Teladoc Health - The Future of Doctor Visit

Teladoc Health - The Future of Doctor Visit

Fundamental approach and Intrinsic Valuation.

Overview

Teladoc Health is the global leader in whole-person virtual care, forging a new healthcare experience with better convenience, outcomes, and value. Their mission is to empower all people everywhere to live their healthiest lives by transforming the healthcare experience. The Aim of Teladoc Health is offering to everyone access to the best healthcare, anywhere in the world on their terms. Their vision is to make virtual care the first step on any healthcare journey and deliver this mission by providing whole-person virtual care that includes primary care, mental health, chronic condition management, and more. They have created a unified and personalized consumer experience, developing technologies to connect patients and extend the reach of care providers, delivering the highest standard of clinical quality at every touchpoint, and enhancing health decisions and outcomes with smart data and actionable insights. Regardless of people’s healthcare needs, across any site of care, they aim to provide the right level of personalized support to meet that need. Following their site, they believe that they have the largest breadth of integrated whole-person products and services in the virtual care industry.

Operating Segments

Teladoc Health Integrated Care Segment

The Integrated Care segment primarily generates revenue on a contractually recurring, access fee basis, typically on a per-member-per-month (“PMPM”) basis. In some cases, Clients primarily pay monthly access fees based on a per-participant-per-month model, based on the number of active enrolled members each month. This segment also generates revenue from the health system and provides to the Clients, related to their licensed technology platform healthcare, primarily in the form of recurring access fee revenue as well as from the sale and lease of devices such as robots, carts, and tablets. The company also generates revenue on a per-telehealth visit basis through certain Clients with visit fee-only arrangements and for certain Clients, they earn visit fees or per-case fees in combination with access fees. Access fee services continue to be the most appealing due to the proven effectiveness of their engagement software platform. Access fees are paid by Clients on behalf of their employees, dependents, policyholders, cardholders, beneficiaries, and clinicians, or as is the case with certain subscribers, fees are paid by their members themselves. Visit fees for general medical and specialty visits are typically paid by Clients and/or members.

BetterHelp Segment

BetterHelp segment primarily generates revenue from paying users who pay a fee, most commonly monthly, to access the network of therapists and psychiatrists. Furthermore, BetterHelp is the leader in the Direct-to-Consumer (D2C) therapy market, both in terms of the number of individuals enrolled and the number of licensed professionals who provide services on the platform. The scale of their data and provider network, powered by data science capabilities, creates a competitive advantage for the company in providing an optimal match of an individual with a provider, increasing the rate of success in therapy.

Revenues

Teladoc revenue streams consist of:

Consultation or visitation fees: When a patient or visitor uses the Teladoc service to speak with a healthcare professional, they are charged a fee for the consultation. The amount of the fee may vary depending on the type of consultation and the specific healthcare professional involved;

Subscription fees: This telehealth giant offers various subscription plans that provide access to its telemedicine services for a monthly or annual fee. These subscription plans may include additional benefits, such as discounts on consultations or access to additional services;

Strategic corporate partnerships: Teladoc partners with employers, health insurance providers, and other organizations to provide telemedicine services to their employees or members. These partnerships involve the payment of fees by the partner organization in exchange for access to Teladoc’s services.

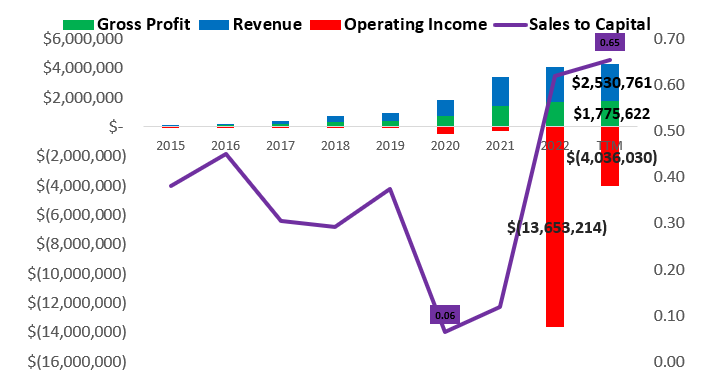

One of the most mandatory signs that we are seeking in non-profitable companies is the expansion of the Revenues. The below table shows that Teladoc Health has a constant growth in revenues with a total increase between 2013 and the TTM (2023) to be at 12.614%. Since Initial Public Offering (IPO), the company had high growth in revenues with the most exceptional years being 2019 and 2020 because of COVID-19. Also, as a disruptor in the telemedicine sector, is very sensitive to macro events, like high interest rates and inflation. As a result, in 2022 the company faced the minimum growth in revenues in the last 10 years and that’s why they came to brigs with the misvaluation of the fair value on Livongo acquisition, which took place in 2020.

Profitability

The company operates in the sector of Healthcare – Information and Technology which has high revenues with average operating margins and high reinvestment rate.

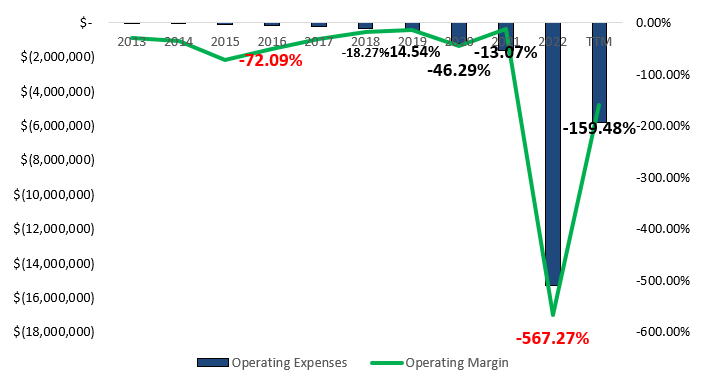

Looking at the above diagram, high growth in revenues and stable sales to capital (stable reinvestment rate) have led to the improvement of the operating margins from -72% (2015) to -14% (2019). In 2020 seems that Teladoc correctly predicted the high growth (for the year 2021) and took the decision to acquire Livongo for 18.5 Billion. The event had a huge effect on sales to capital, which reached the lowest value at 0.06 (huge reinvestment rate) and an increase in negative operating margins at -46%. But it is clear that high investments from the Livongo acquisition, have started to improve again the operating margins at previous levels (-13%) at the end of fiscal year 2021. Finally, in 2022 Teladoc Health experienced the highest operating expenses from the negative profitability of Livongo, which occurred by the high-interest rates and inflation. The event was depicted in the income statement (other operating expenses) as a goodwill impairment (almost 13 Billion) because of the big difference between the fair and book value of Livongo.

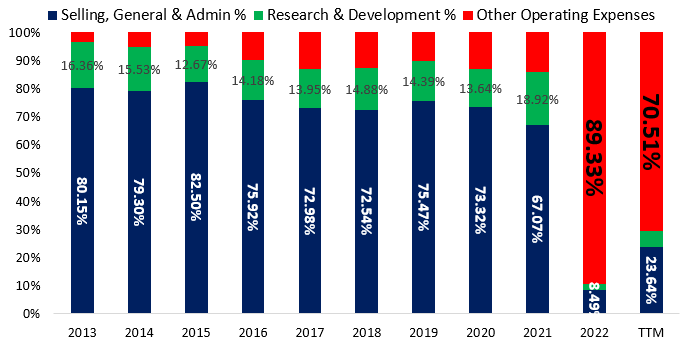

Total Operating Expenses

Sales and Marketing

Sales expenses consist primarily of employee-related expenses, including salaries, benefits, commissions, incentive-based awards, employment taxes, travel, and stock-based compensation costs for our employees engaged in sales, account management, and sales support in addition to commissions paid to external brokers. Sales expenses exclude certain allocations of occupancy expense as well as depreciation and amortization.

Research and Development

Technology and development expenses include the costs of operating on-demand technology infrastructure that is not directly related to changes in revenue or volume of visits, including certain licensed applications, information technology infrastructure, security, and compliance. The technology and development line item also contains amounts charged to expense for research and development, which include costs of new product development, costs to add new features or improve reliability or scalability of existing applications, and other software development and engineering costs to the extent that they are not capitalized. The research and development expenses may enable future revenue growth but are not directly related to current revenues.

General and Administrative Expenses

General and administrative expenses include personnel and related expenses (including salaries and benefits, incentive compensation, and stock-based compensation) of, and professional fees, legal and compliance, operations, human resources, clinical, corporate strategy, business development, strategies, quality, and executive departments. They also include bank charges, most of the facilities costs including rent, utilities, and facilities maintenance, except for amounts allocated to cost of revenues, as well as therapists recruiting costs, related to BetterHelp, indirect taxes, and certain licensed corporate applications.

Survey the Landscape

To set the landscape I will examine the following parameters:

1. How much growth the Telemedicine sector will have?

2. Competition from the companies who operate in the sector.

3. How much is the market share of Teladoc Health in this market?

4. How exactly the macro environment, which operates, will affect the operations?

Following a report from the website www.futuremarketinsights.com, the whole value of the Telemedicine Market in 2023 will be 106 Billion and is projected to grow to 912 Billion by 2033, exhibiting a compound annual growth rate (CAGR) of 24%.

Furthermore, the company held a leading position (Top 5 company) in the market share of Telemedicine which is estimated at 6% in 2023 (source: here).

Teladoc Health Inc. Narrative

Every valuation starts with a narrative, a story that you see unfolding for your company in the future. In developing this narrative, I will try to make assessments for the company (its products, services, and management), the market, the competition, and the macro environment in which operates trying to:

Keep it simple.

Keep it focused.

Stay grounded in reality.

My narrative for Teladoc Health goes as follows:

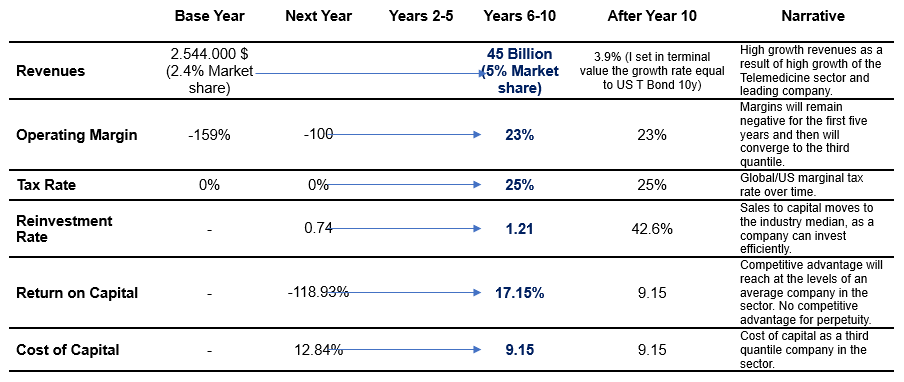

1. Leading company in the Telemedicine sector with revenues to multiply 14 times by 2033 (Market share equal to 5%).

2. In profitability, I searched at the third percentile of the Healthcare Technology and Information sector which is equal to 23%.

3. Reinvestment Rate: This sector has a generally high reinvestment rate (median sales to capital just above 1) and at the same time, Teladoc has to face the high-interest rate and inflation, which has affected Livongo, with higher investment than in the past. As a result, I set for the first five years, sales to capital equal to 0.74 (high reinvestment rate) and after 5 years equal to 1.21 (median of the sector).

Since I have set up my narrative for Teladoc Health, I will check it against history, economic first principles, and common sense:

Valuation Results of Teladoc Health Inc.

Teladoc Health Inc is one of the leading companies in the Telemedicine sector which is going to grow at a fast pace in this decade. I assumed that the market share of Teladoc will be improved from 2%(2023) to 5%(2033) because as a leading company will have a higher competitive advantage than the competitors. Furthermore, I assumed that operating income in the first year will remain negative at -100% as a result of the poor operation of Livongo and then will converge to the third quantile of the sector. Due to high expenses from Livongo, Teladoc will need to make higher reinvestment rates than an average company in the sector and as a result, I set the value at 0.74 for the next years. After year 5, the company will have improved its operations with an established business model and average Reinvestment rate. As a global company that wants to offer a whole care solution, I attached a cost of capital at the third quantile of the sector which is 12.84%. Finally, the company will be efficient as an average company in the sector with no competitive advantage (in perpetuity).

Value of Teladoc Health Inc

Value of Teledoc $7,216,025

Probability of failure = 0.00%

Value of operating assets = $7,216,025

- Debt $1,575,060

- Minority interests $0

+ Cash $958,695

+ Non-operating assets $0

Value of equity $6,599,659

- Value of options $64,601

Value of equity in common stock $6,535,059

Number of shares 159,675.00

Estimated value /share $40.93

Price per share $29.00

% Under or Over Valued -29.14%

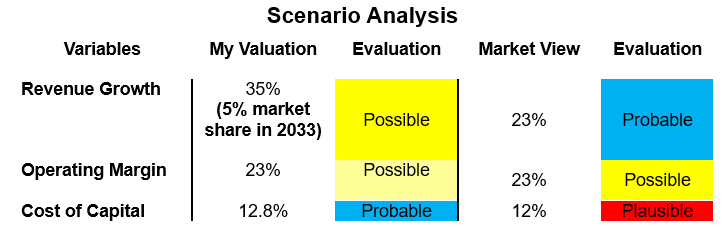

Monte Carlo Simulation, Scenario, and Sensitivity Analysis

The reasons that I use a Monte Carlo simulation are the following:

1. High sensitivity from Revenues growth and Operating margin.

2. To view where my valuation stands and what is the market view about the company.

Revenues Growth: Minimum extreme distribution: 20% Median with St div 3%. Higher probability of upside because 20% is the average of the sector.

Operating Margin: Triangular distribution: 19% to 26%. To include probable and Plausible scenarios.

Cost of Capital: 12.84% Normal distribution: Mean 12% St div 1%. Risk increase as the value increase.

Below you can find the results between the 10th and 90th percentile with medium values which represent the 25th, 50th (Median), and 75th percentile for all the variables.

Since that I have all the available data from the simulation I will examine my valuation and the market view, against the whole probabilistic spectrum that we have created:

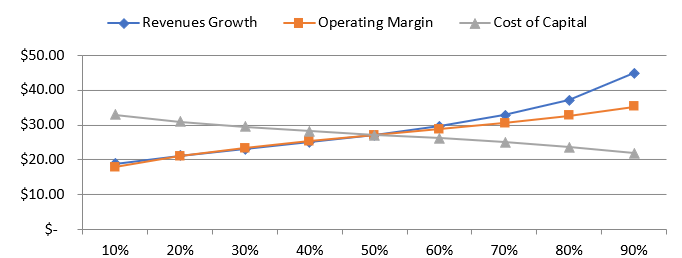

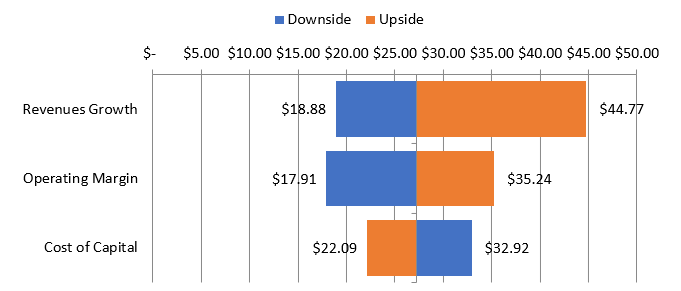

Also, to dive deeper into my valuation I run a sensitivity analysis between the Value per share (outcome) and the 3 variables (inputs) to investigate which of them has the highest impact on my Valuation:

When Value per share is lower than the 50th percentile, the cost of capital has the biggest impact. As the value increases and cross the median (50%) then the revenue growth start to have the highest impact with operating margins coming second.

Revenue growth seems to be the main force for higher values above the median but the interesting thing is that operating margin plays the leading role to more downside when the value per share is below the median which is logical because I have assumed in base year -159% and the next year -100% operating margin. The cost of Capital seems that has the same effect at any stage of the model.

Summary, Thoughts, and Conclusion

1. A good valuation stands between the numbers and narratives. I tried to make estimations in fundamental factors, looking at the history of the company and then I adjusted them to reflect the high competition and the macroeconomic effects.

2. Furthermore, I ran a Monte Carlo simulation to understand where my valuation stands relative to the market view, and what variables should be fulfilled to become my valuation realistic. Also, from sensitivity analysis, I examine the impact of the variables and at which percentile (stage), each of them, has the highest impact.

3. Market View: Teladoc Health is a company with almost similar revenue growth to an average company with medium risk but with operating margins that touch that in the third quantile of the sector (23%).

4. My View: In my narrative, I tried to take advantage of the future high growth of the Telemedicine sector and as a result, I assumed revenue growth of approximately 35%, a high discount rate, and at the same time operating margins equal to that in the third quantile sector with no competitive advantage for perpetuity. As a result, I reached a value of 40$ per share which stands in the 80th percentile of the Simulation. That means, my approach has an 80% chance to be overvalued against the market which offers a 50% chance to be overvalued.

5. Taking into account the above results, the assumptions that the market has done are probable to happen and this price could be a good entry point for holding Teladoc Health Inc in the Long term.

6. The main advantage of Teladoc Health Inc. is that has an early entry in Telemedicine and leads the way in the Global market at the whole care health level. Due to the high growth of the sector, it is avoidable the high competition from other companies and that’s why I assumed that the market share will be at 5% and with a high reinvestment rate. Furthermore and looking at the sensitivity analysis of the company, operating margins play a key role especially at the downside of price because goodwill impairment is depicted as operating expenses and as a result, is not only negative but with high value (-159%).

I assumed that in 2024 the operating margin will have been improved (-100%) as macro events will improve also. If you believe that margins will drop below my assumptions then you should stay away from this stock because affect too much the value per share, at levels that can drop the price between 18$ and 20$. To conclude, for my taste Teladoc Health Inc. is undervalued and I will pay the price of the market. I hope all of you have good investments and thank you for supporting my work.