Boring Is Better - Investing In The Unusual Suspects (HDSN)

Boring Is Better - Investing In The Unusual Suspects (HDSN)

The simpler it is, the better I like it – Peter Lynch

Jump to this week’s investment analysis on Hudson Technologies (NASDAQ: HDSN)

Peter Lynch made his name as one of the all-time, greatest investors by diligently researching his companies, taking the time to understand the products and services, and keeping it simple. Investment ideas don’t need to be some complex product or involve mathematical formulae. What it typically comes down to is understanding what you’re investing in and how to properly invest in it. For most, it will be strictly buying equities. For institutions, it may include buying bonds, preferreds, or derivatives. Fundamentally, however, it all comes down to knowing what you’re buying and how you’re buying it. At the end of the day, an investment is in a company run by people and day-to-day processes. Whether they’re fabricating pipe, developing the next AI breakthrough, or mining for gold, it all comes down to decisions made by individuals given the information present at the time.

For many, and this includes some people I’ve worked with in the industry, investing can be seen as a black box. Nothing upsets me more than investing being compared to gambling. Sure, there are many variables that can affect one’s investment that may be out of reach or incomprehensible, but for the sake of argument, it is absolutely not gambling. Many seem to forget that purchasing shares of a company makes you a part-owner of said company. That’s right, you own xxx% of that company. That provides you with the right to vote, the right to cash flows, the right to assets in the instance of insolvency (after creditors have been paid), and for those with significant ownership, the right to direct the company.

It took me years to fully grasp this concept. I remember when starting out, I’d pitch company after company to my portfolio manager with no luck. He would never admit to it, but I’m pretty sure he thought I was a compete haughty dumb shit for the first 6-to-12 months. One thing I learned from him amongst other seasoned buy-side investors is that the most successful investors spend most of their time reading. Not crunching numbers or trading. Reading. As Gordon Gekko famously said in the movie Wall Street “The most valuable commodity I know of is information”. Knowing how things work and why they work is vital to a successful operation.

Anyways, the point that I’m making is know what you’re buying and why you’re buying it. Many of the companies I’ve presented in my investment blog have revolved around long-term growth and dividend income. During a stock picker’s market, owning the stock that sees the most capital gains isn’t always the most feasible option, especially considering the broader market’s performance throughout 2022. Only one industry came out on top and to this day, still remains severely underinvested in. Energy was the only industry that made substantial, let alone any, gains in the stock market. On top of capital appreciation, many of the companies paid out fat dividends in the range of 4-9%. 2023 has been a rocky start for this industry given various dynamics across multiple plains. From geopolitical risks to increased capital investment, Wall Street just doesn’t seem to like energy.

There has been some positive news that was quickly struck down by veto. Both the Senate and Congress essentially agreed to the idea that ESG initiatives should not be a mandate in an investment portfolio. Before I rub someone off the wrong way, I am fully 100% on board with bettering the planet, decarbonizing the environment, and creating safer and cleaner environments for us to live in. That said, as passive investors in the secondary market, it is not our job to make an impact on these initiatives. Buying shares from a zombie company, or one that cannot sustainably operate through cash generated by operations, is a detriment that many investors, both individuals and institutional, have fallen victim to. The only value owning shares of these companies provides is to increase the share price so that management of said company can sell more shares on the open market to raise capital at a more appealing price. That’s it. No more, no less. The only hope you have left as a shareholder is to pray the company doesn’t go bankrupt before their product goes to market and the company is a flat-out scam.

Some examples could be investing in a traditional auto manufacturer like Ford or GM vs. a pureplay EV technology developer such as Lucid Motors or Rivian. Another area is on a more boring front, recycling. One could go with the traditionals, such as Waste Management or Waste Connections, or go with American Battery Technology or Li-Cycle. Personally, I’d typically lean towards the more traditional firms that have existing cash flow and may be a developer or acquirer of the disruptor.

Speaking of recycling, this turned out to the be perfect segway to my investment idea this week. This week’s idea is Hudson Technologies (NASDAQ: HDSN). Hudson Technologies is a very niche, boring company whose industry can be said to be vital to our standards of living. Hudson provides technical services and distribution services for refrigerant chemical across the United States. These refrigerants are typically seen in residential HVAC systems, and in commercial and industrial type functions. Their line of business is constantly being disrupted by policy and regulation as new and safer chemical compounds are discovered to provide equal or greater refrigeration than their predecessor.

One great advantage that Hudson has in their pocket is the push towards more environmentally friendly regulations. Though it may seem counterintuitive, it actually greatly benefits their core operations of recycling and reclamation business. Despite Hudson being in the business of purchasing and marketing virgin HFCs and HCFCs, the margins on these compounds are dictated by the acquisition price and selling price. The ability to market reclaimed refrigerants allows Hudson to have more control over their operations in which costs are dictated by the ability to purchase used refrigerants and the cost associated with cleansing these compounds. Tighter regulation on the production imports of virgin refrigerants will limit the supply on the market and allow Hudson to have more control over the marketing price. By incentivizing customers to recycle refrigerants will also benefit the environment by limiting the release of these greenhouse gases into the atmosphere.

Much of these chemicals, which I will further get into, create O-Zone depleting emissions, greenhouse gases, and are regulated on their global warming potential (GWP). Traditional refrigerants contain a substantial amount of chorine that have been said to severely damage the O-Zone, leading to safer alternatives over the years. If you consider everything that needs to be cooled, from your home, to your vehicle, to an office building, and a datacenter, refrigerants can be found almost anywhere but typically remain behind the scenes.

One of Hudson’s initiatives that they have been very successful in capitalizing on is the reclamation and recycling of refrigerants. Essentially, they’ll take the used refrigerants that have gone through their lifespan and clean and treat them to be usable again. The value Hudson brings to their clients is the on-site speedy transition from old to new refrigerants.

Peter Lynch, being one of the most successful investors in the business ran his book using a variety of rules. Aside from knowing every little detail about the company, he only bought companies at a good value. one common metric that commonly gets overlooked by the most seasoned professionals on Wall Street is the stock’s institutional ownership, or how many shares professional investment managers hold on their books. You might be asking yourself, why would I want to own shares of company that even the professionals don’t own? Well, that and in itself is the reason. As an investor, it is our job to uncover stocks before everyone else does in order to get the most value of ownership. If the shares outstanding are already fully invested in, the shares won’t have as many new corners to paint. If the institutional ownership is relatively low, this means that there is a much longer runway for the shares to move, leading to a run up in share price as interest increases.

As an investment, Hudson’s stock is trading at a deep discount as compared to its respective market. Priced at 3.5x earnings, firm value is a mere 3.14x EBITDA. Industry market comps are trading at 15x earnings with a firm value of 11.75x EBITDA. This level of dispersion isn’t often seen in healthy companies. Judging by the dwindling amount of Wall Street coverage, Hudson was either forgotten about or hasn’t been found. Given the health of their financials, the drastic deleveraging throughout the last 7 years, and their growth potential, this is a once in a blue moon opportunity to buy a company that has the potential to be a multi-bagger (a Peter Lynch term).

Policy

The Montreal Protocol

“The Montreal protocol is a model of cooperation. It is a product of the recognition and international consensus that ozone depletion is a global problem, both in terms of its causes and its effects. The protocol is the result of an extraordinary process of scientific study, negotiations among representatives of the business and environmental communities, and international diplomacy. It is a monumental achievement.” - PRESIDENT RONALD REAGAN - 1988

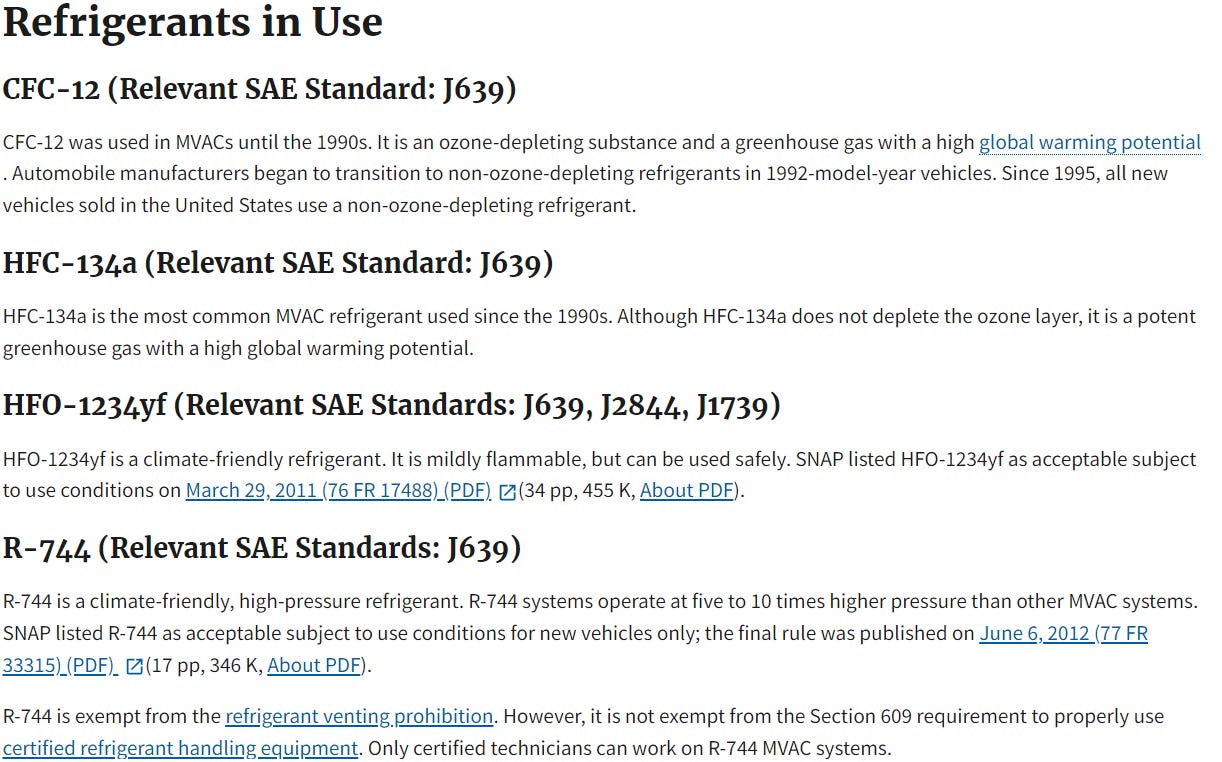

The Montreal Protocol was finalized in 1987 with the intent to protect the O-Zone layer by limiting, reducing, and phasing out the production and consumption of O-Zone-depleting substances. This treaty is a global agreement that became universally accepted and has driven innovation and investment in alternative technologies. The US has been a leader in taking action in reducing these O-Zone depleting chemical compounds, such as chlorofluorocarbons (CFCs). This treaty has also led to the phase down of production of HFCs.

The Montreal Protocol also created The Multilateral Fund that provided financial and technical assistance to developing countries to assist with the phase out. There are four international agencies that manage the activities of the funds: the UN Environmental Programme, the UN Development Programme, the UN Industrial Development Organisation, and the World Bank. Since inception, the Multilateral Fund has provided support for over 8,600 projects across developing countries worth over $3.9b. This includes industrial conversion, technical assistance, training, and capacity development. HCFCs, a commonly used refrigerant that was meant to replace CFCs, are said to produce 2,000x more potent than Carbon Dioxide regarding global warming potential (GWP). CFCs and HCFCs are on track to be phased out through 2030 and replaced with HFCs and HFOs.

Hydrofluorocarbons, or HFCs, were introduced as the alternative to CFCs and HCFCs. HFCs are widely used in air conditioners, refrigerators, aerosols, and foams, among other products. Though HFCs do not affect the O-Zone layer, they do produce a certain level of GWP and are now actively being phased out. Through the AIM Act, the production of virgin HFCs are actively being phased out with production to be limited to 85% of 2014 levels by 2047. The use of HFCFs are being completely phased out by 2030 through the Clean Air Act.

Starting in 2023, according to the AIM Act, new HVAC systems will no longer use R-410A (HFC) and will be replaced with A2L refrigerants such as R32 and R454B. R-410A has been the primary refrigerant for all new residential and commercial air conditioning applications since 2010. These refrigerants are very energy efficient and are capable of absorbing more heat than its predecessor R-22 HCFCs. Like the HCFCs, this HFC will be phased-out in favor of HFO refrigerants. The average life of an AC unit is roughly 10-30 years and should provide users plenty of time to transition without cutting losses on this depreciating asset. In contrast, the price of HFCs may see some increases during the phase-out period as virgin HFCs will no longer be produced.

A commonly used HFC is the R-134a, which is primarily used in automobiles. This refrigerant is used across all classes of vehicles from light to heavy duty. Application of it can be found in heat pumps, chillers, transport refrigeration, and commercial cooling. Due to regulation passed in 2018, only certified 609 professionals have the capabilities to purchase this substance in large quantities. Trade issues have also arisen, further driving anti-dumping tariffs on Chinese produced R-134a.

Through the phase-out period for HFCs, hydrofluoroolefin, or HFOs, will be utilized with a lower GWP. HFOs are said to have a GWP that is 335x less than HFCs and only 4x higher than Carbon Dioxide.

With new technology comes a cost. According to refrigerant HQ, HFO cylinders will cost 5-6x the price of HFCs. Though HFOs are currently being phased-in and not produced at a commercialized rate, only two companies hold patents for the compound, DuPont and HoneyWell. This can pose major problems as stricter transition mandates come to play, especially for the consumer. Though public policy for refrigerants come forth with good intentions, the unintended consequences can sometimes be overwhelmingly burdensome for those it affects.

Be sure to read the full investment thesis on Hudson Technologies on SeekingAlpha. Given the low valuation and long-term runway, this stock has the potential to perform exceptionally well in this inflationary market.

Feel free to reach out with any questions regarding this week’s topic. It covers a lot of ground that many aren’t familiar with and can oftentimes be confusing. I will also review any ideas that have piqued your interest and can help you conceptualize an investment strategy.

Keep reading with a 7-day free trial

Subscribe to ThePeachPit to keep reading this post and get 7 days of free access to the full post archives.