - Okay at what growth rate do they have to grow to generate a 15% cagr return?

Me - That’s a good question, like Charlie said invert - invert always invert.

To generate a 15% cagr return their Market cap has to be Rs 48,734 (today’s) x 16 = Rs 7,68,000 Cr.

Considering PE of 30, Net earnings will have to be = Rs 7,68,000/30 = Rs 25600 Cr.

considering 7% NPM, their revenue going to be = Rs 3,65,714 Cr.

This means they have to grow their revenue by 24% CAGR.

Sam - is it possible to grow 24% cagr for 20 years? oh man, this looks too optimistic to me.

Me - I feel the same, Both of our examples DMART and Bajaj finance were operating in very large markets and they grew from a very low base if we compare from 10 years ago, for example, Dmart used to do Rs 2200 Cr revenue in 2012 which is nothing compared to the amount of grocery sold all over India even at that time maybe 1% market share. Even today DMART enjoys just 10-15% market share.

whereas Nykaa already enjoys a 20-25% market share as of today in Beauty products and perhaps to justify valuation they entered fashion which is 5x the size of Beauty.

but it’s a very competitive market hard to say they will be the winner here as well.

Let’s give it a pass may be the meme I created during IPO is indeed aging well

This was part -1, In this series partwise, we will analyze MapMyIndia, Zomato, Nureca Inc, Latent View, Medplus, and maybe SBI cards. Do subscribe if you haven’t already.