Red Flag Alert – Something Doesn’t Add Up

Red Flag Alert – Something Doesn’t Add Up

The Curious Case of Paycom

Sometimes something is so bad that you just know there’s more to the story.

Such is the case with Paycom Software ($PAYC), a onetime growth stock superstar and maker of payroll and human resources software… whose shares over the past two years have gone through a series of upheavals.

It was the latest, however, that makes you wonder what’s really going on. And which is why, even after the stock’s latest collapse three months ago – in response to third quarter earnings – Paycom warrants a red flag as a stock to avoid...

And that won’t likely change anytime soon, even if numbers are good when the company reports its fourth quarter after the market’s close tomorrow.

That’s because what happened a quarter ago can’t or shouldn’t right or reverse itself so quickly – and certainly not without a good explanation.

I’d go so far as to say that if it did or does, that would raise even more red flags.

Where Our Story Begins…

Remarkably, outside of a few headlines and quick summaries, virtually nothing has been written about why Paycom’s stock tumbled by 37% overnight on shockingly bad revenue guidance... prompting a herd of analyst downgrades.

Nothing, that is, but an exceptionally well-done chronology in this class action lawsuit, which I stumbled on after I had heard the story and dug in myself.

Many investors ignore shareholder class action lawsuits. But this one tells quite a tale. (The company, the best I can tell, hasn’t yet responded.) And I’m guessing the amended suit, if there is one, will be even better, since amended suits tend to include interviews with former employees.

Even without any insider insights, everything that happened was in plain sight in public filings and transcripts.

The Setup…

With a history of seemingly solid execution, investors had come to expect 20%-plus revenue growth at Paycom. The company had initially set its 2023 revenue growth rate at 24% in February, raising it to 25% in May. By August, it had raised the actual dollar amount slightly, keeping the growth rate at 25%.

Enter the third quarter call in November... CFO Craig Bolete stunned investors when he said that fourth quarter growth would be around 14%. But the real jolt was two minutes later, as he wrapped up the scripted portion of his call, when he went on to say...

...we believe it is prudent for us to set expectations for 2024 year-over-year revenue growth of between 10% and 12%.

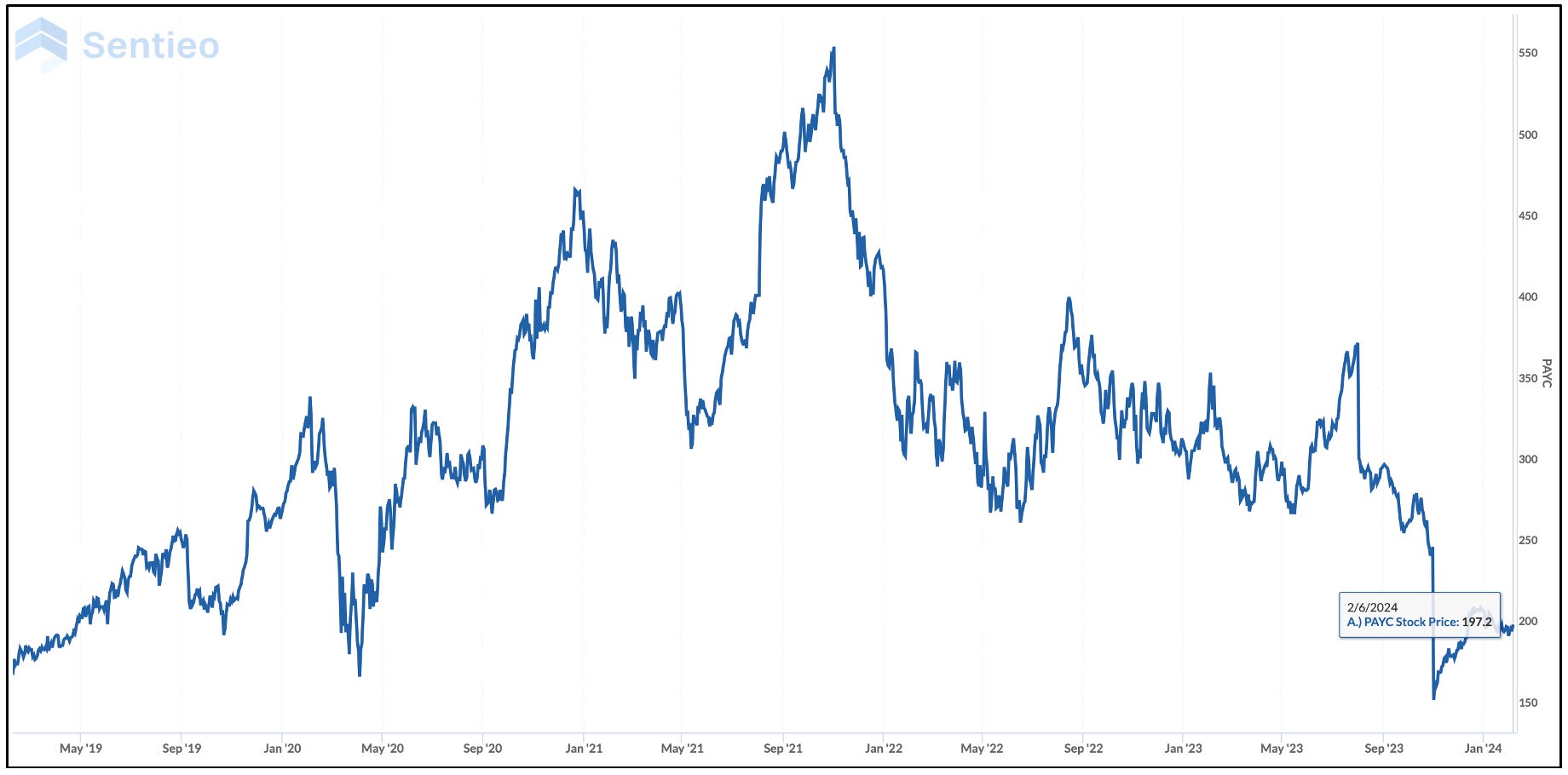

As the chart below (courtesy Aiera) shows, during the call savvy investors immediately started to sell.

That was after the market closed. The real action, as this six-month chart shows, was the next day.

And while the stock has recovered some, it’s still far off its pre-call highs.

No Warning

Here’s the thing...

Companies don’t just cut guidance by that much – like that – without some kind of warning. Doing so, suggests something more might be lurking under the surface. That’s especially true with Paycom, where there wasn’t a hint that anything was amiss other than a surprising slip in the gross margin in the second quarter in August – the one where the dollar amount of revenue guidance had been tweaked higher.

And while the actual number was slightly higher, it wasn’t as much as some analysts had expected. One analyst asked whether the lack of a bigger step-up means “you’re kind of slightly concerned about the second half of the year?”

CEO Chad Richison gave a long, winding response that didn’t really answer the question. (Though, in retrospect, a forensic might very well have seen right through it.)

Another analyst wondered if real revenue growth rates were closer to “the low-20s.” Boelte responded (emphasis added)...

As we looked at guidance, we're still guiding to 25% for the full year and 42% adjusted EBITDA. We haven't given any long-term guidance in terms of revenue, but we have a large opportunity in front of us. We had several announcements on this call. And so, the opportunity is definitely there. It's just up to us to go out and achieve that.

The obvious question... what happened?

The Culprit: Cannibalization

This, as you might guess, is where the story gets interesting...

Paycom blamed the sudden upheaval in its growth on the success of a new software program it rolled out in 2021, dubbed Beti, which stands for the Better Employee Transaction Interface.

The company touts Beti as “an industry-first technology that further automates and streamlines the payroll process, by empowering employees to do their own payroll, which increases efficiencies and reduces errors.”

To hear management tell it, Beti is so good it resulted in fewer “unscheduled payroll runs.” In fact, Boelte explained, it’s “cannibalizing a portion of our services and unscheduled revenue.”

Wait… What?

Cannibalizing a portion of its business? Unscheduled payroll runs?

Based on my scour of filings and transcripts, this was the first time Paycom ever suggested that Beti could cannibalize its existing business... or worse, somehow have a negative impact.

As for unscheduled payroll runs: Until the third quarter, they had never been mentioned on any earnings call, and were only cited eight times in the company’s recent 10-Ks... and never as a risk related to the rollout of Beti. And never with a full explanation about what they are, or quantifying their significance to the company.

What’s clear is that something isn’t quite right at Paycom... and it may be deeper than the cannibalization related to Beti.

Enter… The Secret Recording

Last month The Lost Ogle, which refers to itself as “Oklahoma City’s most popular, revered, and influential digital media publication,” published what it claimed to be a secretly recorded “all-hands on deck product department staff meeting” led by Richison.

Or as The Lost Ogle put it...

Taking place on January 9th, Richison told his product team that he’s “embarrassed” by the company’s software and that he’s canceling all of his 2024 ski trips because the only thing he wants to do in 2024 is “fix the product.”

The publication, which at times injects satire and humor into its stories, added...

Man. You know a company’s software must suck when its billionaire founder and CEO cancels his ski trip to stay in Oklahoma!

Nailed by the SEC

Founded in 1998, Paycom rapidly rose to rank among the fastest growing companies in America. From its IPO at $15 in 2014, its stock went on to peak above $500 in late 2021... even after it was nailed a few months earlier by the SEC for overbilling clients.

Since becoming a public company in April 2014, Paycom has overstated its reported recurring revenues for 2011 through 2020 as a result of "reselling" certain services, i.e., billing its clients for services for which the clients were already paying.

The company agreed to pay a fine of $250,000, plus returning $2.8 million to customers who had been double-billed.

The fine and amount of double-billing was small relative to the size of the company, which this year is expected to generate revenue of roughly $1.6 billion. But when combined with a few other things, the SEC action was against a backdrop of an aggressive culture in an industry that is only getting more competitive.

Or as Kerrisdale Capital wrote in July 2022 in what, as it turns out, was an exceedingly prescient report...

Paycom may be one of the best performing software stocks since its IPO, but its industry is becoming saturated and commodified, and competition is becoming ever more brutal.

The red flags don’t stop there...

The Company Plane

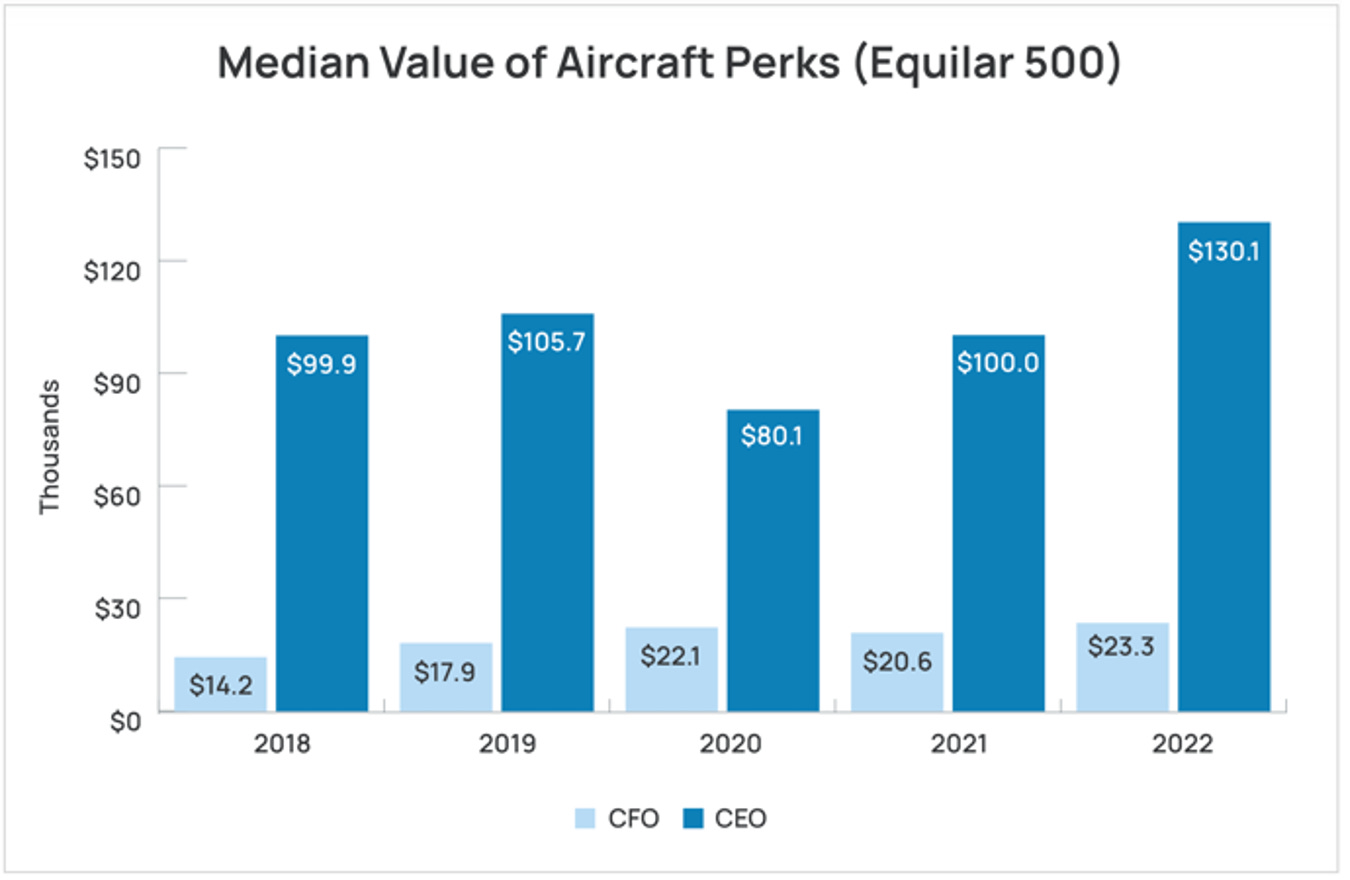

Consider, for example, CEO Richison’s personal use of a company plane. It’s not unusual for top executives to use the company’s plane for non-business uses, with the company footing the bill.

According to Equilar, 45% of CEOs of the top 500 companies ranked by revenue received aircraft perks in 2022, with a median value of $130,000.

By contrast, Paycom’s most recent proxy shows that Richison’s compensation included $637,462 for his “non-company use” of the company plane. Not only is that considerably more than executives at much larger companies, but the amount has nearly quadrupled over the prior five years.

Paycom also picks up $138,594 for his “personal security detail” and the $10,500 tab for his country club, as well as health benefits and his 401(k) match.

Compared with Peers

By contrast, the CEO of his closest competitor, Paylocity – which is close in size – is not compensated for use of a company plane, a security detail or country club membership. His other compensation is a mere $25,000, which includes the company’s match to his 401(k), executive health and wellness screening and “spousal travel benefits.”

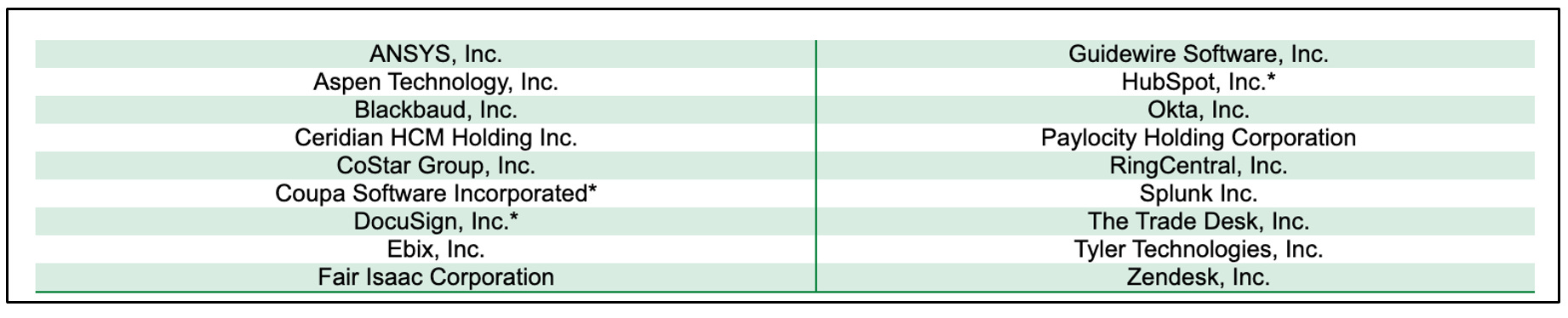

What’s more, of the 18 companies in the peer group cited by Paycom in its proxy for compensation purposes, only two others – CoStar Group and Ring Central – reported compensation for personal aircraft purposes.

The reimbursement at CoStar – whose market cap and revenue are substantially larger than Paycom – was less than half Paycom’s.

Speaking of planes: Paycom, which is based in Oklahoma City, discloses that it leases its plane from Oklahoma Aviation. As it turns out, Boelte, the CFO, owns a plane there. In 2022 and early 2023, the company said it paid Oklahoma Aviation $120,502 to use Boelte’s plane. It’s unclear how much of that went to Boelte.

Other Items of Interest…

Stock buybacks. Paycom talks a lot about how much money it is returning to shareholders via stock buybacks.

However, unlike most companies that tout share repurchases, Paycom’s outstanding share count doesn’t budge. Typically, the benefit to shareholders is when the share count falls, leaving them with a bigger piece of the pie.

With Paycom, it seems the biggest winners are executives, since either all or part of the repurchases have been used to satisfy tax obligations “for certain employees” when their restricted stock vests.

Stock incentives. And in a sign of hubris from the bygone days of the pandemic/zero interest rate-fueled stock market bubble...

On November 23, 2020, as Paycom’s shares sailed above $400, the company granted Richison 1.6 million shares of restricted stock that vest in two equal tranches: The first, if the stock hits or exceeds $1,000 and stays there for 20 consecutive days within six years of the grant; the second, if the stock hits $1,750 within 10 years.

The company called the stock “a powerful motivating tool to encourage Mr. Richison to continue to deliver performance over the 10-year period...”

Hubris Gets Humbling

Maybe, but targets like that also suggests corporate ego run amuck, which can be exactly when missteps and overly ambitious projections happen.

If in doubt, look no further than something else Paycom did near the peak of the market’s insanity in 2021, when the company purchased the naming rights to the downtown Oklahoma City arena, home to the Oklahoma City Thunder National Basketball Association franchise.

Before becoming Paycom Center, it had been known as Chesapeake Energy Center. Once high-flying Chesapeake – whose colorful founder and CEO Aubrey McClendon died in a car crash in 2016 – filed for bankruptcy a few years later.

In the press release announcing its deal with the arena, Paycom made a point of saying that its stock market value was around $23 billion.

Today it’s less than half that.

The stadium curse, as it’s sometimes known, strikes again.

As usual, if you liked this please click the heart button below and feel free to share with your friends.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!)

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Twitter (X) and Threads @herbgreenberg.

That airplane sleight of hand is clever. The even greater 'voila' will be when a C-suite also owns the real estate to which the naming rights fees get remitted....

The stadium curse strikes again!