What is a Software Company Worth?

What is a Software Company Worth?

Putting twenty years of public company data to work to help inform what you should pay.

At ParkerGale, we buy private software companies. Mostly from founders who bootstrapped them from inception. Several years later, we sell these companies after recruiting new management teams, running our operating playbooks, making add-on acquisitions, and improving lots of other things to scale the company. As part of this buying and selling, we are constantly asking ourselves:

What should we pay for a new investment?

At what value could we sell a company we already own?

We build complicated Excel models, conduct months of due diligence, and talk to bankers and buyers to help answer these questions, but like every other private equity firm, we also look to private market values and comparable public companies (we call these “comps”) to help us pinpoint the recent prices companies with similar characteristics – size, industry, growth, profitability – have traded.

For software transactions, comps boil down to multiples of revenue and EBITDA. What multiple of last year’s or next year’s revenue should we pay? And for what multiple could we sell? There is more that goes into it (and there is a long list of heuristics buyers, sellers, and bankers use) but multiples are pretty good indicators and help us easily fit companies into different buckets. Yet, sometimes when we use these methods, nuances get lost, making our comparisons inaccurate or, even worse, a sneaky form of wishful thinking. Here’s the good news: In our industry, the market will eventually tell you what you’re worth. Eventually, you won’t have to guess anymore.

We don’t think much of the publicly available valuation data out there for software companies is that great. This is partly because there are so many different kinds of software companies. Ford and Lululemon both sell stuff, but you wouldn’t put them in a group called “Companies that Sell Stuff.” Yet we tend to do this when we look at software companies. Software companies can be cloud-based or on-premise, license or subscription, B2B or consumer, and can serve wildly different end-markets. And we think that these distinctions are important when analyzing valuation metrics.

Additionally, private investors tend to hold their cards close to their chest. Few funds provide accurate valuation information to the public and when they do, it’s rarely standardized. Our industry loves add-backs, pro-formas, cash EBITDA, and adjusted run-rates. These accounting wrinkles make much of the data hard to rely on. And while there are mountains of data on public software companies, the indices are far from perfect comps themselves. They’re either too monolithic (because an aggregate view of software companies is often distorted by a handful of large companies driving the data) or too narrowly focused (encompassing just a small slice of the industry). You might feel smarter after studying an index of public infrastructure software stocks, but we can assure you this isn’t telling you much about what a private vertical SaaS company is worth.

So, what’s a middle market software investor to do? Not all software companies are the same, and most of the attention is skewed to the flashy, high-growth, high-burn, cloud stocks. But using those as comps for middle market buyouts will lead you to the wrong conclusions. First, you can’t go back that far (maybe to 2009) to get a big enough data set on cloud software companies. This also happens to coincide with a record bull market so how do you differentiate between luck and skill during this period? And how does any of this apply to your typical middle market software company? Several investors in our business do a great job covering the SaaSy side of public software companies. Hat tip to Jamin Ball’s Clouded Judgement and Bessemer’s Emerging Cloud Index, two resources we read regularly and helped inspire us to publish our own thoughts on the subject. Check out their stuff for sharp analysis of public cloud software players.

We all love talking about the highfliers, the college dropouts, the world-changers, the mega-trends. And when narrative (software is eating the world) collides with policy (bailouts, ZIRP, stimulus) you can have a self-reinforcing cycle where everything goes up and to the right. That is, until it doesn’t. Were investors wrong about software company valuations in 2021 or are they wrong today? And for the newly-minted portfolio managers and private investors that cut their teeth investing during the recent bull market, maybe our analysis will provide a catalyst to looking at software investing in a new way. When you look back far enough and analyze the data, we think we can reveal some interesting learnings that we integrate into our daily valuation debates.

At ParkerGale, we think that what you pay for an investment matters a whole lot to your eventual investment return, and we’ll admit that the price of entry over the past few years for most software buyouts has shocked us. We have been at this a while and have invested through our share of market bubbles, so we have some strong views on the subject. During the dotcom boom and bust there were a lot of companies valued on some pretty nutty metrics (eyeballs, anyone?). While the metrics this time around are more real (annual recurring revenue, net revenue retention, Rule of 40), investors were rewarded by setting aside historical valuation guidelines to pursue a “growth at any price” investment strategy. This time is different, they’d say. That is, until it isn’t – you know that saying about history not repeating, but probably rhyming.

At ParkerGale, we are unapologetic lower middle market, value-oriented, software buyout investors with a team who has been at it for over twenty-five years. So, you can imagine we scratched our heads a lot during this bull market trying to make sense of the valuations being paid for software companies by people we know to be rational, reasonable investors. While we’ve never spent much time looking outward for validation for what to pay, it was hard not to notice prices rising every day. But instead of throwing out our rulebook, we doubled down on relying on the tools we’ve built over the years to stay disciplined. And today, we are sharing one of those tools with you – our twenty years of middle market software company valuation data. In this first installment, we dare to take the Growth vs. Value debate head on.

Building a Software Index for Growth Equity and Middle Market Investors

First, we had to build an accurate data set. We took the iShares Expanded Tech-Software Sector ETF (IGV) one of the longest running and most comprehensive (though not exhaustive) ETFs tracking public software companies to use as a benchmark index for our analysis. This helped us go back two decades, which is important if you want to capture a few cycles. While the IGV is a good proxy for how the full software stock universe performs, we think it is too monolithic to rely on for private company valuation purposes – large-caps and highfliers driving the index can over-inflate valuation and can’t be relied upon when applied to small, private companies.

Next, we used FactSet to screen public software companies over the past 20 years to ensure that we included companies the IGV missed. After that, we separated the IGV and our additional set of screened companies into two buckets – what we call the PG Growth Equity Index (PGGE) and the PG Middle Market Buyout Index (PGMM) to distinguish between what growth investors generally look for when taking minority stakes in rapidly growing software companies and what middle market investors generally look for when buying control of software companies.

Our simple criteria to separate the two buckets (which we can all quibble about and, believe me, we did a lot of quibbling inside our firm) is below.

PGGE: All public software companies that grew over 25% in a given calendar year irrespective of profitability.

PGMM: All public software companies that grew between 5% and 25% in a given calendar year, while also maintaining at least 10% EBITDA margins in that same year.

In parsing the list, we focused on enterprise software companies only. This means we left out consumer software companies such as Meta and AirBnB and FinTech companies such as Affirm and Block. Other analysts doing similar work might choose to leave these in, but we think they distort our data because most tech-focused private equity firms avoid consumer and FinTech in favor of B2B enterprise software companies focused on vertical markets or infrastructure tools.

Twenty Year Trends

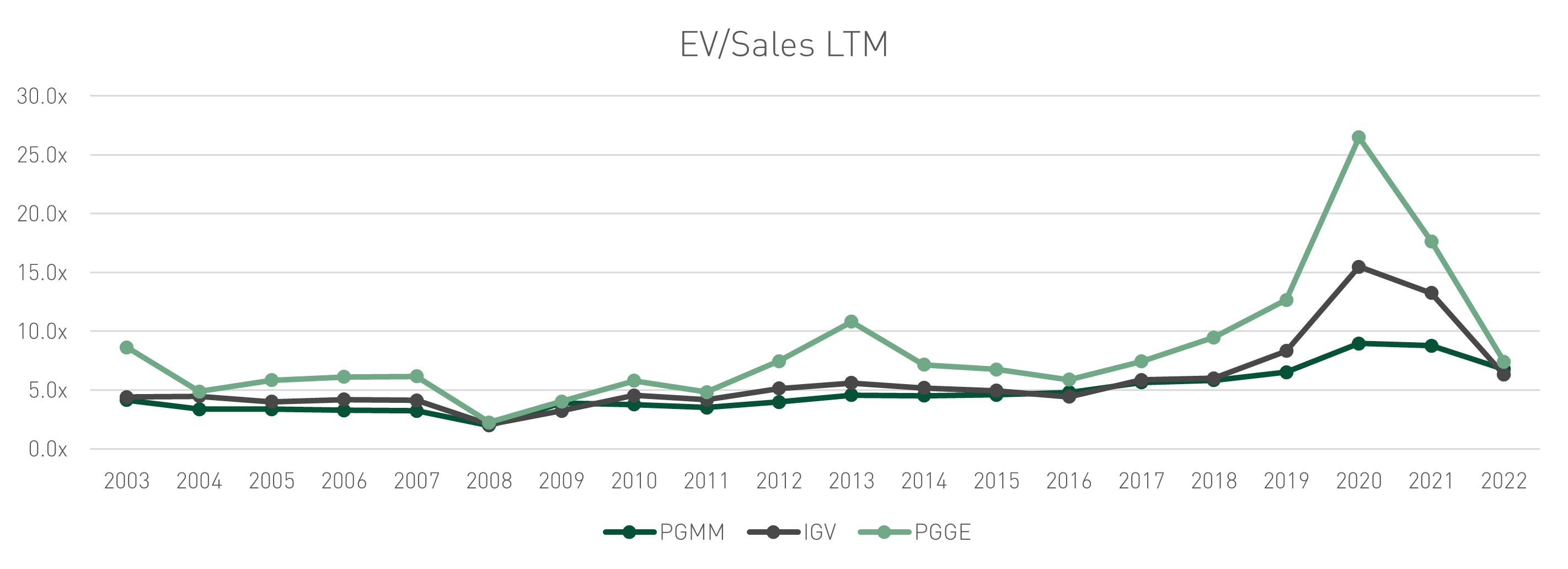

Now that we have all the companies categorized, we can compare how their valuations trended over time. Let’s start with revenue multiples (Enterprise Value / Sales). We like to use Last Twelve Months revenue in our analysis (rather than Forward Twelve Months) because we think it is more accurate to look at actual results rather than projected results (we used estimates for 2022 for the few companies that have not yet reported). You might disagree but we don’t think most people (especially optimistic management teams at small software companies) are great at predicting the future. And, let’s be honest, using forward revenue multiples just helps your multiple look lower than it actually is (especially for high-growth businesses). We’re not here to make your investment memo look more conservative, we’re here to tell you the truth with data. We think the public markets have come to agree recently as future results are getting harder and harder to predict which has been reinforced by this earnings season.

In our first chart below, we plot how revenue multiples have trended over time. After a gravity-defying decade, not surprisingly in 2022, revenue multiples across all three indices (the benchmark IGV, as well as PGGE and PGMM) reached five-year lows, slumping to 6x to 7x trailing revenue. In only four of the last twenty years did revenue multiples for the growthiest companies captured by the PGGE Index surpass 10x revenue (2013 and 2019-2021), despite the common refrain from many in our business that 10x is the target. In fact, in 14 of the past 20 years, the PGGE cohort traded below the 20-year average of 8.4x revenue. Interestingly, multiples in all three indices converged last year for the first time since 2008. When we look at the past 20 years, we see the peaks and valleys of the PGGE cohort, while the PGMM cohort is steadier. Even more, we see how the PGGE cohort affects the overall software universe when we look at the peak of our benchmark. While the PGMM Index never reaches the heights of the PGGE Index, the PGGE Index has sunk to the same lows of the PGMM Index twice – in 2008 and today. This is a pretty clear indication that in downturns, your growth won’t save your valuation. A tough lesson to learn and one you would have missed if you didn’t go back far enough in the data set.

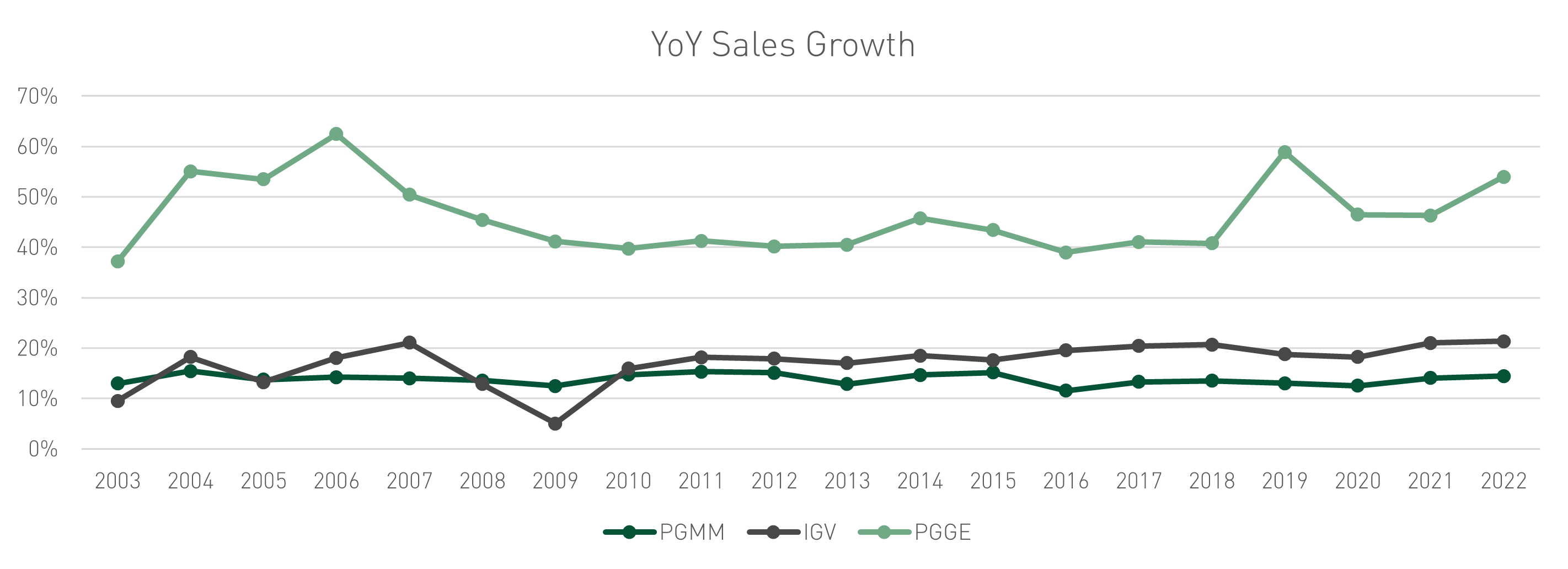

Below, we chart average revenue growth rates for PGMM, PGGE, and IGV. Average revenue growth for PGGE over the past 20 years was an impressive 46%, over three times as fast as PGMM which grew 14% on average.

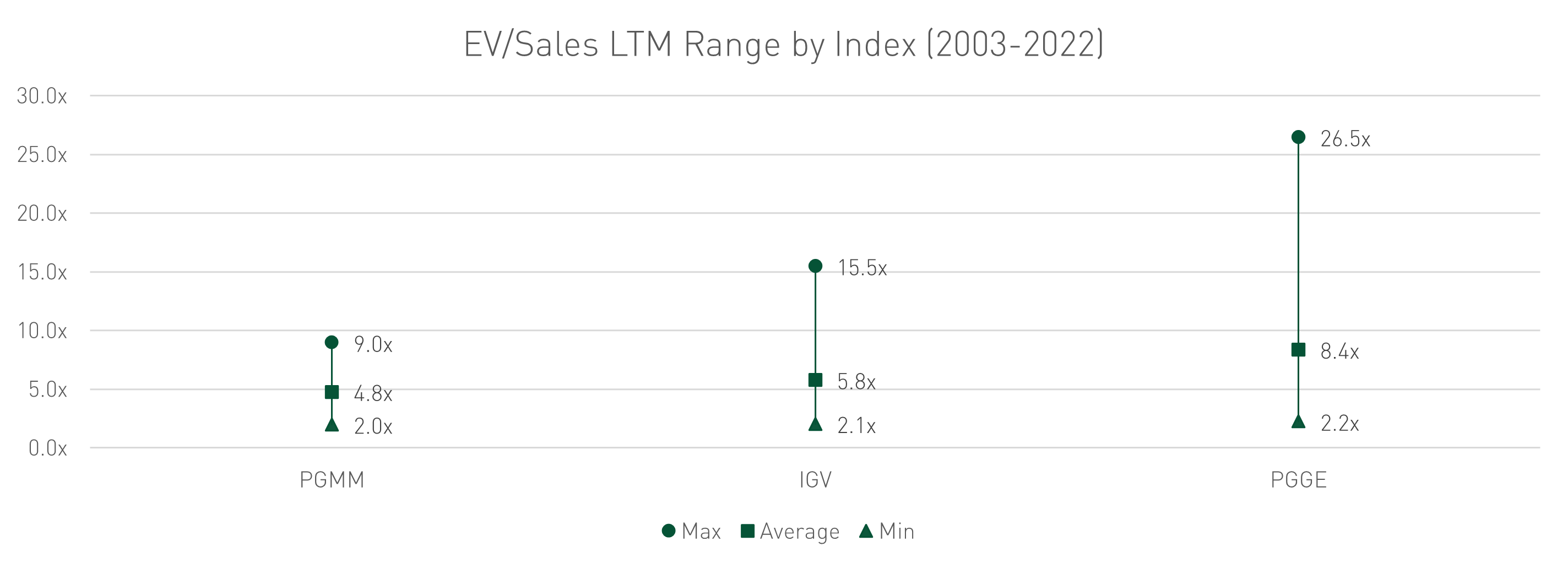

For three times the revenue growth rate, you are paying on average 8.4x revenue for PGGE versus 4.8x revenue for PGMM. However, over the past twenty years, multiples ranged between 2.2x and 26.5x for PGGE versus between 2.0x and 9.0x for PGMM pointing to the volatility of PGGE names and the importance of timing the market to generate returns. From their highs in 2020, the PGGE revenue multiples have compressed by 19 turns, (or 72%) while the PGGM multiples compressed about 2 turns (or 24%).

To better visualize the three indices, we charted the range of revenue multiples for each above. We see that the PGMM stocks trade in a tighter revenue multiple range than the PGGE names. Our PGMM cohort trades more closely to the benchmark in terms of variability as well. The range for PGGE represents the upside opportunity when investing in growth stocks over the past 20 years. The range for PGMM represents the steadiness of these stocks’ valuations. Now think of these ranges together with the line graph of revenue multiples. Yes, PGGE had more upside overall (that’s what you are paying/hoping for), but these opportunities only surfaced during two short windows in mid-2013 and late 2020. We’ll revisit this later when we examine annual share price performance for the three indices as well.

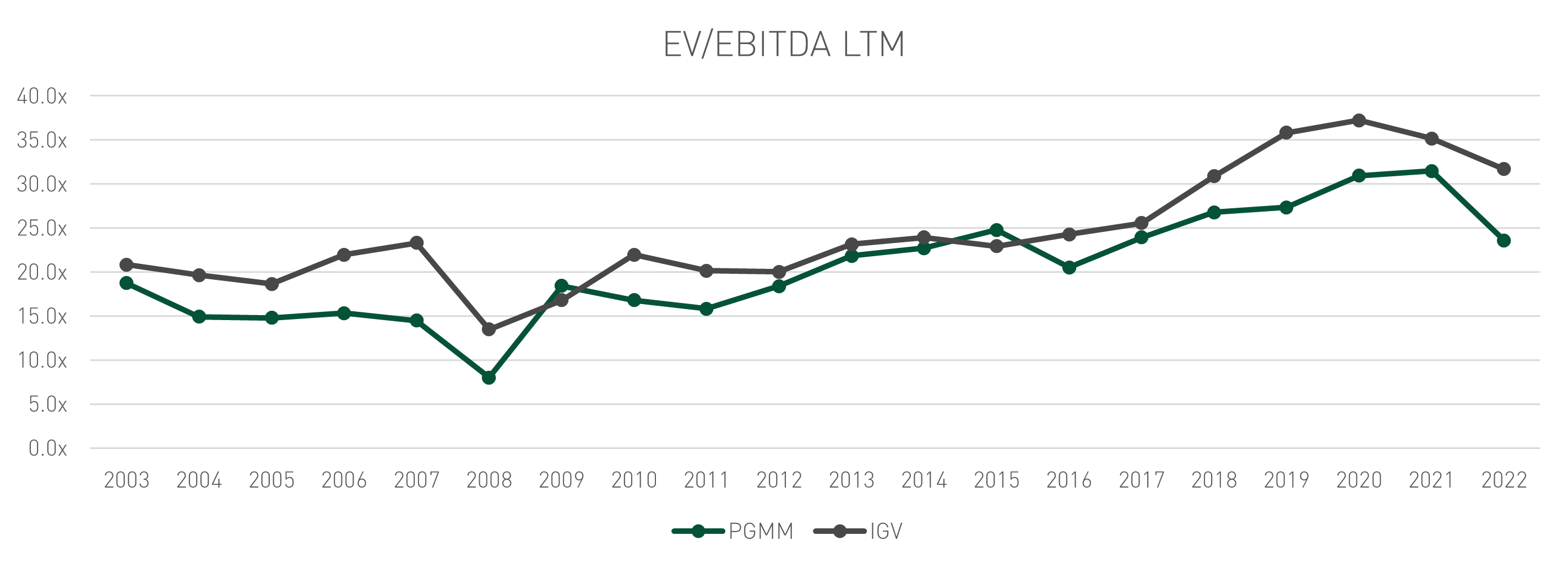

Now let’s turn our attention to EBITDA. With high revenue visibility, high gross margins, low capex, and high operating leverage, software companies can be EBITDA machines if you choose to run them that way. And, as you’ll see in the chart below, there are trade-offs between growth and profits for which you might (or might not) get rewarded.

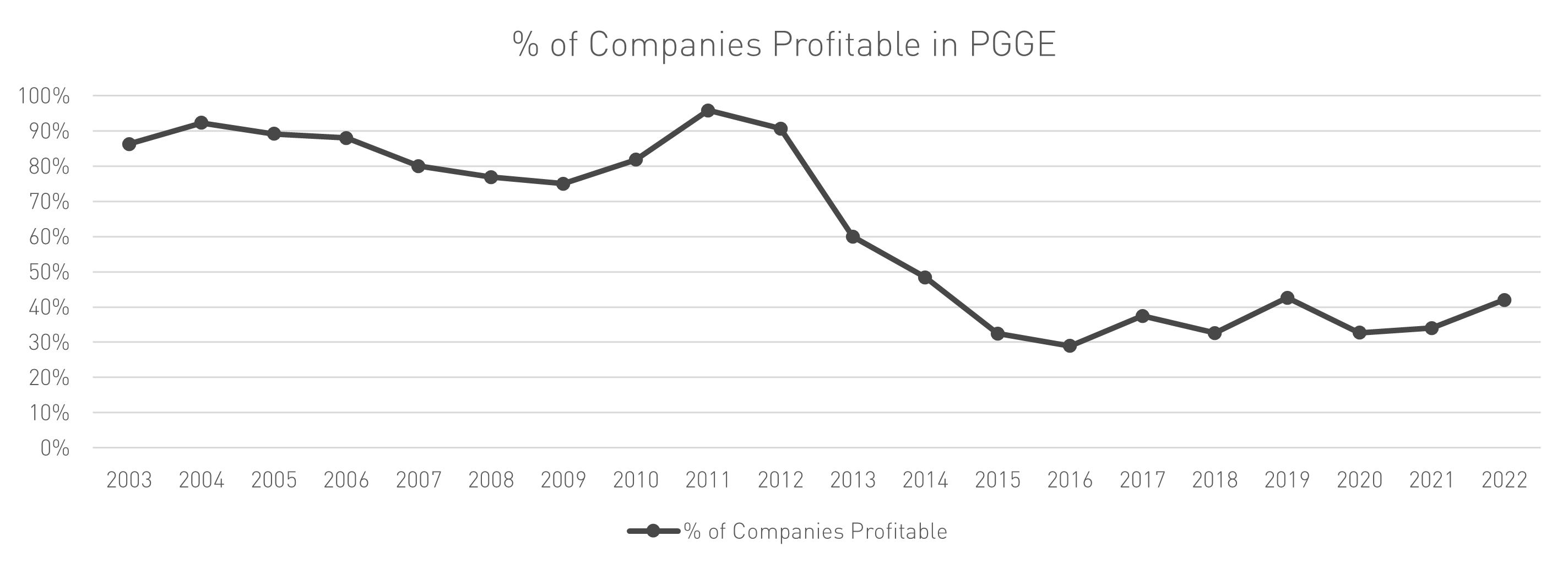

We looked at our indices to see how markets value EBITDA over the past twenty years. Below, we only show the PGMM Index and the IGV benchmark because, starting in 2012, profits somehow lost their appeal in the PGGE Index. What happened in 2012? Maybe, there were subliminal messages in the Gangnam Style video that swept the globe that year (what’s “go big or go home” in Korean?). While the trend toward profitability is returning, there are major trade-offs to growth on your path back to profits.

In the chart below, you can see that EBITDA is nicely rewarded and companies in the PGMM Index (recall this is any company in our universe of software stocks with at least 10% EBITDA margins and between 5% and 25% revenue growth) saw steady multiple expansion for over a decade. Not surprisingly, the index hit its low point during the Global Financial Crisis, at high single-digit EBITDA multiples. However, as we can see compared to the revenue multiple charts above, EBITDA multiples have not come down as quickly, still holding up at 20.5x trailing EBITDA even at what many consider “trough” valuations for software companies in the current market. And, if you believe that most software companies, even the profitable ones, are cutting costs, then either EBITDA multiples are coming down, or valuations of profitable software companies are going up (we think they’ll likely go up). Interestingly, today’s EBITDA multiples for the PGMM cohort are about the same as they were twenty years ago. Isn’t it nice when the market gives you an obvious target to price your private software acquisition? Somewhere safely below a number at which you could sell in the future, providing some possible multiple expansion at exit? And this is another good reminder that looking back further in the data helps inform decisions you could make today.

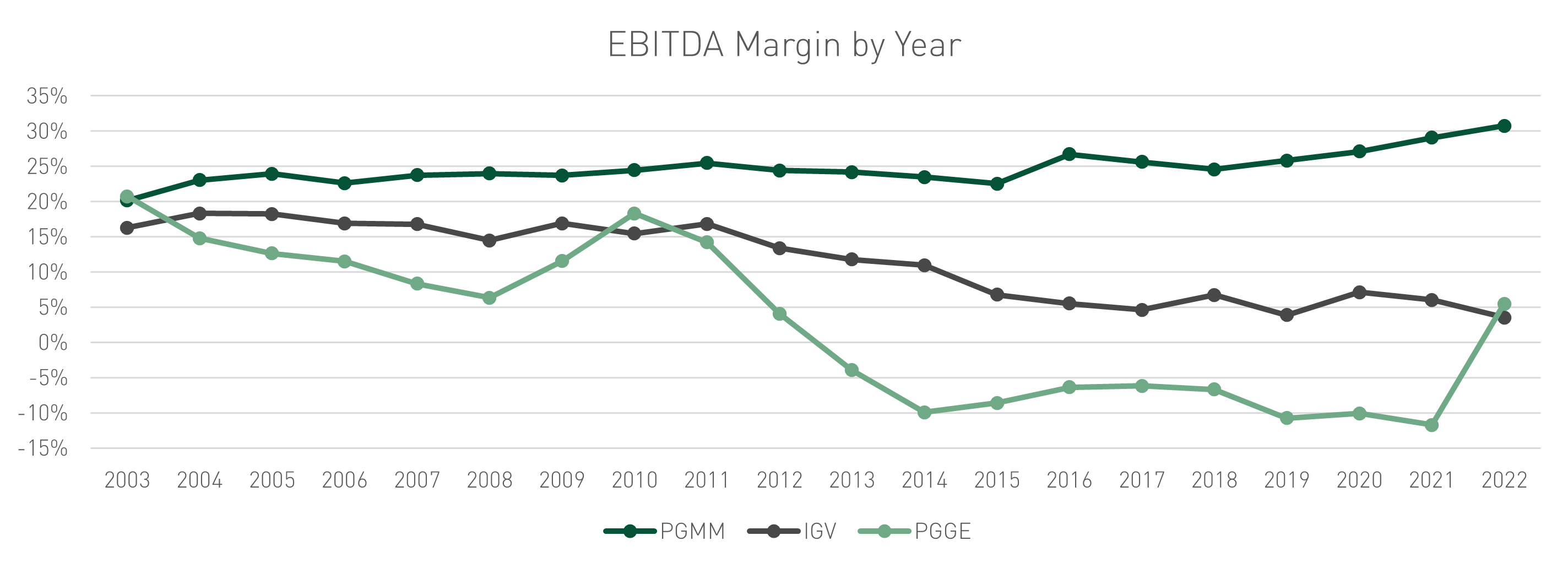

What about the profitability of those companies in the PGGE Index? We mapped the EBITDA margins on a yearly basis for both PGGE and PGMM to see the fluctuations. PGMM companies consistently delivered 20% to 30% EBITDA margins on average over the past twenty years, even during economic downturns. We acknowledge that our filtering on companies with at least 10% EBITDA margins would show consistent profitability, so we also applied our growth filters (5% to 25% revenue growth) without an EBITDA margin filter and still found that over the past 20 years, EBITDA margins averaged 16%. Growth names on the other hand, had positive EBITDA margins for the first ten years of our analysis but have been negative up until 2022. As you can see in the chart below, and it just reinforces what you are reading every day in the news lately, there is a shift toward profitability. After a decade of losses (on average) the PGGE cohort is finally lurching to break-even by the end of 2022. But at what cost to growth? We’ll find out soon enough.

Stock Performance

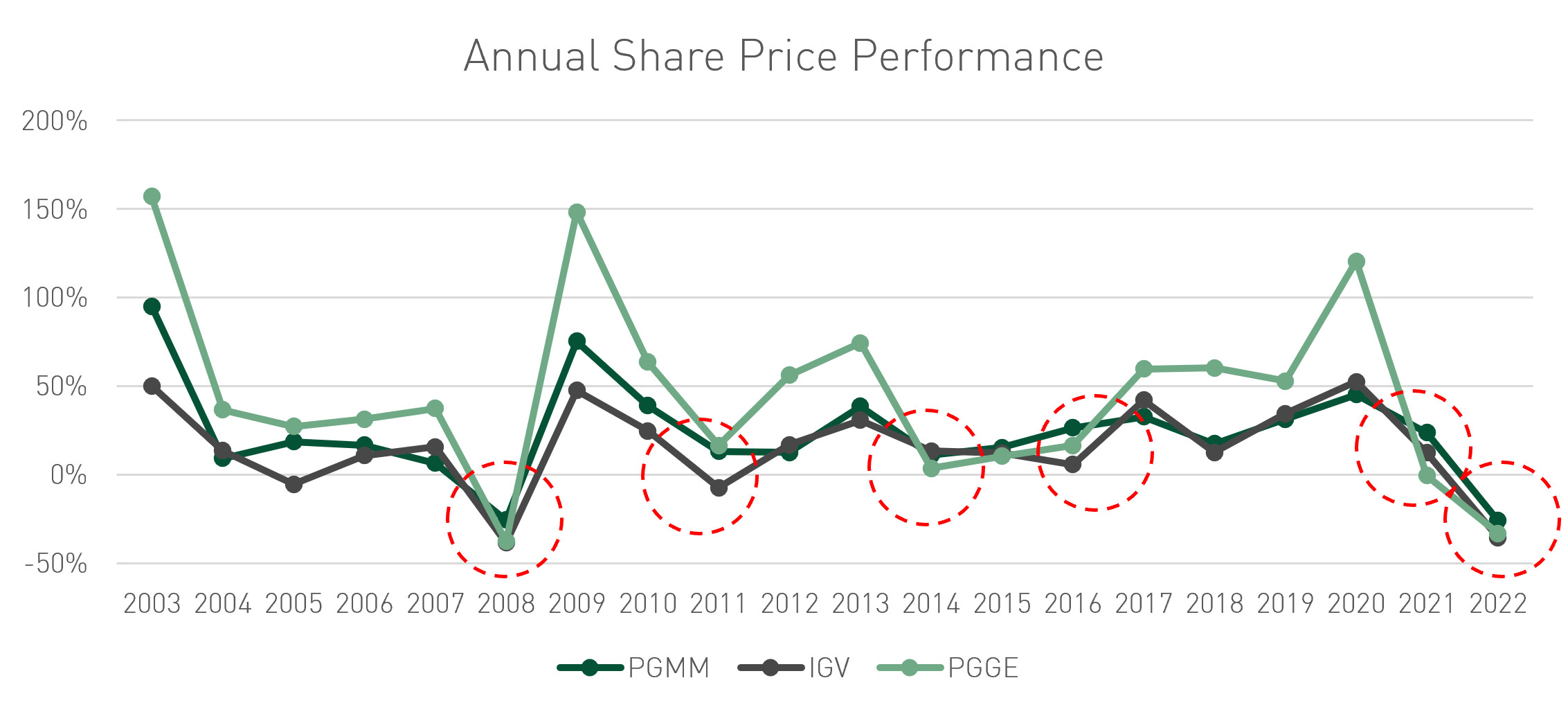

To see how investors rewarded these different approaches, we looked at the average annual share price performance for each index, by year. What jumps out to us is the consistency of share price performance for the PGMM Index. Keep in mind, this does not mean that you could buy the PGGM Index stocks at any time and generate a 20%-plus annual return. However, it does illustrate the lower volatility of PGMM compared to PGGE. Take 2022 for example. The PGGE Index was down 33% versus negative 26% for PGMM Index.

Let’s think about the ranges of revenue multiples that we discussed above. As we said, the PGGE Index had more upside from a revenue multiple perspective. And as you can see in our Annual Share Price Performance chart below, PGGE stocks generated a much higher return in peak years. Aside from coming out of the 2008 crisis, PGMM delivered smoother share price performance than PGGE. One attractive feature of middle market buyouts is consistency and predictability of the assets you buy. The sawtooth nature of the PGGE chart speaks to the emphasis on timing that is needed to generate those outsized returns from the PGGE names. Maybe we are old school, but as private equity investors, we think consistency is good and market timing is bad.

What Does This All Mean?

As investors, we get to choose the game we want to play and at ParkerGale, we have chosen a steady path with fewer bumps and divots. While roller coasters are fun to ride, we don’t think they should inform your investment approach. Remember we are private equity investors. In the public market, you can be in and out of a stock quickly if you see the company miss projections or if the stock price goes down. In private markets, you don’t have nearly as much control over the timing of exits given that it takes months to prepare and take a company through a sale process and by then, market values might have changed dramatically as we have seen over the past twelve months. We think the PGMM style gives us a steady path on a sunny day while the PGGE style (for us) feels more like Space Mountain: a roller coaster ride in the dark.

A momentum strategy with PGGE-type companies, can make you money, but you must weather the ups and downs and investors’ changing appetites for growth and profits. PGMM companies have demonstrated they can still grow in downturns and are more profitable on average, giving you multiple ways to generate returns (dividends, de-levering, etc.). The PGMM approach is less volatile than PGGE but could require longer investment horizons to allow lower revenue growth rates to compound over time. If you can time a PGGE approach accurately, you get the benefit of faster growth, increasing valuations, shorter holds, and likely higher IRRs. But you got to time it. The revenue multiples you see in the charts above speak for themselves. Over the past 20 years there were only two narrow windows to take advantage of the upside for PGGE stocks as compared to PGMM, which had a smooth, steady march upwards.

EBITDA is a great metric that buyout folk like to use, but it is more than a metric. One great feature of software companies compared to companies with more capital-intensive business models is that they can generate high profit margins and, if unprofitable, can quickly pivot to profitability if they make hard choices.

Over the past few years many PE-backed software investors used piles of increasingly available debt to help justify investment returns at historically high entry prices. While PGMM-type companies are not immune to the dangers of over-leveraging (with many software companies levered today at more than 10x EBTIDA), they can rely on their cash flow to cover the ever-increasing debt costs as interest rates continue to rise. PGGE type companies who raised debt, however, did so based not on EBITDA but on recurring revenue metrics and are now facing rising debt service levels that need to be funded with minimal (or no EBITDA). When your cash flow won’t cover your debt service, there are only three solutions – raise more equity, cut costs, go bankrupt. More equity hurts the return, especially in a declining growth environment. Cutting costs likely brings down your growth rate, which likely lowers your revenue multiple, which hurts returns. I don’t think we need to explain what bankruptcy does to your equity returns, though there are likely to be some lenders who own some pretty nice software companies over the next twelve to eighteen months.

Conclusion

2022’s valuation decline, and the challenges that follow, are just your regular reminder from the market of what happens when you pay peak entry prices and the market goes down. And when you use a lot of debt to make the return math work, and then the market turns on you like it just did, you are left with a long list of tough choices. We’ll have to wait to see how private investors re-value their portfolio companies based on the market decline. Some of that will be foisted on them as banks dust off their workout playbooks when rate adjustments work their way through low EBITDA private software companies with high levels of recurring revenue debt.

Software buyouts priced at peak values between 2020 and early 2022 that don’t have debt issues, will likely experience longer hold periods giving them time to grow back into their lofty multiples. And with declining growth rates, those hold period are going to be pretty long, making raising that next fund harder than it has been in a while. This will be quite the about-face for funds who delivered strong returns taking advantage of historically short hold periods over the past few years. How they, their portfolio company management teams, and LPs handle this whiplash will be telling.

While we think the shift from growth at all costs to a balance between growth and profitability, is a welcome change (and much healthier for shareholders and management in the long-run), it is not easy to pull off without negatively impacting the key metric on which private tech investors originally based their entire investment thesis – GROWTH.

This is the challenge facing public and private investors alike. But it is inevitable. If you paid 15x forward revenue for a company growing 40% a year and break-even, and now you must generate profits, it is very hard to maintain that growth rate. So, you’ve just paid a historically high entry multiple for a PGGE-type company that potentially gets valued in the future like a PGMM-type company on the exit. And the public market data we show above proves this out – in tough times, PGMM and PGGE valuations converge. Tough for PGMM company returns, but potential catastrophic for PGGE company returns. How this plays out is exactly what all tech-focused buyout and growth equity investors (and their LPs) are waiting to see. It will drive the returns of the recent fund vintages and GP’s abilities to raise funds at the size and pace they’ve become accustomed.

We hope sharing some of our own tools and opinions helps you think about Valuations a little better and adds to the conversation about what you should pay or where you could sell. We think taking a long view is instructive and helps smooth out some of the noise of this historic bull market we just lived through. If you are early in your investing career and this is your first downturn, we hope our analysis provides a different view on the software investing world. Hang in there. We can assure you that this, too, shall pass. And, we promise that you will learn more during this downturn than you learned during a bull market.

We will update these indices regularly so please check back in to see what the future holds. And we’d love to hear from you about our work. Please reach out and tell us what you liked, what we missed, and how we can improve.

For our next installment, we will look at small cap names (sub $2B market cap) to see how our analysis changes when we focus our analysis down market.

Disclosures

Actual financial data and estimates for the calendar year ending 2022 were pulled from FactSet as of 3/3/2023.

Investing involves risk, including the loss of all or a significant portion of amounts invested. Past performance is not a guarantee of future results.

The information contained herein is for informational purposes only and should not be considered investment advice. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitutes our judgment and are subject to change without notice. All information with respect to industry data has been obtained from sources believed to be reliable and current, but accuracy cannot be guaranteed. Certain economic and market information contained herein has been obtained from published sources and/or prepared by other parties and current as of the date of publication shown.