MERS

I know I said no posts this week, but I’ve been thinking about this topic for a few days, so here you go, before I go. A little reminiscing.

I was writing about these things in emails to friends years ago, and that’s where these recollections are from.

This post is for subscribers only. Thank you.

The other day I heard someone mention “MERS”, which gave me flashbacks from the bubble before this bubble. I hadn’t heard the acronym in years, yet it was a massive national fraud that somehow has disappeared from our collective memory, buried down the memory hole that stores so much of our history. I’ll just share some of the things I have saved here, for posterity.

This is a nice overview of MERS from 2010, I believe by Karl Denniger. The link no longer exists.

“In the mid-1990s mortgage bankers decided they did not want to pay recording fees for assigning mortgages anymore. This decision was driven by securitization—a process of pooling many mortgages into a trust and selling income from the trust to investors on Wall Street. Securitization, also sometimes called structured finance, usually required several successive mortgage assignments to different companies. To avoid paying county recording fees, mortgage bankers formed a plan to create one shell company that would pretend to own all the mortgages in the country—that way, the mortgage bankers would never have to record assignments since the same company would always “own” all the mortgages.

They incorporated the shell company in Delaware and called it Mortgage Electronic Registration Systems, Inc. Even though not a single state legislature or appellate court had authorized this change in the real property recording, investors interested in subprime and exotic mortgage backed securities were still willing to buy mortgages recorded through this new proxy system…

Because the new system cut out payment of county recording fees it was significantly cheaper for intermediary mortgage companies and the investment banks that packaged mortgage securities. Acting on the impulse to maximize profits by avoiding payment of fees to county governments much of the national residential mortgage market shifted to the new proxy recording system in only a few years. Now about 60% of the nation’s residential mortgages are recorded in the name of MERS, Inc. rather than the bank, trust, or company that actually has a meaningful economic interest in the repayment of the debt. For the first time in the nation’s history, there is no longer an authoritative, public record of who owns land in each county…

Both the MERS-as-an-agent and the MERS-as-an-actual mortgagee theories have significant legal problems. If MERS is merely an agent of the actual lender, it is extremely unclear that it has the authority to list itself as a mortgagee or deed of trust beneficiary under state land title recording acts. These statutes do not have provisions authorizing financial institutions to use the name of a shell company, nominee, or some other form of an agent instead of the actual owner of the interest in the land. After all the point of these statutes is to provide a transparent, reliable, record of actual—as opposed to nominal—land ownership.

Conversely, if MERS is actually a mortgagee, then while it may have authority to record mortgages in its own name, both MERS and financial institutions investing in MERS-recorded mortgages run afoul of longstanding precedent on the inseparability of promissory notes and mortgages…

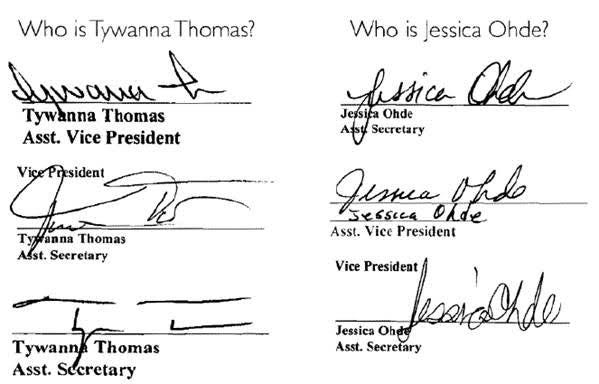

As a practical matter, the incoherence of MERS’ legal position is exacerbated by a corporate structure that is so unorthodox as to arguably be considered fraudulent. Because MERSCORP is a company of relatively modest size, it does not have the personnel to deal with legal problems created by its purported ownership of millions of home mortgages. To accommodate the massive amount of paperwork and litigation involved with its business model, MERSCORP simply farms out the MERS, Inc. identity to employees of mortgage servicers, originators, debt collectors, and foreclosure law firms. Instead, MERS invites financial companies to enter names of their own employees into a MERS webpage which then automatically regurgitates boilerplate “corporate resolutions” that purport to name the employees of other companies as “certifying officers” of MERS. These certifying officers also take job titles from MERS stylizing themselves as either assistant secretaries or vice presidents of the MERS, rather than the company that actually employs them. These employees of the servicers, debt collectors, and law firms sign documents pretending to be vice presidents or assistant secretaries of MERS, Inc. even though neither MERSCORP, Inc. nor MERS, Inc. pays any compensation or provides benefits to them. Astonishingly, MERS “vice presidents” are simply paralegals, customer service representatives, and foreclosure attorneys employed by other companies. MERS even sells its corporate seal to non-employees on its internet web page for $25.00 each. Ironically, MERS, Inc.—a company that pretends to own 60% of the nation’s residential mortgages—does not have any of its own employees but still purports to have “thousands” of assistant secretaries and vice presidents…

Typically, the same person holds both the note and the deed of trust. In the event that the note and the deed of trust are split, the note, as a practical matter becomes unsecured. Restatement (Third) of Property (Mortgages) § 5.4. Comment. The practical effect of splitting the deed of trust from the promissory note is to make it impossible for the holder of the note to foreclose, unless the holder of the deed of trust is the agent of the holder of the note. Without the agency relationship, the person holding only the note lacks the power to foreclose in the event of default. The person holding only the deed of trust will never experience default because only the holder of the note is entitled to payment of the underlying obligation. The mortgage loan became ineffectual when the note holder did not also hold the deed of trust…

If the growing line of cases asserting that MERS is neither a mortgagee nor a deed of trust beneficiary is correct, then courts must soon confront profound questions about the very enforceability of MERS’ security agreements. ... There is a compelling legal argument that loans originated through the MERS system fail to create enforceable liens…

The mortgage industry has premised its proxy recording strategy on this separation despite the U.S. Supreme Court’s holding that “the note and the mortgage are inseparable.” If today’s courts take the Carpenter decision at its word, then what do we make of a document purporting to create a mortgage entirely independent of an obligation to pay? If the Supreme court is right that a “mortgage can have no separate existence” from a promissory note, then a security agreement that purports to grant a mortgage independent of the promissory note attempts to convey something that cannot exist.

While this argument will surely strike a discordant note with the mortgage bankers that invested billions of dollars in loans originated with this simple flaw, the position is consistent with a long and hitherto uncontroversial line of cases. Many courts have held that a document attempting to convey an interest in realty fails to convey that interest when an eligible grantee is not named. Courts all around the country have long held: “there must be, in every grant, a grantor, a grantee and a thing granted, and a deed wanting in either essential is absolutely void.”…

Nonetheless, in Chauncey, the trial court, intermediate appellate court and New York’s highest court all agreed that the attempt to convey an “in blank” mortgage failed. The Court of Appeals explained, “No mortgagee or obligee was named in [the security agreement], and no right to maintain an action thereon, or to enforce the same, was given therein to the plaintiff or any other person. It was, per se, of no more legal force than a simple piece of blank paper.”…

In a stunning betrayal of the policies that ground the ancient statute of frauds principal commanding that we commit transfers of land interests to writing, mortgage bankers wrote millions of mortgage loans that did not specify who the actual mortgagee was. For over a hundred years, our courts have held that “legal title to real property may not be established by parole.”…

Who owned MERS? This is an archived link from May 2008. It’s like a who’s who of mortgage fraud.

Countrywide Home Loans, Inc. (Bank of America)

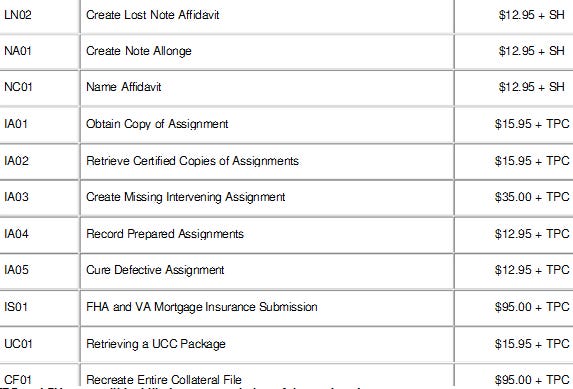

4ClosureFraud Posts Lender Processing Services Mortgage Document Fabrication Price Sheet

We’ve said for some time that document fabrication is widespread in foreclosures. The reason is that the note, which is the borrower IOU, is the critical instrument to establishing the right to foreclose in 45 states (in those states, the mortgage, which is the lien on the property, is a mere “accessory” to the note).

The pooling and servicing agreement, which governs the creation of mortgage backed securities, called for the note to be endorsed (wet ink signatures) through the full chain of title. That means that the originator had to sign the note over to an intermediary party (there were usually at least two), who’d then have to endorse it over to the next intermediary party, and the final intermediary would have to endorse it over to the trustee on behalf of a specified trust (the entity that holds all the notes). This had to be done by closing; there were limited exceptions up to 90 days out; after that, no tickie, no laundry.

Evidence is mounting that for cost reasons, starting in the 2004-2005 time frame, originators like Countrywide simply quit conveying the note. We are told this practice was widespread, probably endemic. The notes are apparently are still in originator warehouses. That means the trust does not have them (the legalese is it is not the real party of interest), therefore it is not in a position to foreclose on behalf of the RMBS investors. So various ruses have been used to finesse this rather large problem.

The foreclosing party often obtains the note from the originator at the time of foreclosure, but that isn’t kosher under the rules governing the mortgage backed security. First, it’s too late to assign the mortgage to the trust. Second. IRS rules forbid a REMIC (real estate mortgage investment trust) from accepting a non-performing asset, meaning a dud loan. And it’s also problematic to assign a note from the originator if it’s bankrupt (the bankruptcy trustee must approve, and from what we can discern, the note are being conveyed without approval, plus there is no employee of the bankrupt entity authorized to endorse the note properly, another wee problem).

We finally have concrete proof of how widespread document fabrication was. For some reason the ScribD embeds aren’t working correctly, you can view the entire Lender Processing Services price sheet here, and here are the germane sections.

Not only are there prices up for creating, which means fabricating documents out of whole cloth, and look at the extent of the offerings. The collateral file is ALL the documents the trustee (or the custodian as an agent of the trustee) needs to have pursuant to its obligations under the pooling and servicing agreement on behalf of the mortgage backed security holder. This means most importantly the original of the note (the borrower IOU), copies of the mortgage (the lien on the property), the securitization agreement, and title insurance.

Also notice that there is a price for creating allonges. We discussed earlier that phony allonges have become the preferred fix for the failure to convey notes properly

From Improper GMAC Affidavits Leading to Charges of Document Fabrication to Change Title:

The cure for the mortgage documents puts the loan out of eligibility for the trust. In order to cure, on a current basis, they have to argue that the loan goes retroactively back into the trust. This is the cure that the banks have been unwilling to do, because it is a big problem for the MBS. So instead they forge and fabricate documents.

The letter in particular mentions an allonge. An allonge is a separate sheet of paper which is attached to a note to allow for more signatures, in this case, endorsements, to be added. Allonges have had a way of magically appearing in collateral files while trails are in progress (I’ve seen it happen in cases I was tracking; it’s gotten so common that some attorneys warn judges to be on the alert for “ta dah” moments).

The wee problem with an allonge miraculously being discovered is that the allonges that show up are inherently in violation of UCC (Uniform Commercial Code) provisions (UCC has been adopted by all states, a few states have minor quirks, but the broad provisions are very similar).

An allonge is NOT to be used unless all the space on the original note, including the margins and the back side of pages, has been used up. This is never the case. Second, an allonge has to be so firmly attached to the original document as to be inseparable. Thus an allonge suddenly being discovered is an impossibility (well impossible if it were legit), yet it seems to happen all the time.

“So wake up and smell the coffee. The story that banks have been trying to sell has been that document problems like improper affidavits are mere technicalities. We’ve said from the get go that they were the tip of the iceberg of widespread document forgeries and fraud. This price sheet provides concrete proof that the practices we pointed to not only existed, but are a routine way of doing business in servicer and trustee land.”

As a practical matter, the incoherence of MERS legal position is exacerbated by a corporate structure that is so unorthodox as to arguably be considered fraudulent. Because MERSCORP is a company of relatively modest size, it does not have the personnel to deal with legal problems created by its purported ownership of millions of home mortgages. To accommodate the massive amount of paperwork and litigation involved with its business model, MERSCORP simply farms out the MERS, Inc. identity to employees of mortgage servicers, originators, debt collectors, and foreclosure law firms.

Instead, MERS invites financial companies to enter names of their own employees into a MERS webpage which then automatically regurgitates boilerplate “corporate resolutions” that purport to name the employees of other companies as “certifying officers” of MERS. These certifying officers also take job titles from MERS stylizing themselves as either assistant secretaries or vice presidents of the MERS, rather than the company that actually employs them. These employees of the servicers, debt collectors, and law firms sign documents pretending to be vice presidents or assistant secretaries of MERS, Inc. even though neither MERSCORP, Inc. nor MERS, Inc. pays any compensation or provides benefits to them.

Astonishingly, MERS “vice presidents” are simply paralegals, customer service representatives, and foreclosure attorneys employed by other companies. MERS even sells its corporate seal to non-employees on its internet web page for $25.00 each. Ironically, MERS, Inc.—a company that pretends to own 60% of the nation’s residential mortgages—does not have any of its own employees but still purports to have “thousands” of assistant secretaries and vice presidents.

Here's the problem. In creating MERS, these institutions actually changed the land-title system that this country - for much of its history - has relied upon to determine legal ownership status of land titleholders.

Not only did the lenders sidestep (read that to mean avoid) paying billions of dollars in fees to local governments, they paid themselves from the fees that MERS collected.

MERS is facing class-action lawsuits and civil racketeering suits around the country and their members are being individually named in all these suits. One suit alleges that MERS owes California a potential $60 billion to $120 billion in unpaid land-recording fees.

If suits against MERS and all its members are successful, unpaid recording fees and fines (that can be as much as $10,000 per incident) would make every one of them insolvent.

Guess what happened next?

Get Ready for the Great MERS Whitewash Bill

“The system is known as MERS, the acronym for a private company called Mortgage Electronic Registry Systems. Set up by banks in the 1997, MERS is a system for tracking ownership of home loans as they move from mortgage originator through the financial pipeline to the trusts set up when mortgage securities are sold.

The system has come under scrutiny by critics who charge MERS with facilitating slipshod practices. Recently, lawyers have filed lawsuits claiming that banks owe states billions of dollars for mortgage recording fees they avoided by using MERS.

If courts rule against MERS, the damage could be catastrophic. Here’s how the AP tallies up the potential damage:”

Assuming each mortgage it tracks had been resold, and re-recorded, just once, MERS would have saved the industry $2.4 billion in recording costs, R.K. Arnold, the firm's chief executive officer, testified in 2009. It's not unusual for a mortgage to be resold a dozen times or more.

The California suit alone could cost MERS $60 billion to $120 billion in damages and penalties from unpaid recording fees.

The liabilities are astronomical because, according to laws in California and many other states, penalties between $5,000 and $10,000 can be imposed each time a recording fee went unpaid. Because the suits are filed as false claims, the law stipulates that the penalties can then be tripled.

“Perhaps even more devastatingly, some critics say that sloppiness at MERS—which has just 40 full-time employees—may have botched chain of title for many mortgages. They say that MERS lacks standing to bring foreclosure actions, and the botched chain of title may cast doubts on whether anyone has clear enough ownership of some mortgages to foreclose on a defaulting borrower. The problems with MERS system led JPMorgan Chase CEO Jamie Dimon to stop using MERS for foreclosures in 2008.

Now it appears that Congress may attempt to prevent any MERS meltdown from occurring. MERS is owned by all the biggest banks, and they certainly do not want it to be sunk by huge fines. Investors in mortgage-backed securities also do not want to see the value of their bonds sink because of doubts about the ownership of the underlying mortgages.

So it looks like the stage may be set for Congress to pass a bill that would limit MERS exposure on the recording fee issue and perhaps retroactively legitimate mortgage transfers conducted through MERS private database.

Self-styled consumer advocate Neil Garfield says the legislation is already being drafted:”

After years of negative judicial decisions about the use of a straw-man on mortgages, MERS was about to lose its existence as well as its credibility. But now all of that is set to change as Wall Street money is pouring into the coffers of those who are receptive (i.e., almost everyone in Congress). The legislation is already being drafted under the interstate commerce clause to ratify MERS and everything it did retroactively. It appears that the Obama administration is ready to pardon all the securitization deviants by signing this bill into law. This information is corroborated by several people who are in sensitive positions — persons who would be the first to know such proposals. Fortunately, there are some people in Washington who have a conscience and do not want to see this happen.

“Garfield is overstating things a bit. In truth, the results of the legal challenges to MERS have been mixed. But it is very plausible that the banks might want to put to rest any ongoing uncertainty about the legality of MERS. I wouldn't be at all surprised if Congress manages to pass a bill that bails MERS out of its legal issues.”

MERS prevails in Massachusetts, Hawaii “Plaintiff’s theory that the note and the mortgage somehow became disconnected from one another, and that the mortgage should disappear as a result, is therefore not tenable as a matter of law," the court opinion states.

Bank gives man foreclosed house

Perry Laspina was in the middle of foreclosure with the possibility of losing the house he owned in Jacksonville. Then the mail came one day in late January telling him that the house was his.

Despite the $72,000 mortgage that he barely paid anything on, despite the foreclosure ... the house was his.

In the middle of foreclosures gone wild, of a system overloaded by sheer volume, judicial investigations and allegations of corners cut, Laspina ended up with the house.

Despite the fact that he didn’t have an attorney in the foreclosure proceedings, the mortgage holder simply gave up and walked away…

In December, officials for MERS, which acted as the mortgage holder, signed and filed the documents saying it “has received full payment and satisfaction ... and does hereby cancel and discharge said mortgage.” Laspina had paid less than $1,000 toward the principal on his $72,000 loan. [This paragraph was in the original article, but was not archived - rh]

No link - it’s been long scrubbed - but this is from May 2011:

"Jeff Thigpen, the register of deeds in Guilford County, North Carolina, a county of about 465,000 in the center of the state (the largest city is Greensboro), decided to survey all the mortgage documents submitted to his office by DocX, a notorious "mortgage mill" that processes documents on behalf of lenders, between August 2006 and April 2010. He was inspired by a 60 Minutes investigation revealing numerous forgeries, backdating, and other false information on mortgage documents. "When I saw that [story], I was basically on fire," Thigpen says. "'I know this material is in my office, I've got to find it, I've got to get it out.'"

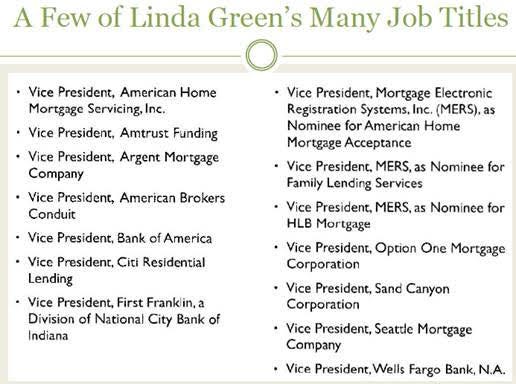

Out of the 6,100 documents Thigpen examined, 4,500 showed signature irregularities. The name of one DocX employee, Linda Green, who was acting as a vice president for several major banks, was forged 15 different ways on the Guilford County documents, rendering them invalid. Thigpen's investigation was one of the first systematic assessments of mortgage document fraud in the entire country, certainly more robust than anything conducted by state and federal regulators...

To reduce costs, the banks invented and funded the Mortgage Electronic Registration System (MERS), an electronic registry that allowed banks to circumvent county registers and thereby avoid paying the recording fee of roughly $35 per mortgage."

Appeals Court Clarifies MERS Role in Foreclosures, June 13, 2011

"The ubiquitous Mortgage Electronic Registration Systems, nominal holder of millions of mortgages, does not have the right to foreclose on a mortgage in default or assign that right to anyone else if it does not hold the underlying promissory note, the Appellate Division, Second Department, ruled Friday. "This Court is mindful of the impact that this decision may have on the mortgage industry in New York, and perhaps the nation," Justice John M. Leventhal wrote for a unanimous panel in Bank of New York v. Silverberg, 17464/08. "Nonetheless, the law must not yield to expediency and the convenience of lending institutions. Proper procedures must be followed to ensure the reliability of the chain of ownership, to secure the dependable transfer of property, and to assure the enforcement of the rules that govern real property." The opinion noted that MERS is involved in about 60 percent of the mortgages originated in the United States."

Robert Schiller: How Tales of ‘Flippers’ Led to a Housing Bubble, May 2017

Schiller blamed the bubble on house flippers.

This was a great response, from the comments:

It’s very demoralizing to read such deliberately misleading stuff from such a distinguished author. Very powerful interests have worked relentlessly to prevent consensus about why the housing boom and bust happened since the collapse of the debt derivatives casino. This article contributes to that confusion by studiously ignoring the institutionalized fraud that made the MBS and CDS casinos possible. This is an astonishing omission.

In 2005, a banker at WAMU offered me a million dollar liar’s loan, no questions asked. I wasn’t even making 6 figures. I told him he was crazy and walked out. He could do that because WAMU was going to dump that subprime loan into a bundle, wipe out the connection between deed of title and promise to pay using the fraudulent MERS system, use the fraudulent credit rating system to give that garbage security a AAA rating and then sell potentially toxic slices of that fraudulently-created pizza to shadow banking and foreign investors hungry for return. All that fraud was possible because the creators, sellers and buyers of that junk, along with people just standing around the casino watching all the fraud, were allowed to buy and sell insurance against collapse of those toxic securities in the form of credit default swaps without having to maintain the capital reserves to pay off those swaps should default occur. That was the biggest fraud. Flippers did not cause the housing boom and bust. Fraud by lenders, enabled by legislators, did.

—Joe, NY

"The mortgage servicers hired people who would never question authority," said Peter Ticktin, a Deerfield Beach, Fla., lawyer who is defending 3,000 homeowners in foreclosure cases. As part of his work, Ticktin gathered 150 depositions from bank employees who say they signed foreclosure affidavits without reviewing the documents or ever laying eyes on them -- earning them the name "robo-signers."

The name Linda Green can be found signed to countless mortgage documents we found in area courthouses. She's listed under a number of titles, allegedly working of numerous banks.

But look at the signatures. You don't have to be a handwriting expert to see they were not signed by the same person. That makes them fraudulent.

8News found more than 20 different variations of the Linda Green signature in courthouses right here in the Metro-Richmond area—prime examples of what's known as robo-signing—a fancy phrase for fraud and perjury on legal mortgage papers.

"This was a widespread national conspiracy," said state senator Chap Peterson.

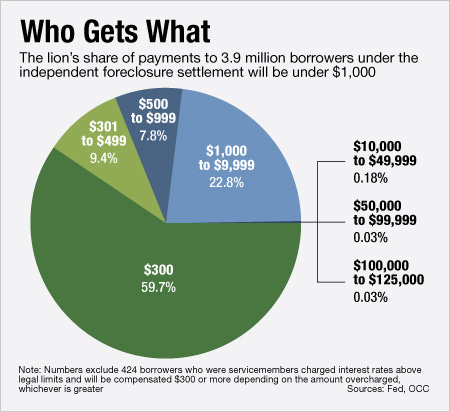

The Banks' "Penalty" To Put Robosigning Behind Them: $300 Per Person

“Regulators reached the mortgage settlement in January after calling off a prolonged and costly independent foreclosure review.”

Will the Real Linda Green Please Step Up?

Memories, memories, memories....the things we did to dig out of this were huge. They changed a lot about MERS, but not what it was at its core. And...lots of policies on attach and affix for the note and allonge, etc. What's (not) funny is that instead of the money going to the borrowers it went to the Independent Foreclosure Review (IFR) auditors - in our case, PwC. And then once the Fed finally realized all the money was actually going to go to the auditors of the Big 5 b/c they didn't find the fraud they thought (yes, of course those documents should not have been signed that way, but no borrower at my former company at least was incorrectly taken to foreclosure in terms of were they in arrears - of course can only speak to what was found when I was there). So a whole bunch of extra procedures were added, a whole bunch of check-the-box stuff, but nothing fundamentally changed....except of course FNMA and FHLMC require you originate in MERS. The auditors got rich, the former signers got harassed, and creak, creak, creak, the engine is starting up again in earnest. We will have the regulatory cycle again without a doubt...

All the senior executives of all the banks should be in prison. All the regulatory agency officials should be in prison. All the politicians should be in prison. None of them should be allowed to work in any capacity of trust. But, of course, none of them were ever even worried. The corrupt system is corrupt for their sakes.