MORAM - Unidata investment thesis + Jadestone Proposed Financing

MORAM - Unidata investment thesis + Jadestone Proposed Financing

Moram - Sunday 11th June 2023

Hi there,

This week we are sharing two publications, a thesis on an Italian small cap that is growing a lot and we consider has a lot of potential and an analysis of Jadestone's situation after this week's proposed finance.

Unidata: an Italian telecommunication company whose principal service is providing broadband connectivity in Italy (lagging in deploying high-speed broadband connectivity to European peers and full of opportunity). Growing double digit and with presence in high-growing industries such as Cloud or IoT. Recurrent nature of the revenues, great margins of all the segments of the group, set several JV to expand itself, management owning 60% of its shares…

Jadestone: Analysis of Jadestone's recent financing proposal where we thoroughly analyze the proposed financing, the current situation of the company, the scenarios going forward for investors and opportunists, and our thoughts and actions regarding this event.

Best,

Moram team

(If you have any questions, feel free to reach out on info@moram.eu)

1) Unidata Investment thesis

Unidata - Investment thesis in a nutshell

We go back to Italy to discover another small cap opportunity growing at a high pace in a high-growing sector with significant tailwinds trading at good prices. Unidata is an Italian telecommunication company whose principal service is providing broadband connectivity to residents, businesses and public sector administration mainly in Rome and the surrounding Lazio region.

Compared to the rest of big European countries, Italy was (and still is) lagging in deploying high-speed broadband connectivity. With this scenario, Unidata has profited from this opportunity and has been one of the first-movers, building a proprietary infrastructure of more than 5,700 kilometres of fibre optic.

Apart from providing connectivity, Unidata competes in high-growing industries such as Cloud or IoT. We highlight the recurrent nature of the revenues and the great margins of all the segments of the group. Thanks to an aligned management holding more than 60% of shares, they are exploiting rising opportunities with an aggressive capital allocation, through Joint Ventures but also with an acquisition that will double Unidata’s top-line. This week, they have been included in the STAR segment, which will improve the liquidity and recognition of a company with low trading volume.

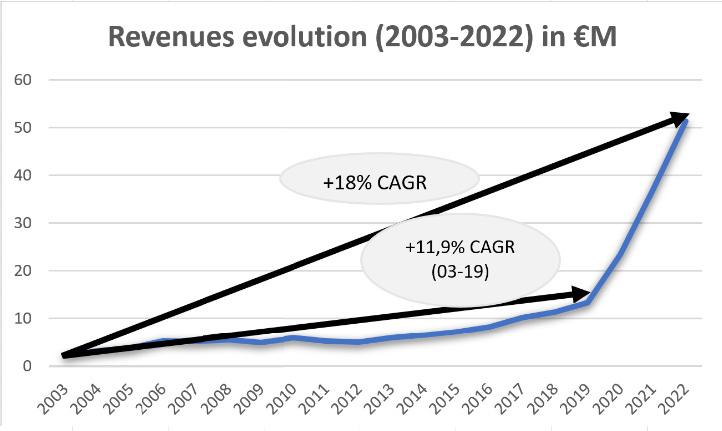

After 2019, the top-line growth has been an impressive 56% CAGR. This growth is partially explained by the measures to Covid to improve the broadband connection of the country that the Italian government and the EU have taken, accompanied by a growth in the quality demands of the customers.

But there is another part of this growth that we believe that can be maintained for the next years that is explained by the aggressiveness in the strategy. Since 2019, Unidata has gone public, has made an acquisition of 58 million, which is more than doubling the revenues it had in 2022, has opened new headquarters in Bari, has started several business lines and is undertaking three joint ventures with well recognized partners with investments that go up to €100 million.

With a market cap below €125 million, Unidata is trading at a significant discount compared to the traded peers. Our play in Unidata is for the long term. During these years they will continue to build the fibre network which is expensive to build and significantly decreases the margins, but once it is finished, the operating leverage will play by their side, being the operator it is easy to make even better margins while gaining scale.

Through the following pages, we analyse Unidata going through its history and business model, discussing the TWT acquisition with some comments about the management. We will see one by one the undertaken joint ventures as well as the markets where Unidata competes with a positioning relative to competitors. We will finish with a detailed PL model to get to a fair value of the stock and some conclusions of our thoughts of this company.

Short History and Business Model

Although Unidata has a long history (around 38 years in business), it has not been until recent years when the company has accelerated their operations, being the last two years very active on the development of new projects and undertaking also a transformative acquisition.

Unidata was founded in Rome in 1985 by three of the current main shareholders (Renato Brunetti, Marcello Vispi and Claudio Bianchi) with the initial objective of designing and manufacturing computers and servers. The company keeped with these activities for 14 years, when given the initial uprising of the internet, they changed to become an Internet Service Provider (ISP) in 1994.

Unidata was sold to a British group in 1999 and was acquired back in 2002, when it began building the proprietary fibre optic infrastructure and the Data Centre. At this point, Unidata was both an ISP and a telecommunications operator. In 2017, they expanded their business to IoT and Cloud. And signed an ambitious partnership agreement with OPen Fiber, a leading telecommunications operator for the development of fibre optic infrastructure.

In March 2020, Unidata launched their IPO, raising €5.7 million. In the recent years, the company has pushed hard to be one of the first movers in FTTH (Fibre To The Home), developing an extensive infrastructure in grey areas (markets with only one operator and where it is unlikely that another network will be installed. In Italy is common the governmental support to develop these areas), and launching a series of ambitious Joint Ventures.

Earlier this year Unidata bought TWT for €58 million, a telecom company that will enhance the recurrent nature of the revenues, the cash generation and that will expand the business from the Lazio region also to Northern Italy and will position the group with a more diversified customer base. To finance all these growth opportunities, Unidata raised over 15 million earlier this year at a share price of €42, (current valuation €40/share)

With a fibre-optic network of more than 5,700 km which is constantly expanding, and for which Unidata has already spent €60 million since 2018, a wireless network and a proprietary data centre, Unidata supplies very high-speed connectivity services using FTTH (Fibre to the Home) network architecture. Among other solutions, Unidata also offers VoIP, data centre and cloud services.

This fibre infrastructure has been built in the Lazio region (Rome’s region) reaching in 2022, 290,000 housing units. To give an advance of the expected growth of the company, they expected to hit 500,000 in 2025.

80% of the network used to bring Fibre-to-the-home (FTTH) is proprietary and the rest is used thanks to agreements with wholesale grantors, the so-called IRU agreements, which are a telecommunication lease agreement that can't be annulled where operators purchase the infrastructure right of use. It is usually a very long term contract, in the case of Unidata with a length of around 15 years.

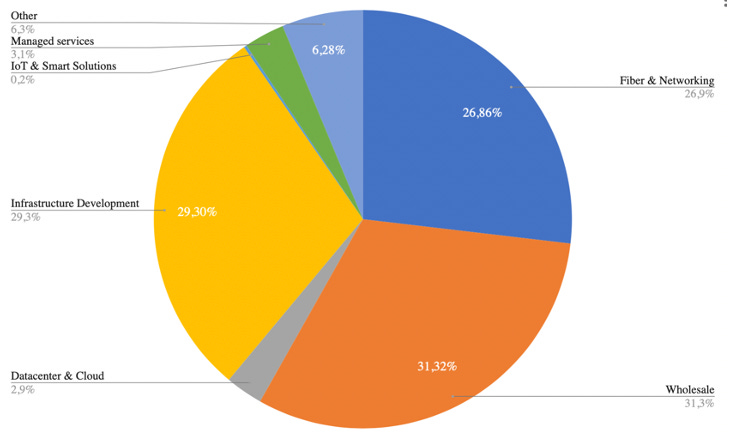

The company divides their revenues in different sources of revenue that, in our opinion, complement themselves placed in difficult to disrupt markets with a bright future.

Fibre & Networking: Unidata brings internet connectivity to final customers mainly thanks to their fibre proprietary FTTH network architecture. The growth in customers has been unstoppable during the last few years. As an example, in 2022, the number of Consumer customers grew by 30%. It currently reached 290,000 residential and business units and with one of their Joint Ventures they are continuing to build infrastructure in grey areas. In this source we group the revenues from internet access through optic fibre, XDSL and wireless, but also the voice trading and the wholesale service.

Providing internet access is a service with recurrent revenues, a short payback period and that can be scaled. A critical measure in businesses like this is the churn rate. Unidata has a c.12% churn rate, compared to a typical 14.7% (we have used the source with the lowest figure) in the telecom sector in Italy. However, Intred, the most comparable competitor has a churn rate below 4%.

We analyse each segment of its business model, discuss the TWT acquisition with some comments about the management. We see one by one the undertaken joint ventures as well as the markets where Unidata competes with a positioning relative to competitors. We finish with a detailed PL model to get to a fair value of the stock and some conclusions of our thoughts of this company. (Get the best price on our website!)

2) Jadestone Proposed financing or how to squander the credibility of management

After having been covering Jadestone for over two years and following it since 2020, today we write an article about the company's latest move, surely at its most critical point, both due to its financial situation and the credibility of the management, which has clearly been called into question.

After several weeks of consecutive communication errors that had driven its price to a 2.5-year low, Jadestone has issued a capital increase in which its largest shareholder, Tyrus Capital, along with the board and the rest of the main institutional investors, have participated.

This article aims to cover the details of the capital increase, the current situation of the company (from a financial and operational standpoint), reflections on this latest move, the scenarios that arise from now on (both for current investors and opportunists), the resulting financial structure, and our point of view.

Disclaimer: This article solely explains our opinions based on publicly available information published by the company and does not constitute any form of financial advice.

Jadestone (LON: JSE - Market cap $270MM) announced a capital increase on Tuesday.

They placed $52.6MM ($2.6MM fees)among institutional investors, and there will be an open offer for minority shareholders amounting to €8MM (approximately $8.6MM), allowing them to acquire 1 share for every 30 shares they currently hold, at a price of 45p per share.

Additionally, a $35MM standby working capital facility has been signed (by Tyrus Capital), which will be reduced based on the result of the placing that exceeds $50MM. From our perspective, the terms of the facility seem distressed: 5% undrawn / 15% drawn amount + 4.3% arrangement fee (minimum $1 million) + $30MM in warrants with a strike price of 50p over 36 months.

In other words, in exchange for approximately $85MM, the number of circulating shares will increase from the current 446MM to around 570MM if the warrants are executed.

Tyrus participated in the capital increase with its current 26.45% ownership and commits to lend, up to a maximum of $50M (Equity Underwrite Facility), the gap to $50MM of capital rise intended. Naturally, they charge a fee for providing this assurance: 5% undrawn / 13.5% drawn amount + an arrangement fee of $2.15 million. Note: the Underwrite Facility wasn’t necessary as the placing was oversubscribed.

We believe that the terms are highly dilutive for minority shareholders but beneficial for the major shareholder, Tyrus Capital (which is, after all, a Hedge Fund pursuing its own objectives).

This is happening despite having signed a $200MM Reserve-Based Lending (RBL) facility just 10 days ago.

The RBL facility was intended to cover the necessary Capex for Akatara, M&A activities, and infill drillings (so far, at least $50MM has been drawn to repay the interim facility).

Initially (as announced in April), the RBL facility required to hedge 40% of the production (from 4Q23 to 3Q24 inclusive), but now it has been changed to 50% of production from 4Q23 to 2Q25.

Currently, 64% of the production ( required to hedge) has been hedged at $70 per Brent barrel through swaps. This is the minimum Brent price in the last 2 years (and several dollars below the current 2024-2025 forward curve). These hedges include any potential premium.

In this context:

Jadestone was already producing 17,800 barrels per day, with 7,000 barrels coming from Montara, its main asset. The shutdown of Montara for 7 months significantly depleted the company's cash reserves.

The company's value had decreased by 40% in recent months, partly due to operational issues at Montara and partly due to poor communication through RNS (Regulatory News Service) announcements during this period.

Jadestone had been involved in M&A operations and had implemented a share buyback program, spending approximately $20MM to repurchase shares when the stock was trading between 70-90p.

This lead us to share some reflections regarding decisions taken by Jadestone’s management

Why did they need this financing if the RBL was closed just 15 days earlier? What has happened in a span of six weeks of time that requires diluting investors by 27%? Additionally, why is the RBL expected to be reduced in three quarters' time?

It appears that no one was able to conduct a stress test between July 2022 and January 2023 when they were finalizing the acquisition of North West Shelf and completing the 10% acquisitions of Lemang PSC and Sinphuhorm, while Montara was shut down and they were buying back shares under the assumption of Brent at $70 (the 10-year average). Did they not anticipate the extended operational issues at Montara?

Why do the conditions of the standby working capital facility resemble those of a distressed company and why were they signed despite not needing it? Why wasn't a bridge loan sought in 2023 if the debt problem is expected in Q2 2024?

As of May 31, 2023, the company had $41.2 million in cash and a debt of $50 million. With the $200 million RBL facility (available since May 22, 2023) and repayment of the current debt (actually paid on the 1st of June as confirmed in the Annual Report submitted on the 8th), the company's liquidity would amount to $191.2 million. The company itself expects to use $135 million of the RBL in the next 6 months, leaving $56.2 million still available in six months from today, which considers zero cash generation at 17,000+ boepd. Is a standby working capital facility at a 15% rate necessary at this moment?

The repair of the Montara FPSO could have potentially been carried out at a shipyard in Southeast Asia, taking less time and resolving all the problems, including those that persist today, such as the closure of petroleum tanks. It is unclear whether this decision was made to save money, due to lack of knowledge, or due to limited space in shipyards.

How will the developments in PNLP (formerly non-operated assets in Malaysia that Jadestone now plans to redevelop) and Vietnam be financed? Is it the right time to invest in assets as problematic as PNLP, whose FPSO was in such poor condition that it lost its classification?

and about its communication to the market…

If they were producing over 17,000 boepd, why wasn't it communicated to the market until after the capital increase, despite the company announced they wanted to improve its communication with shareholders?

The series of grave errors in the RNS announcements in recent months, such as publishing incorrect guidance (revising it downward by 1,500 boepd shortly after presenting it), the need for Montara to halt production for a few days due to a typhoon without it being disclosed despite the impact on production, or the continuous suggestion that end of repairs was imminent without providing any planning - even an approximate one. Why didn’t any of these incidents cost the IR their position?