A Dollar Smirk

A Dollar Smirk

The market likes to hate on the USD, but a cyclical bottom is forming. A rethink on long-run policy lays the groundwork for calendar spreads to drive equity dynamics again, and the USD as a vol hedge.

The Macro Rant is a weekly newsletter on global macro with multi-asset perspectives.

The Quick Read

Euro has cyclically topped. Beware the 200-day moving average; a break is needed to take out the sequence of higher lows in EURUSD. It would signal a sell the rally stance.

Cyclical impulses that support euro performance have lost momentum while the US looks primed to benefit. EURUSD can easily find itself sub-1.05 by year-end.

The USD smile is back in force; China and the Eurozone are on the wrong side of it.

The USD can benefit on a late cycle reboot. But that eventually leads to a back-up in 10y yields and a SOFR curve to price in higher for longer before it becomes self-limiting.

That puts episodic equity vol back in play. This is because real yield and calendar spreads correlations with the equity market have strengthened. This increases the appeal of the USD as a vol hedge.

A Jackson Hole Symposium can lay the foundation to pressure SOFR calendar spreads beyond M4 to become less negative over the balance of this year.

Why so serious?

Nothing is certain except death and taxes…and perma-euro optimism. Almost without fail, every year consensus forecasts a stable or stronger EURUSD. Even at the cyclical tops. Once in a while, perma-euro optimism works out because even a broken clock is right twice a day.

Getting the euro call right hinges on whether you can call the macro cycle. Easy right? This is because the euro is a pro-cyclical currency. Suffice to say, those cyclical supports are hanging on by a thread.

There are many ways to capture this, but a deviation from trend basis (using the 200-day moving average) puts that cyclicality on fine display. When the Fed downshifted policy and China relaxed its zero-COVID policy late last year, the euro experienced a multi-standard deviation positioning squeeze and front-ran the rebound in the global PMI.

But it is hard to find a reason for staying long the euro or look for trend upside when domestic cyclical supports have lost momentum.

The current backdrop is effectively the opposite of the setup late last year when markets celebrated China’s COVID zero-to-hero. It’s now back to zero as it turns out that burst of activity was short-lived and structural problems in China are rearing their ugly head.

In the US, it’s quite the opposite. In broad USD terms, the ISMs - preferably viewed as a ratio between services and manufacturing - is actually too weak. If the ratio collapsed, then the current level of the USD is justified. That would need to be services driven given the make-up of the US economy. That seems unlikely. And as foreign direct investment in China continues to dry up, manufacturing may start to play a larger more positive role. Arguably, ISM manufacturing - which is higher beta - is displaying signs of troughing. So, the ratio could collapse, but for good reasons.

If you’re thinking to yourself that this sounds like a USD smile framework, then you are correct. Made famous by Stephen Jen, it seems that the Eurozone and China are on the WRONG side of the smile and that the US is entering some lite-form of exceptionalism. Perhaps, more of a USD smirk.

Mark your calendars

Even if the Fed has made its last hike, the economy is still below its choke rate. That makes it harder to compel a recession. So the risk is that the market is making the wrong assumption again when it comes to 2024 pricing. There are some mechanical reasons for pricing to persist in the curve, the argument here is that it is on borrowed time. That is likely to get tested into the end of the year.

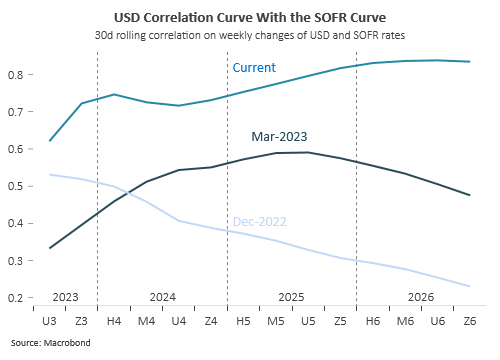

It also means that calendar spreads beyond M4 need to become less inverted. M4-Z4 is likely to be higher beta, but less inversion there will drive less inversion elsewhere (through M4-Z5). This will matter for the USD given that it is displaying much greater sensitivity strip pricing in the SOFR curve.

The nature of correlations is that they ebb and flow, and so will the USD’s correlation curve with SOFR. But, with the debate on structural shifts at this Jackson Hole Symposium and proclamations of higher for longer real rates, the correlation range may be stickier further out the curve…or until something breaks.

Missing the forest for the trees

USD bears have sort of made their mark that weakness will come in the form of the Fed cutting rates. Empirically, the results are mixed. It’s a relative game. What you tend to see first is that risk assets plummet and the dollar’s vol hedge becomes desirable. Once forceful policy reflation kicks in, then risk premiums ease and the market is happy to sell dollars.

Markets can be myopic. With so much focus on when the Fed will cut, it is easy to lose sight that others are already doing so already.

Back in December 2022, when the Fed downshifted on hikes, it handed off policy leadership to others; the ECB turned up the heat and the BOJ changed YCC. Now, European PMIs are trying to find a bottom, China has lost momentum, and the BOJ doubled the YCC target yet the bond market shrugged. It’s no wonder that German bunds have outperformed Treasuries this summer (and it is unlikely to change).

As noted above, most regional markets are on the wrong side of the dollar smile. STIR markets seem to have an appreciation for this, with variability in curve pricing more US centric than in other curves.

More warning signs

This comes at an interesting milestone for the US dollar, which has breached the 200-day moving average. Typically, such a breach marks an inflection point in the trend though it takes a convincing turn in the 200-day itself (after breach) to solidify the trend.

Tactically, one could make an argument that some USD pullback is overdue given recent firmness this summer. But, this is more of a buying opportunity than it is a sign to double down on dollar shorts.

We argued last week that equities can still stay lofty as it enjoys a late cycle boost in the US. The AI craze is not over, and that will probably drive foreign capital flow into the US (supporting the US dollar…), as we last saw during the DotCom boom (before it went bust).

But, the equity market will be prone to episodic vol spikes over the balance of the year. The 10y real bond yield and the US equity market spent Q2 going their separate ways, but are now inseparable again as duration views come into question.

This means that the USD is likely to renew its vol hedge properties…

…as several currencies are now vulnerable to Fed cycle pricing and higher bond yields...

…and EURUSD may not be able to resist the pull of destiny from rate spreads.

…threatening the sequence of higher lows.

So which spreads matter for the equity market? Take your pick. Turns out SOFR calendar spreads in the red and green strips are very negatively correlated with an equal weighted S&P 500 (almost as much as they were over the last 12 months when the Fed was racing to hike). If one is to embrace higher for longer, then risk looks more vulnerable now than it did in Q2.

Putting it more plainly, the time is coming to curve your enthusiasm on broad risk allocations. Upside in risk assets is as good for as long as the Fed allows it.

Good luck.