On the Prowl for A Molecule - But at What Cost?

On the Prowl for A Molecule - But at What Cost?

Inside Japan's hydrogen industrial strategy

Japan is on the prowl for a molecule. A molecule that can decide the nation’s energy future. A molecule composed of two hydrogen atoms.

Toshiba and Toray are developing new technologies that would reduce the cost of producing green hydrogen. Panasonic too. Kansai Electric is considering buying hydrogen from Canada. A Japan-Australia joint venture set in motion the first steps toward a hydrogen supply chain. Hydrogen was on the agenda when Prime Minister Kishida visited Saudi Arabia and the UAE. The first hydrogen fuel station for taxis in Japan began opened for business. All of these things happened in the last five months.

Japan’s push for hydrogen is industrial policy par excellence. Industrial policy is the use of a set of policy tools to support particular industries that the state deems are strategically important.

In the post-Cold War western world, where free markets are ostensibly the norm, the term had an unfamiliar ring. Recently, industrial policy has returned. This time, it’s in the form of “green industrial policy,” the herculean effort to turn the massive ship of the fossil-based energy system to a low-carbon one. Japan’s fossil fuel ship is particularly massive — nearly 85% of the country’s total primary energy came from fossil fuels in 2022. Hydrogen is one of a whopping 14 sectors that the Japanese government has identified as “promising fields that are expected to grow” and are crucial for turning that ship.

Japan is no stranger to hydrogen. Public and private hydrogen initiatives have been ongoing in Japan since the 1970s. But what is new is the focus on hydrogen as a Swiss army knife of the clean energy transition and as a centerpiece of a national level industrial policy. The Japanese Ministry of Economy, Trade and Industry (METI) put out a Strategic Roadmap for Hydrogen and Fuel Cells in June 2014, outlining quantitative targets for cost and scale of hydrogen use. Three years later in 2017, a comprehensive Basic Hydrogen Strategy introduced more quantitative targets for 2020, 2030, and the “long-term perspective of around 2050.” It’s the document - first in the world of this kind - that embodied the government’s approach to developing the hydrogen industry.

Finally, in early June this year, the Japanese government published an updated version of the Basic Hydrogen Strategy.

What is in the latest Strategy? How will it fare? At what cost?

Basic Hydrogen Strategy

In Japan, energy is among METI’s uniquely wide policy portfolio. METI shapes energy policy by convening committees of experts, usually drawn from industry and academia, to discuss overarching policy strategies. These committees craft policy proposals, which are then submitted them to the Prime Minister’s Cabinet and the national legislature. In a polity where politicians of the dominant Liberal Democratic Party permeate the upper echelons of the bureaucracy and the executive and legislative branches, these proposals often become law without quarrels. That’s Japanese politics in a nutshell — part democracy, part bureaucracy.

The Basic Hydrogen Strategy is one such proposal. It sets out the elites’ thinking around the role and uses of hydrogen in the energy transition, and sets targets and timelines. In April last year, METI reconvened the committee of 21 senior politicians and heads of the ministries and gave it an insipid title that inspires yawns and glazed eyes — Ministerial Council on Renewable Energy, Hydrogen and Related Issues. The committee met twice, and on its second meeting on June 6, published the updated 42-page Basic Hydrogen Strategy.

Compared to the US and Europe, where solar, wind and EVs do the heavy lifting of decarbonization, the hype around hydrogen is much more visible in Japan. This commercial by Kawasaki is just one of many ways that big industrial players are hoping to get public buy-in around their hydrogen engineering efforts.

Government policy corresponds to the hype. The Kishida cabinet hopes to direct over ¥15 trillion (USD 106 billion) in private-public investments over the next 15 years to bolster hydrogen use in the country.

Why Hydrogen?

The headline benefits of hydrogen are by now well-known. It’s a combustible fuel that doesn’t emit greenhouse gases (GHGs). It’s a medium that can store energy for longer periods than the typical battery can. It’s a versatile energy source that can, in theory, be used to generate electricity, heat buildings, power vehicles and produce industrial chemicals.

As a country perpetually concerned with its resource scarcity and energy security, Japan finds hydrogen especially alluring. It’s conventional wisdom among Japanese elites that aggressive deployment of renewables is impossible because of the country’s land scarcity and mountainous geography. As a source of clean energy that not solar or wind, hydrogen is seen as a central pillar to Japan’s climate goals. Hydrogen can be made from a variety of sources — renewables or fossil fuels (put a pin in this — we’ll talk more about this) — and in regions outside of the oil- and gas-exporters that Japan relies on so heavily. Because hydrogen can act as an energy carrier, Japan can partner with countries rich in renewable energy and effectively “import” renewable electricity from abroad. Put another way, Japan can “outsource” renewable energy generation through hydrogen.

Plus, hydrogen can be used as an industrial feedstock, rather than simply as fuel. This means it can be used in a sweeping array of economic sectors.

Finally — and this is paramount — Japan has a head-start in the key technologies that produce and turn the molecule into coveted fuel: fuel cells.

The Ambition: “Hydrogen Society”

The Hydrogen Strategy aims to capitalize on all of these advantages. Most importantly, the government wants to reduce the price of hydrogen so that it’s competitive with the price of liquefied natural gas (LNG) today. By 2030, it hopes to get hydrogen down to ¥30 per Nm3 and by 2050, ¥20 per Nm3 (the Strategy points out that in March 2023, LNG was ¥24/Nm3 in Japan).

Policymakers hope that this price reduction will be brought about by a massive increase in hydrogen consumption. The Strategy proposes that, by 2030, the entire economy should be using 3 million tons of hydrogen. By 2040, 12 million tons. And by 2050, 20 million. These figures supposedly also include the use of ammonia, but the breakdown between hydrogen and ammonia isn’t given.

The Demand Side

How will all of this hydrogen be used? The Strategy envisions that sectors across the economy — electric generation, transportation, manufacturing, metals, chemicals, households — will be run on hydrogen.

For the electric generation sector, the Strategy hopes that large power plants will be able to run on 30% hydrogen (and the rest natural gas) by 2030. Co-firing of ammonia with coal is currently being piloted at 20%. Government hopes this figure will reach 100% in the future. The remaining CO2 emissions in meantime, it reassures us, will be sequestered through CCUS.

In transportation, putting 800,000 fuel cell vehicles (FCVs) on the road and building 1,000 hydrogen refueling stations by 2030 is the goal. The government also hopes to use Japan-made fuel cells in freight and passenger trains, domestic shipping, residential, commercial, and industrial buildings. It goes as far as saying “we will secure the top place in the global market by creating a condition in which Japanese fuel cells are ‘everywhere, all time.’” (p. 16)

In industry, it envisions that hydrogen will be used as feedstock, reducing agent, and fuel in the cement, metals, and chemical manufacturing sectors. Ammonia, that hydrogen carrier and a non-GHG emitting molecule in its own right, is heavily featured as a fuel and raw material for many applications.

The faith and responsibility that the Japanese state places on these molecules is tremendous. “Hydrogen Society” - that’s the government’s buzzword epitomizing this vision.

The Supply Side

If the vision for hydrogen use has implications for society inside of Japan, the government’s plans for the hydrogen supply chain may alter the geopolitical landscape.

In the words of the Strategy, a “large-scale and resilient” supply chain will need to be built to mass produce and transport the hydrogen to the home market. The government is aiming for ¥15 trillion ($105.9 billion) of public-private finance to be directed toward this endeavor over the next 15 years. Funding is to be deployed from public institutions like JOGMEC, Japan Bank for International Cooperation, Development Bank of Japan, Nippon Export and Investment Insurance, and the yet-to-be-established GX Promotion Organization. These will be supplemented by spending funded by Japanese Government Bonds worth $60 billion. Government coffers will be thrown open.

Recall one of the advantages that Japan sees in hydrogen — that it can be produced in resource-rich countries and shipped to Japan as an energy carrier. This is where Japan’s ambition to build a hydrogen supply chain may impact the political economy of energy far beyond the island nation. Much of the funding planned for the supply chain development will be directed overseas, where Japanese firms partner with foreign counterparts to build infrastructure for hydrogen production and transport.

Recall one of the advantages that Japan sees in hydrogen — that it can be produced in resource-rich countries and shipped to Japan as an energy carrier. This is where Japan’s ambition to build a hydrogen supply chain may impact the political economy of energy far beyond the island nation.

This outward-looking portion of the hydrogen industrial policy is well underway. In 2017, four major Japanese infrastructure and trading firms began the world’s first demonstration project to transport hydrogen from Brunei to Japan. The infrastructure needed to transport the natural gas-derived hydrogen to Japan was completed in December 2020, and the first shipment was made in February 2022.

In 2018, Kawasaki Heavy Industries began a joint construction of a coal gasification demonstration plant in Victoria, Australia, with electricity producer AGL. Just a few months ago, the project received a financial boost from the Japanese government’s Green Innovation Fund (I hope the irony’s not lost on anyone).

On the ammonia front — a fuel in its own rights but also a hydrogen carrier that’s much more convenient to transport and store than hydrogen itself — Japan and Saudi Arabia has been in talks for a while. Way before Kishida visited the Arab kingdom, delegations from the two countries held symposiums in 2017 to discuss hydrogen and ammonia production. Japan received the first cargo of ammonia from Saudi Arabia this past April.

Needless to say, all of this requires enormous state intervention. Many of the technologies that would make up this supply chain (electrolyzers, pipelines and ships appropriate for hydrogen transport, the carbon capture technology to justify fossil fuel-based hydrogen production) as well as the demand side (hydrogen gas turbines) are still in their early stages. Government and publicly supported institutions are ready to back these ventures with grants and insurance.

On the diplomatic front, the Japanese government is busy signing bilateral agreements with countries near and far to build the supply chain for domestic hydrogen consumption. These diplomatic efforts provide the economic certainty that private companies need for long-term investments. In so doing, it also hopes that Japan’s hydrogen-related technology will be the gold standard everywhere.

Running Fast Down the Wrong Path

There is no doubt that Japan is running fast to reinvent itself as a Hydrogen Society. But there are many reasons to be worried that it’s tumbling headlong down the wrong path. I’ll just touch on one of them here: GHG emissions.

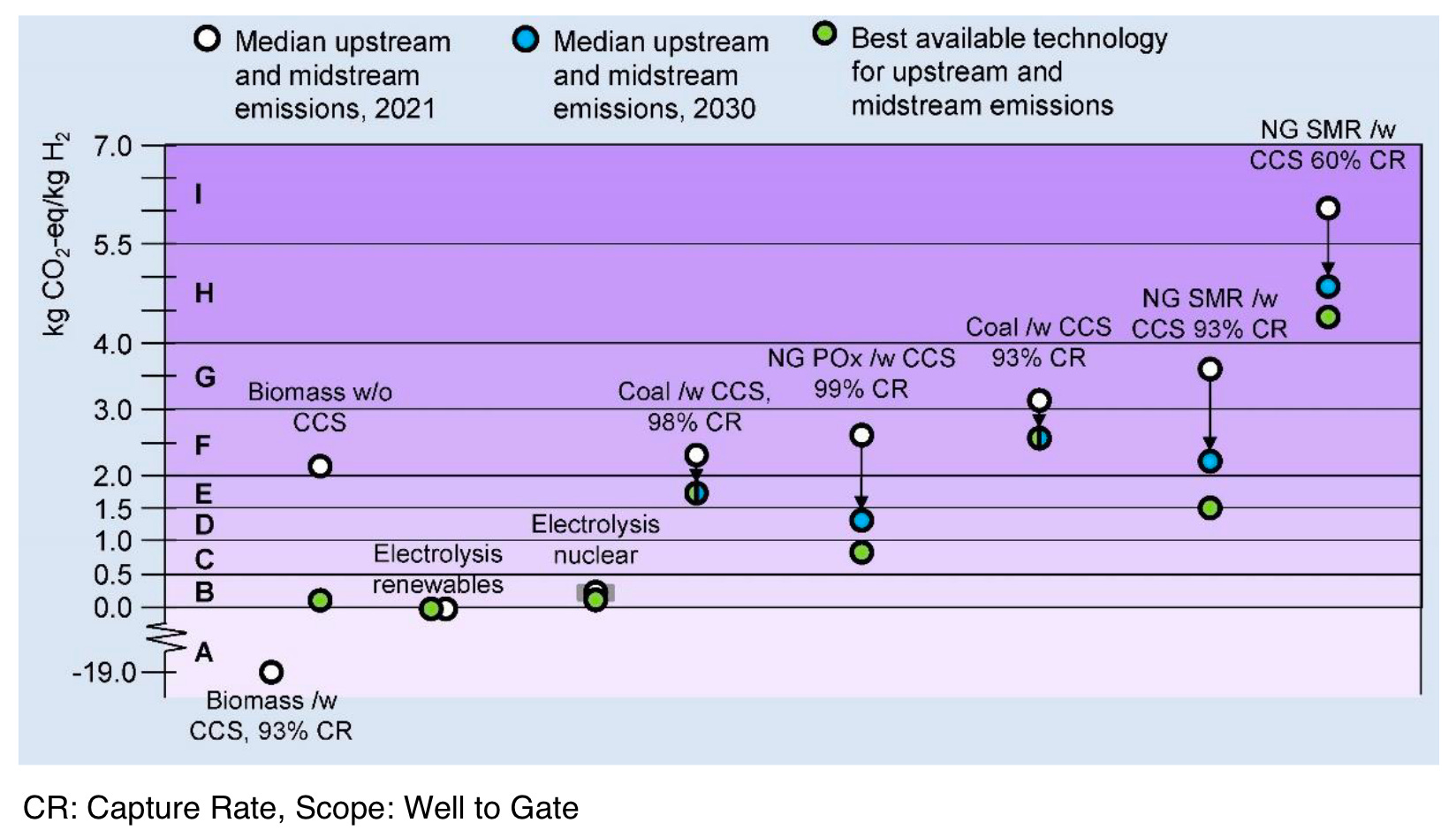

I’ve been hinting at this already. While the Strategy pays lip service to the need for renewable-based hydrogen in the long term (probably closer to 2050), it’s completely accepting of hydrogen made from natural gas or coal (”gray hydrogen”) and fossil fuel-derived hydrogen with carbon capture (”blue hydrogen”) in the foreseeable future.

Banking on gray or blue hydrogen does not help reduce GHG emissions. This is even more true when that hydrogen is used for blending with natural gas or co-firing with coal. It obviously prolongs existing coal plants. What’s worse, Japanese energy companies are building yet new one plants.

Even more insidious is the lifecycle emissions of these types of hydrogen. On these points, the Renewable Energy Institute of Japan (REI) is scathing. Referring to data from the International Energy Agency, REI explains that (p. 9):

Emissions from gray hydrogen produced by natural gas reforming are 35% higher than emissions from burning natural gas. Therefore, if hydrogen is used only for fuel, such as for generating power, continuing to burn natural gas will produce less GHG emissions. The 6th Strategic Energy Plan [published by METI in 2021] sets a target of co-firing hydrogen at a rate of 30% at gas-fired plants by 2030, but if gray hydrogen is used, GHG emissions will be 10% higher than not co-firing

You read that right: because of the emissions from production, transformation, and transportation, fossil fuel-derived hydrogen without CCS has higher emissions than simply burning natural gas for electric generation. To call this a clean energy strategy is a downright farce.

What’s the Strategy’s thinking on blue hydrogen? Unlike the 2017 version, the revised Strategy defines low-carbon hydrogen as anything with an emission intensity (3.4 kg-CO2/kg-H2 or below, if you’re curious). But in a detailed comparison with standards set by other countries and private-sector organizations, REI concludes (p. 4) that “out of all the players, Japan’s reference value represents the lowest hurdle to emissions.”

Even if Japan were to adhere to a stricter standard of emissions intensity, best available data indicates that capturing emissions from hydrogen production is still a less than second-best climate solution. REI points out, again using IEA data, that even when most of the CO2 is captured, emissions from blue hydrogen is still significantly higher than from “green” hydrogen (produced with renewable energy via electrolysis).

Independent research by Robert Howarth and Mark Jacobson, published in Energy Science & Engineering in 2021, also found that blue hydrogen’s GHG emissions are more than 20% higher than burning natural gas or coal for heat.

The crucial thing to remember is that these conclusions refer to lifecycle emissions. Once gray or blue hydrogen is shipped into Japan, that hydrogen itself is zero-emission. By outsourcing hydrogen production to other countries, Japan is condemning its trade partners to do the emitting so that it can claim to be clean. This fact really gets under my skin.

By outsourcing hydrogen production to other countries, Japan is condemning its trade partners to do the emitting so that it can claim to be clean.

Adam Tooze recently observed that while the urgency of the climate crisis demands the strong arm of the state, industrial policies tread worrying close to a pitfall. “For decades,” he writes, “economists warned of the dangers of trying through industrial policy to pick winners. The risk is not just that you might fail, but that in doing so you incur costs. You commit real resources that foreclose other options.”

Japan has firmly hopped on the bandwagon of the budding hydrogen industrial policy across the world. Politicians, bureaucrats, and industrial elites are putting a stunning degree of faith and resources into bringing about a Hydrogen Society. The government is set to pour trillions of yen into developing the supply chain and end-use industries for hydrogen over the next several decades. Yet considering that in many of these areas, electrification is simply the smarter and cheaper decarbonization solution, and that the production and use of hydrogen will exacerbate lifecycle GHG emissions, it seems beyond doubt that Japan is committing a grave and costly mistake.