Behind the Block: PoW vs PoS

Behind the Block: PoW vs PoS

Part 1 - Proof of Work: what is it and can you still make money mining cryptocurrency.

This week I learned (or rather re-learned) a vital lesson: don’t underestimate yourself! Since the pandemic, I delivered multiple public and private talks, workshops and webinars, all online. It has been four years since I last presented in-person, so when I was invited to talk in front of a local crypto community, I got nervous.

I went to this great university tech campus in Faro, south of Portugal, and as soon as I saw first people entering the room I felt my heart sinking just a bit. 😅 Thoughts like “what if I bore them” or “they must know more than me” started ringing in my head.

It was an intermediate level discussion on proof of work (PoW) and proof of stake (PoW) - comparison, strategies to follow, what research is needed to understand where to invest, what pitfalls to look out for. I even brought props with me, an ASIC cryptocurrency miner that was once part of my mining farm.

As soon as I started my presentation, I felt in my element. I like to engage my audience with questions and I soon realised my ten years in this industry are valuable, and I know more than I give myself credit. It’s not like I lack confidence or I don’t know what I’m capable of, but like most of us, I sometimes think that other people know just as much. After all, there’s so much information available. However, as my husband and my son tell me (frequently), just because people trade crypto or read articles about it, doesn't mean they do research or try to understand basic concepts.

It’s not a criticism as we all have different goals I suppose: I see myself as an educator spreading knowledge and a philosophy, whilst others just want to diversify their investments. And that’s ok, because my personality pushes me to learn about where I put my money and why, and that’s just my way of doing things.

Now, getting back to the reason I’m writing today, I thought to share with you what I talked about this week.

Because there is a lot of information to digest, I will be splitting this in two parts:

In this article I will be explaining proof of work networks, what is mining, is mining still profitable,

andnext week I will be continuing with proof of stake, brief history, and what to look for when considering staking.

Understanding Proof of Work (PoW)

Let's kick off with Proof of Work. Imagine you're in a competition where the first to solve a complex puzzle wins a prize. In the blockchain world, these puzzles are cryptographic problems, and the participants are called miners. These miners use powerful computers to solve puzzles, and the first to do so gets to add a new block of transactions to the blockchain. This process is known as mining, and the reward? A certain amount of cryptocurrency.

But what is a blockchain? In a sentence, blockchain is a vast accounting ledger, in digital format. A ledger, in the simplest terms, is like a detailed notebook or a diary that keeps track of every transaction or activity that happens within a business, or in the case of cryptocurrencies, within a blockchain network. Think of it as a record book where every entry details who gave what to whom, or who received what from whom.

Governance in a proof of work network often stems from community consensus. Miners and other participants often gather in forums or through other informal channels to discuss changes. However, sometimes significant changes require a consensus that's hard to achieve, leading to forks—splitting the blockchain into two paths. A famous fork example is the Bitcoin and Bitcoin Cash split in 2017, sparked by disagreements over block size.

Bitcoin is the first cryptocurrency to introduce the concept of PoW and blockchain to the world. As of the latest data, the Bitcoin network has over 1 million miners. These miners validate transactions and secure the network, making it incredibly resilient against attacks.

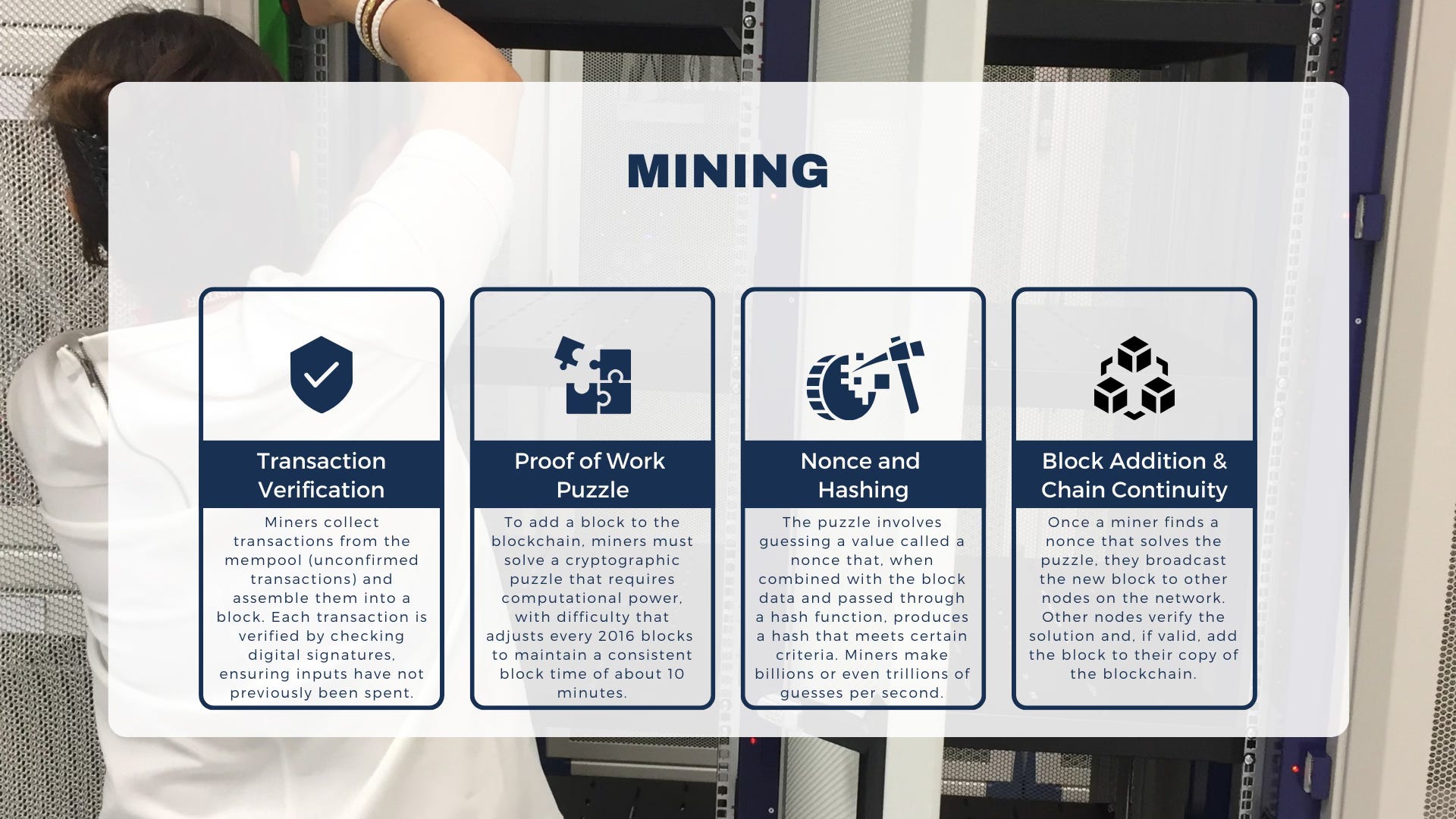

Have you ever thought how mining effectively adds blocks to the blockchain? Here is one of my slides that explains the process to an extent (and yes, 😅 that’s me in the background setting up my miners).

There are a few concepts that I would like to explain:

In a proof of work network not only do you have miners, but you also have nodes. A node can be any of us having downloaded a copy of the blockchain on our computer, and keeping live (which means it gets updated in real time so the computer must be online at all times). The difference between nodes and miners is straightforward: while all miners are nodes, not all nodes are miners. Nodes maintain a copy of the blockchain and uphold the network, but miners do the heavy lifting of processing transactions and securing the network. Together, they make sure the network is decentralised and secure.

A mempool is a memory pool, or simply said a list of transactions that you and me want processed. These transactions are not yet confirmed and not yet added to the blockchain.

A nonce is short for “number only used once”, or else, a unique number that can’t be repeated.

A hash function takes information (in this case, the block's transactions, the previous block's hash, and the nonce) and produces a unique, fixed-length string of characters. No matter how many times you hash the same information, you'll always get the same result, but if you change even a tiny part of the information inserted, the result hash will be completely different.

The Reward Mechanism: the first miner to solve the puzzle and have their block added to the blockchain receives a reward in two parts:

Block Reward: a predetermined amount of new bitcoins created and awarded to the miner. The block reward halves approximately every four years in an event known as "halving." On April 20th, 2024 the current reward of 6.25 bitcoins per block will be cut in half, but this will continue to decrease over time until all 21 million bitcoins are in circulation.

Transaction Fees: in addition to the block reward, miners also collect the transaction fees associated with the transactions they have confirmed and included in the block.

Let’s use an analogy to understand mining better.

Imagine you're at a carnival, and there's a game where you need to guess a combination of numbers to unlock a chest. You don't have a clue what the combination might be, so you start guessing. Each guess takes a bit of time because you have to try the combination on the lock.

In this game, the chest is the new block that miners are trying to add to the blockchain, and the combination lock is the cryptographic puzzle. Your guesses are the nonces, and the act of trying the combination on the lock is the hashing process. The first person to guess the right combination (find the nonce that produces an acceptable hash) gets to open the chest and claim the prize (the block reward and transaction fees).

The difficulty of finding the correct nonce is by design. In the carnival analogy, if the combination was easy to guess, or if you had a key that could open any chest, then the game wouldn't be fair or fun. By making the puzzle hard to solve, PoW ensures that:

It takes significant computational effort to find the solution, securing the network against fraudulent activities.

It creates a competitive environment where miners are incentivised to participate and invest in computational resources.

It regulates the creation of new blocks, ensuring a steady, predictable supply of new bitcoins until all 21 million are in circulation.

Can you still make money mining cryptocurrency?

Yes, you can still make money mining cryptocurrency today, but the approach and profitability depend on the choice of cryptocurrency, the cost of electricity, and the hardware used. Here are a few ways to approach mining in today's world:

1. Mining Less Popular Cryptocurrencies

Example: Think of it like fishing in a smaller pond where there are fewer fishers but plenty of fish. Mining cryptocurrencies like Ravencoin or Monero isn't as fiercely competitive as mining Bitcoin.

How: You can use gaming computers (GPUs) to do this mining. These aren't as powerful or expensive as the specialized equipment needed for Bitcoin, making it easier to start.

2. Joining a Mining Pool

Example: Imagine a group of fishermen pooling their resources to catch a big haul. Everyone contributes their nets (computing power), and when they catch something, they split it based on who contributed what.

How: When you join a mining pool such as Slush Pool for Bitcoin or other pools for alternative coins, your computer adds its power to a group of others. The money you make depends on how much work your computer does compared to the rest.

3. Cloud Mining

Example: This is like renting a boat and fishing gear at a lake. You pay to use the equipment, and you keep all the fish you catch, minus the rental costs.

How: You pay a company like Genesis Mining or Hashflare to use their powerful mining machines, which are stored in big data centers. You make money from any coins that are mined, but you have to subtract the fees you pay for renting the equipment.

4. Mining with Renewable Energy

Example: Think of this as using a windmill to power your water pumps for fishing instead of paying for expensive electricity. If the windmill is your own, you don't pay for the wind!

How: You set up your mining computers (rigs) in a place where you can use cheap or free renewable energy, like solar panels. This cuts down on the biggest cost of mining—electricity—making it more likely that you'll make a profit.

Each of these methods offers a different way to get involved in cryptocurrency mining, depending on your resources, interests, and the amount of effort you want to put in. Whether you're working alone or with others, using rented equipment or your own setup powered by the sun, there's a mining style that could suit your situation.

Steps to consider when deciding what to mine:

Assess profitability: Start by visiting a website like whattomine.com. This site helps you understand what cryptocurrencies are currently profitable to mine. You can enter details like your mining hardware's capability (hash rate) and your electricity cost to get an estimate of your potential earnings and expenses.

Cost of mining equipment: Next, look up how much it would cost to buy the mining hardware. This could range from basic setups like GPUs (the same kind used for gaming) to more specialised mining rigs. The price will vary depending on how powerful the hardware is and what kind of cryptocurrencies you want to mine.

Choosing the type of mining equipment: if you’re buying a GPU to mine and after a while your chosen cryptocurrency becomes too expensive to mine, your GPU can be reconfigured to various other cryptocurrencies. An ASIC (application specific integrated circuits) miner is manufactured and coded to mine ONLY a specific cryptocurrency and can’t be repurposed.

Break-even analysis: Calculate how long it will take for your mining earnings to cover the cost of your equipment and electricity. This is when you start making a profit. It’s crucial to know this so you can decide if the investment in time and hardware is worth the return.

Comparing options: Sometimes, buying the cryptocurrency directly might be cheaper or less hassle than mining it. Another option is to rent mining power from services like NiceHash, where you can pay to use someone else's mining rigs. Compare these options to see which offers the best return on investment without needing to buy and maintain your own equipment.

Market accessibility and liquidity: Check where the cryptocurrency you plan to mine can be traded. If it's only available on obscure or foreign exchanges that you can't access or that don’t adhere to current standards, it might be hard to sell your mined coins. Look for coins that are listed on reputable, accessible exchanges to ensure you can easily trade them.

Additional Tips: Solo mining has become quite difficult with increased competition. It’s helpful to connect with other miners or mining communities to get insights into what’s currently trending and worth mining. These contacts can provide valuable advice and updates on the mining landscape.

Further resources:

Blockchain demo: An insightful demonstration on how blockchain works.

Blockchain.com Explorer: Offers detailed information on Bitcoin transactions, blocks, and addresses. You can view real-time blockchain data and various network statistics.

Website: https://www.blockchain.com/explorer

Blockchair: A versatile blockchain search and analytics engine for Bitcoin, providing detailed data on transactions, blocks, and addresses, alongside a wealth of network statistics.

Website: https://blockchair.com/bitcoin

BTC.com: Provides detailed data on Bitcoin blocks, transactions, and statistics, including mining information, pool distribution, and network activity.

Website: https://btc.com/

CoinMarketCap: Provides key statistics, such as market cap, volume, supply, and price changes for both Bitcoin and Ethereum, among other cryptocurrencies.

Website: https://coinmarketcap.com/

Glassnode: Offers advanced blockchain data and analytics, including on-chain metrics, market indicators, and insights for Bitcoin, Ethereum, and other cryptocurrencies. It's particularly useful for more in-depth analysis.

Website: https://glassnode.com/

Well, that’s it for today! I hope it helps you understand a relatively young technology that might become an integral part of our future.

Until next week, if you have any questions just write it in the comments below.

Thank you for sharing. Your use of metaphors makes everything really easy to understand. Keep going! I loved this quote: "My personality pushes me to learn about where I put my money and why, and that’s just my way of doing things."