Founder secondaries, VC exposure to crypto and Twitter takeaways

Founder secondaries, VC exposure to crypto and Twitter takeaways

Stretch Four Insights Volume 44

This newsletter is brought to you by Future.

This week I hit all my scheduled workouts and my body is feeling it. It only makes sense to stay active during the holidays and Future makes this easy and realistic. As November comes to an end my trainer and I will start to plan for what 2023 will look like as I have some big goals on the health and fitness front. This week I hit some big strides and was able to hit 42 inches on the box jumps for 25% of my set. This is progress for me as I don’t believe I have hit that number since my college days. Start off the new year with Future and join me on my fitness journey.

Want to sponsor a newsletter or deep dive? See our sponsorship information here.

Happy Saturday,

Welcome to all the new subscribers who are joining me through Twitter. This week I will break down what data I used to write my now viral tweet about Tribe Capital. Thanks for subscribing. I am a two-time venture-backed builder (ModernTax) who writes weekly about things happening across my industry (fintech, and tax related technology factors), sometimes NBA, and general founder and the startup eco-chamber type stuff.

With Thanksgiving and Black Friday behind us it is only downhill from here until 2022 becomes a thing of the past. Many of us in tech, whether we are founders, operators, or investors, are likely looking forward to that. It’s been a grueling year for the industry for many reasons.

I enjoyed this tweet from David Serna with the Founder’s Podcast and this is how I am approaching 2023:

This week I was back home in San Francisco and we celebrated our first Thanksgiving with our son, Cain, here in the Bay area with family.

This week’s newsletter will highlight:

Are founder secondaries a thing of the past?

A $1.5 billion venture fund that might overly exposed in the crypto bear market

Are larger than life good storytelling founders ruining it for everyone else?

Let’s dive in.

Quote of the Week:

“Will it make the boat go faster?”

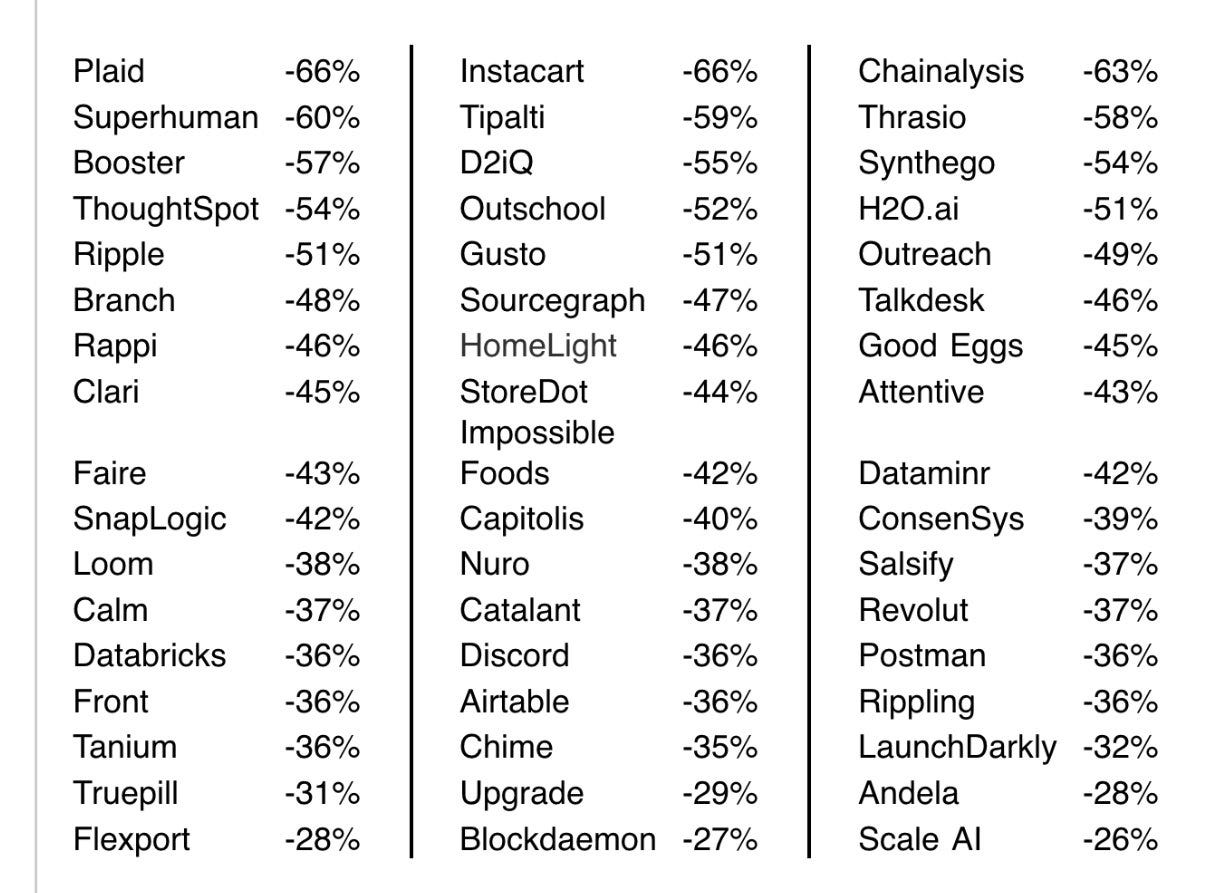

Chart of the Week:

Tweet of the Week:

This was one of the most viral tweets of the week and had me thinking a lot about weight loss, lifestyle, and supplements moving in to the new year. I also talked to my 80 year old uncle this week and he reminded me, “you don’t see a lot of overweight old people.”

Twitter Takeaways

Jumping right into a tweet of mine that got some pretty interesting engagement on Twitter this week.

My reasoning for this tweet related to Tribe Capital, a fairly outspoken “differentiated VC” being involved in the three companies mentioned.

First some backstory. Pipe was in the news this week after all three founders abruptly stepped away from the company citing lack of experience in fintech. Bolt, which I wrote about here in May, has come under scrutiny as the founder and former CEO stepped down in February — and the company has been in flux ever since. I need not mention why FTX was mentioned in the tweet.

Tribe Capital is ran by Arjun Sethi and is an offshoot of Social Capital, ran by Chamath Palihapitiya. Tribe publicly shares on their website that they have exited Pipe and they have written off both FTX and FTX US, but they do consider Bolt as an enduring high performer in their portfolio as they list it as a company worth ~$2-5B. While this valuation is not only down significantly from the Series D valuation raised in October 2021 it may be worth even less if it went to the public market.

Startup investing is brutal right now

Full disclosure, it’s hard to build startups and make money in venture in general, but from the summer of 2020 until the spring of this year everyone looked like a genius. Tribe Capital along with many other venture firms capitalized during that cycle and likely deployed large amounts of capital. It became easier for some founders to raise large amounts of capital at high valuations, and it became easier for venture capitalists to mark up their investments to raise larger funds and charge higher management fees and they took advantage.

Tribe was able to deploy a massive amount of money during this time period and everything looked amazing on paper especially their crypto bets. I would hope they exited some positions but according to their own reporting they only realized investments in five companies total.

This year as the market has cratered and we have seen some of those white-hot companies from the past two years come crumbling down things have gotten quite a bit rockier, sans a VC getting testy on Twitter. Fast, Bolt, Pipe, FTX among others have in some cases completely shut down and in other cases the founders have stepped away after raising massive funding rounds at sky high valuations not even six months earlier in some cases.

On the venture side, Tribe is one of the most active crypto investors and while I am sure Arjun and the Tribe team feel confident about their positions the top of their portfolio is highly overexposed to crypto.

Three of their top four investments, by valuation, are all crypto companies and with Coinbase being the only publicly traded comparison with $10 billion valuation I highly doubt Kraken, ConsenSys, and Digital Currency Group would fetch valuations anywhere close to that in any market. Even in the second tier of companies Tribe counts as its most successful you see even more crypto exposure with both Binance and Moonpay.

Final Thoughts

The other underlying theme here that mostly no one knows what they are doing and many of us as founders and investors are all trying to learn what is happening in real time. In 2021, everyone was an expert, up rounds were happening daily, IPOs were a real thing. This year not so much. The other not so obvious thing from my view as a founder is that a large majority of these startups are founded by the charismatic, predominantly white male, founders and not surprisingly these were the founders able to raise at astronomical valuations on their terms last year. As the bills are approaching and these companies are not growing as fast as they were initially they now need to raise more money as many of these same founders are stepping away.

Founders taking secondaries comes under fire.

The past few weeks have been brutal for technology and venture-backed founders. Elizabeth Holmes was sentenced to over eleven years in prison. SBF was exposed for cashing out $300 million in secondary in a round of a little over $400 million after essentially being responsible for losing nearly $8 billion in customer’s money being held with FTX. This week, three founders stepped down from once buzzy unicorn startup Pipe, which made a name for allowing software companies sell their annual contracts for upfront advances. While there are no confirmations, there are assumptions that the founders were able to take large secondaries considering the company raised more than $300 million in debt and equity over a two year period and at peak reached a $2 billion valuation.

There is nothing illegal about taking secondaries and it has been encouraged in some cases, considering a founder wants to start a family, buy a home, or has a specific need for a family member. It also can give founders more incentives to stay in the game for the long haul and go the distance versus selling early, but the diligence likely goes up as venture capitalist now have more power thanks to the frothy markets and the examples of founders taking advantage of the benefits.

What’s Next

December is around the corner which means 2022 is nearly a thing of the past. This year has seen highs and lows and planning for 2023 will be critical on both the business and newsletter front and I am working on some formats.

As always, I would love your feedback especially if you are new please email me at matt@stretchfour.co

Back to the trenches.

Best, Matt