Over Concentration In Your Portfolio Tends To End Very Badly

Over Concentration In Your Portfolio Tends To End Very Badly

You’re Probably Over Concentrated Right Now!

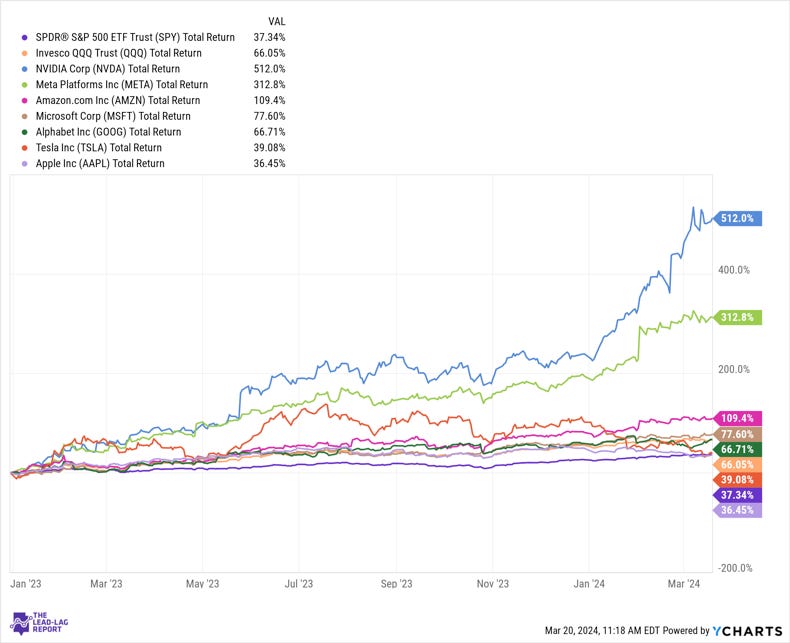

I probably don’t need to tell you that much of the U.S. equity market’s return since the beginning of 2023 have been driven by just a handful of stocks - the “magnificent 7” as they’ve come to be known. While these stocks have had their moments of weakness, their path of returns has mostly been higher and higher.

The humorous thing about this chart is how well even the “poor” performers have done. Of all the magnificent 7 stocks, Apple has had one of the more relatively unremarkable runs over the past 15 months. It’s still up 36% over that time, essentially matching the return of the S&P 500. Tesla is down more than 40% from its 2023 high, yet is still up nearly 40% over the entire measurement period. Yes, NVIDIA and Facebook have been the clear drivers of tech’s huge run, but there’s strength across the board here.

If you’ve been heavily invested in this group over the past year, congratulations! You’ve probably enjoyed some pretty hefty returns! However, if you’re banking on these types of returns continuing, you should probably adjust your expectations now. In fact, it’s probably a good time to reassess your portfolio allocation altogether. The more these stocks go up in value, the more concentrated and top-heavy the major indices become. The concentration is fine on the way up, but it’s likely to be painful on the way down.

How concentrated are we talking about? Here’s the latest top 10 holdings for the S&P 500.

About 32% of the S&P 500 is concentrated in the top 10. Of that, 28% is invested in the combination of the magnificent 7 stocks (Tesla is just outside the top 10 with a 1% allocation).

The concentration in the Nasdaq 100 is even worse.

40% of this index is still concentrated in the magnificent 7 stocks. I say “still” because in July of last year, the Nasdaq initiated a special rebalance of the index just to address the overconcentration issue. Prior to this, the 7 biggest issuers accounted for 56% of the index with Microsoft accounting for more than 12% itself. The one-off rebalance helped improve the situation, but with the mag 7 still accounting for $2 of every $5 invested in QQQ, it’s still a problem.

Investors, for their part, haven’t cared. As far as they’re concerned, tech is the only game in town.

Looking at just sector funds, investors are plowing all of their money into tech and virtually nothing else. If you want to take this a step further, nearly 70% of ETF flows over the past year have gone into equity funds. Among U.S. equity ETFs, more than 85% of flows have gone into large-caps (the S&P 500 funds, obviously, accounting for most of that). Growth has outdrawn value by a 15-to-1 margin.

Investors have only been interested in mega-cap growth & tech and that’s been the case for a long time.

That creates a big overconcentration problem. Investors are very overweight in this category and are exposing themselves to significant downside risk should conditions change. Everybody thought the same during the tech bubble 20+ years ago too. The internet was going to change everything, so investors bought up every tech and internet stock they could find regardless of valuation or business viability. Looking at you pets.com! The internet was indeed revolutionary, but the tech bubble burst regardless. We could be heading for a similar fate today, the only difference being that AI takes the place of the internet as the major catalyst.

How big is the concentration problem? It’s created a market that we haven’t seen in 100 years!

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.