Risk on Infinity

Risk on Infinity

This article will take you down the historical marvels that began the hyper financialization of the global market cap.

Welcome back to NeuroInvest Research!

Let’s dive right into it.

In the last few decades, market participants had been conditioned to an environment of falling rates and tailwinds for assets. Whether that was real-estate, stocks, you name it, the market juiced it.

This article will take you down the historical marvels that influenced this behavior.

What the article will cover:

3 influential periods that juiced the economy

The side effects of juicing AKA ‘credit’

What these historic events can tell us?

Epoch #1

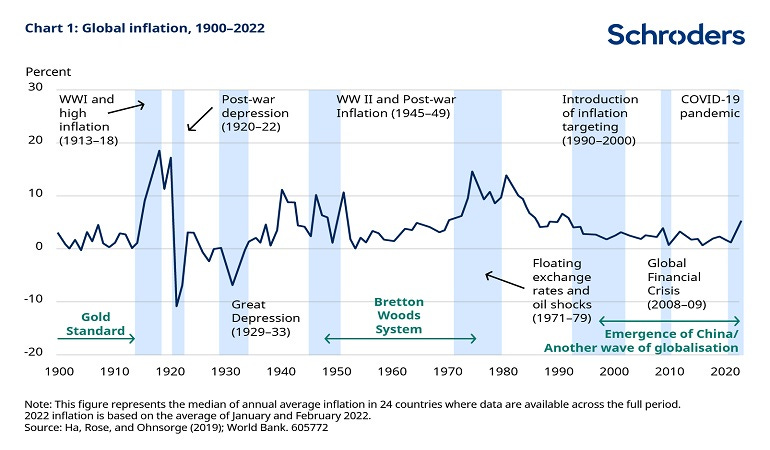

The end to the gold standard.

The virtuous cycle began as early as the 50’s within the Eurodollar system, and accelerated when President Nixon took coordinated actions to close the gold window in 1971.

In the midst of a gold run, and inflation running rampant, Nixon’s administration began coordinating a battle plan to keep the inflation beast under control. The first course of action was the decision to sever the gold channels from foreign governments; ultimately, preventing the redemption of dollars for gold.

The second order effect was a direct attack on wages and prices.

You may be asking yourself, why is this important?

Well, all the current macroeconomic events, would add up to be the perfect set of ingredients to brew a deflationary decade and the beginnings of a risk on infinity.

Green light for Risk.

Amidst the current policy changes in the U.S, China, was simultaneously setting lower global labor costs - adding to this seemingly limitless supply of goods and services.

Western businesses, particularly multinationals, were extreme beneficiaries of this environment. Falling interest rates, globalization, the ability for corporations to reduce their cost basis offshore, it all seemed quite too perfect if you were ahead of the game and played your cards right.

Epoch #2

The wake of radical capitalism.

71 brought an era of credit expansion, leading the profit share of GDP to elevated levels. When credit was cheap, and accessible, it brought a new standard.

It was only until the great financial crisis (GFC) when everything hit a wall. It turned out that this constant accumulation of debt backed by rising asset prices was not sustainable.

Who would have known *cough* (sarcastic remark).

For decades, everything in the world had been deleveraging. Which, in the eyes of the central bankers, could be offset with a reflationary lever, AKA printing money, or what you should be calling it by now printing ‘bank reserves’.

Post GFC, new regulations and conditions were unraveled, hoping to provide more stability and risk management to the private sector balance sheet.

Big money would of course seek a place to park their cash and reek better rewards. The waves of liquidity poured into assets, stocks, etc., entities looking to capitalize on the new era of cheap money.

Green light for Risk.

It’s important to note, deflation tends to have inhibitory reactions on consumer spending and limits the components that make up economic growth. Companies respond to these deflationary regimes with layoffs, salary reductions, slowing production which adds weight on the shoulders of policy makers.

Over the course of history, deflationary environments tended to breed these hyper financialized states soon after.

Don’t worry we’ll dive deeper into this.

Epoch #3

Helicopter money.

The third epoch is post-COVID. This risk on period enabled such an extreme degree of money printing that it outpaced dramatically even a record amount of fiscal spending and fiscal borrowing.

The ‘helicopter’ money gave the public sector a reason to spend on the already juiced up market. The common narrative ‘get rich buying stocks’ sent hypnotic waves across the globe.

Green light for Risk.

Unfolding the Layers of the Current Epoch

During these periods of hyper-financialization, approximately 60% of global GDP had been destroyed in terms of asset valuations.

Market participants did not want to see the truths - an inflated market cap is not always a function of it’s organic and productive economic output. The juice that influenced these high multiples and large spreads, was largely the result of cheap credit and weak monetary transmission mechanisms.

The problems become transparent when the punch bowl is taken from the party, but in the case of our monetary system, the debt is left to be paid off.

Food for thought: Our monetary system is designed with competitiveness in mind. It is a profit driven world that conditions these unnecessary bad norms and shorter-term policy choices. Capitalism, unregulated had bred this competitive nature in finances and commerce, but in light of the necessary real growth that we desperately needed - a trigger for demand of credit.

Today, these valuations are already trending downward to connect back to their organic mean. In an environment where credit is being absorbed (quantitative tightening), as well as becoming increasingly more expensive, earnings tend to fall short of their performance.

Does this start to make sense? Why things have been so gloomy, and the final straw for a recession seems to permeate through each click of your social media feed?

Based on these historical reiterations, the outcome and the current data seems seems to conform to that gloomy premise.

Let me explain.

A weak hand of cards.

The current macro-condition require positive real rates to choke off inflation; however, balance sheets are less equipped to handle positive real rates, largely because of the current debt levels.

The rising cost of servicing the debt is going to keep squeezing incomes, which will likely carry into a spending contraction. Since labor is the bread and butter of economic output (spending and income), the major impact on employment is to be seen.

With regards to this sequence of events, is inflation likely to persist or are we done seeing it for now?

This is the question that has stumped many economists today - are faced with a deflationary or inflationary environment moving forward?

Even though it is never black or white, we can run some quantitative diagnostics to determine the potential likelihood of each of these potential scenario, of course using historical parallels.

Stay tuned for more updates regarding this debated topic.

I hope I have shed some light on these paradigm shifting epochs.

Please do comment, share, like. You know the drill :)

You can also find me presenting my work on Twitter: Neuro__Invest

A Glimpse Into the Market Diagnostic Reports!

Coming to you soon!

I write and share this work for the sole purpose of my passion for understanding the monetary system. If you made it thus far on this journey with NeuroInvest Research, I greatly appreciate your presence.

Aside from the current monthly research papers, NeuroInvest Research will be offering a free Market Diagnostics Report. The reports be covering the current market trends, analyzing macro conditions, bitcoin on chain analysis, as well as, a completely transparent, medium to long term actively traded portfolio.

More details to come soon! Keep updates.