Mother Trucker

The trend is your friend … until it ends

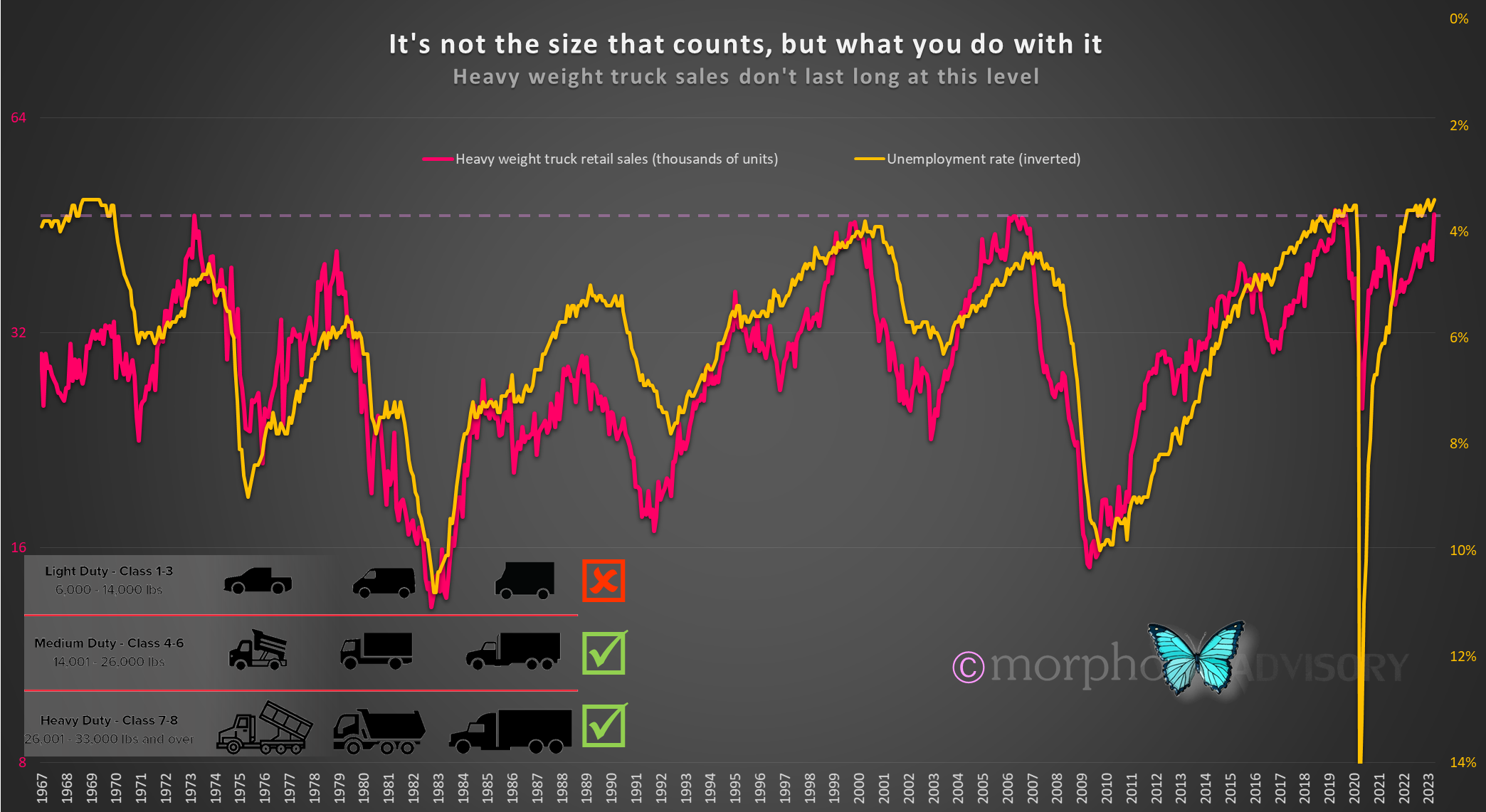

There has been some persistently good economic data of late. Most of it good on a relative basis, i.e. the ISM Manufacturing Index not as negative as expected, but some of it good in absolute terms, like the Unemployment Rate at 3.4% and U.S. heavy weight truck sales jumping higher last month. With so much mixed data about it is giving plenty of ammo for each side of the bull-bear stand-off in markets, and that is creating the current pain trade. In my opinion, the current pain trade is this long, slow sideways (directionless) market. It is a market that requires patience, discipline and resolve as it attempts to slowly erode the will of participants, causing doubt and questioning. I think what has added to the slowness is the fact that we are heading into the most predicted recession in history.

Since the GFC and its dramatization through movies such as The Big Short, more people are aware of macroeconomic conditions than ever before. This has led to people entering short positions in mid-2022 only for the market to subsequently hold up. This is the pain trade in action. The market inflicts pain on those people who want to profit the most, but who also want to experience losses the least - the weakest hands.

In any event, the economy will be the ultimate arbiter of the direction of markets, which brings us back to the low Unemployment Rate and U.S. heavy weight truck sales, which had their 4th highest monthly sales in April 2023.

Surely, this sort of economic data means the economy is strong? The Fed certainly think the economy is strong enough to warrant higher rates while still thinking they could be in for a soft landing - maybe even no landing, i.e. no recession.

Yes, the narrative sounds good, but let’s look at that data another way.

Historically, when heavy weight truck sales get to this level we are at the peak of the economic cycle and there is nowhere to go but down. Additionally, there seems to be a pattern of a jump of several thousand unit sales late in the cycle, like a last surge before the end.

The correlation of the unit sales of heavy weight trucks with the unemployment rate has over 50 years of data. Both suggest we are near the end.

It’s not surprising, really.

Central banks have been raising interest rates rapidly on a highly indebted population.

The size and speed of the rate rises are another factor to consider. It is said that “people don’t like change”, but I think that is inaccurate. I think people don’t like rapid change.

We are likely at the end of central bank rate hikes, with the possibility of maybe a single additional hike, but that is immaterial. We are now waiting for the impact of the last 15 months of rate hikes to feed through. It reminds me of those reality TV games like Survivor where contestants have to balance, touch/hold something, or carry a weight for a prolonged period of time. Slowly, one by one, the contestants fall away. That’s what central banks are now doing. They are not going to drop interest rates just because some banks fail. No, they’ll arrange new ownership for them, but they’ll keep rates up until they see inflation very near to their target, which will be near Christmas at the very earliest, quite possibly into 2024 because central banks like hard data (actual economic data, not survey data), which is lagging (it takes time after the event for this data to be published). Only if something breaks in the economy will they ease earlier.

I don’t know what it’s like where you are, but many people are beginning to struggle financially here in NZ, and the entire Western developed world is going through the same cycle. The pressure is up and some people are just hanging on, while others are hoping that rates fall before the interest rate on their loans reset.

And here’s the thing that most people don’t seem to understand, including central bankers, economists, Wall St analysts etc. When the economy enters a significant downturn, it’s not linear like a Survivor endurance challenge where, one at a time, people drop off. No, the downside is exponential and accelerates quickly. The failure to understand this aspect is why people are so calm looking at the data at present, because it looks linear in the initial phases, i.e. each 25bp or 50bp hike hasn’t added to any significant change in the economy or personal bankruptcies etc. The same is true with the stock market, equity valuations have simply fallen in a linear manner reflecting the change in interest rates (the discount rate). The aggregate impact of all rate hikes combined with prolonged pressure creates for an explosive mix - a chain-reaction.

A series of unfortunate policy reactions

The rapid rise in interest rates has been a reactionary response to inflation.

Inflation was caused by a reaction to Covid-19 where governments threw money at people who didn’t need it (for the most part). People were locked up in their homes and unable to travel. They were given stimulus payments plus virtually free money when it came to borrowing. All this free/cheap money plus unusable travel funds were diverted into other consumer activities, e.g. online shopping; buying new vehicles; online trading; property renovation … plus many people returned to their home countries, pushing property prices higher in those locations.

How do we make sense of what ‘normal’ should be when we are still in an environment distorted by reactive behavior?

The relationship between the price of copper to that of gold is a good gauge for interest rates. The price of copper reflects economic activity, whereas gold reflects risk aversion.

At present, longer-term interest rates have gone significantly above where economic activity suggests they should be. They have still been rising even as economic activity (copper) has fallen relative to risk aversion (gold). This is due to central banks ramping interest rates higher to bring inflation back down. This overshoot is going to have consequences, just as the Covid-19 stimulus had consequences.

When it comes to understanding risk, there is the probability of an event occurring, but there are also the consequences should that event occur. The academics in our leading institutions look at the former and disregard the latter.