Floor and Decor

Floor and Decor

Could it be a $15-$20 billion dollar company in 5 years?

Since I did my last FND 0.00%↑ article a few assumptions have changed but my interest in the company has not. Floor and decor remains the single best one stop shop for hard surface flooring and accessories and continues to take market share from other retailers. They have recently seen a slow down in revenue and a decrease in comparable store sales. This may present an opportunity if there is a further sell off.

My basic thesis for Floor and Decor has been that they will continue to take market share from other competitors including major retailers like Home Depot, Lowes, Dal-Tile and The Tile Shop. Im familiar with this company because Im a general contractor that specializes in remodels. This company has become the go to store for our crew and virtually all of our customers are referred to Floor and Decor when choosing any hard surface flooring or tile or wall tile.

Floor and Decor is a simple understandable business. They provide a one stop shop for an underserved niche in construction which is hard surface flooring and tile. Their product categories include various wood and vinyl flooring applications, wall tile, shower tile, floor tile, bathroom and kitchen vanities and “decor’. They also sell virtually all installation accessories, tools and building materials necessary for doing the job. The majority of their revenue comes from laminate and vinyl, more specifically a product called LVP (Luxury Vinyl Plank) the next biggest portion of sales comes from tile, wall tile and accessories.

LVP has become very popular in recent years because it has the look of luxury wood but with all the benefits of vinyl such as its being waterproof, affordable, scratch resistant, impact resistant and it’s also easy to install so your labor costs will be lower than having a contractor lay tile or actual wood flooring.

Flooring and tile are one of most important jobs in finish construction because they really tie the room together. For example when you walk into a kitchen or bathroom the first things you’ll likely notice are the flooring, the countertops and the tile backsplash behind the sink or stove.

I can say from personal experience that people (clients) stress more about these items than anything else during the entire building process. Unfortunately no one really cares whether the toilet drain was assembled and sealed property or whether the shower is correctly waterproofed, they just want to make sure the tile floor looks great. I cant blame them because it’s the most noticeable aspect of finish construction.

I say all this to make the point that this is a part of construction that demands a broad selection to accommodate different personal tastes and Floor and Decor has as provided that selection and it’s simply unmatched.

Its all part of their Strategy

Floor and Decor has a simple strategy, they have more selection at lower prices, which creates a gravitational pull when people are choosing where to shop for flooring, tile and accessories. Now, they have any kind of hard surface flooring or tile anyone could want, but they may not have every single specialty tool every contractor wants, but since they are basically the go to place for everything else, most contractors will just use their selection (which is always good anyways) because its easier than driving across town to the mom and pop tile store.

The average Floor and Decor retail store is 79,000 sq feet and its mostly dedicated to to flooring, tile and accessories. In comparison Home Depot’s retail stores are about 105,000 sq feet on average which must be divided into roughly 15 different categories.

Home Depot and Lowe’s have to be very intelligent about how they allocate floor space because they are trying to please many different customers, for example if they give too much floor space to lumber or flooring they would diminish their value proposition for customers in more profitable categories like appliances or electrical.

Floor and Decor on the other hand isn’t trying to please 15-20 different categories of customers, they’re targeting just one so in order to retain their value proposition they simply need to follow trends within their niche and allocate floor space accordingly.

They also have a direct sourcing model which allows them to offer every day low prices which are difficult to compete with. Most of the products we use are cheaper at Floor and Decor compared to other places but even if they have a few products that are more expensive we still shop there simply because they’re a convenient one stop shop.

Growth

Looking at their growth strategy in their annual report it’s clear they’re navigating the same path as Home Depot. They understand the key things that have contributed to Home Depot’s success which is not surprise because the CEO worked for Home Depot for most of his life. Here is their strategy.

Open Warehouse-Format Stores in New and Existing Markets

Increase Comparable Store Sales

Expand Our “Connected Customer” Experience (online experience)

Continue to Invest in the Pro Customer

Continue to Invest in Design Services

Expand Our Sales Growth in Commercial Flooring

Enhance Margins Through Increased Operating Leverage

Store count and online presence

Right now Floor and Decor needs to focus on opening as many locations as possible with similar unit economics, which we will get to later. I also want to see them continue to invest in their online experience and pro customers. This is of utmost importance in this phase of company lifecycle.

A note on comparable store sales.

In the most recent quarterly report their comparable store sales declined 6% and revenue came in at just 4%. This is typical for retailers in the home improvement sector during period where interest rates are rising.

I’m expecting this slowdown to last for the remainder of the year and possibly into mid next year. Construction has slowed down a bit, especially the remodel and renovation industry. As interest rates have increased people have become more reluctant to borrow against their homes and remodel.

Pro services

I cant express enough how important it is for them to build the loyalty of pro customers. Home Depot has done a magnificent job of retaining pro customers though different referral programs and pro services, which has afforded Home Depot continued growth despite store count being flat the last decade. Pro customers are only 10% of Home Depot customers and yet they make up 50% of their sales. Floor and Decor generates 40% of their revenue from pro-customers currently and I expect this to grow. Pro’s are big ticket spenders and repeat customers so its makes sense for them to build pro loyalty. Home Depot has done this in some amazing ways which I will describe in detail in upcoming letter.

This needs to be one of the priorities for Floor and Decor if they want to continue growing after they finish building their store count to 500 locations.

Commercial opportunity

Commercial construction is made up of commercial building such as apartments, office buildings, industrial spaces, hotels, schools, hospitals, convention centers and so forth. The commercial hard surface flooring and tile market is estimated to be about $16 billion and they are targeting this group which is slightly different that the home building and renovation target market.

Let me explain

In construction sometimes different people make the decisions when choosing products like flooring and tile. Sometimes the builder, developer or owner to chooses the products which is most common in residential construction. This is basically where the owner or contractor selects products according to the owners specific taste. Floor and Decor has historically focused their sales efforts in this area on contractors and owners.

Another way selection is done, which is a bit more common in commercial projects, is where an architectural or design firm chooses the products for the according to some color or design scheme. Floor and decor estimates this accounts for 60% of the total market.

With their acquisition of Spartan surfaces they’re attempting to serve this part of the market by catering to architects and design firms who specialize in large scale projects. This could prove to be and important avenue for future growth for them.

In some ways this move is strategically similar to Home Depot’s venture into the commercial MRO market with their acquisition of Interline Brands and HD Supply. In both circumstances they are catering to a larger scale pro customer that’s more involved in the commercial construction industry.

The operating leverage/ ROA ROIC phase

Eventually Floor and Decor will slow down new store investments and focus on squeezing more productivity and profit without increasing their fixed assets and infrastructure. Home depot is the perfect example of this, they have done a great job of increasing sales/earnings without increasing stores, mostly through pro loyalty. This is a period when they should ideally see higher returns on capital.

Floor and Decor’s goal is to open 500 US stores which they claim will be achieved within the next 8 years or so. After they have reached this goal I assume they will either begin acquiring other competitors, paying a dividend and repurchasing shares.

I think there is a significant opportunity for Floor and Decor to return cash to shareholders through dividends and buybacks if thy choose to do so.

Management and company culture

Floor and Decor’s CEO spent the majority of his life working for Home Depot and worked his way up to Executive vice president of operations, marketing and merchandising. He’s had enough time to digest the successes, strategies and blunders of Home Depot along the way. I’m confident he knows what it takes to run a successful home improvement retailer.

They also mentioned that 70% of store senior management positions were from internal promotions which is always good to see because it shows that the company culture is good and people are willing to stick around and build their careers at Floor and Decor.

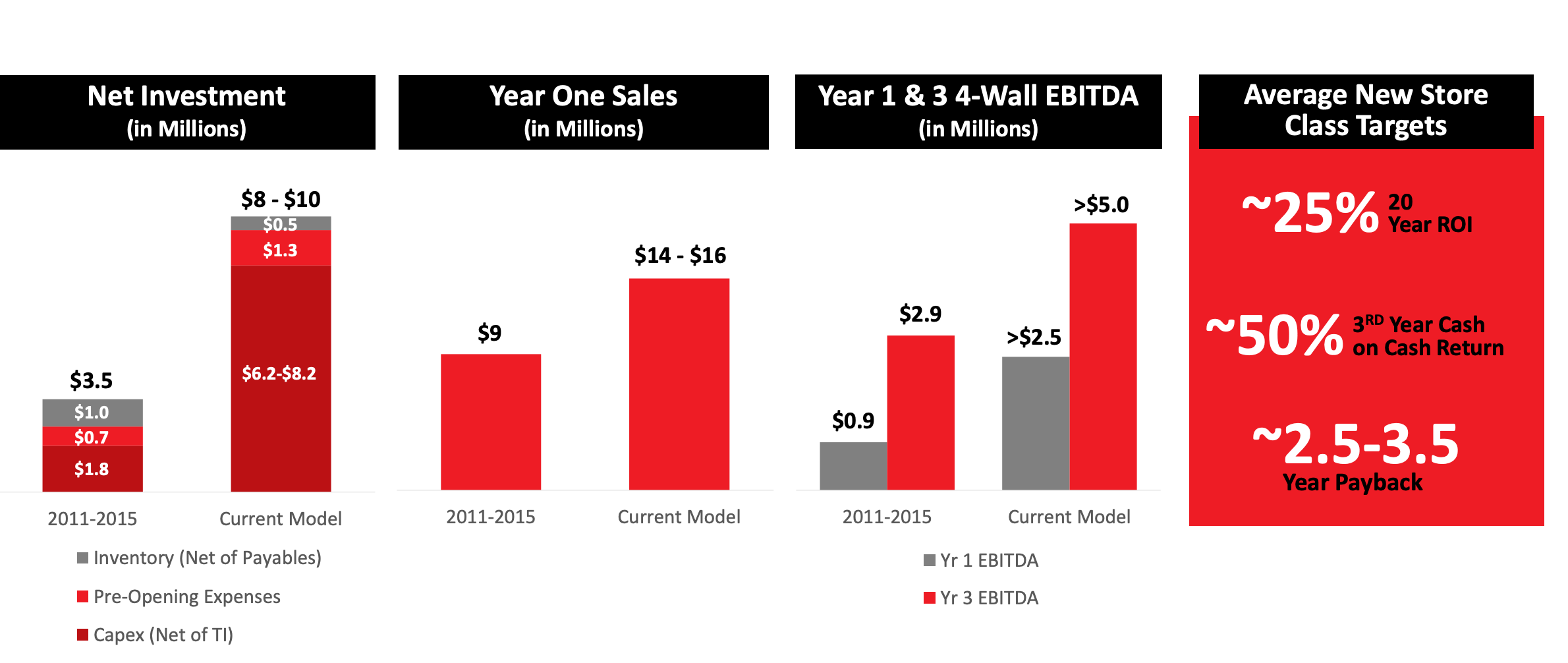

Unit economics

Floor and Decor has great unit economics. Below is a break down of their store economics relative to the upfront investment. In their investor presentation they say they can earn a 25% (EBITDA) cash on cash return on an 8-10 million dollar cash outlay for each new store.

My model (below) is similar but it includes the total revenue and earnings which includes a very small amount of revenue (probably less than 1%) from spartan surfaces and assumes a $10 million initial cash outlay to be conservative. But it basically validates what management is claiming in their investor presentation.

They currently average about $21.67 million in sales per store, $12.49 million in cost of sales per store, $6.36 million in SG&A expenses per store and $1.96 million in operating income per store which is roughly a 20% EBIT return. It also shows a 27% EBITDA return which is pretty close to the model they laid out in their investor presentation.

I don’t personally like EBITDA because it’s a bit too far up the income statement for me, although in this case I guess it’s alright because they’re just attempting to show the economics of the business.

They believe they can increase margins over time which gets me a little excited but I’m not going give them credit until I see it.

Risks

I think the biggest risks are probably macro related, flooring is not an industry that thrives in tough macro environments, some areas of construction are more recession proof and flooring and tile just aren’t one of them because it’s so dependent on discretionary spending.

Another risk is if they simply don’t execute on their plan to grow their store count to 500 as fast as they said they would. For a company trading at roughly 35x earnings I think they could easily get repriced down to 25x if same store sales continue to slide and they don’t execute on growing their stores as fast as they said they would.

A very important risk they did not mention

They did not mention competition in their business risk section which is very important. This means that they don’t believe Home Depot, Lowe’s, Dal tile and The Tile Shop are great risks to them. I absolutely agree with this and personally think it’s the other way around, Floor and Decor poses a big risk to other retailers especially small mom and pop shops as well as companies like Dal Tile and The Tile Shop.

Valuation

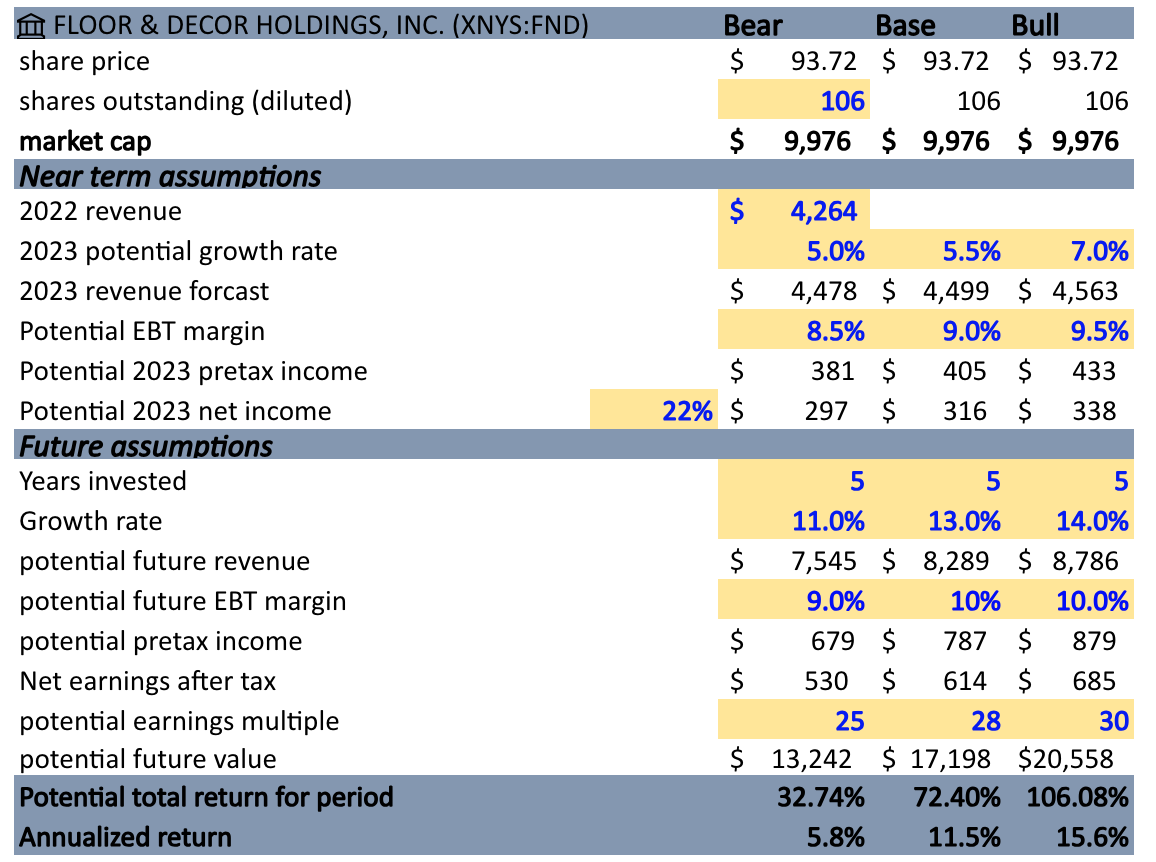

I expect FND 0.00%↑ to continue to grow nicely over the next decade, although I think the next year or two may be slow enough to put a damper on the average growth rate over the next 5 years. Im assuming growth rates between 11-14% plus a possible multiple contraction to possibly 25-30x. These are conservative estimates.

I love this company and think its has a bright future but I want a bigger bargain. It getting closer but its not quite in my sweet spot. If FND 0.00%↑ were to fall back into the $80 range or if they dramatically surprise to the upside for a few quarters I would consider adding to my position.

Now, if the stock goes back down into the 65-70$ range I’ll probably increase my position considerably. This would give a high probability of a double or triple over the next 5 years.

Thanks for reading!