A Response to Kerrisdale's MicroStrategy Thesis

A Response to Kerrisdale's MicroStrategy Thesis

And a word of caution...

Kerrisdale Capital recently came out with a report detailing their thesis for a long bitcoin/short MicroStrategy pair trade.

The report made the rounds on Twitter, being cited as a reason for the $MSTR underperformance the day it came out (I’m dubious but it doesn’t really matter), and I’ve gotten a lot of questions about my thoughts on it so I figured I’d publish a quick reponse.

MSTR was down 11% the day the report came out (before market open on March 28) on a day bitcoin was up 3.4%, closing the premium to NAV MSTR trades at by call it 15% in a day. For all I know, Kerrisdale could be out of the trade for a tidy 15% one day profit.

I have a lot of respect for Kerrisdale. I'm subscribed to all of their reports, read most of them, and have followed them into some short ideas before.

I think they’re missing the forest for the trees on MSTR.

“In the long run we are all dead.”

Look, I get it.

In the long run, and assuming bitcoin keeps going up, MSTR should trade for the value of its bitcoin holdings.

It currently trades for 250% of the value of its bitcoin holdings. It traded for the value of its bitcoin holdings as recently as January. It is reasonable to expect the current premium to NAV to collapse back down to zero. Long bitcoin, short MSTR, 150% return, have a nice day.

But when MSTR was trading at the value of its bitcoin holdings two months ago, was it reasonable then to expect it to blow out to 250% in two months? Because that’s what happened.

My primary point is that it is also reasonable to expect it to blow out to 300%, 400% … 500%? There’s really not a level where I’d think “that’s impossible,” until we start getting into law of large numbers territory.

And, moreover, if you want to take a stab at guessing which way it is going to go next, I think you’d be better served studying bitcoin, memes, S&P 500 inclusion rules, and short squeezes than studying the premium to NAV.

Your counterparty doesn’t care about premium to effing NAV.

They care about Michael Saylor memes, squeezing hedge funds out of business, and pumping stocks into the S&P 500 where they can dump it on retirees.

“The market can stay irrational longer than you can stay solvent.”

I hate quoting Keynes in a bitcoin-adjacent post so much, but man he did have some bangers.

The primary point Kerrisdale makes is that MSTR trades an “unjustifiable” 2.6x premium to NAV, and that “no fundamental reason for this premium exists.”

And yet, it exists.

We must ask ourselves, why? Maybe fundermentalsss are not the best place to start formulating a thesis on MicroStrategy.

To me, arguing that something is not tethered to reality and then betting on it becoming tethered to reality is not a good strategy.

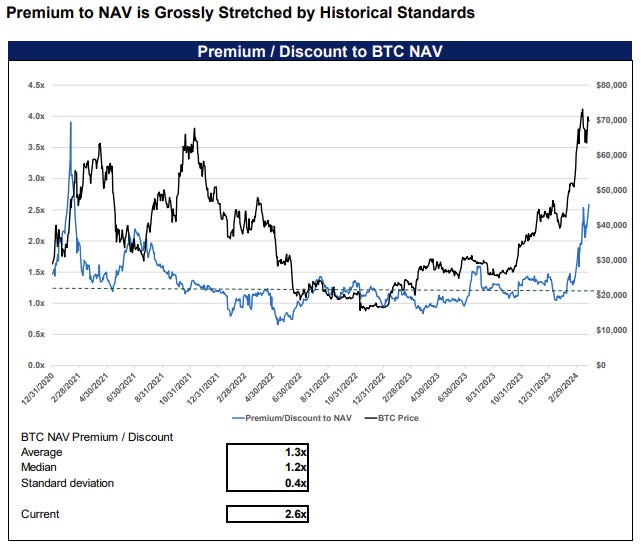

They point out the current premium to NAV is stretched by historical standards, and I don’t disagree:

But guess what? I see a historical precedent on that chart for a 4x premium to NAV. That’s 150% from where we are now.

So that’s what, 150% up 150% down risk/reward, assuming the premium doesn’t blow out to levels higher than it ever has before?

I used to trade these pairs professionally — share class pairs, premium/discount to NAV, tracking stocks — and in my arrogance and naivety, was carried out in a body bag too many times because I thought “there’s no way the spread blows out to all-time highs again, right?”

Not again. Not me.

What IS The Right Premium for MSTR?

Kerrisdale concedes in their report (top of page 5) that some premium is warranted, just not 150%.

Which begs the question — how much then?

I try to dive into this question in my recent post MicroStrategy Is A Bitcoin Bank, where I suggested one could view MSTR as a bank that was compounding book value per share and apply a multiple to book value to value the business, as opposed to a closed-end fund that was trading at a premium to NAV and assuming the NAV premium would ultimately collapse to zero.

It’s a quick read and I encourage you to read it, but the TLDR is:

MSTR has compounded bitcoin per share at 18.9% since Q4 2020 and trades for 2.5x tangible book.

JPM has compounded tangible book value per share at 9.2% over the same period and trades for 2.4x tangible book.

Both have a balance sheet that they leverage to try and grow book value per share. MSTR has done this more effectively than JPM since they adopted their bitcoin strategy. Which valuation is unjustifiable? I’d argue neither.

Because of MSTR’s leverage (they have borrowed money to buy bitcoin), you would expect their NAV to increase more than the bitcoin price in a bull market and fall more than the bitcoin price in a bear market. The below table from MicroStrategy’s Q4 2023 earnings report illustrates some hypotheticals, with Kerrisdale’s commentary below.

This was from February 5, 2024, when the price of bitcoin was $42k and MSTR stock was at $490.

Since then, MicroStrategy has indeed taken $1.4 billion in incremental leverage with not one but two convertible note offerings, and the bitcoin price has hit the first checkpoint at $69,000.

So, $1 invested in MSTR stock on February 5 is already worth $1.95 today assuming no change in premium to NAV (in reality, it is worth $3.45 today because not only has the NAV increased but the premium to NAV has increaseed as well), while $1 invested in bitcoin on February 5 is worth $1.60 today.

Kerrisdale acknowledges the potential impacts of leverage on their trade by including this slide and discussing it, but argues even in MicroStrategy’s most bullish scenarios the gains in the NAV relative to bitcoin do not justify the premiums.

The above is basically a sensitivity table, with the two inputs being incremental leverage and bitcoin price.

It’s only been two months and already MicroStrategy has exceeded the maximum incremental leverage considered by the table.

Are we sure they’re done issuing convertible notes?

Are we sure bitcoin isn’t going above $250k?

In A Bitcoin Bull Market, The Premium Is Likely To Increase

This one is both true historically based on the empirical evidence, and also true in theory because of the leverage in the model discussed above.

Let’s look at this chart again. What do you notice?

What I notice is that when bitcoin rips to new all-time highs, is exactly when MSTR’s premium to NAV hits new highs as well.

What makes anyone think it won’t happen again?

The time to go long bitcoin/short MSTR is in a bear market, not a bull.

We are in a bull market.

Who Is The Counterparty?

I’ve spent entirely too much time addressing the premium to NAV debate, when at the top I made the point that it doesn’t even really matter.

So, what does matter?

Whenever I’m in a trade, I like to ask myself “who is on the other side of this trade?”

So, who is long MSTR when, as Kerrisdale points out “bitcoin is now easily obtainable through brokerages, crypto exchanges, and more recently low fee ETPs and ETFs.”?

I am, because I’m bullish bitcoin and I see the potential for MicroStrategy to become a meme stock. I’m not selling because I think the premium to NAV is going to collapse in the middle of a bull market. I’m holding, because I think the opposite.

Thousands of bitcoiners are, because they bought at cheap prices and like owning a bitcoin piggy bank that grows their bitcoin per share over time. They’re probably not selling.

Index rebalance pod shops are because MSTR is eligible for both Nasdaq 100 and S&P 500 inclusion. They’re not selling until the indexes add the stock.

Professional squeeze traders are, because they see the short interest is 22% and a new big name announces publicly that they’re short every month. They’re not selling until people lose interest in shorting.

And the reddit / retail crowd hasn’t even really got in on the action yet, because options are too expensive because the stock price is too nominally high.

But what do you think is going to happen when people start to realize we’re just a few out-of-the-money calls away from that $3,000 dot com bubble peak?

The most entertaining outcome (as if we were in a movie) is the most likely

Then the stock-split comes, sending shares up another 10% because now retail options punting is nigh.

“Who controls the memes, controls the Universe”

Money is a meme.

Bitcoin is the ultimate meme.

Because Bitcoin is good art.

Or better yet, because Bitcoin is elegant and beautiful fashion, sitting at the intersection of art and commerce.

Most importantly, because owning Bitcoin has been an authentic expression of identity, an extremely positive identity of autonomy, entrepreneurialism, and resistance to the Nudging State and the Nudging Oligarchy.

— Ben Hunt, In Praise of Bitcoin

Jeo Boden is a meme.

Costco hot dogs are a meme.

Michael Saylor is a meme.

GameStop was a meme.

What do you think GameStop’s premium to NAV was when it went up 100x in 6 months? What was the fundamental value?

Kerrisdale and everyone else who has taken a shot on the long bitcoin / short MSTR pair trade might very well be right! They might even probably be right. They’ll almost certainly eventually be right.

They might make money, and I sincerely wish them the best. We can even both make money at the same time! I’m simply betting on MSTR to go up. They’re betting that MSTR doesn’t go up more than bitcoin, or down less than bitcoin.

But there’s got to be easier ways to make money and sleep at night.

I’ve never seen a more combustible set-up.

If it were me, I’d only trade the short-side on short-term catalysts and with tight stops.

MicroStrategy or The Real Thing?

I want to conclude by emphasizing that owning MicroStrategy is not a substitute for owning bitcoin.

It is a bitcoin price exposure vehicle, like an ETF, but with leverage and more volatile.

Sometimes the price performs better than bitcoin, sometimes it performs worse than bitcoin. There is no guarantee how it will perform relative to bitcoin going forward.

You cannot spend MSTR shares for goods and services, and you cannot send them around the world. You cannot carry them with you across borders.

Whether you should hold spot bitcoin or MSTR I think depends on your thesis and holding period.

If you think bitcoin is on a death march to $100k within the next 3 months because of ETF flows and the upcoming halving and you want to punt 50 bps of your capital on that thesis in an attempt to grow your fiat wealth, maybe being long MSTR stock is a suitable expression of that trade.

If you think bitcoin is money and you want to save 10% of your capital in it, permanently, then holding spot bitcoin is probably a better expression of that trade.

NONE OF THIS IS EVER FINANCIAL ADVICE DO YOUR OWN DUE DILI.

Good luck out there, and please be careful shorting memes.

🎯💯