Don't Forget the Micro "Tells"

Don't Forget the Micro "Tells"

Follow conference calls from "indicator" companies...

Editor’s Note: Thank you for all the comments and “likes” for Sunday’s video post “The Market’s Secret Volatility.” Based on the feedback I received, I’ll continue to stick mainly to written posts in Free Market Speculator with the potential addition of 1 or 2 video posts per month.

I’m also looking at the feasibility of adding a transcript to some future video posts to render the content as useful as possible.

Thanks again for all the input and feedback, it’s greatly appreciated.

—EG

In this service, I spill a great deal of digital ink on “big picture” macroeconomic indicators and trends.

I’m talking about the monthly BLS employment reports, retail sales and the monthly Institute for Supply Management (ISM) Purchasing Managers Index (PMI) to name just a few. However, it’s just as important to keep a close eye on the micro – individual earnings reports and news from key companies in various industries.

I’ll give you an example.

Almost 20 years ago when I started an energy-focused investing service, I would scrutinize every quarterly earnings conference call and analyst Q&A session from Schlumberger (NYSE: SLB), the oil services giant now known simply as SLB Inc. I’d try to listen to, or read transcripts from, every conference where Schlumberger’s management team made a presentation.

I’m not exaggerating when I say these calls were a gold mine – a secret weapon for identifying the most powerful trends and developments in the industry.

Back then, the CEO of Schlumberger was Andrew Gould and he’d not only discuss Schlumberger’s own results but offer wide-ranging commentary regarding all corners of the energy industry. I always found him to be straightforward and frank – he’d highlight areas of concern, or pockets of weakness, as readily as singing his company’s praises.

Through the end of December I’m offering 90-day free trials to the paid tier of The Free Market Speculator, which includes our model portfolio recommendations and special subscriber-only content and alerts.

Try the paid tier of The Free Market Speculator for the next 90 days, and if it’s not for you, for any reason whatsoever, simply cancel before your trial is up and you won’t be charged for the service.

This special Christmas offer is available ONLY through this link:

And Schlumberger was ideally suited to know exactly what was happening in the industry, because the company then (as now) operated in virtually every oil or gas-producing region of the world and performed work for producers of all sizes.

I can’t tell you how many profitable trends Schlumberger helped me identify over the years and, just as important, how many times comments from the company prompted me to recommend selling a stock that was facing headwinds.

And, yes, I still listen to every call from Schlumberger even though Andrew Gould retired as CEO back in 2011 and the company has had two new CEOs since that time.

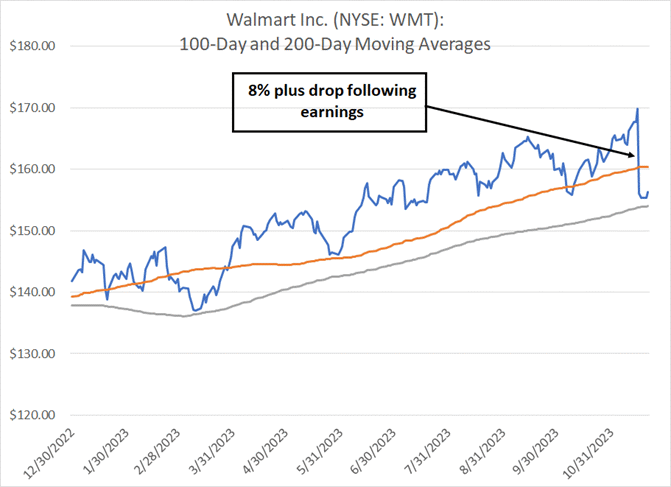

A second example of an “indicator” company I follow is Walmart (NYSE: WMT), the discount retail giant that reported earnings before Thanksgiving week. Since the company sells everything from groceries to electronics, sporting goods, and apparel, and operates in virtually every region of the US, Walmart has unparalleled insight into the health – or lack thereof – of the US consumer.

First up, Walmart shares were crushed following their recent earnings release, declining more than 8% in the trading day after the call:

Source: Bloomberg

And that’s despite the fact WMT beat Wall Street consensus earnings and revenue estimates for its fiscal third quarter and raised guidance for the full year.

The reason for the weakness appears to be management’s cautious tone on the consumer, and consumer spending, as we enter the all-important holiday season. During the prepared remarks management noted:

Turning to guidance. We're confident in our agility and our ability to execute and we're focusing our investment in areas where we can widen our omni advantage, deepen engagement and drive sustained growth in new revenue streams. We like our position relative to competitors as we've maintained strong price gaps and increased share while preserving flexibility to respond to competitive dynamics. But we're not immune from the vagaries of the economy. We see our customers showing ongoing discretion in making trade-offs to be able to afford the things they want given the sustained high cost of the things they need.

Recently, we've experienced a higher degree of variability and weekly performance in between holiday events in the US, including seeing a softening in the back half of October, it was off-trend to the rest of the quarter. Sales during November have turned higher as unseasonal weather abated and we kicked off holiday events.

So, sales have been somewhat uneven and this gives us reason to think slightly more cautiously about the consumer versus 90 days ago. We still expect sales growth to moderate in Q4 versus prior quarters as grocery inflation further normalizes towards historic levels.

Source: Walmart Inc. Q3 Earnings Call November 17, 2023

The good news is prices for some grocery items are beginning to ease from last year’s peak – in particular, WMT’s management team called out lower pricing for dairy, eggs, chicken and seafood calling them “pockets of disinflation.”

However, the bad news is two-fold. First, inflation in other grocery necessities, including beef, dry groceries and consumables, remains elevated.

And, second, just because pricing is lower on a year-over-year basis doesn’t change the fact overall pricing levels are still elevated in absolute terms. For example, comparing overall grocery prices to two years ago, WMT indicated inflation was still up by the “high-teens” percentage range.

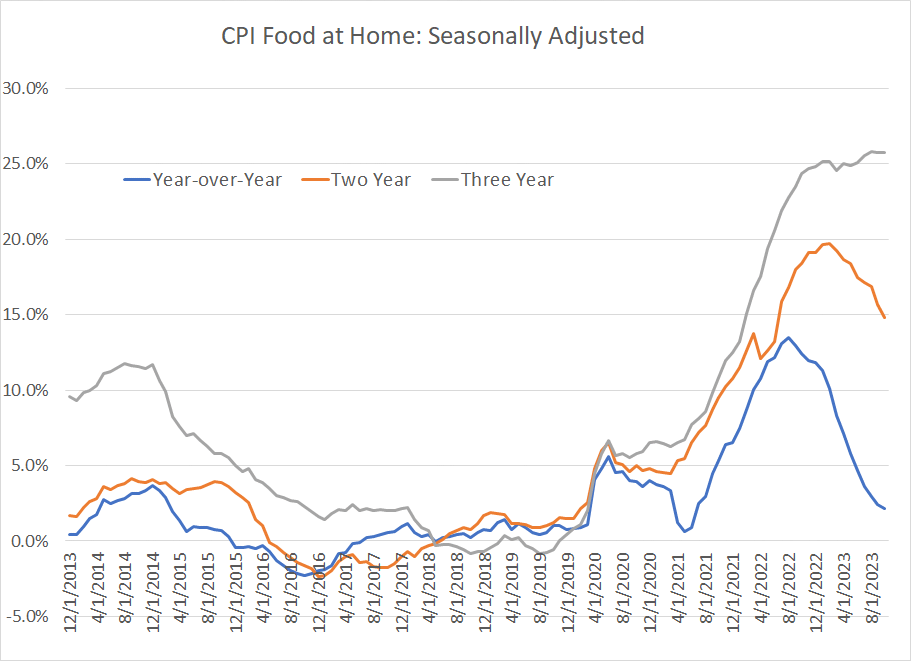

We can see this in the official Bureau of Labor Statistics (BLS) CPI data as well:

Source: Bloomberg, Bureau of Labor Statistics

BLS breaks consumer food price inflation into two main buckets – “Food at Home” and “Food Away from Home.” The former reflects the cost of all sorts of basic grocery items including cereals and bakery products, nonalcoholic beverages, dairy, meats and seafoods. And my chart above shows inflation in Food at Home CPI over 1-, 2-, and 3-year lookback windows.

If you look at the blue line (year-over-year), the data here looks encouraging. While prices are still higher on a year-over-year basis, the rate of inflation is down to +2.1% compared to a peak of +13.5% in August 2022.

However, look at the other two lines on my chart. On a two-year lookback (currently that’s compared to the same period in 2021) food at home CPI is still running +14.8%, down from a peak of +19.7% back in February 2023, but still elevated by any historical yardstick. The three-year lookback is even more worrying at +25.7%, pretty close to the cycle peak of 25.8% set in August 2023, just a few months ago.

And it’s important to put this data in context. As you can see in my chart above, prior to the COVID lockdown mess in 2020, food price inflation was contained for much of the 2013 to 2019 era. In fact, there were plenty of examples in 2016-19 where food costs saw outright deflation, and prices fell for many of the grocery products in the CPI basket.

Think about this from the perspective of an American consumer doing their basic grocery shopping each week. Over the 10+ years leading up to roughly 2021, they’d become accustomed to relatively little net change in the cost of filling up their shopping carts, so the 2021 boom in inflation represented a real shock.

And, amid all the talk of peak inflation on a year-over-year basis, some consumers simply aren’t feeling much relief, because they’re comparing the cost of their current shopping carts to what was considered normal just two or three years ago.

That’s the basic point Walmart drove home in their call – especially for consumers in lower and moderate-income categories, inflation of that magnitude represents a squeeze to household budgets. That’s forcing customers to cut back on purchases of discretionary items including general merchandise products like apparel, sporting goods and electronics.

As Walmart put it – the high cost of things consumers need is forcing them to cut back on the things they want.

What’s really interesting about all this is management’s comments regarding a notable softening in sales, and a lot of week-to-week variability, in the second half of October. Later, in the Q&A portion of the conference call, management indicated the softening in sales was something they had not seen all year until late-October, which prompted them to call it out in their release as a material change in consumer behavior.

Also, during the Q&A portion of the call, Walmart mentioned a number of trends they see impacting the consumer right now including credit tightening and deteriorating balance sheets, the restart of student loan repayments impacting about 27 million Americans and even some anomalous weather ay the end of October that could have impacted Halloween sales.

It's crucial to understand Walmart was NOT saying Christmas season sales would be weak, or that US consumer spending was about to collapse. However, when such an important retailer highlights a meaningful change in the pattern of consumer spending it’s enough to make me sit up and take notice.

A few more comments in the call caught my attention. One point is that while grocery and, particularly, dry groceries and consumables prices are still inflating, management indicated prices for general merchandise products have been coming down for a while now. Management also noted prices have started coming down “more aggressively” into the current quarter (Q4). Indeed, Walmart mentioned that in early 2024 the company could find itself in a “deflationary environment.”

Simply put, when consumer confidence is high, spending and demand growing, you’re unlikely to see outright deflation in the price of discretionary general merchandise items. Brass tacks: Deflation happens when there’s more supply than demand and companies are cutting prices to try to encourage buyers.

This also points to a promotional holiday shopping season in 2023 where retailers will need to offer discounts and other incentives to attract a more price-conscious shopper.

Last point:

On wages. We're staffed, ready for the holiday. For the most part, stores and distribution centers are completely staffed. There are some locations that will continue to hire, and we didn't go out this year with a large number of people that we intended to hire for the holiday. We're happy with our full-time part-time ratio and where we need hours the next few weeks, which is really next week for food leading into the event Wednesday going into the Thanksgiving holidays and Black Friday, we'll be ready to manage the business with our existing associates.

Source: Q&A Portion of Walmart Earnings Call November 17, 2023

Walmart is a major employer in many parts of the US. Coming out of the 2020 COVID lockdowns, the company struggled to hire enough employees to staff its stores and distribution centers; rising wages were a cost headwind for all retailers.

This comment certainly suggests staffing and wage cost inflation aren’t a huge concern for Walmart heading into the busiest season of the year. I suspect this is part of the general softening in the labor market I’ve written about in several recent issues and posts including “Recession Risks Rising.”

Almost three-quarters of fund managers surveyed by Bank of America in their latest Global Fund Manager Survey published on November 14th, now expect the US to avoid recession and see a “soft landing,” up from a similar portion expecting recession a year ago in November 2022. That’s not a good sign – historically, soft landing was the consensus on Wall Street ahead of every recession of the past quarter century.

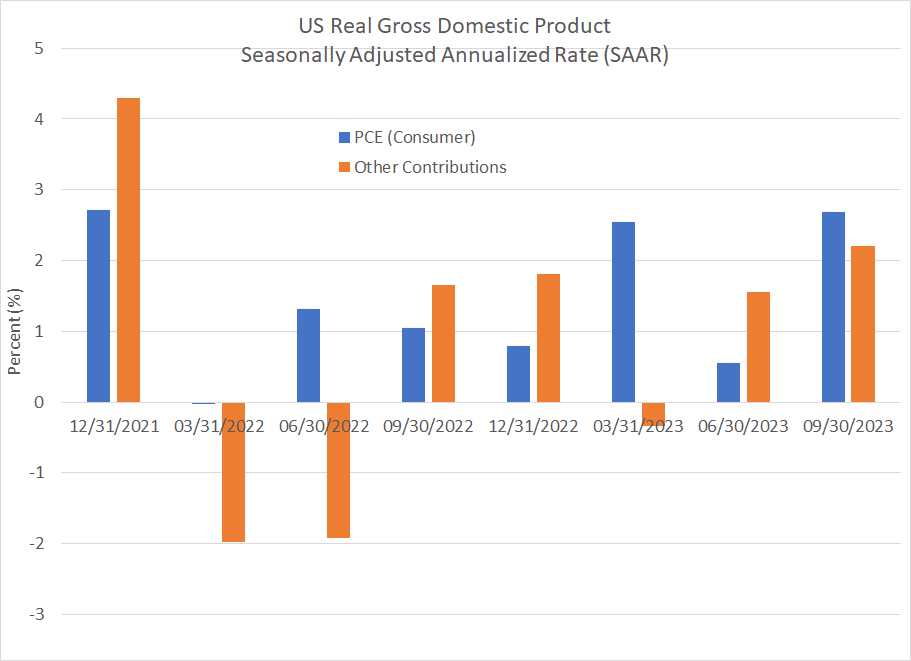

For much of 2022-23 the consumer has been more resilient than most expected, particularly in the face of tightening credit conditions and rising interest rates. That’s helped buoy the economy and avert recession:

Source: Bloomberg, Bureau of Economic Analysis (BEA)

This chart shows the real seasonally adjusted annual rate of US Gross Domestic Product for each quarter since Q4 2021. I’ve broken GDP growth down into two components – consumer spending (blue bars) and everything else. As you can see, the consumer has added to economic growth in every quarter since Q1 2022 and, in many, quarters such as Q2 2022 and Q1 2023 consumer spending has been the only bright spot for the economy.

If Walmart’s comments regarding cracks in US consumer health prove out, those soft-landing hopes could fade quickly. And, with most fund managers positioned fora benign outcome, the impact on stock and bond markets would be dramatic.

My view remains there’s additional short-term seasonal upside for the broader market through yearend or into January; however, the risks continue to mount for the economy and equity markets looking further into 2024. In the model portfolio I’ll continue to recommend ways to benefit from the market upside for now, but I fully expect to be dusting off our trusty recession playbook in the next few months.

With these points in mind, I’m adding a new position to the model portfolio this week:

Actions to Take

Keep reading with a 7-day free trial

Subscribe to The Free Market Speculator to keep reading this post and get 7 days of free access to the full post archives.