Why GBP, JGBs, and Yen Remain Shortable

Why GBP, JGBs, and Yen Remain Shortable

Unpacking Macro Headwinds, Technical Alignments, and Factors Behind Three Macro Positions

Hey crew,

I meant to send out this report to you all yesterday, but I was under the weather trying to recover; thanks for your patience.

In this report, I’ll outline a balanced perspective on why my outlook for cable, JGBs and the Yen remains short. As always, it is an actionable piece with a balanced set of perspectives both for and against the trades.

“strong opinions, weakly held”

Sterling Shorts

Positioning: Underweight

Since the start of the year, I’ve been vocal about my bearish outlook on cable. The pound has stood out as a currency with great downside potential, aligned with the macro data and it becomes ever more clear as to why one would be bearish on the pound.

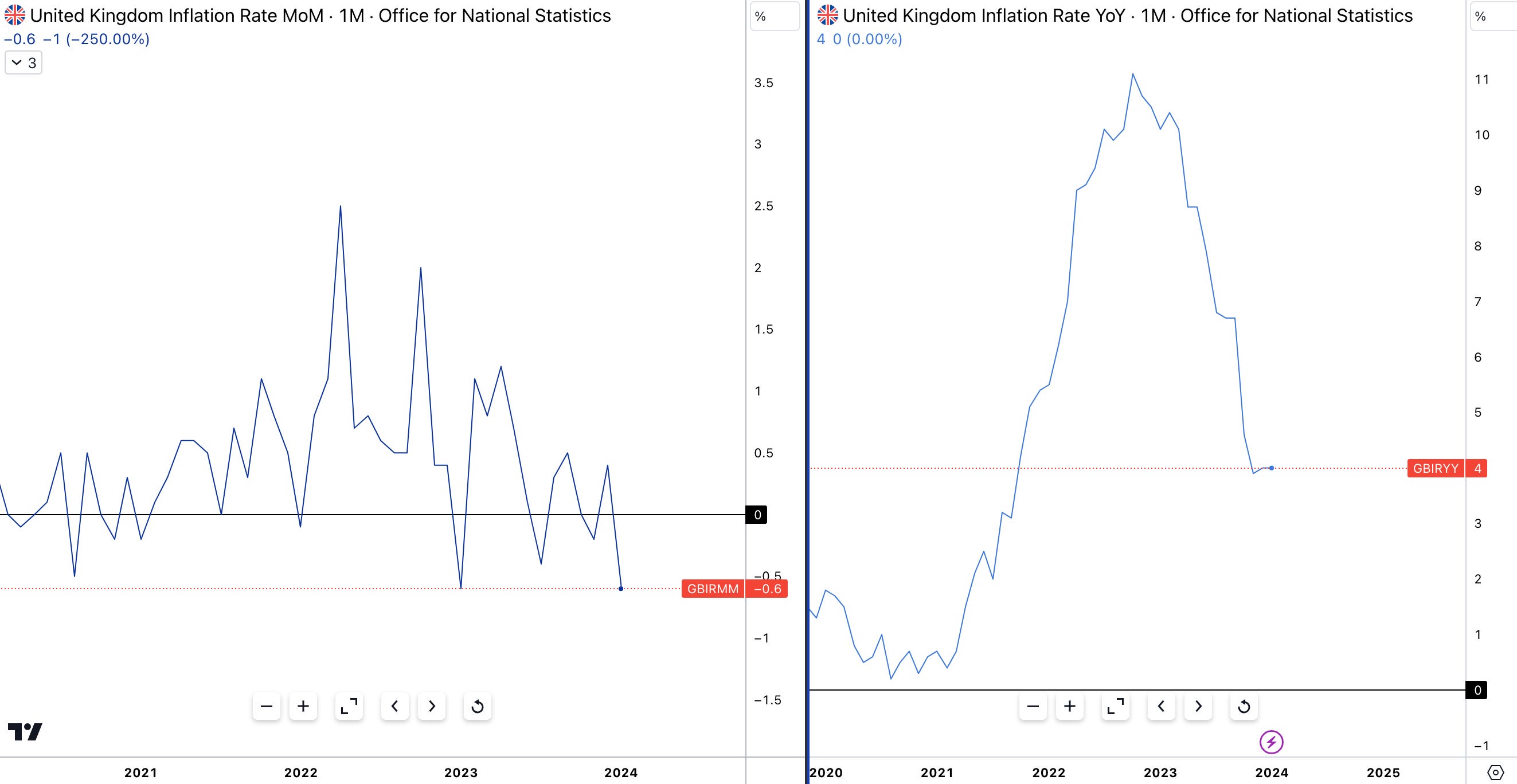

This week we received a significant set of data coming from the UK economy further confirming my positioning. Inflation in the UK remains stagnant, which toughens the situation for the BOE as GDP data disappointed to the downside confirming the UK is in a technical recession. Headline CPI was forecasted to rise to 4.1% but held steady at 4.0%, whilst the MoM reading showed a 0.6% contraction.

Core CPI remains fixed at 5.1% demonstrating the challenges the BOE faces with bringing down the services component of inflation. Unlike the rest of the economy the labour market has continued to bolster positive data with the unemployment rate declining to 3.8% and average hourly earnings + bonus increased 5.8% in December.

To anticipate future trends, we must examine leading indicators. In this case, the Producer Price Index (PPI) serves as a valuable tool to gauge potential downstream impacts on consumer inflation. While current data suggests a continued downward trend for headline inflation in the UK, potential headwinds are present. The ongoing evaluation of the Israel-Hamas conflict's economic repercussions and elevated transportation costs due to diverted naval routes remain risk factors for European energy markets. Nevertheless, it's important to note that year-end data for January 2024 revealed significant declines in gas (-26.5%), oil (-9.2%), and electricity (-13%) prices, indicating an overall bearish trajectory for energy costs.

Data released from the ONS on the 15th of February confirmed the UK slipped into a recession with GDP contracting 0.3% in Q4, YoY for Q4 GDP contracted 0.2%. The high cost of living, coupled with crippling inflation has kept the UK economy stagnating over the past 12 months.

So what does this mean for sterling?

As always it’s important to bring back each data point to the question of “Where is opportunity?”. With the UK officially in a recession, and the U.S bolstering in strength and growth shown by their latest Q4 QoQ GDP figure of 3.3%, the pound is on a perfect stage to see prolonged weakness which I believe can last right up until the general elections here in the UK.

The transmission of monetary policy on FX is very simple. The framework to understand, interpret and come to an investment conclusion must be clear.

Let’s review the factors influencing my short bias: