Valuation: Story Meets Numbers (Issue #75)

Valuation: Story Meets Numbers (Issue #75)

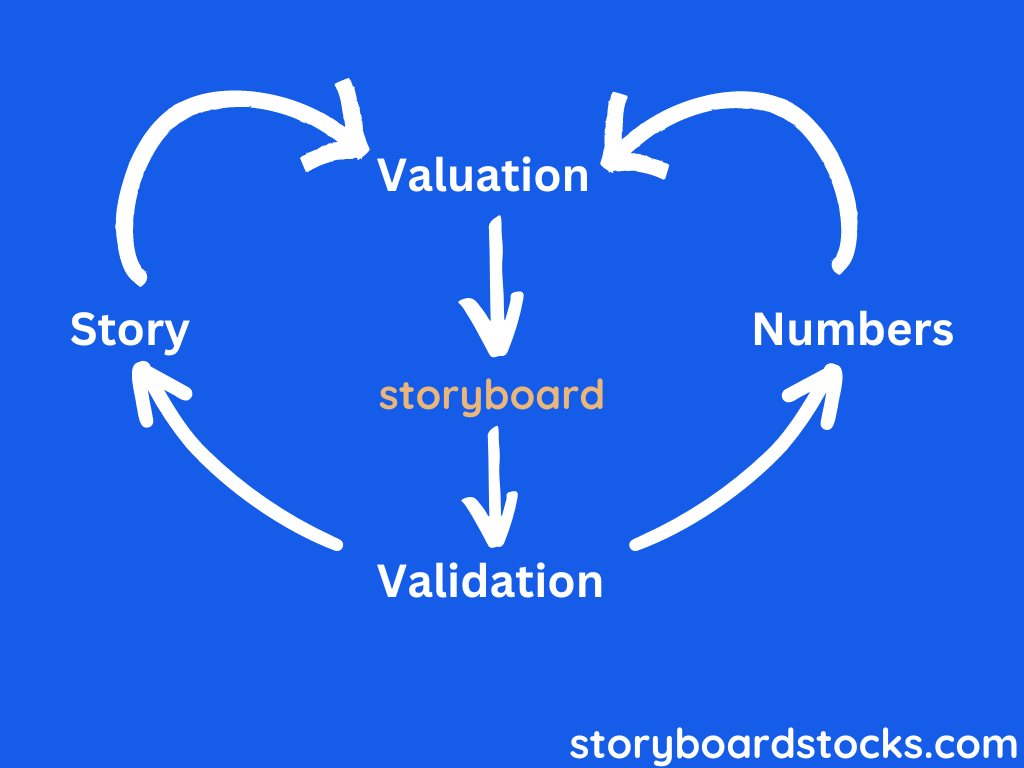

“Valuation is a bridge between stories and numbers.”

Aswath Damodaran

Welcome To StoryBoard! Today is the official launch of a valuation tool that bridges the gap between stories and numbers. Connecting the two gives us as investors a chance to better understand the companies we are researching. All too often we focus on the numbers without adding meaning to them. Numbers for the sake of numbers are not useful in the analysis process, only numbers with matching stories are useful.

Aswath Damodaran observed that valuation is a bridge between a story and numbers. There are literally thousands of tools to track and refine the numbers side of investing, but next to zero, that create structured stories. Valuation projection numbers are guaranteed to be wrong, but the story can be right. So I choose to weigh them more evenly. That is why I built Storyboard.

Storyboard’s mission is to link these four elements together and help investors make and continue to make better investment decisions. Linking the story to the numbers establishes a clear benchmark, this helps investors find out if they are on track, underperforming or overperforming.

A critical factor in investing is that the valuation will be proven right or wrong only over time. That means that the valuation used to bridge the two needs a way to track how reality diverges from the model and its assumptions: were the estimates too high or too low? Did management execute in a way that supports or changes the assumptions? There are many questions to track over time, but these are usually done only by tracking numbers. Tracking numbers to validate ongoing investment is a necessary, but insufficient approach. A numbers-only validation misses major changes in the investment operations and may break the valuation model, think of spinoffs, M&A, entering new markets, and taking on debt as examples. Even absent dramatic changes, the numerical validation should be linked to the progression of the goals in the investment story to show which parts are strengthening, weakening, or under threat.

Numbers show what happened in the past, and they can project into the future, but they do not show the company’s story and whether the story is weakening, strengthening, or changing. The future returns that made Amazon such a success were not in any of its e-commerce numbers, it was in the changing story from eCommerce to Cloud to platform. Stories are how companies grow and die. Knowing the difference is the difference between investing success and failure.

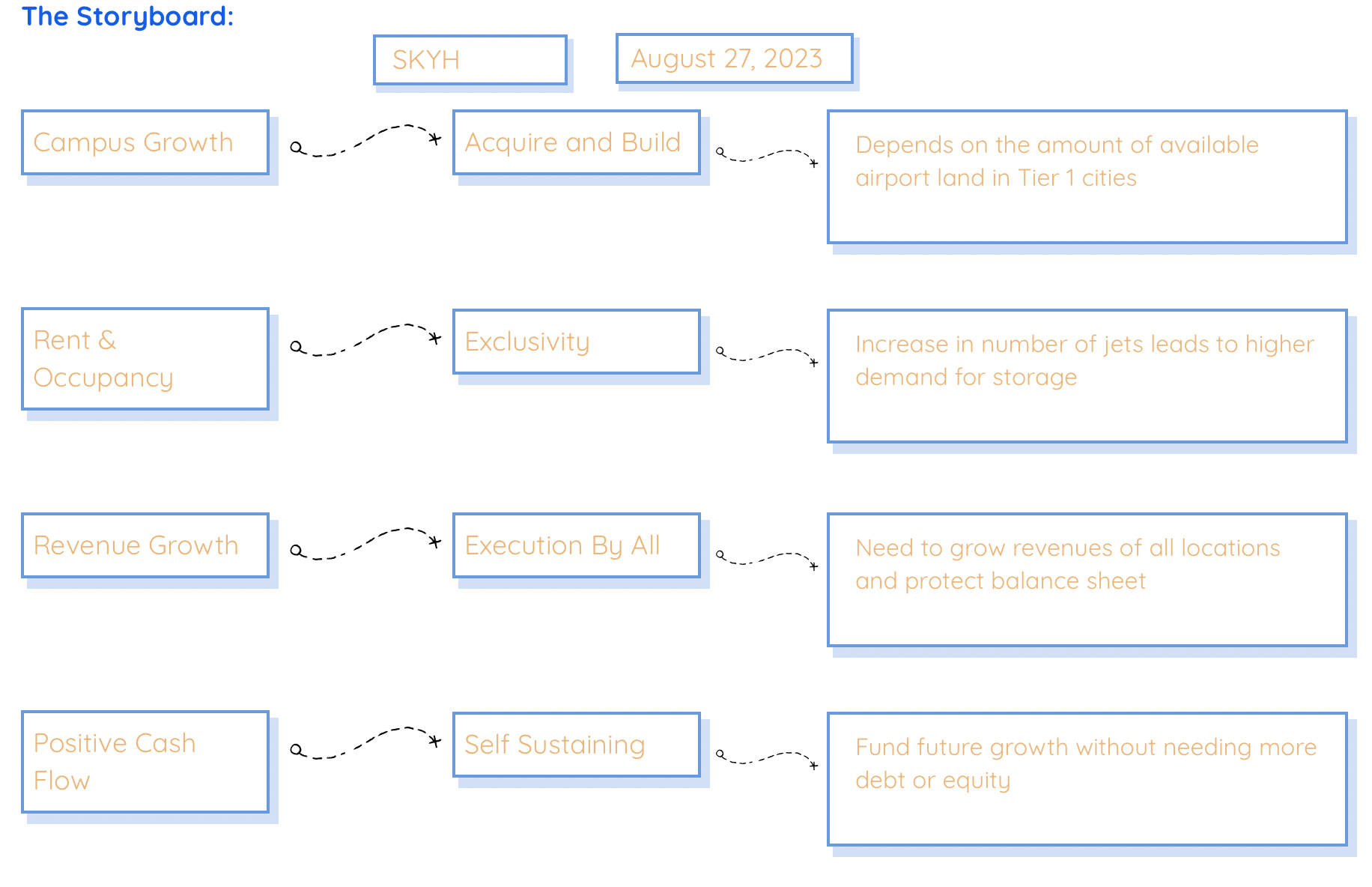

Example- Let’s dive into the SkyHarbour story.

SkyHarbour Group is the definition of a story stock.

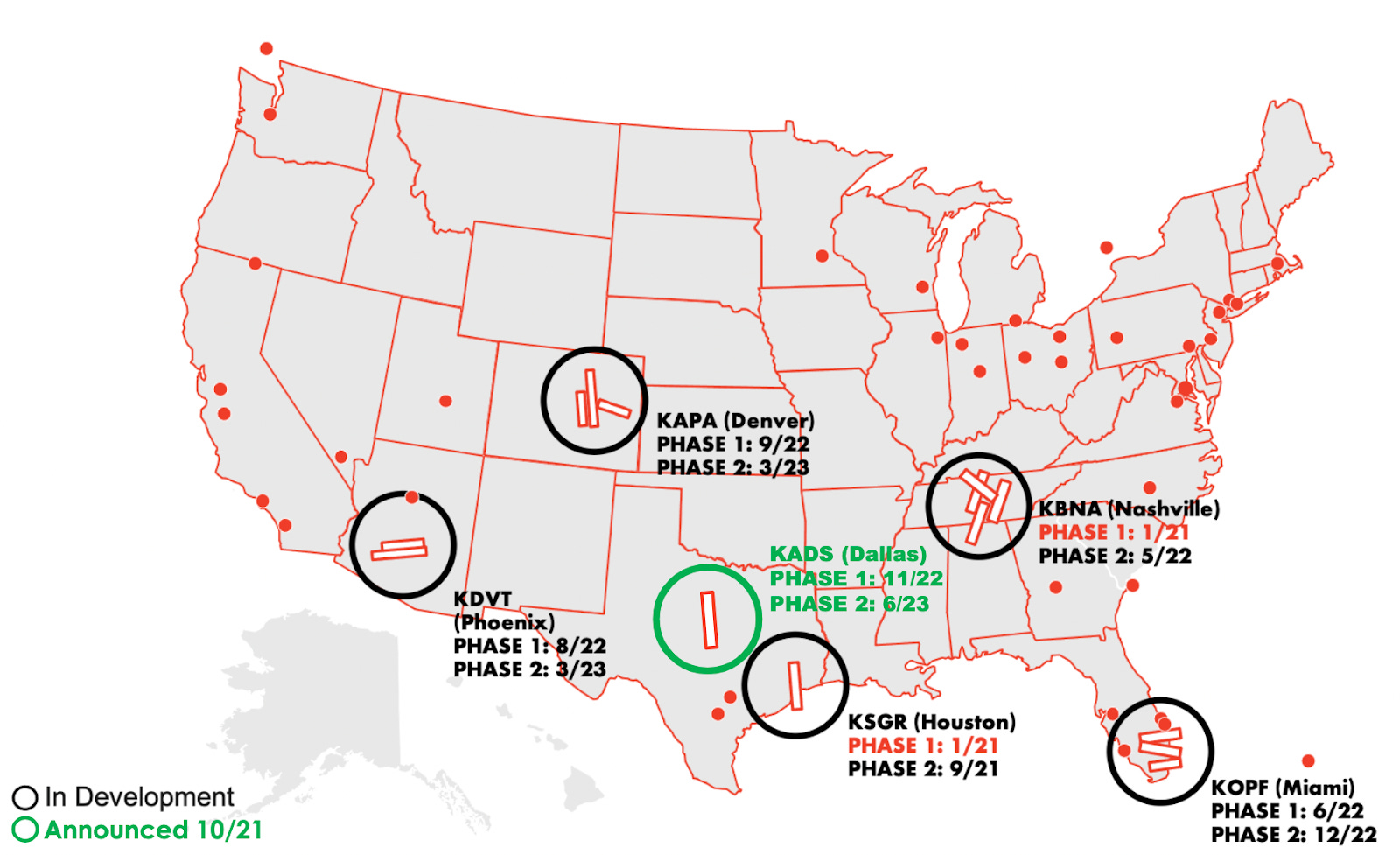

SkyHarbour builds and leases private airplane hangars to private jet owners, mainly focused on jets owned by companies. The company started when Tal Keinan, a former Israeli fighter pilot, noticed that while companies made very large investments in private jets as critical corporate assets, they lacked quality, accessible hangar space to make full use of the assets. The rapid growth in private jet ownership and not much growth in hangar space to house them creates the opportunity for Sky Harbour to build its niche. It operates in many ways like an early-stage specialty REIT (though it is not structured as a REIT today) and is actively building its base of hangars at 6 airports in the US where they will have campuses. The campuses are built in Phases with most Phase I’s set (Nashville, Phoenix, Dallas, Denver, Miami, and Houston) to be completed by the end of 2024.

Some look at Sky Harbour’s numbers and see the potential for exorbitant returns from warrants on paper, others look at the currently low revenues and have no faith in the company. As an investor in the company, both of these overly precise calculations are likely to be proven wrong over time or at least incomplete. Neither of them incorporates the context of the story. They don’t show the entire picture. Instead, it is like trying to figure out where you are on an ocean journey by looking only through a porthole.

Like every IPO company, when SkyHarbour launched it filed a glossy S-1 document with a great story to tell. Now, the SkyHarbour story is being put to the test in the real world. Thinking through the essence of the future possible, plausible, and probable outcomes of these decisions is the essence of investing. These can be only partially represented in numbers.

One measurement of SkyHarbour’s progress shows that many of the company’s revenue projections have been behind original estimates. On top of that some construction projects were delayed due to supply chain factors outside the company’s control. But stories are not static, SkyHarbour responded to these challenges by taking more direct control of the construction and development projects. Investment is about the future. Its project pipeline and development execution going forward will determine much of its near-term revenue opportunity. The company continues to sign more ground leases and plans expansion to more cities are in the works. Understanding the company’s story, how it evolves, and tracking progress is the way to uncover hidden value.

“Nothing is ever as good or as bad as it seems”

Jeff Galloway

Opportunity

Private jet sales growth continues to outpace hangar growth. Most US airports are run by municipalities that lack the incentive to run costly expansion projects to address the private jet storage gap. This creates an increasingly high demand for jet storage. SkyHarbour sees their total addressable market (TAM) at 50 airfields in the US. Each airfield can have multiple stages or phases of SkyHarbour campuses each comprising multiple hangars. The company is further advantaged by using their quality of service as a competitive advantage. Most air care in the US is subpar service and extremely inefficient. SkyHarbour works to provide the best service and most efficient experience.

“If your company owns a $50 million business jet. We think most people who are in that situation place a very high premium on time.”

Tal Keinan, SkyHarbour CEO

Return Profile

Building Block 1 - The Unit Story

SkyHarbour’s unit economics are comprised of rentable square feet in hangar space, the price per square foot it rents at, the hangar occupancy rate, and its development and operational costs. On a unit level, SkyHarbour aims to earn double-digit net operating income yields. Meaning they have unit profitability and efficiency.

The proof is always in the pudding of how well this theory works in practice. There are three SkyHarbour airports that are fully operational today. So far two SkyHarbour campuses (Miami-Opa Locka and Nashville) have produced over 30% return on project equity. It is proof of the potential for large returns on a per-unit basis.

Building Block 2 - The Corporate Story

This unit economics are important to show that each airfield can earn a return to justify its place in SkyHarbour’s portfolio. However long-run returns for the company rely on scale and operating leverage. Going forward, there are over 20 new airfields to construct and lease for SkyHarbour to lease, build, and rent at attractive prices to sucessfully prove out its market growth story. Can the company walk and chew gum at the same time? For a development company with aggressive TAM to go after, can Sky Harbour develop 20+ more airfields while also operating more airfields, and at the same time maintain cost control discipline? On a unit-by-unit basis, development work may be front-loaded until each hangar build-out are complete, but there are years worth of building ahead of SkyHarbour. On top of this, unit level operational work will at least scale linearly with size. SkyHarbour's operating leverage storage needs to prove that some system-wide fixed costs are diluted with size.

Looking forward, SkyHarbour believes it will be able to build to a target of around 20 sites (including existing) without any additional fundraising. This will help them achieve most of their short-term projections as they grow into their TAM.

Building block 3 - The Investor Return story

To the extent that SkyHarbour can deliver on the operating leverage story, the company can generate meaningful recurring cash flows over time. This margin can be used to fund further expansion, which puts the company in control of its own destiny instead of the whims of capital markets. From there, cash flows can be used to pay investors dividends, or participate in buybacks.

As the company matures, the long-run return profile may in fact look like a specialty REIT paying out predictable, safe, and growing dividends. This will depend on many factors including how sticky customers are, company pricing power on rents, growth within the existing base, and overall development and operational risk management.

Execution

Tracking the pipeline from the start begins with dirt. On ground leases, SkyHarbour is in exclusive negotiations in multiple cities for space that can double its rentable square footage.

From the ground to operations is about development. When SkyHarbour went public through the Yellowstone Acquisition Company (SPAC) there were 6 locations/campuses in development. Now there are 3 locations operational with Houston at 94%, Nashville at 64%, and Miami at 71% leased. The following three other campuses are set to all be completed by the end of 2024 these include Denver, Dallas, and Phoenix. There are also site expansions to the existing campuses in the planning and permitting phases. The company is receiving a little over $27 per SQFT in existing leases. This number is expected to increase.

Over time revenue is probably not the most effective number to track SkyHabrour’s business, but it is one useful way to monitor early stage progress. Development progress has encountered some headwinds with projects taking longer to complete. The company fell far short of their projected ~$5m in revenue for last year. They are also on track to miss this year’s projections with $1.7m in revenue in Q2 2023 not even close to the $17.6m projected for the year from the IPO Investor Presentation. For this, I will be watching to see how it changes as more hangars are rolled out and how the potential new ground leases can add to revenues in the future. For now, SkyHarbour’s execution remains well behind the numbers envisioned at IPO time.

Pricing is an important factor in the SkyHarbour story. Because it is a new type of business niche, there is a lack of comparable data. A REIT that rents strip mall space can readily attain highly accurate rental rates to base its business on. But there is no simple precedent for a company renting hangar space across the US. This makes price per square foot and occupancy rates, very important pieces of the early stage SkyHarbour story to monitor. For Price/SQFT SkyHarbour reported this week that it has seen it can produce ~$45 per SQFT on new leases. Previous estimates accounted for closer to ~$38. This should help them get closer to their future projections. Already the Houston, Nashville, and Miami facilities are at 94%, 64%, and 71% capacities (respectively).

Headwinds

As a new company in a new space, there are several structural risks to SkyHarbour’s story that can cause them to underperform expectations. If and when construction difficulties in the form of extended timelines or increased costs occur is a prime example of a very current risk. Investors should closely track the time it takes to acquire new ground leases, what type of city are they in (Tier 1, 2, 3), how long it takes to go from ground lease to operational, and how long it takes to be at or near full capacity of rented.

Similarly, pricing power is an unproven assumption at this point, SkyHarbour has made the point that it is selling into less cyclical markets due to its focus on corporate-owned jets, and that this combined with the pain point of low availability and lower quality hangar space availability will translate into sustained higher prices. This needs to be proven out in the marketplace. And if this optimistic scenario is the case, will SkyHarbour attract competition in the space?

On the financial side, SkyHarbour went public in the era of easy money and low-interest rates, since its IPO there has been a sea change. SkyHarbour was fortunate to secure its bond issue at large size during a time of generationally low-interest rates, but when it needs to tap debt markets again, there is a good chance of increased interest rates on new debt needed to fund the additional developments.

A knock-on effect is that when SkyHarbour went IPO and issued bonds to raise capital they included comparison companies. These were an assortment of specialty REITs that at the time were trading at 25-30x Price/FFO since then they have fallen to the teens. This doesn’t bode well for reinforcing a high valuation for them. Investors should revisit assumptions on how to value cash flows over the long run in a higher rate environment and choose scenarios from a range of possible, plausible, and probable cash flow valuations.

Finally, the last clear risk looking forward would be justifying the expense and absorbing the cost of Rapidbuilt. The acquisition should help with construction efficiency and effectiveness, but the cost is still significant and it will be important to see how the purchase affects construction and development costs.

Tailwinds

There are some ways that SkyHarbour can perform better than expected. For example, they may see a meaningful decrease in construction costs now that they have purchased Rapidbuilt a pre-manufactured construction company. Another way to outperform would be if the company’s execution ability with occupancy, rental rates (price/SQFT), or other metrics were optimized. There has already been evidence of successful execution at the Miami and Nashville campuses.

So far the balance sheet has plenty of capital to fund development and most of it is held in treasury bonds, This will be increasingly powerful with multiple options to financing the new efforts towards the planned new airport developments.

The company is excited about the next 6 new airport negotiations with half of them expected to close deals on ground leases by the end of the year and the rest by Q2 of next year. In addition, 5 of the 6 are what SkyHarbour classifies as Tier 1 markets with the last being a Tier 2 market. As a reference point, SkyHarbour views Miami as a Tier 2 market. This means the 5 other contracts could be of significant size and value if/when they close. So far the average cost for development has been between $45m-$60m meaning these new contracts combined would cost between $275m-$350m. Historically, only 40% of these deals have been financed with cash. Therefore, SkyHarbour would be on the hook for ~$100m for all of these deals, with the remaining ~$200m being financed through debt or equity.

Looking Forward

Stories are built on assumptions of how things will unfold. The best story in the world does not matter if there is not execution to deliver. Ultimately, the story shows the path and the numbers prove the results. Since investing is about the future, context from the story is essential to know what measures matter when. For SkyHarbour, the first 6 campuses are expected to have completed at least Phase I by the end of 2024. This means 2025 will be the first full year at this next level of scale, 6 base campuses, making 2025 an important inflection for the company to demonstrate results. Beyond this, there are still 4 Phase II’s in process or yet to break ground that will continue the growth. The company announced negotiations on six additional cities for ground leases that if successful will further expand its development pipeline. This will be a chance to prove long-term projections for rentable square feet, number of hangars, and number of campuses.

Accounting statistics only show a surface-level view of the company. In order, to track the true story of SkyHarbour it takes a bit more effort. If SkyHarbour’s story plays out then we will see a flow of new ground leases, followed by efficient development of airfields in well chosen locations coming online, followed by a continually high level of occupancy at each campus at profitable prices. There are risks at each of these steps. Will the company be able to develop, operate, and scale in parallel as it matures? This cycle allows me to easily track the story at multiple key points.

There is only one guarantee with a valuation projection or future estimate, is that it will be wrong. However, this doesn’t mean that valuations are not important or useful. There are two parts to every valuation, stories and numbers. Most focus simply on the numbers. The numbers are guaranteed to be wrong, but the story can be right. So I choose to use the context of the story to choose the right number at the right time and weigh them more evenly.

This was the first StoryBoard style story (bridging story and numbers). I will be continuing case studies and analysis in this style. I think it is a more comprehensive and accurate lens to look at businesses. There are forums on the site for you to share your own stories and ideas. I am excited to see what people think of the tool. This is still very much in development with adjustments and additions to be made so please reach out with any suggestions or questions to me at pillarsandprofits@gmail.com.

Until Sunday,

Soren

Your mobile website is all over the place. Unuseable on mobile.