Investment Framework Laid-Out

Investment Framework Laid-Out

Upgraded Portfolio Tracking for 2023

This time last year the market was already down 6% and never looked back (keep falling, as you know). This year we are up 4.2% after the first 23 days. Is it too early to say that 2023 could be a “green” year? In my Predictions edition I was a bit on the pessimistic side and called for a 12% decline in the S&P by year end after a strong Q2 rally. But I am an optimist at heart and happy to be wrong on my stock market prediction, especially if that means our portfolios have nothing but positive returns this year.

One of the difficult things about writing this newsletter is the wide variety of knowledge regarding investing from newbies to highly experienced. In this edition today, I will attempt to appeal to all of you as I lay out a new game plan for this year. If I miss the mark, please add to the comments. But first, if you haven’t subscribed yet, please do by smashing the button below:

Mental Models

As humans, we have an internal operating system that I’ll refer to as our mental model. This model helps us navigate the world we live in and respond to external stimuli. Each person’s mental model is unique and has evolved over time. The key here is to acknowledge that you have a model. If you are not being intentional about evolving and molding your model, you are doomed to operate in ‘auto’ mode and crap just happens to you.

The same can be said for investing. Everyone should have a plan. Create a model, or framework, specifically for you and your financial goals. It could include taking advantage of your areas of expertise or interests; however, it should accommodate for the amount of time and effort you are willing to put into it. You also need to access your willingness to accept risk or avoid it. The chart shows the risk continuum from low to high. Where do you stand?

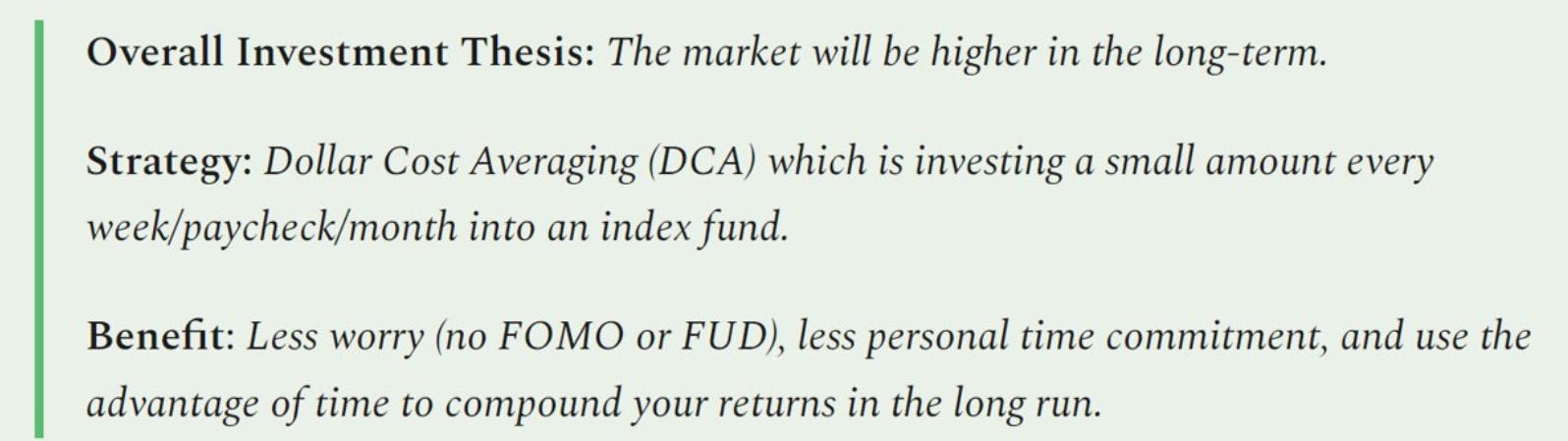

For most people, dollar-cost averaging into an index fund or exchange-traded funds (ETFs) is a great strategy because: 1) it is consistent, 2) does not spend a lot of your time, 3) it fairly low on risk scale, and 4) takes advantage of compounding appreciation over time.

The purpose of this newsletter is to build my investing framework in public with all of its flaws, warts, and Easter eggs. You should not adopt my exact framework but look to how the structure is built and tweak it for your own purposes.

Note: Before engaging in the world of investing, ensure you have created an emergency fund of liquid assets (like Cash in a savings account) of 2-6 months of expenses. Then, let’s talk about building wealth.

FYI only. Here are a few links to resources on personal finance (there are many more).

Investopedia: Personal Finance CNBC: Personal Finance Personal Finance 101

Journey to the Framework

It would be helpful to give some context to my background and mindset before laying out the investment framework for this newsletter. I grew up in Green Bay, Wisconsin, so was always a big Packers fan even though my sports were soccer and bowling. When graduating from college in December of 1985, I decided to move to a much warmer climate - Tempe, Arizona. There, I worked full-time while earning an MBA at Arizona State over a 3.5-year period. I didn’t make enough money as a Commodities Broker (where I first learned about technical analysis and investing), so found a job at a new operations center for Discover Card managing 24 people in the call center. Since I wanted to gain more experience in my field of finance, took a job at Honeywell as a financial analyst. The strange thing was that when I was living and working in Arizona, it always seemed like I was on vacation in this sunny, warm climate.

Decided to move back home to Wisconsin in 1990 and found a job in the energy efficiency world in Milwaukee even though I didn’t understand why a utility would pay their customers (in form of rebates) to use less of their product (electricity). But since I wanted to get back to Wisconsin, accepted the job and figured that I’d get a ‘real’ job in a couple years. This job turned into a successful 30-year career in an industry where we were creating solutions to combat the huge societal challenge of climate change. By helping utilities implement their energy efficiency programs, we were in the trenches everyday helping customers save money while reducing pollution and building a greener grid.

This experience has made me a strong believer in the future of the clean energy transition and decarbonization of our economy over the next 30 years. We have seen significant progress in the past decade, but I believe it is set up to accelerate speed by 2030. It feels to me that the 2020’s is where we hit the tipping point on renewables, electric vehicles, and battery storage where these sectors could grow at 25%+ CAGR (compounded annual growth rate).

Therefore, I am willing to allocate a portion of my investment portfolio into these sectors. However, to ensure clarity, I still have a majority of investment in assets that mimic the S&P 500 index. In addition, I recently added bonds to my portfolio now that there is an actual rate of interest that is interesting. For me, crypto is worth a single-digit portion of my portfolio. Finally, an allocation of 10-30% into your core investment thesis makes sense (i.e. clean energy stocks and ETFs). My strategy is to gain an advantage over the general market index return by positioning a portion of the portfolio into a core thesis that I believe will deliver superior returns over a 5-10 year timeframe.

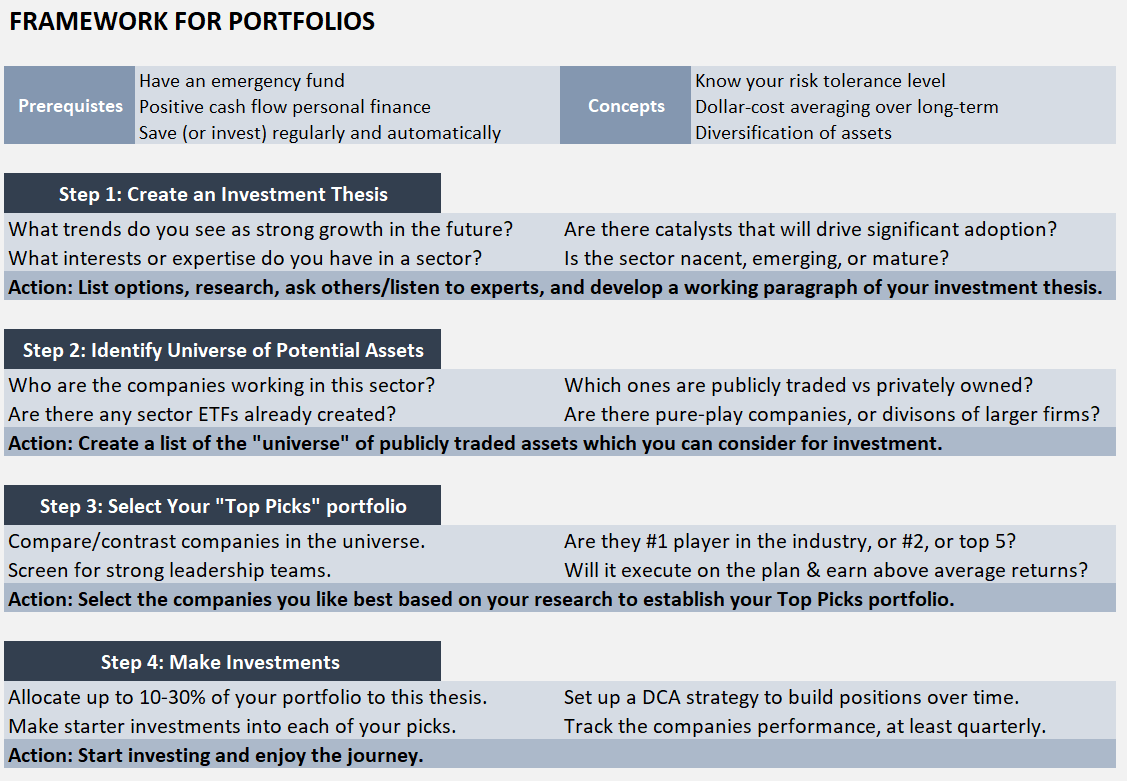

The “Portfolios” Framework

The idea of thinking in terms of Portfolios is the diversification of your investments. Diversification of investments is key to risk management and important to protect our portfolio from disaster of a “too many eggs in one basket” problem. The framework is a recipe for how you create your own investment portfolio.

Another important concept to the framework is investing regularly over time. I’ve written about dollar-cost averaging (DCA) in the past and a twitter thread on the topic. The thesis of DCA is explained below.

Here is the golden ticket of this edition of the newsletter. The Framework to use for putting together an amped up portion of your portfolio to drive above average returns in the long run.

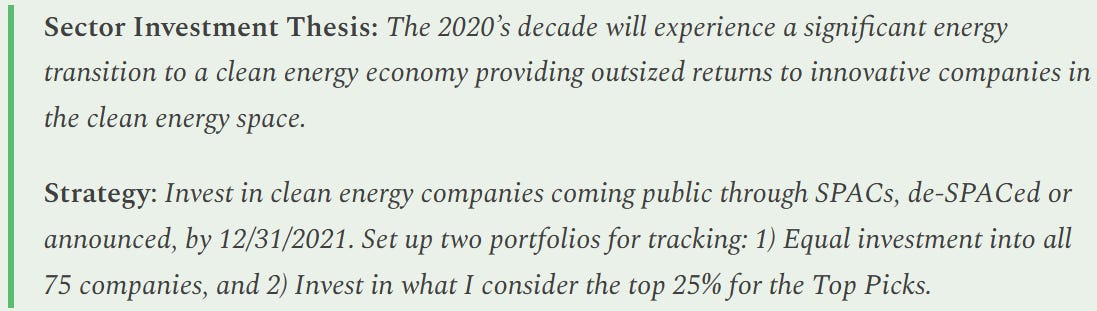

For example, my core investment thesis that this is the decade of significant progress in the energy transition and decarbonization sectors. Below was written about 18 months ago when I started the Top Picks portfolio.

Don’t have time for this type of research or don’t like to do this kind of work? Two quick solutions. First, there are many sector ETFs out there to choose from. If you like a sector, investing into an ETF (or basket of ETFs) may be your way to play this game. Or secondly, if you really like the clean energy thesis, continue to follow this newsletter and invest alongside in one or more clean energy ETFs (and tell your friends!).

2023 Portfolios Configuration

Welcome to the new Portfolios Tracking table for 2023. I’ve tweaked the format and added a few new portfolios and benchmarks to track. Let’s take a closer look section by section. The first section is focused in on our clean energy portfolios.

We keep the Top Picks portfolio which is a more actively traded portfolio during the year. Last year, it took a brutal loss of -55%. There was a lot of selling in the last quarter to get into a more defensive mode as we reduced the number of companies in the top picks from 19 down to 11 and made room for about 40% cash balance on 1/1/23 to give us some dry powder to work with and add to current positions, or new companies, at attractive levels.

The equal-weighted universe has also been trimmed. This list eliminated all stocks that were trading under $2 per share as of 12/31/22 as well as a handful of stocks that were either delisted from the exchange, went into bankruptcy, or had been acquired. Originally, we were tracking 75 tickers in the universe and now is at 37 tickers after the adjustments. Before the end of the month, I do hope to add a handful more based on 2022 new de-SPACed companies that were not on the original list on 1/1/22, so the list will likely be between 40-45. Top Picks beat the universe by 13% in 2022.

NEW Portfolio- Clean Energy ETFs. As a benchmark, we used QCLN (First Trust Clean Edge Green Energy Index) but there are many other clean energy and sustainability ETFs to choose from. For purposes of our ETF portfolio, we have selected seven clean energy ETFs that will each have an equal portion of this portfolio. The table below shows the ETF ticker, the size of the ETF, its 2022 return, % of ETF made up by their top 6 holdings, and the top holding of each.

NEW benchmark- Telsa (TSLA). Telsa is more than an electric vehicle company with its products expanding into battery technology, renewables, and autonomous driving. It is one of the most followed stocks in world, so why not track its performance against our other portfolios. Hey, in 2022, our Top Picks portfolio outperformed Tesla (-55% vs -65%).

The second group is Cryptocurrencies and is largely unchanged from our tracking in 2022 with the exception of dropping the creator coin portfolio. It was hard to find a diversified portfolio for this category and, in essence, creator coins are for developing internal economies similar to how credit card points, or airline miles boost engagement with one’s customers (or communities) and therefore not necessarily an investment vehicle.

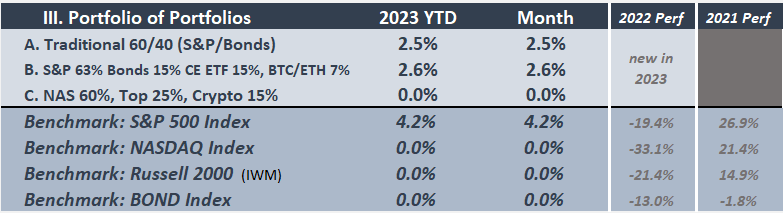

This is a brand-new section - three Portfolio of Portfolios. This section shows how one can build a diversified portfolio through incorporating investments in several categories. The first one is called the “traditional”, a 60/40 strategy split between stocks and bonds used by money managers for a long time, so it could also be called the “boomer” portfolio. The next one is similar to my own allocation to assets: 63% to the S&P index, 15% in bonds, 15% into clean energy (I’ll use the ETF portfolio for purposes here), and 7% into a BTC/ETH 50/50 portfolio. The third and final portfolio is a high-risk allocation between the NASDAQ index (60%), the Top Picks portfolio (25%) and the crypto portfolio (15%). In the benchmark section, the Bond index has been added.

This is also a brand-new section- DCA Portfolios. Since I’ve advocated strongly for dollar-cost averaging, let’s create a few portfolios using DCA and track against the benchmarks. Most of the DCA activity will be buying as of the close of the last day of the month. The one exception is portfolio “D” which will make it buys when the S&P index hits specific lower levels → 10% of investment made on 12/31/22 close (3839) and then another 10% invested at 3700 and each time the S&P drops 100 points all the way down to 2,900. This is an alternative way to employ a DCA strategy. I will likely report on this section on a quarterly basis instead of monthly.

If you made it this far, thank you. I hope you felt it was worth the read. I appreciate you as a subscriber to this newsletter and would love to expand the reach to help more people build their portfolio and achieve above average returns. Please share.

The first 2023 update will be here soon with only one week left in January. It should be a very interesting ride this year.

Efficiently yours,

DT