Keep Rollin' (In 2024)

When most people think about the future, they ignore that the future is a distribution of possibilities – Howard Marks

December 23, Washington DC. As the winter chill settled over the nation's capital, the corridors of power in Washington were not entirely dormant. A pivotal moment in American economic history unfolded on this crisp December day in 1913. The stage was set for a crucial vote on the Federal Reserve Act, a piece of legislation that aimed to reshape the country's financial landscape.

The timing of the vote added a layer of intrigue to the proceedings. As politicians scurried to finalize their holiday plans and festive cheer echoed through the halls of Congress, the fate of the Federal Reserve hung in the balance. Many key figures were already mentally transitioning to the holiday recess, their attention divided between the weighty matters and the impending respite of the season.

The Federal Reserve Act, despite its historical significance, faced the challenge of navigating the legislative landscape during a time when attention spans were waning. The vote became a testament to the delicate dance between policymaking and the broader rhythms of political life. Critics argue that the holiday timing might have played a role in the Act's passage, as key opponents may have been absent or less engaged during the vote.

Nonetheless, as the vote took place in those final days leading up to Christmas, the Federal Reserve Act secured its place in history. The twelve Federal Reserve Districts, each with its Reserve Bank, became the new framework for American monetary policy. The Act's proponents celebrated its passage as a crucial step towards a more stable and responsive financial system capable of addressing the challenges of an evolving economic landscape.

In the early years following its establishment, the Fed embarked on a journey to assert its role and navigate the challenges of a rapidly changing economic landscape. The Federal Reserve Act granted the institution the responsibility to conduct monetary policy and promote stability. Still, the interpretation and execution of these mandates required a period of trial and error. During the First World War, the Fed played a critical role in financing the war effort and managing the economic repercussions of the conflict. It implemented policies to control inflation, stabilize prices, and support the issuance of government bonds. Post-war, the Fed faced the monumental task of transitioning the economy from a wartime footing to peacetime conditions, bringing its own challenges, including shifts in demand and production.

The early years of the Fed were marked by a series of experiments in monetary policy and attempts to find the right balance between intervention and laissez-faire economics. The 1920s saw a period of relative economic stability, followed by the devastating crash of 1929 and the subsequent Great Depression. The Fed's response during these years came under scrutiny, with debates about its effectiveness in preventing and mitigating economic crises. The early history of the Federal Reserve reflects the institution's learning curve and the evolving nature of central banking as it adapted to the complex dynamics of the US economy.

It's somewhat amusing that the Federal Reserve's birthday, marking the inception of modern central banking, falls so close to Christmas, the world's most celebrated day. Intriguingly, a cult of personality has developed around the key figures of central banks within financial markets. Whenever they or their board members address an audience, market participants listen attentively, parsing every word spoken.

Remarkably, in the initial decades after the Fed's establishment, public interest in central bank policy was considerably lower than it is today. It can be argued that the more central banks intervened, the more people focused on them. Eventually, central banks acknowledged the growing interest and adopted more proactive communication strategies.

Since the 1980s, the impact of market movements in response to central bank communications has intensified, further magnified by increased guidance, forward guidance, and more significant intervention within financial markets.

This week was a "Super Central Bank Week" with decisions from the Fed, the ECB, and the Bank of England. As of my writing, only the FOMC meeting has concluded, and as anticipated, the Federal Reserve maintained unchanged interest rates. Considering the persistently decelerating consumer price inflation in November, the ECB and the Bank of England will likely follow suit, providing no impetus for a rate hike.

While the opening statement remained largely unchanged, market attention primarily focused on alterations to the Fed's dot plot, representing the expected Fed Funds Rate for each FOMC member. According to the dot plot, the median projection for the Fed Funds Rate at the end of next year dropped from 5.1% to 4.6%. Notably, the Fed shifted one projected rate cut from 2025 to 2024, indicating that FOMC members anticipate the same rate cuts by the end of 2025.

Market participants interpreted this as a significant pivot by the Fed. Bond prices surged, the two-year yield dropped approximately 30 basis points, and the 10-year yield fell below 4%. Equally, stock market participants welcomed the pivot, with every US index experiencing a rally. It appears that my intuition about the Russell 2000 benefiting the most from the pivot was accurate, as it emerged as the best-performing index after the FOMC decision.

Regarding economic activity, the Fed noted the following:

The statement also noted that the economy “has slowed,” after saying in November that activity had “expanded at a strong pace.”

In the news conference, Powell said: “Recent indicators suggest that growth in economic activity has slowed substantially from the outsized pace seen in the third quarter. Even so, GDP is on track to expand around 2.5% for the year as a whole.”

Conversely, the Fed appears willing to continue with Quantitative Tightening, even though it might cut interest rates more than previously thought. Interestingly, the market paid little attention to that and celebrated the "good news" of the upcoming Fed pivot.

However, market participants shouldn't interpret Powell's remarks as an ultra-dovish shift. The changes in the FOMC projections solely reflect the latest drop in consumer price inflation, but that doesn't change the fact that real interest rates are still positive. As long as they remain positive, they'll undoubtedly dampen economic activity moving forward into 2024.

Looking ahead, the future development of consumer price inflation will remain an essential variable for future central bank policy. The Fed projects core inflation to fall to 3.2% by year-end and to be at 2.4% in a year. In the Eurozone, the ECB projects inflation to fall to 3.2% by the end of 2024.

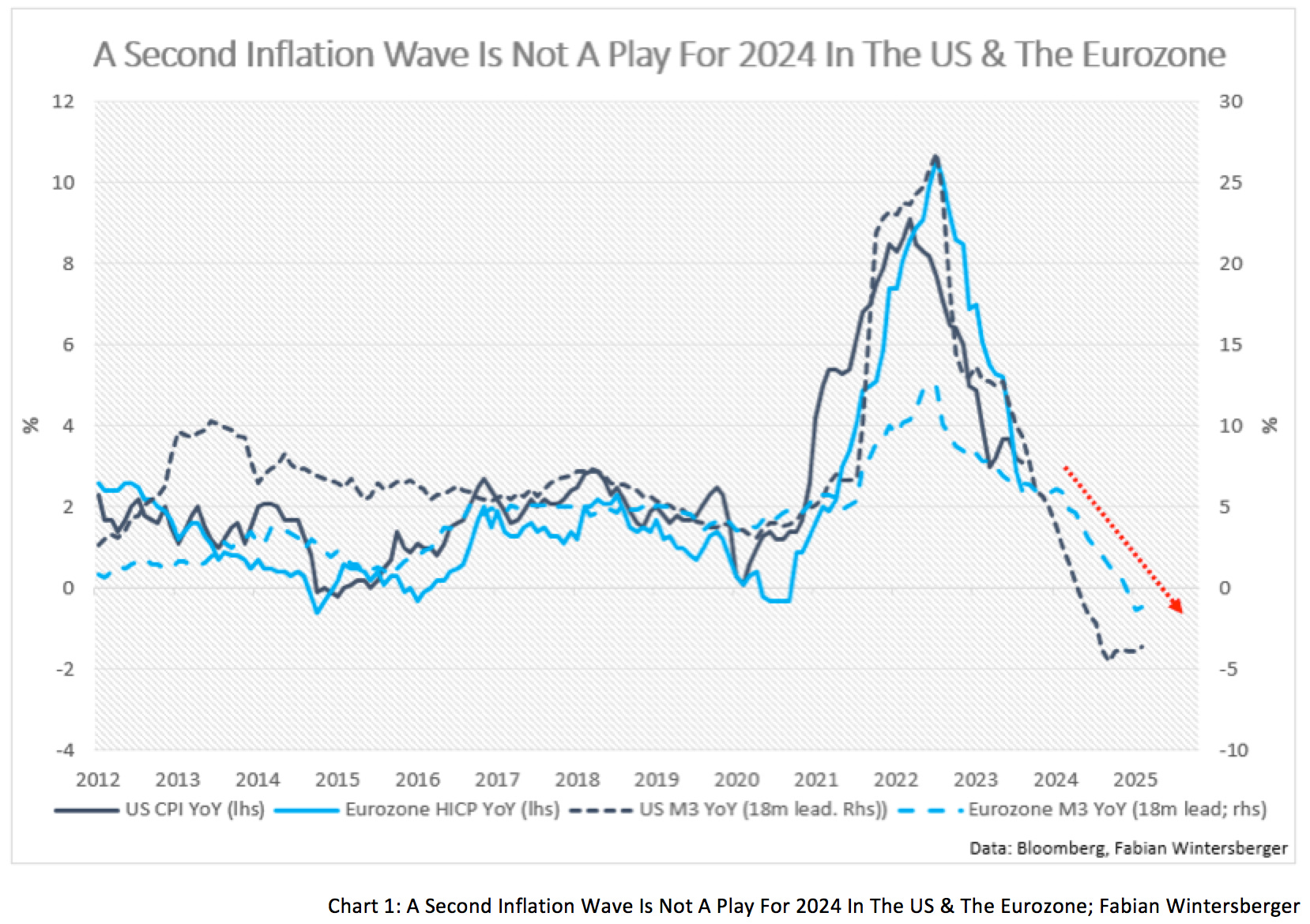

Some financial commentators fear that the projected monetary easing could result in a resurgence of inflation in 2024. However, most of them pay very little attention to changes in broad money supply and thus conflate relative price changes with increases in the general price level. In both the Eurozone and the US, the broad money supply has been contracting for quite a while now.

Looking at the money supply, fears of a second wave of inflation in 2024 are unwarranted. Changes in the money supply will affect the broader economy with a lag of about 18 months, which means that the projected rate cuts in 2024 will not influence inflation sooner than in 2025 or 2026. In fact, it seems that the Fed's and the ECB's projections are too high, and inflation might turn into deflation in the second half of 2024.

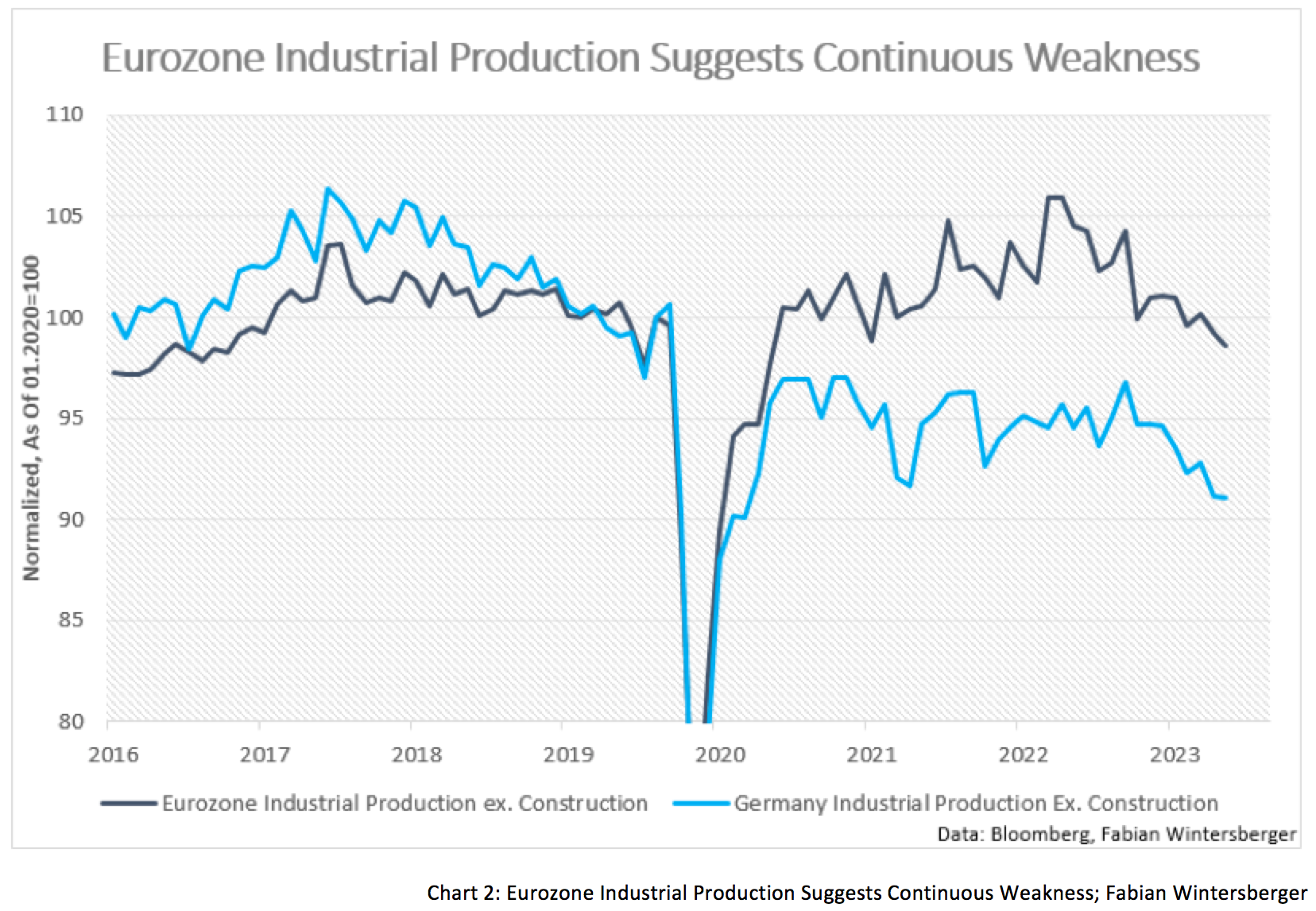

Before delving into what's in store for financial markets in 2024, let's take a closer look at the economy. Beginning with the Eurozone, the latest figures indicate an overall contraction in industrial production. Recent ZEW numbers reveal that investors remain pretty pessimistic about the present situation, but there is optimism that things will improve in the future.

Most economists in the Eurozone anticipate economic growth next year, signaling the potential end of the current recession. However, businesses, particularly small and medium enterprises (SMEs), appear less optimistic. According to the German Middlestand and Economic Union, German SMEs are in a precarious situation. Insolvencies have sharply risen, and orders continue to decline.

Meanwhile, the German government coalition has put forth a revised budget that could act as another drag on economic activity, containing spending cuts and higher taxes. As reported by Reuters:

The government will save 1.4 billion euros per year with new plastic regulations. In the future, companies that put plastic into circulation will pay the levy, which was previously paid by the German government to the EU.

A CO2 surcharge on fuel, heating oil and gas is to be increased, under the coalition agreement.

Considering this, it's challenging to envision robust economic growth for the German economy, and consequently, the entire Eurozone, in the coming year, even though the first quarter might hold some positive surprises. Overall, however, industrial production signals continued weakness. Since 2020, German industrial production has declined by nearly 10%, with a corresponding decrease of about 1.5% in the Eurozone.

Considering all these factors, my intuition tells me that the ECB will need to cut interest rates more extensively than the current market expectations, and QT might transform back into QE. It's worth noting that, in reality, QE never genuinely ended for Italy. To this day, the ECB is still purchasing Italian government bonds, and if the crisis escalates next year, it will likely increase its purchases again.

Let's shift our focus to the US economy. Currently, an increasing number of analysts and economists echo Claudia Sahm's assertion that economic actors are faring better than pre-pandemic, while surveys indicate the opposite. However, the latest NFP report from last Friday can be viewed as another supporting point for the advocates of a soft landing.

As mentioned earlier, the Federal Reserve has acknowledged that economic activity has been slowing considerably. The recent decline in inflation means that real wages are once again slightly positive on a year-over-year basis. However, this is merely a consequence of disinflation and doesn't necessarily translate into a brighter economic environment.

I've delved into the recent surge in debt-financed consumption, but debt levels are relatively low concerning financial wealth. Nonetheless, beyond the challenges posed by aggregate numbers, the issue arises because, for many Americans, the increase in financial wealth exists mainly on paper due to house price appreciation.

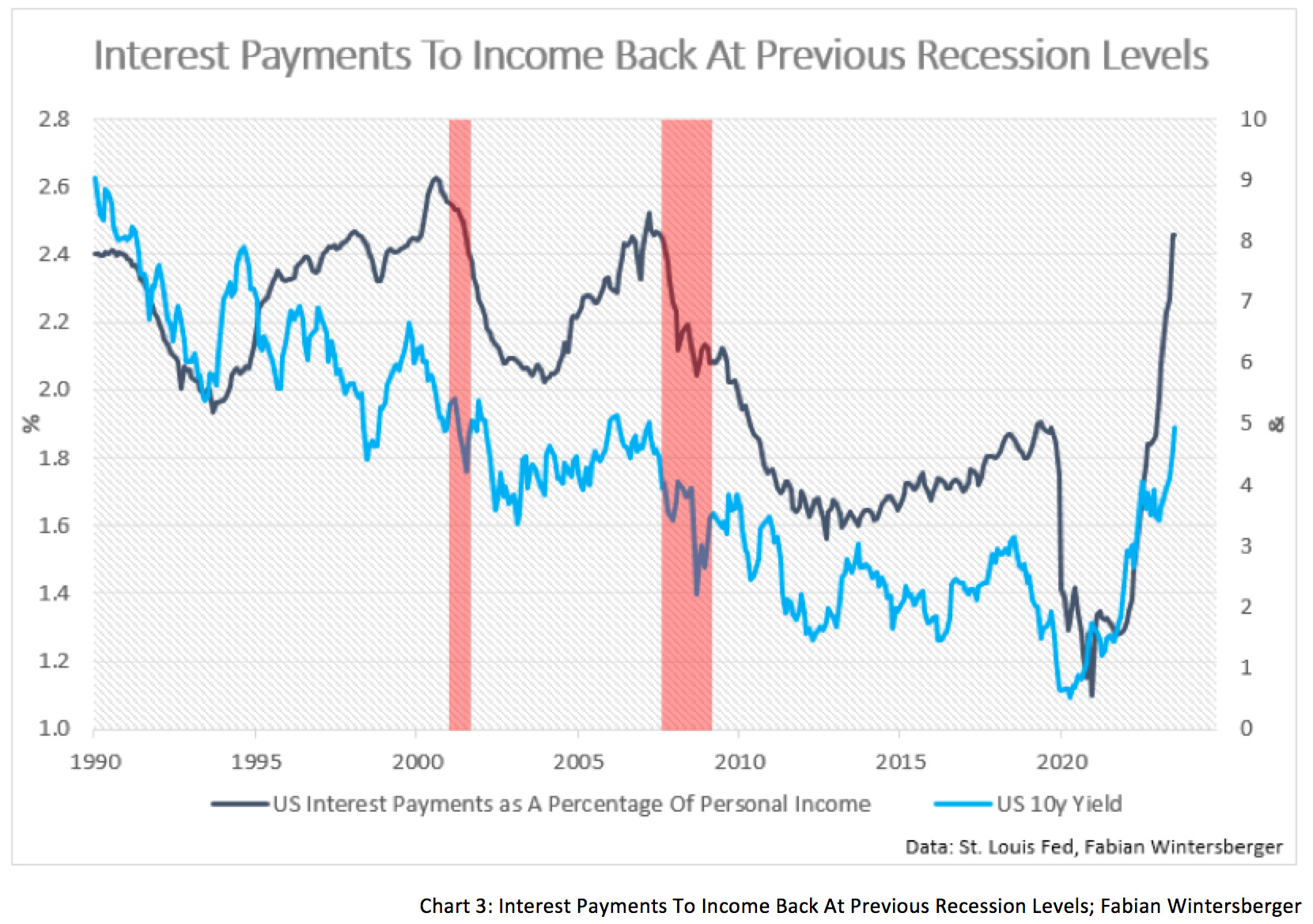

When comparing interest payments to income, the narrative takes a different turn. Due to the surge in interest rates, interest payments have risen sharply, outpacing income growth. Consequently, interest payments relative to income have returned to levels seen in previous recessions.

Hence, I believe the consensus has again misjudged the situation, and a soft landing will not materialize. Those who advocate for a no-landing scenario for the US economy will also find themselves on the wrong side. The fact that market participants are pricing in a soft landing doesn't deviate from past recessions, where the assumption was often that a soft landing could be achieved.

Let's now focus on assessing what this means for financial markets in 2024, although I must disappoint you if you seek forecasts pinpointing where markets will be in December 2024. Ultimately, most forecasts you encounter these days are likely to prove inaccurate as input variables are constantly in flux.

Most Wall Street firms project that the S&P 500 will be at or above 5,000 points by year-end. The most pessimistic outlook comes from Morgan Stanley, forecasting a year-end close for the S&P 500 at 4,500, approximately 200 points lower than its current level.

However, I anticipate that stock markets will surge to new all-time highs in the short term, exhibiting a classic blow-off top. Ongoing disinflation and rising probabilities of future rate cuts will be seen as a tailwind for the stock market, overshadowing the fact that real interest rates will remain more restrictive than they were during the 2010s.

Contrary to the prevailing sentiment, I don't believe that Jerome Powell and his colleagues at the Fed will aggressively cut interest rates as soon as signs of an economic slowdown emerge. Doing so would contradict everything Powell has communicated over the last two years. I expect the Fed to maintain positive real interest rates for a more extended period than other central banks.

Regarding the bond market, I don't foresee a return to the low-interest rate environment of the 2010s but rather anticipate a continuation of the counter move that has already begun. However, the economy may fare better than initially expected at the start of the year, potentially pushing the US 10-year yield back up close to 5%. In my opinion, this suggests a cautious long position in the bond market could be considered.

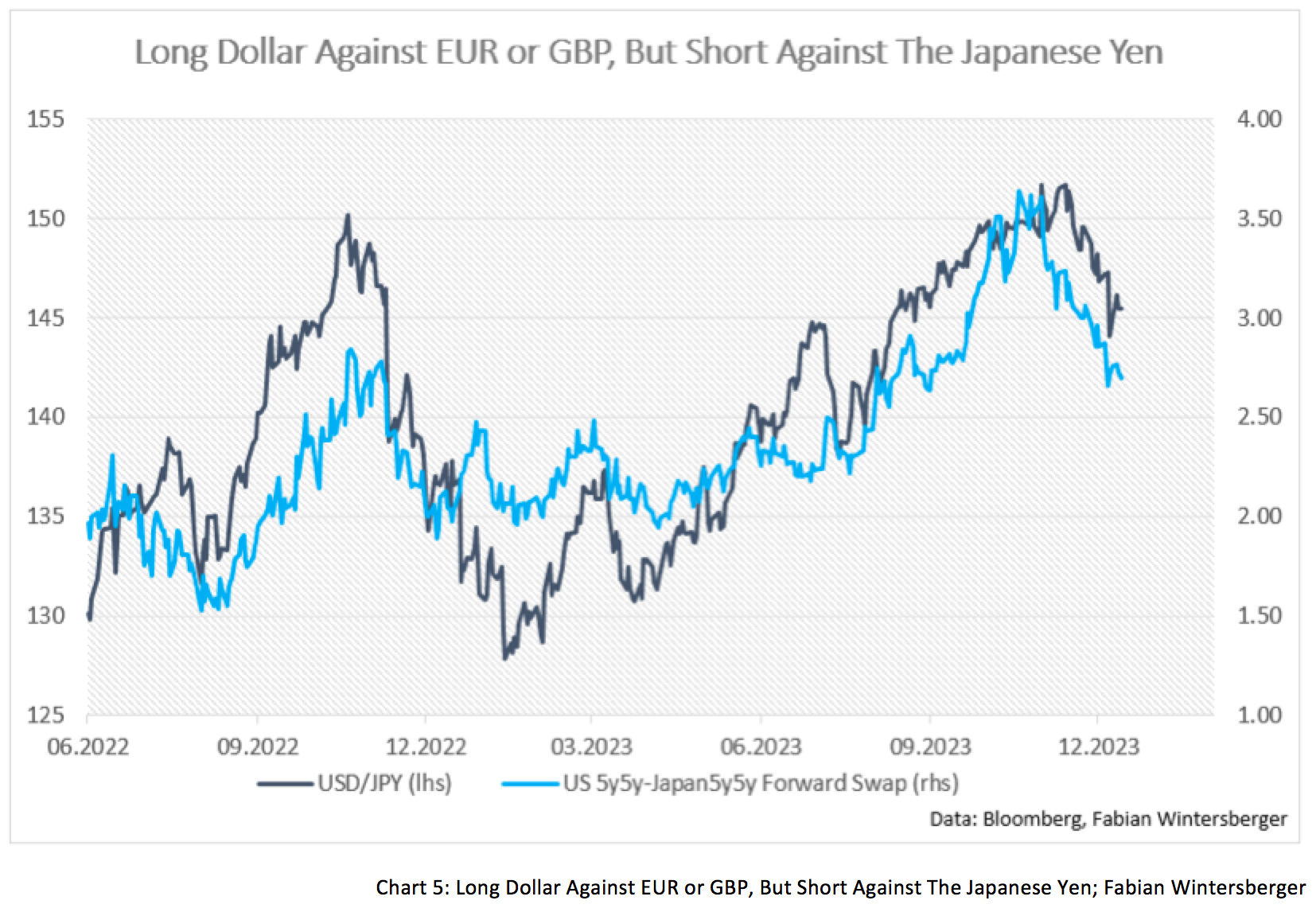

Bond traders should closely monitor the actions of the Bank of Japan in this regard. Japan has yet to tighten its monetary policy, meaning that in the event of easing from the ECB or the Fed, the Bank of Japan may not ease as extensively. This would render domestic bonds more appealing to Japanese investors, potentially supporting another uptick in global yields.

Lastly, I'd like to touch on foreign exchange markets briefly. The dollar has recently weakened, and the consensus is positioned for a sustained period of weakness. However, as I mentioned earlier, I don't believe the Fed will ease monetary policy as much as other central banks. Consequently, I maintain the viewpoint that shorting the rallies in EUR/USD will be a more favorable trade than shorting the dollar.

The Japanese Yen is the only currency I anticipate strengthening against the US dollar. This is because rate differentials will likely narrow in the upcoming Fed rate-cutting cycle. When examining 5y5y differentials, it appears the dollar is already overvalued relative to the Yen.

I feel that the 2020s will continue to be a rollercoaster for financial markets. Although the overall trend of higher yields will persist, I anticipate that 2024 will bring lower bond yields. The stock market will reach new all-time highs and then face challenges before experiencing a decline, especially if the hard-landing scenario materializes.

Overall, one can assert that financial markets will remain as intriguing as in previous years.

Keep rollin’, rollin’, rollin’, rollin’ (uh)

Keep rollin’, rollin’, rollin’, rollin’ (what)Limp Bizkit – Rolling

This marks the final edition of Weekly Wintersberger for this year. The next installment will be published on January 12.

I wish you all a Merry Christmas and a Happy New Year!

Fabian Wintersberger

Thank you for taking the time to read! If you enjoy my writing, you can subscribe to receive each post directly in your inbox. Additionally, sharing it on social media or giving the post a thumbs-up would be greatly appreciated!

(Please note that all posts reflect my personal opinions and do not represent the views of any individuals, institutions, or organizations I may or may not be professionally or personally affiliated with. They do not constitute investment advice, and my perspective may change in response to evolving facts.)

really interesting point about debt service /income vis-a-vis debt service /wealth and the strains it may create. I am with you on early strength and then a reversal. the sugar high of this pivot concept is going to fade. the one potential offset is the fact that it is an election year and Yellen will do all she can to stimulate the economy