Silver Institute’s Interim Silver Market Review

Silver Institute’s Interim Silver Market Review

From the Silver Stock Investor newsletter | December 2022

This content is made possible through subscriber support. Not a subscriber yet? Click here to see our subscription options or click the button below to subscribe to the full Silver Stock Investor letter.

Every year, The Silver Institute publishes its annual World Silver Survey in April. But in November, that’s followed by a mid-year review which updates the forecast for that calendar year. A couple of weeks back, the Interim Review was presented for 2022, and it’s a whopper.

To start, here are the key takeaways for me:

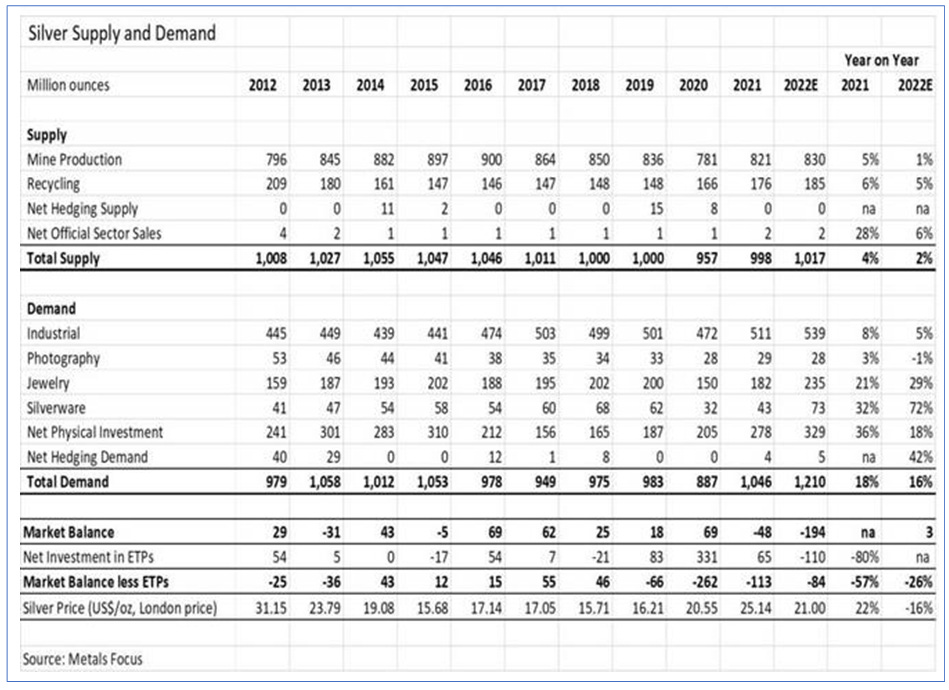

Global silver demand is expected to reach a new high of 1.21 billion ounces this year, an increase of 16% over 2021

Mine supply is only expected to be up 1%, while recycling is expected to be up 5%, with overall supply up just 2%

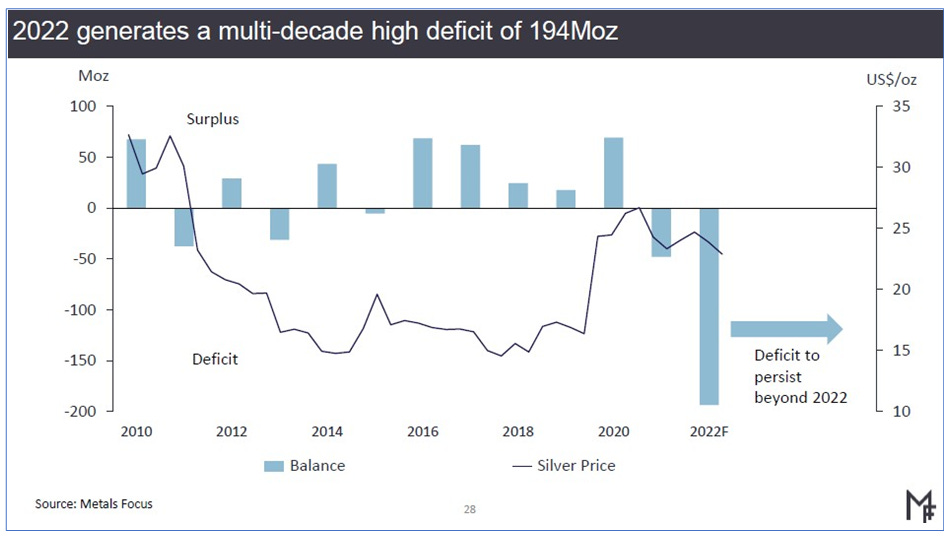

This year will mark a second consecutive annual deficit, reaching 194 million ounces

That’s a multi-decade high and up 4 times over 2021’s 48 million-ounce shortfall

Now let’s pick apart some of the details to better understand how The Silver Institute reaches these conclusions.

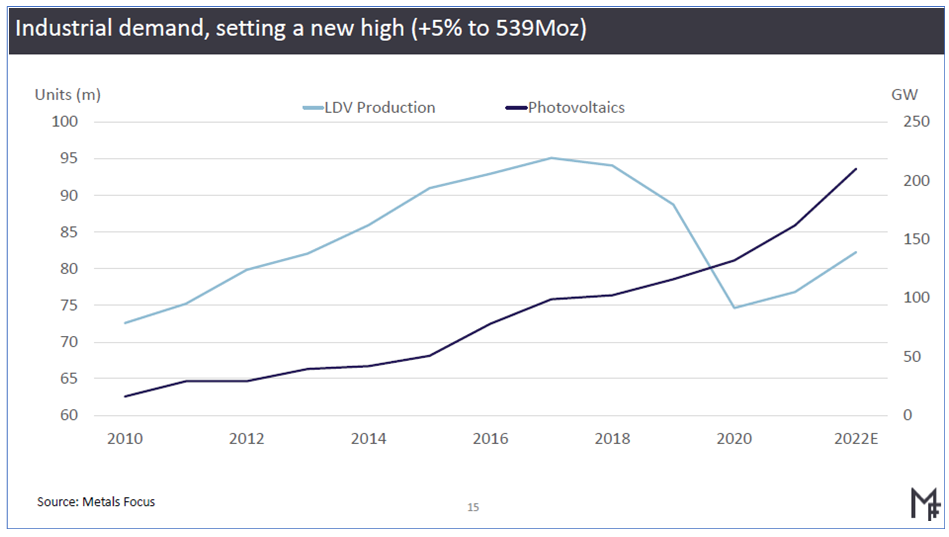

As a whole, industrial demand is expected to jump to 539 Moz, up 6% over 2021. The ongoing green transition is to thank, with ongoing vehicle electrification, the spread of 5G technologies, and governments’ swelling support for green initiatives. The Institute expects industrial demand

strength will make up for potential economic weakness and softness in consumer electronics demand.

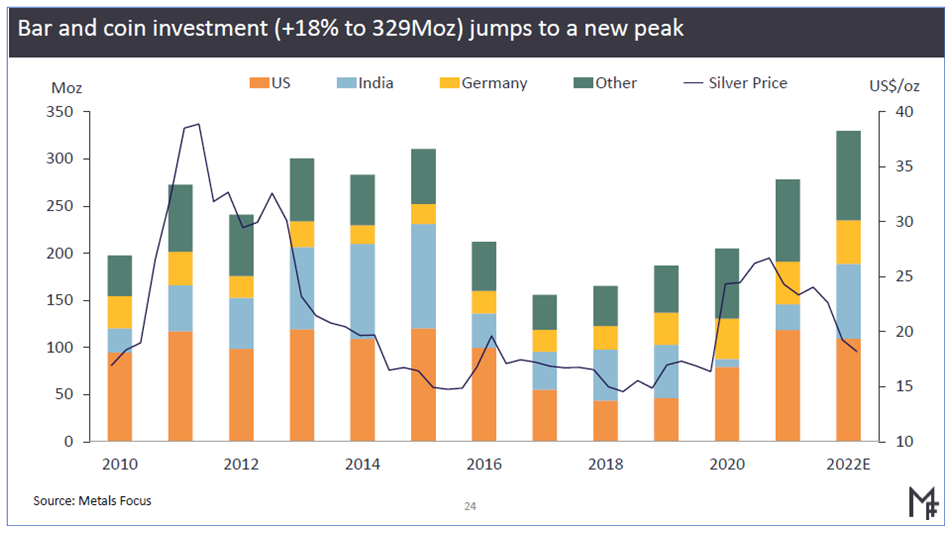

Physical investment is expected to soar by 18% over last year to 329 Moz., setting another record after 2021. This has been revised upward by 50 Moz. over their forecast of 279 Moz. in April. Consider that this is also despite very tight physical markets, with some products in some jurisdictions commanding as much as 100% premiums on certain one-ounce silver coins.

The Institute cites this explosive demand as being driven by fears of high inflation, the Russia- Ukraine war, worries about a possible recession, lack of faith in government, and robust buying on silver price weakness. In addition, demand from India has nearly doubled after plunging last year.

As for Exchange Traded Products (ETPs), also referred to as ETFs, demand is expected to a considerable drop, swinging from forecast growth of 25 Moz., instead to a decrease of 110 Moz. The Institute cites silver’s price volatility as a reason investors have sold and taken profits.

However, this is the first significant drop since silver ETFs were offered in 2006, and may have contributed to spot silver price weakness. It’s likely the decrease in ETF holdings has already played out. However, this is not the same silver that goes into more refined silver coins and bars. And that helps to explain the disconnect between the spot price, and the much higher price for higher grade investment silver.

Metals Focus, who does the research for the annual survey and this interim report, expects silver prices to average $21 this year, down 16% over the 2021 average. They reason that they see the Fed continuing on its rate hiking path, making the US dollar stronger and boosting US bond yields, increasing the opportunity cost of owning silver instead.

As I pointed out in the key takeaways, above, silver from mining (82% of supply) is only likely to rise by 1% or 830 Moz., rather than the 2% forecast earlier this year. Silver recycling, which accounts for about 18% of supply, is expected to be up by 5%, instead of the 4% expected in the April survey for 2022.

Tightness in mine supply has a lot to do with 70% of silver produced as a by-product of other metals, and even some primary silver producers. They expect Mexican and Chilean output to jump as recent silver projects continue to ramp up. But that will be somewhat offset by falling output from other big silver producing countries like Peru, China, and Russia. Silver producers have also suffered from inflation, especially thanks to higher oil and natural gas prices, pushing costs higher.

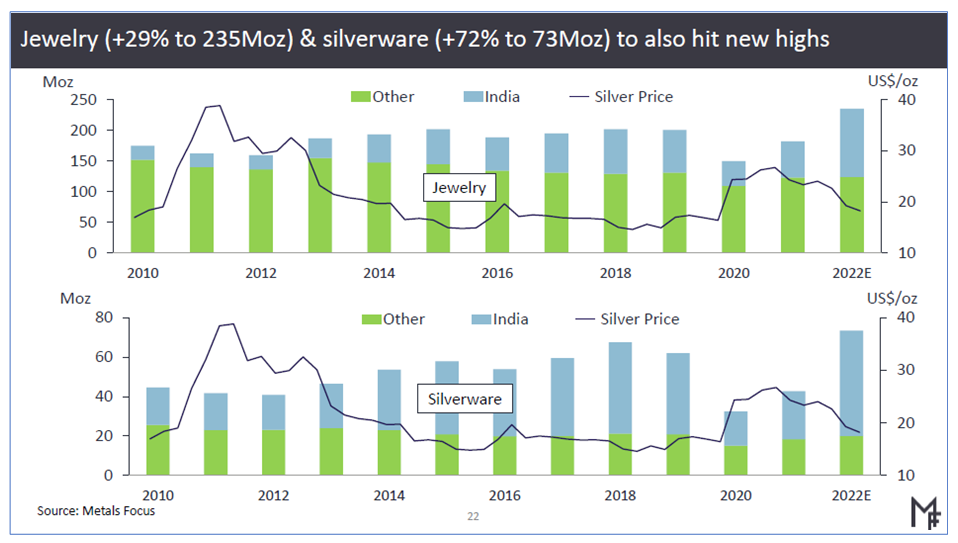

The silver jewelry and silverware sectors are expected to enjoy large jumps of 29% and 72% to 235 Moz. and 73 Moz. respectively, rather than the 11% and 23% originally forecast in April. After last year’s weakness, the massive rebound in appetite from India has led to a need to restock inventories before their late year festive season.

It’s interesting to note the extreme robustness of demand so far this year. In the April World Silver Survey, Metals Focus had forecast a supply deficit of 71.5 Moz. Instead, they are now expecting this year’s shortfall to hit 194 Moz. That’s an astounding 2.7 times, and a serious challenge to the supply side of the equation. I believe a large part of that ballooning deficit is due to soaring silver demand from the solar panel industry.

I’ve explained in presentations that between 2013 and 2021, silver demand from solar output grew by whopping 125%. And in 2021 alone, it was up 13% over 2020. Although the Silver Institute and Metals Focus didn’t single out revised silver demand from the solar panel industry in this recent interim report, I think it’s having an outsized impact. After all, the International Energy Agency (IEA) says solar power represents just 3% of global electricity right now, but that by 2030 it should grow by a whopping 8.5 times!

If solar panels currently consume 12% of annual supply, then by the end of this decade, they could require all of the current annual supply of silver. Naturally, that’s unlikely, because silver is crucial to so many other applications, and it’s highly coveted as an investment too. But this suggests silver prices could rise dramatically on limited supply and soaring demand.

As I said at the outset, the fundamentals for silver look extremely bullish. And this latest update from The Silver Institute and Metals Focus only cements this thesis further.

Demand is expected to be up this year by 16%, while supply is only expected to eek out a 2% increase. And that’s leading to a gaping hole deficit of 194 Moz. for 2022, the largest in decades.

Even if 2023 sees demand moderate somewhat, potentially on the back of Indian stock replenishments, overall demand appears set to grow at a healthy clip, while supply is likely to keep struggling. On that basis, I think 2023 will be another deficit year for the silver market, even if to a lesser degree than this year.

And that suggests silver maintains one of the most bullish profiles of any asset. I’m looking forward to what 2023 could bring for silver and silver stocks.

To see our subscription options, please click here. To subscribe to the Silver Stock Investor, please click the button below.

Add promotional code RESOURCEMAVEN30 during checkout and get 30% OFF!