Boston Omaha & SkyHarbour Earnings (Issue #74)

Boston Omaha & SkyHarbour Earnings (Issue #74)

TL/DR:

New Tool!

Boston Omaha Earnings

SkyHarbour Earnings

Watchlist & Portfolio Updates

Hi all, I am very excited to announce a new tool I built will be launching tomorrow! I am very excited to see what you all think and I will be incorporating it into the newsletters (especially the deep dives). I know it will be a great value add. Look out for tomorrow’s special edition newsletter to find out what it is and how to use it! Subscribe if you haven’t already to get first access:

In the meantime, both Boston Omaha and SkyHarbour Group released earnings this week.

Boston Omaha (NYSE: BOC — $537.19m)

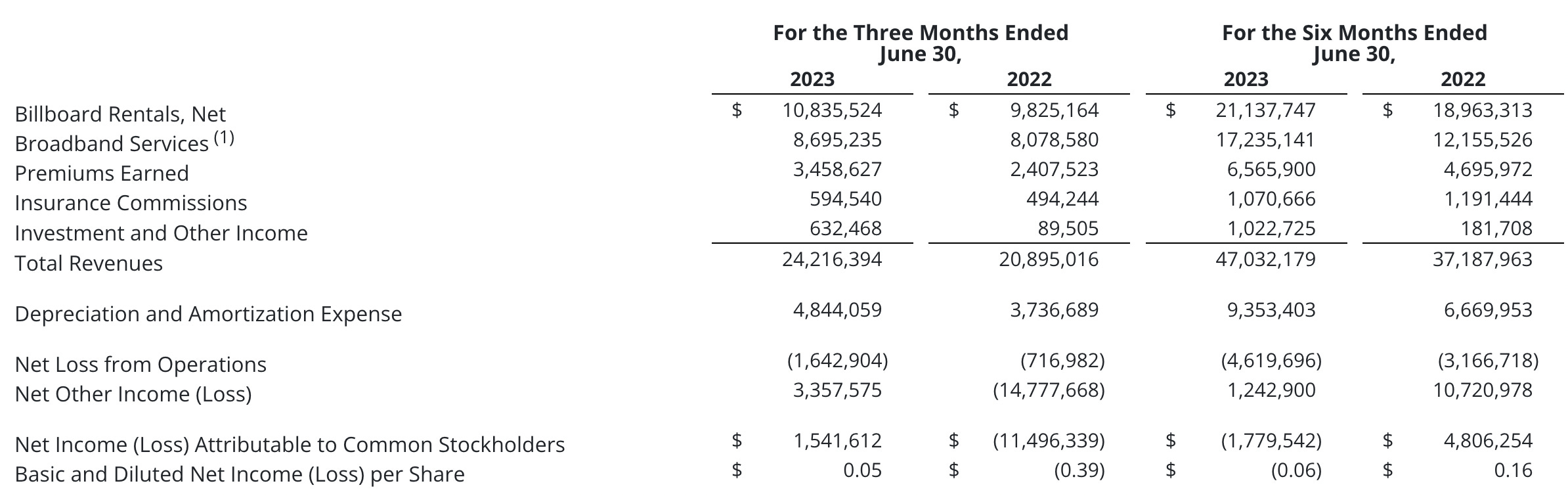

Their earnings are pretty straightforward (for once). All branches saw year/year increase in revenue. Most notably premiums earned grew by ~44% to $3.46m. Meanwhile, billboards grew steadily, and broadband the supposed “growth engine” grew by less than 8%. Insurance has recently been viewed by management as a place where cash gets stuck, however, clearly, it is producing solid returns. For broadband, while it did not grow significantly this quarter it had strong growth throughout with year so far growing from ~$12.2m to ~$17.2m in the first 6 months of 2023.

Boston Omaha also grew assets by ~$85.4m with ~$36m being unrestricted cash and investments. Now total assets is ~$773m

Broadband is my biggest focus going forward so the development of their current and future revenues will be something to watch. I am also curious to see how billboards and insurance, two of the legacy branches of Boston Omaha, evolve with growth as other parts of the company become more meaningful and focal points.

SkyHarbour Group (NYSE: SKYH — $255.48m)

SkyHarbour is a bit less straightforward than Boston Omaha. Their revenue was $1.7m for the quarter a massive increase from $409k Q2 2022. This is also 56% growth from Q1 2023.

“As of June 30, 2023, cash, restricted cash, and US Treasury investments amounted to approximately $150 million”

SkyHarbour Group 8-K

SkyHarbour bought a pre-engineered metal building manufacturing company during Q2. This should help in the construction process of multiple sites. Phase I for Phoenix and Denver are in action and Dallas is in pre-development for Phase I. All these should be completed during 2024. Also:

Houston 94% leased

Nashville 64% leased

Miami 71% leased

The company expects to be fully leased for those locations by Q4. In addition, Negotiations are in the works for new ground leases at six key airports. The average projected rents of these are expected to exceed the rent from the first six campuses. This would add 1.5m SQFT to the SkyHarbour foot print. Half of these leases are expected to be signed by Q4 and the rest by Q2 2024.

““The Sky Harbour team’s energies remain focused on the dual objectives of 1) maximizing unit economics and 2) aggressively pursuing scale.”

Tal Keinan SkyHarbour Group CEO

These are promising results for SkyHarbour so far. There is still a lot to come. One concern as a warrant owner in addition to common shares it that the managers call the warrants at $10 per share as mentioned in the prospectus. I think we may see more rallying once the new leases are officially secured, as revenue continues to go, and when the Phase I’s construction are completed throughout 2024.

Watchlist Updates:

Portfolio Updates:

To access the full spreadsheets and linked deep dives go here.

Until Tomorrow,

Soren