Investing in Carbon Credits

I recently learned about the Carbon Credit market… and it blew my mind. Carbon credits are beautifully uncorrelated to everything else in the stock market and have unique structural downside protections - i.e., an Auction Reserve Price (“a price floor”) that rises yearly by 5% + the annual CPI inflation report.

I’ve invested a small amount of money into the following two stocks: KraneShares California Carbon ETF (KCCA 0.00%↑) & KarenShares Global Carbon ETF (KRBN 0.00%↑) for exposure to the carbon credit market in California and the rest of the world.

Since launching in 2021, KCCA 0.00%↑ has gained +10%

While KRBN 0.00%↑ has gained +90%

What are CCAs? CCAs are tradable carbon emission credits under the California Cap-and-Trade system. Each carbon credit gives a business the right to emit 1 ton of greenhouse gasses into the atmosphere. A business that is a “carbon emitter” (think utility companies, oil refiners, dairy farms, industry, etc.) must acquire and redeem 1 carbon credit for each ton of carbon emissions they release in a year. They acquire carbon credits in only two ways: 1. For free from the State (30%) & 2. buy them at quarterly auctions (70%). They can also buy or sell these carbon credits in secondary transactions with other companies or through listed carbon credit futures contracts.

In a marriage of capitalism and policy, CARB (California Air Resources Board) authorizes certain financial players or non-compliance entities to hold carbon credits. They’re effectively seeking to create a market-derived equilibrium in the price of carbon credits that helps push the overall trend towards reduced carbon emissions.

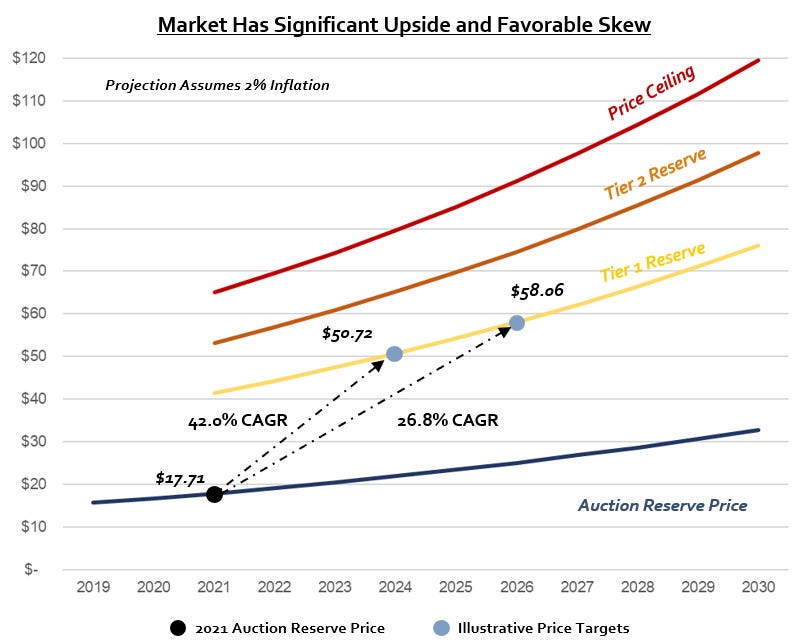

So far, through implementing a steadily rising minimum floor price and by steadily decreasing supply, the California government has been successful in their goal of creating a market structure that pushes the price of carbon credits up over time. We can see the effect of this practically by observing the trend of carbon prices over time at auction.

(Source: California Air Resources Board, found in “Summary of Auction Settlement Prices and Results” PDF)

The current CCA program was launched in 2013 to follow through on a bipartisan mandate to achieve a 40% reduction in carbon emissions versus 1990 levels by 2030. California has since expanded its long-term mandate to include complete carbon neutrality by 2045; however, the current Cap-and-Trade law creates the carbon credit market running through 2030.

Why are carbon credits destined to rise? The core of the thesis is that the program is very ambitious and there are significant impediments to successful de-carbonization by industry in the near term. Therefore, significantly higher upfront prices for carbon credits are needed to drive any meaningful progress toward California's carbon-neutral climate goal.

The path to the 2030 goal requires a reduction in emission by about 4% per year. But the industry has been struggling to reduce emissions at all, despite significant investments in clean energy. Thus, even with the temporary emissions reprieve caused by COVID lockdowns, California is far away from achieving it’s emissions goal.

In the early years of a Cap-and-Trade program, the supply of carbon credits is plentiful and the price floor is low. This allows carbon emitters to ease in and gradually get used to the system. Then, each year the the new supply of carbon credits is reduced and the price floor is increased.

But now, we have reached the “middle innings” of the program timeline, and moving forward, the demand for carbon credits will likely outstrip future supply. The total amount of purchasable carbon credits has already peaked, and is beginning to contract. The issue will grow more and more acute in the later years of the program. Expect the market to react to the oncoming shortage in the near term as speculative interest increases and buyers adjust their behaviors. That is a beautifully skewed risk/reward.

What could go wrong? We break the risks down into five buckets and discuss why we find each highly-unlikely to derail our thesis. The risk buckets are: 1) California adversely amends, 2) Federal pre-emption concerns, 3) Businesses leave CA, 4) technology breakthroughs lower emissions, and 5) market concerns (liquidity, etc.).

California is not likely to back off or adversely amend the Carbon Credits program. I think a tightening of supply and higher prices a reasonable probability, but I also think it is very low likelihood that California acts adversely. They have a demonstrated history of taking the lead on climate reform and strengthening their objectives. The Cap-and-Trade law is settled legislation with bipartisan support. The revenues from the program are critical and growing larger and more important to the budget over time. California has fought through constitutional challenges and industry outcry and only deepened its commitment to ambitious climate objectives, like the 2045 carbon neutrality order of 2018.

There are no plans for the federal government to impose a carbon tax. It is well settled with policy makers that federal follow-through on this point will be complementary, not pre-emptive of California Cap-and-Trade. We expect many more states to either petition California to join their market (on terms at least as strict as current) or to form their own carbon allowance markets modeled after California.

High tax states like CA and NY are nothing new and there is some reasonable premium that businesses and consumers bear for locating there. Cap-and-Trade can certainly push the boundaries here down the road, but ultimately businesses don’t have enough mobility in the short term to materially affect near term supply/demand models.

Similarly, it doesn't seem possible in the near term for technological breakthroughs to meaningfully alter the path to carbon credit shortage. Even if EVs were to be adopted at a rate 2x faster than expected, the impact would not be significant in the 3-4 year trading horizon.

Currently, the CCA market is large and liquid and dominated about 5 to 1 by “covered emitters” versus financial participants. Futures trading volumes of the front month routinely exceeds $2 billion per month and transaction costs are low. Market participants are limited in the amount they can bank and CARB controls the number of market participants. Liquidity is therefor super-adequate at present to build, adjust and monetize holdings of CCAs, but it’s certainly something that could fall apart at any point.