Guide to the LNG market + Serica's Tailwind acquisition

Guide to the LNG market + Serica's Tailwind acquisition

MORAM - 3rd September 2023

Hi there,

Today is a very special publication as we are sharing our "Guide to the LNG industry" which, along with the publication of "The natural gas market explained" released in May, we believe provides a fairly comprehensive explanation of the industry for any investor interested in natural gas. Additionally, we are sharing the Excel file containing all the information used for the analysis.

In the same way, and thanks to DanielCastrille , a contributor we greatly admire, we are sharing the analysis of Serica's latest acquisition (Tailwind) in the North Sea and the company's prospects - without paywall

As we have mentioned many times, we will always provide some free content, but if you want to support our project, in addition to the Excel file with all the information about the LNG industry, you will also have access to all our analyses and articles, an education section, monthly Q&As with the team, portfolio management, theses / analyses suggested by our users, and much more!

Investment Theses in small caps:

Some of our recent analyses: Unidata, Arcos Dorados, New Fortress Energy, Twin Vee, Sanlorenzo, Catana Group, Intred...

Macroeconomics:

Discussion of current topics and their implications/actionable related ideas (e.g., BRICS vs G7 and effects on emerging markets)

Analysis of the functioning of specific sectors (As today’s article)

Education:

During the next 4 months, we will be focused on valuations (Our idea is to replicate the process followed by an institutional) and the debt side - Types of debt, differences, things to look at when analysing a company…all from a practical standpoint & examples

Serica Energy - Post Deal situation: A potential opportunity in the North Sea

Today, we want to talk about a well-known UK company in the natural gas sector, Serica Energy. Serica produces 5% of the gas in the United Kingdom, has a market capitalization of £920 million, and is listed on AIM London under the ticker symbol SQZ:LON.

We already conducted an analysis at the beginning of last summer about Serica. However, the main reason we are bringing this analysis is because Serica has undergone a radical transformation in this period due to the merger with Tailwind, resulting in a change in its capital structure as well as its production, which has increased from 25k to 45k with prospects for further growth.

First, we will discuss the situation of Serica prior to the deal, the context of the merger, the assets of Tailwind, and how the resulting company stands.

Serica Pre-deal

The company before the merger was a company that produced around 25 kboed, primarily of gas (approximately 80% of its total production), and had 2P reserves in 2022 of 74.9 MBoe, which they managed to increase compared to the 62.2 Mboe reported in 2021.

Serica SQZ:LON consisted of 5 main assets, 3 in the area known as BRK (Bruce, Keith, and Rhum) that produce from the same platform and are operated by Serica (70 Mboe net reserves) and 2 minot ones outside this area (Erskine and Columbus).

Among the 3 main assets, Rhum (WI 50%) is the main one. It is a mature field that maintains good production figures after the start of a well that was abandoned in the primary development of the asset but was successfully recovered for production at the beginning of 2021. It has a fairly stable production of about 15.5 kboe/d net for Serica.

Bruce (WI 98%) is a very mature asset in its final years of production, but after minor work carried out in 2022, production was maintained without decline during the year (about 5 Kboed), and its 2P reserves improved. Furthermore, more similar work is scheduled for this year. - last year Capex was £16MM -

Keith (WI 100%) is also a very mature asset that has not been producing for a few years. A plan has been devised to rectify an electrical fault that halted production in 2020; it was barely producing an average of 1 kboed in 2019.

Outside the BRK area, the company has a stake in Erskine (WI 18%), an asset operated by Ithaca that has extended its life beyond expectations for several years. It produces about 1.7 kboed net and maintains its reserves compared to 2021 at 3.4 Mboe net for Serica.

The last asset is Columbus (WI 75%), a field brought into production at the end of 2021 that has performed worse than expected. In 2022, it produced 1.9 kboed net for Serica with a significant decline. There has been a substantial reduction in its reserves, leaving them at 1.1 Mboe net mainly due to two factors: the large decline and the planned closure of the facility to which the asset's production is sent, expected in 2026.

In addition to these assets, the company holds several exploration licences, with no clear vision at present of whether they will be able to expand the company's reserves.

Merger context

Last year was an extraordinary year for the gas sector due to the Ukraine war and the destruction of the 2 pipelines that connected Russia and Europe. Europe, in particular, the northern countries, was excessively dependent on cheap gas from Russia. They had not done their homework in terms of having sufficient regasification capacity to replace that gas, and it was necessary to fill all inventories to try to reduce the potential shortage problem that could occur in winter. To assist in this endeavor, mandatory consumption reductions were decreed for both individuals and companies. The price of gas skyrocketed due to this situation, leading producing countries to raise taxes radically and confiscatorily (up to 75% in the case of the UK). After that, an unusually mild winter arrived, causing prices to decrease to current levels of between €25-35/Mwh, prices that we believe are sustainable from now on due to the need to permanently incorporate LNG into the European supply mix.

Amidst this situation, there was a very attractive merger offer from the shareholder's perspective by Kistos PLC (we commented about it last summer after talking to Serica’s CEO) This offer was rejected by management as they considered it insufficient, which in turn prompted an offer to purchase Kistos, which was also rejected for the same reason.

A few months later, the offer for the operation we are discussing became known. Tailwind approached Serica to propose a merger. Initially, the operation was not well-received from the perspective of many investors, due to the very negative comparison with the previous offer received from Kistos and the volatile gas situation. The conditions were clearly much less economically favourable for Serica than those offered by Kistos. £58.7 million was paid in cash, £277 million in debt, and 111 million shares were issued at an average price of £2.85/sh. Additionally, the company came with a very poor hedge of 11,000 bbl/d of its oil production during 2023 at $61/bbl and an average of 4,000 bbl/d at $75/bbl during 2024. The allocation of capital was far from ideal; the lack of a reference shareholder meant that the management did not bother to seek the best conditions given the circumstances. But the deal made sense in other respects. It shifted the company's production profile to one that was almost balanced between oil and gas, making it less dependent on gas price fluctuations. Furthermore, it brought with it tax advantages (tax losses of £1400 million) that amount to around £470 million of FCF in the coming years, and if used wisely, they will help mitigate the impact of taxes on Serica's income statements, as is expected for most companies in the UK.

Tailwind Assets

The assets that Tailwind contributed to the deal are primarily oil producers, and their 2P reserves stood at 55.5 Mboe at the beginning of 2023. The main assets are in a hub called Triton, including the FPSO responsible for production, of which a 46.4% WI is controlled. The fields in this hub are Gannet E, Bittern, Evelyn, and Guillemot W/NW.

Gannet E (WI 100%) is a mature asset that has been in production since 1998. During this year, an infill drilling campaign was carried out in one of its wells, resulting in the asset producing an average of around 10 kboed since its completion in February.

Guillemot W/NW (WI 10%) is an asset of which a small portion is owned. It only produces about 250 boed net for the company.

Bittern (WI 64.6%) is a very similar asset to Gannet E. It was commissioned in the year 2000 alongside Guillemot W/NW. A very successful work campaign was carried out in 2019, leading to its current production of around 6 kboed net for Serica.

The company's latest asset in this hub is Evelyn. The first phase of this asset started production in September of last year and has been having quite solid production of around 4.5 kboed. It appears that the decision to continue developing the second phase will be made.

There is also an asset in its final exploration phases, Belinda. The project for the future development of this asset is currently being finalized and is expected to be presented in the coming months.

In addition to this hub, Tailwind also contributes a 25% WI in the Columbus field and 100% of Orlando, which is performing similarly to Columbus in terms of decline. It currently produces about 3.6 kboed.

Lastly, there is the Mansell field, an asset that was already in production but was decided to be decommissioned after three years. Its redevelopment is currently being planned, and it is estimated to have 2C reserves of at least 16 Mboe.

Post-merger situation

Finally, after accepting the merger, the situation is that Mercuria, the majority shareholder of Tailwind, has gained control of Serica with a 25.2% stake in the company. This can be positive for better capital management than what has been done so far. Several members of Mercuria have joined the board, including their CFO. The company is also working to reorganize internally so that the tax losses can be applied to all of the company's assets from 2024 onwards, not just those coming from Tailwind.

Regarding the financial situation, if we go back to January, we find a company with a net debt of around £10 million GBP, taking into account its Working Capital. Additionally, we estimate that it has ARO (Asset Retirement Obligations) between £150 million and £180 million net of taxes approximately, but these obligations would extend over a long period. They are not expected to be paid off before 2035. Extraction costs have remained very similar to what they were, around $17 per barrel of oil equivalent (boe).

Serica has become a company that, in this market environment, can stand out from the rest of the small and medium-sized companies that have their assets primarily in the UK. Without intending this to be an valuation of the company, considering an average production of 45,000 barrels of oil equivalent per day (boed) and oil prices of $75 per barrel in 2023, $70 per barrel in 2024 and 2025, and gas prices around €40 per MWh in 2023, and €35 per MWh throughout 2024 and 2025, a Free Cash Flow (FCF) Yield of 30% would be obtained for each of these three years with the current share price of 2.40 GBP/share.

Furthermore, the company's upcoming organic investment plans are quite ambitious. In the assets of the BRK hub, there are plans to make slight improvement interventions in Bruce and Keith during the years 2023 and 2024, to ensure that these fields at least do not reduce their production in the next 2 years. Further ahead, several targets are being evaluated for infill drilling in Bruce. In the Triton Hub, there are scheduled slight interventions in Guillemot, as well as an infill drilling well. Three more wells are planned for 2024. In Gannet E, a sidetrack similar to the one carried out last year is planned, as well as one for Bittern. Towards the end of the year, the development of Phase 2 of Evelyn is scheduled, and during the year, the FID (Final Investment Decision) for Belinda may be presented.

Potential near term catalyst derived from the merger include:

- A change in the corporate structure that will place all of the company's assets under the umbrella of Tailwind's tax losses. The company is already working on this, and it is expected to be completed before 2024.

- Acquiring assets outside of the UK, in jurisdictions that are more tax-friendly. Mercuria's entry into the company and their experience in such deals will aid in this.

- Improving shareholder returns, primarily through dividends. If suitable assets for acquisition are not found, the company is open to share buybacks.

- Possible improvements in taxes in the UK. The governing party is shifting its stance towards the country's energy security and a domestic O&G sector with much lower emissions than in the past. This cannot be sustained with the current tax system, which drives companies away since it barely allows for profit, and companies continue to bear all the risk of the initial investment. The UK might move towards a system similar to Norway's, with high taxation but a shared risk from the start of the investment, or the Dutch system, which is much more flexible regarding high taxation, as it only applies to gas and is based on the excess of the selling price above a specified value and above commodity futures.

Disclaimer: This article does not intend to be an investment thesis for Serica but simply an analysis of the company's post-merger situation with Tailwind. It should also be noted that the primary author of the analysis holds a position in the company and may have a positive bias towards it.

Guide to the LNG Market

As we've discussed on numerous occasions in recent years, natural gas is expected to be one of the fastest-growing energy sources in the next 20 years, second only to renewables. This is due to its lower emissions compared to traditional fossil fuels (coal and oil) and its greater stability compared to renewables. Until not too many years ago, the natural gas market was not global but rather localised due to a lack of infrastructure to transport natural gas from one part of the world to another (When it is transported by ship and not through pipelines, it has to be liquefied, transported in the form of LNG and regasified).

However, this industry has seen significant development in the last two decades, driven by events such as the shale gas boom in the United States, China's rapid growth (also emerging Asia), and disasters like the Fukushima nuclear incident in Japan. In this context, liquefied natural gas (LNG) has played a pivotal role, with its volume quadrupling in the last 20 years - basics like arbitrage concept etc are explained in the mentioned “The natural gas market explained” published in May -.

In this article, we aim to explain how this industry works, providing all the details of the three involved components: demand, supply, and transportation. We analyze the demand from the 53 countries that have regasification plants, providing details of all the regasification plants that have been built and those planned, including portable FRSUs, storage capacity of major countries, and discussing the key companies in this part of the chain. We do the same for the export side, where, in addition to countries, we also show all operating and planned FLNG projects. Similarly, we have all operating LNGCs in the spreadsheet and data on those under construction until 2028. Finally, we discuss the current situation, what is expected in the short and medium term, and our point of view regarding portfolio management.

To achieve this, we have built a comprehensive database that includes the names, owners, and characteristics of all 734 LNG vessels (including the 49 FRSUs), all existing and planned liquefaction plants worldwide, regasification facilities, FLNG projects, and data on all countries involved in the industry. We've compiled all this information into an Excel file, which is available - via our website - to all our premium subscribers.

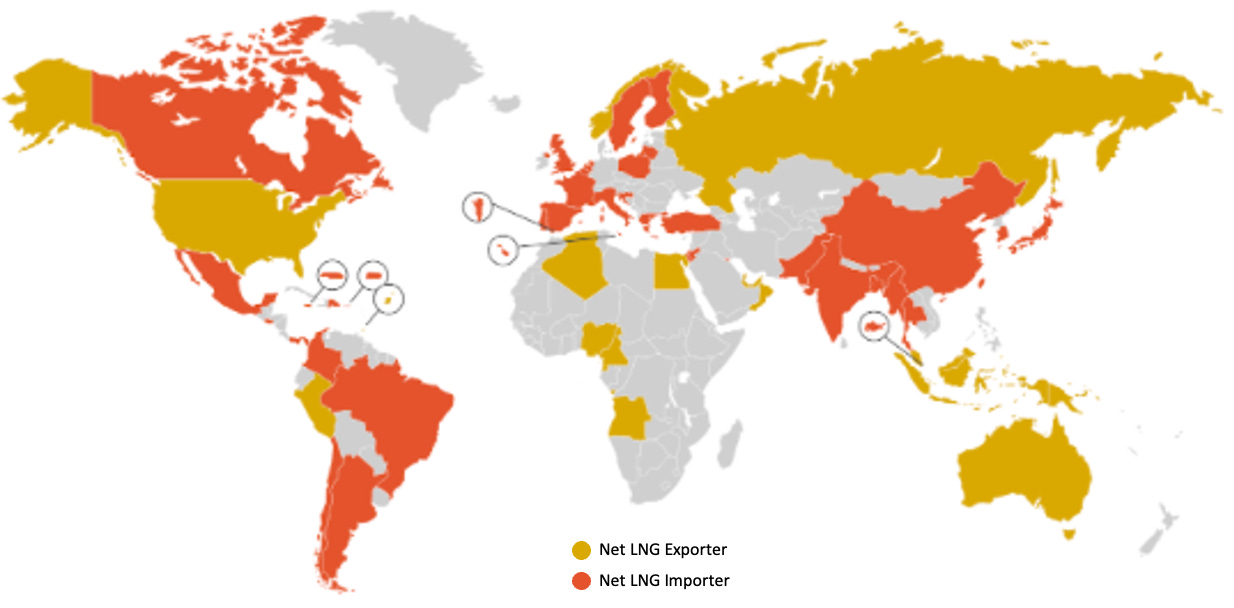

Demand / Imports

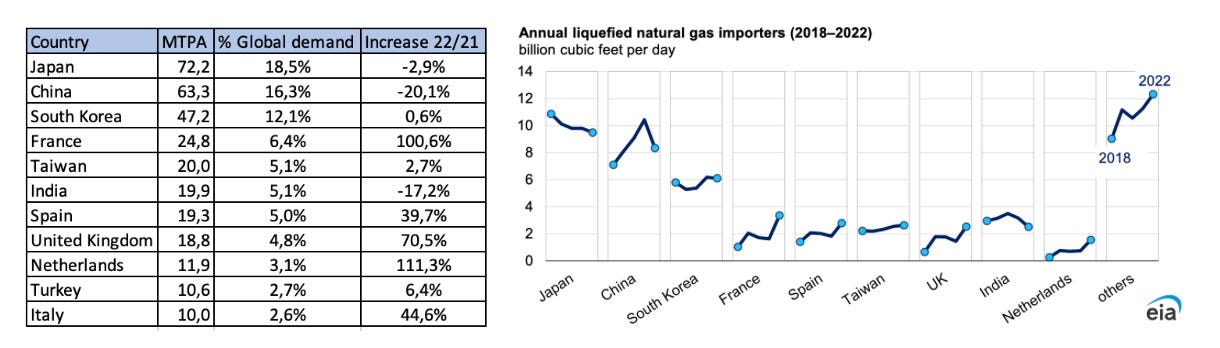

The demand for LNG has experienced significant growth in the last 20 years, going from barely 10 billion cubic feet per day (Bcf/d) in 2000 to 50 Bcf/d today. During this period, the primary driver of this growth has been Asia, driven by the expansion of China and other emerging markets. As of today, Asia accounts for 65% of LNG demand, although it has lost some market share in the past year due to China's slow reopening and increased LNG imports in Europe as a result of the conflict in Ukraine. The main contributors to this demand are Japan, South Korea, and China. However, India (which is experiencing tremendous growth in the number of LNG terminals) and Taiwan are also notable consumers, each representing approximately 5% of global consumption.

In Europe, due to the conflict in Ukraine and sanctions against Russia, the region now accounts for slightly over 30% of global demand. France, Spain, and the United Kingdom stand out, collectively representing 16% of global demand among the three of them.

Note: Different units

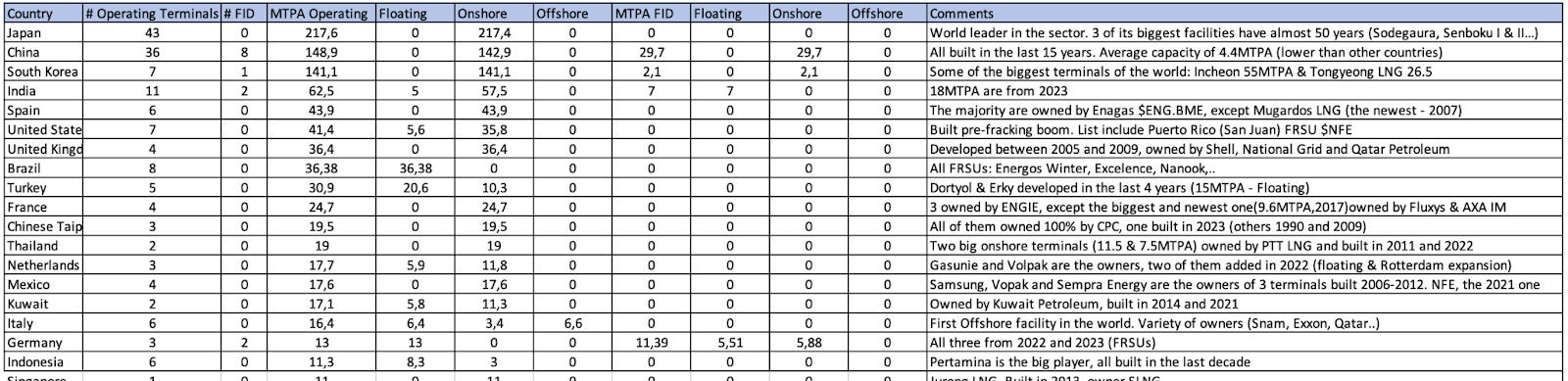

However, a significant difference among countries lies in their storage capacity, which is an important point to understand and consider. Japan, the largest LNG importer, does not have underground storage, and its capacity is limited to what is associated with its import facilities, specifically 12 billion cubic meters (bcm), enough to cover only about 36 days of average winter demand. This makes Japan an active player in the purchase of new cargoes (we discuss this further in the LNG Shipping section). South Korea faces a similar situation with storage capacity at 6.56 bcm. China's storage capacity is somewhat higher (and growing) at 19.8 bcm, but it still only covers 10% of its demand. It's also worth noting that India, despite its rapid growth in the LNG industry, has not yet developed strategic reserves.

In Europe, the situation varies significantly between the UK, which has storage capacity for approximately 3% of its demand (2.3 bcm), and the European Union, which, with 103 bcm, covers one-third of its winter demand.

In general, the impact of a colder-than-normal winter (due to limited storage) and the ongoing need for LNG supply can be observed.

Regarding regasification capacity (which is necessary to introduce the received LNG into the local network), Asia has capacity for 611 MTPA, Europe for 221.9 MTPA, the Americas for 216 MTPA, and the Middle East for 51 MTPA.

Out of this regasification capacity, 177.3 MTPA is provided by floating storage and regasification units (FSRUs). There are 49 FSRU vessels operated by 22 different companies, with Höegh ($HLNG.OL - acquired by Morgan Stanley), Excelerate Energy ($EE), and Energos Infrastructure (a joint venture between Apollo and New Fortress Energy $NFE) being the three most significant players in this space.