The Effects Of Low Interest Rates

The Effects Of Low Interest Rates

In my last article I explained why gold might be a good investment in 2024 (and probably also in the years to come) and why stocks should be rather avoided. We are looking at the development over the last fifteen years and how the world and financial system ended up here.

One aspect I mentioned in my last article were the extremely low interest rates. I wrote:

Aside from the extremely high debt levels around the world and the extremely high debt-to-GDP ratios, the zero interest rates we had for a long time and quantitative easing are also strong hints we are at the end of a long-term debt cycle.

Also last week, Howard Marks published another one of his memos titled Easy Money and one of the major topics of the memo were the extremely low interest rates and the effects these extremely low interest rates had in the last fifteen years.

In the following article we look at the low interest rates and what effect they have not only on the financial system but also on society as well as politics and how they are also responsible for some of the major problems we are facing right now.

A Few Simple Financial Basics

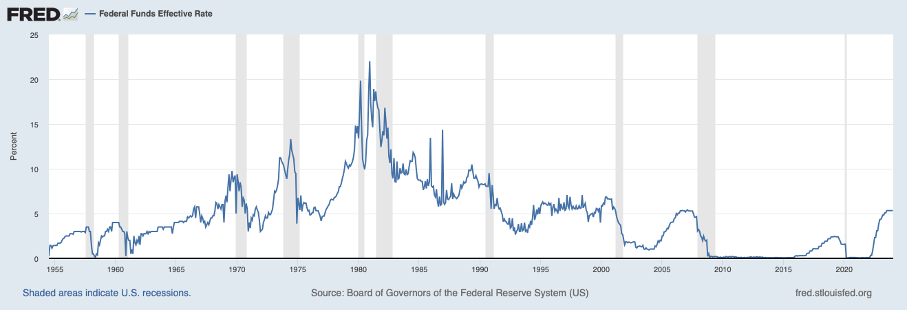

For starters, let’s look at the interest rates in the United States in the last few decades to understand why we are talking about extremely low interest rates. The following chart is showing the federal funds rate since the early 1950s.

In the chart we see not only the extremely long time of zero interest rates (between 2008 and 2015 as well as between 2020 and 2022) but we also must go back about 75 years to find another time of interest rates coming close to zero in the United States.

We can provide much more evidence, but I think the chart is enough to show that zero interest rates are rather seldom and certainly not the norm. And these extremely low interest rates are affecting the economy and financial markets in different ways.

Stimulating The Economy

First, central banks are using the tool of lower interest rates to stimulate the economy. With interest rates being lowered, opportunity costs are also being lower, and people are rather willing to spend money. If I get lower interest on my savings account, I might have less motivation to save the money and rather spend it on goods and services. And especially if I get zero interest on my savings, opportunity costs for spending the money are also zero (at least in the short term). Marks is writing in his memo:

„For example, if someone’s thinking about taking $1 million out of savings for a purchase at a time when savings accounts pay 5% interest, they’re likely to understand that doing so will cost them $50,000 per year in forgone income. But when the rate is zero, there is no opportunity cost. This makes the transaction more likely to occur.“

Rising Asset Prices

And while people use money, that is not generating any interest in a savings account, to buy goods and services, many are also buying financial assets like stocks or real estate to chase higher returns. These assets not only promise higher returns but are usually also associated with higher levels of risk. The problem is that these risks are often ignored in times of zero interest (we will get to this).

And as more and more people are chasing assets that promise a higher return, more and more capital is flowing towards these assets leading to rising asset prices. And other people are observing these rising asset prices – confirming that these assets are obviously a great investment. This is leading to even more people investing in these assets, leading to even higher asset prices. This is creating a feedback-loop that can push asset prices for these assets higher and higher and we are looking at a kind of self-fulfilling prophecy.

Howard Marks once again:

„In this way, capital moves out of low-return, safe assets and in the direction of riskier opportunities, resulting in strong demand for the latter and rising asset prices. Riskier investments perform well for a while under these conditions, encouraging further risk taking and speculation“

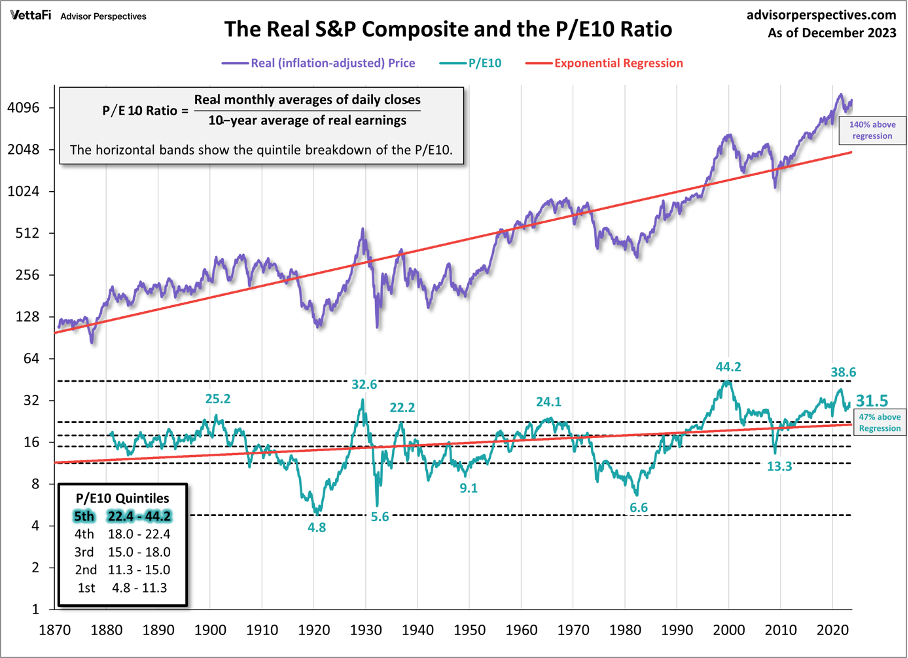

And that asset prices are rising too much (and that these rising asset prices are not justified by fundamentals) can be shown by looking at reported CAPE ratios. When looking at the situation in the United States once again, we see CAPE ratios only witnessed in the quarters around 2000 and 1929.

Rising Debt Levels

And due to low interest rates people are not only spending cash instead of saving it, people are also taking on huge amounts of debt – as the (opportunity) costs for taking on debt are also low. This leads to higher and higher debt levels – not only for individuals (households) but also for states and corporations.

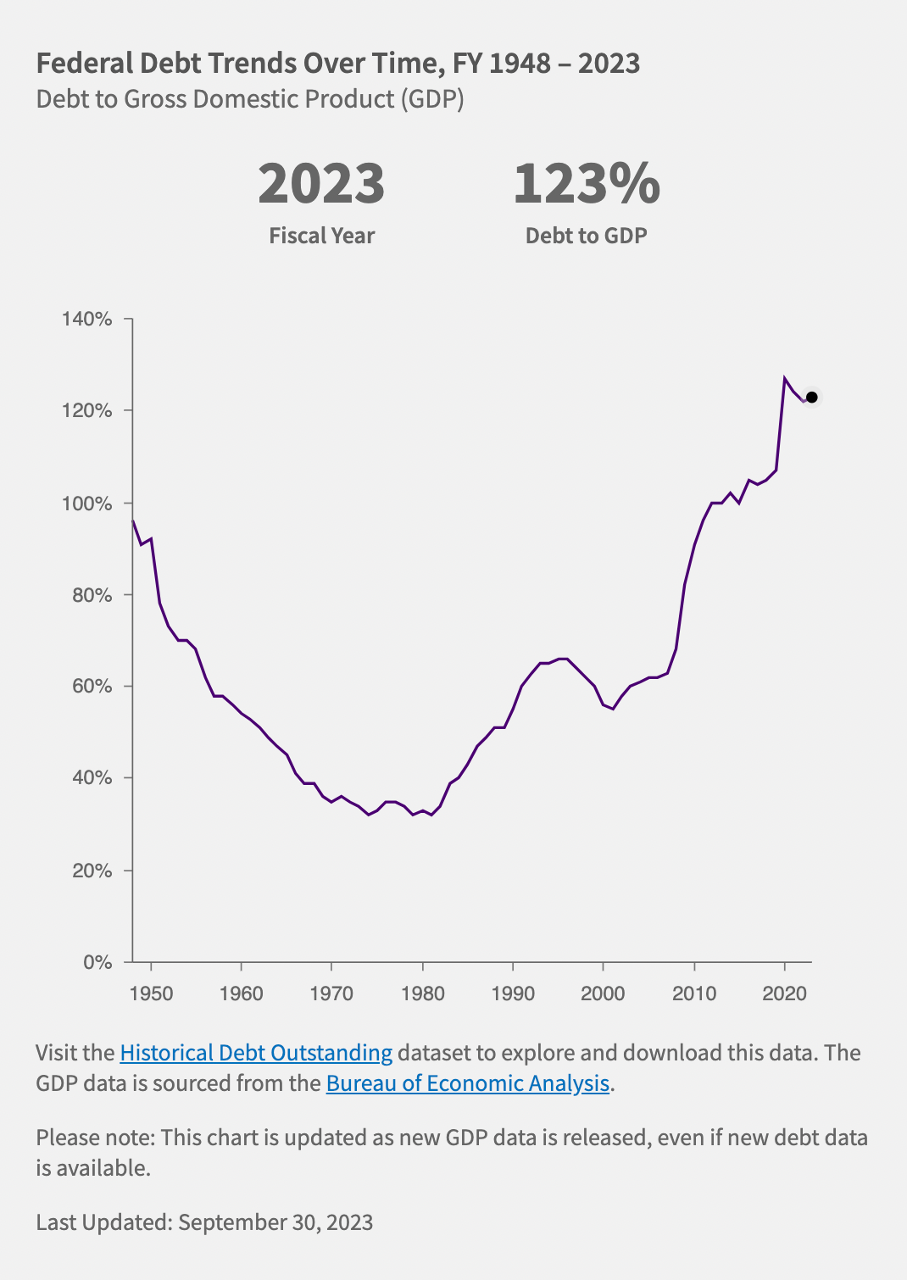

And when looking at global data, we see constantly rising debt levels, but we don’t see such an extreme increase in the last 10-15 years. However, when looking at the United States and the U.S. government debt-to-GDP ratio we see a huge increase since the Great Financial Crisis.

Messing Up The Psychology of Investors

Not only have low interest rates an impact on asset prices and debt levels, but it also has a huge impact on investor psychology and behavior. We already mentioned above that low interest rates lead to increased spending. But there are more psychological ways how low interest rates influence investors.

Unnecessary Risk Taking

Low interest rates make it difficult for investors to achieve meaningful returns and in a search for higher returns, investors are usually taking additional and unnecessary risks. In this context, Howard Marks mentioned the concept of “malinvestments” – a term popularized by Friedrich Hayek. The term is describing the idea that in a low interest environment, investments are made that should not be made. And usually, investments are made for a long-time horizon (investments or projects that might take decades to lead to real gains or profitability).

Marks is also providing some examples like investments in scams happening more and more (major examples might be Theranos and FTX) or investing in 100-year bonds issued by Argentina, a country that defaulted several times in the past century (and also defaulted again since issuing the bond).

And in such an environment investors and companies usually take on more debt than they should and are using leverage – a combination that can becomes extremely dangerous when rates are suddenly rising.

Expectations of Continued Low Rates

But another problem that arises in low interest rate environments is the expectation of investors that low interest rates will continue for a long time. And in 2024 we can already state that investors learned the hard way this is not true and in 2022 and 2023 we saw the fastest rate increase cycle in the last few decades, which caught several investors by surprise.

Additionally, investors also expect continuously increasing asset prices – and that expectation is still alive and well. Especially as many investors can’t even imagine anymore that asset prices might decline – the conviction that the FED will save the stock market again and again seems to be deep-rooted right now.

And similar to the years 1928 and 1929 where we can find some – in hindsight – very funny quotes about the bull market never ending and the economy never seeing another shock again, I assume future generations will also look back at 2023 and 2024 and find similar funny quotes.

Messing Up The World

So far, we talked only about financial aspects and how low interest rates have an impact on investing and investors. However, low interest rates also have an impact on other social systems and impact society and social development.

As Howard Marks also pointed out in his memo, low interest rates lead to increasing asset prices (stocks and real estate) and usually the already rich are holding more stocks and own real estate -exacerbating the already existing inequality. While “the rich” get richer by holding stocks, the rest of the population (especially the low half) is even penalized by rising prices and no interest in their savings account. Ray Dalio is talking in his book Principles for dealing with the changing world order about the conflicts within countries escalating as a strong hint for being near the end of the cycle.

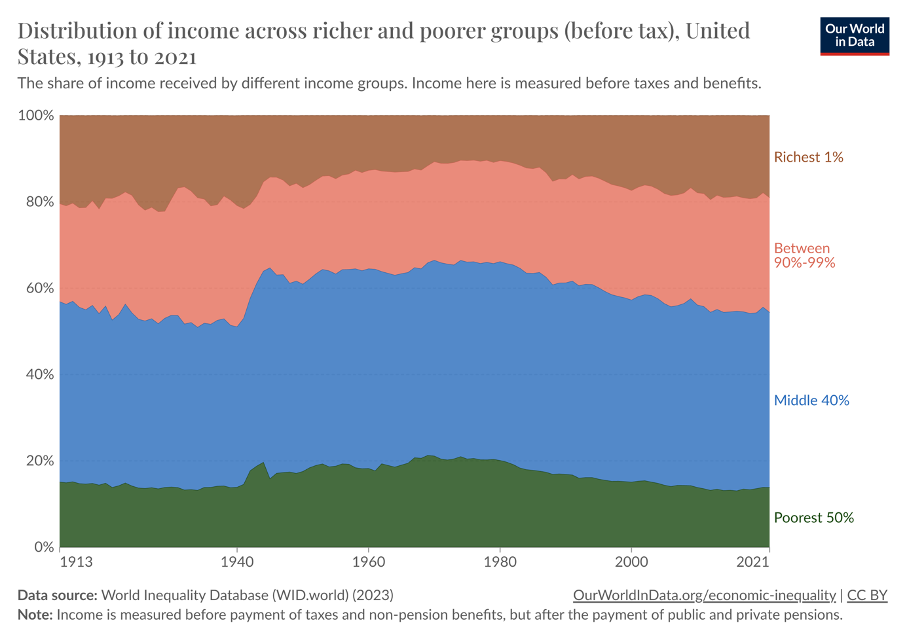

When looking at the United States – and many other countries are showing a similar picture – the richest 1% hold 19% of wealth while the poorest 50% hold only 13.8% of wealth combined.

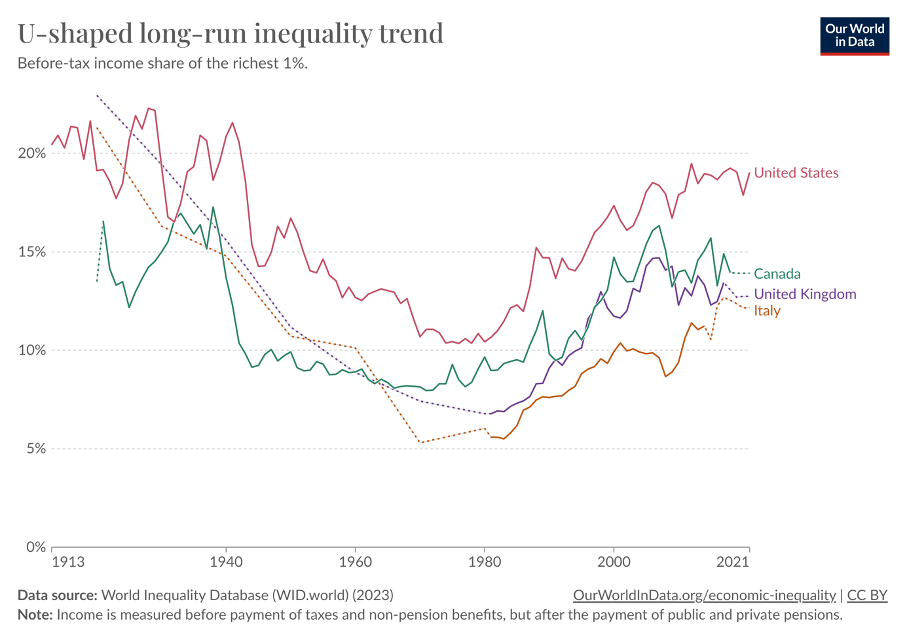

And when looking at different countries we see the before income tax share of the wealthiest 1% rising since the late 1970s or early 1980s. Joe Hasell is writing:

„From the 1980s, inequality began to rise again in many high-income countries, tracing a ‘U-shaped’ pattern over the past 100 years. The US is a clear example of this, as shown in the first chart. After a sustained rise over the last 40 years, before-tax inequality in the US is roughly at the same level today as it was a century ago. The US data is shown along with three other countries that saw substantial rises in inequality in recent decades: Canada, the United Kingdom, and Italy.“

Making it difficult for ordinary people to make ends meet as prices for everyday products rise faster than incomes and real estate is so expensive that ordinary people not only have to say goodbye to the dream of ever owning a house, but rent is also taking a much bigger part of the monthly income making it more and more difficult to have enough money for other necessities – not to mention a vacation or other “small luxury”.

And with internal conflicts within a country rising, usually external conflicts are also rising. We can already see rising conflicts and although this is often subjective the risk of war is increasing. While most European or U.S. citizens still can talk about the risk of war, Ukraine, Israel, and Sudan are already facing deadly wars.

Implications For Investors

At this point it seems important to point out again that nobody knows what will happen and like everybody else I don’t have a crystal ball. We only have to acknowledge that we are seeing several patterns again that lead to the so-called Great Depression in 1929 in the United States (and many other countries around the world) and to another financial crisis in the late 1980s/early 1990s in countries like Sweden, Norway or Japan.

And although we never know what will happen, we should prepare for scenarios that seems likely or plausible and in the following weeks I will talk about what could happen in the years to come and how we could prepare (so far as it is possible).