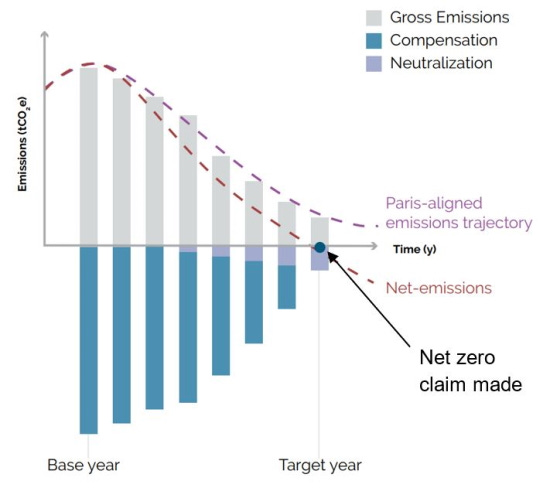

Carbon Credits from the Voluntary Credit Market

Carbon Credits from the Voluntary Credit Market

(Part 1/N) – Types of Credits

Considering another COP (n+1) meeting is currently wrapping up, let’s explore the ever evolving and changing global carbon credit market / regime / scheme

We know trying to understand the carbon credits markets is extremely exhausting but also very important. The Voluntary Credit Market (VCM) is slowly becoming the bedrock of achieving net zero for many corporations and nations, but due to the opaqueness of markets and lack of consistent frameworks, you may honestly be paying some guy in New Jersey not to cut his bushes for a year.

So, in this piece, let’s start with some basic terminology around type of credits and build from there:

Types of Credits:

Offsets:

Carbon Credits based on an “offset” is paying for someone else to do “good”, meaning choose a low-carbon choice. The credit seller or issuer sells a credit representing the offset between the higher NPV (Net Present Value) / Higher Carbon Decision and the lower NPV / lower carbon decision. The value of the credit should be the offset to make the lower NPV decision comparable to the higher carbon decision.

The intrinsic value of these offsets should be the following, assuming no friction (Txn Fees / Middlemen)

Pitfalls of offset-based credits:

A large issue with offset based credits is the economics of the high NPV project are not clearly defined, declared or even intended, meaning there is no real “offset”. Therefore, the buyer is theoretically providing a subsidy

a. Examples:

i. The issuer had no intent in doing the alternative, such as issuing credits to ensure a forest is not cut down, but there was never an intent to cut the forest down to begin with

ii. Building a renewable energy facility which increases overall generation capacity; while potentially beneficial in the long-run, the new facility is not removing or offsetting any existing emissions

Accurate Cost of Capital or Discount Rate: Accurately reflecting the geographical and geopolitical risks into the cost capital

Project Projections vs. Project Reality: Does the carbon offset perform as intended. These efficiency issues are expected for almost all projects, but does the project NPV account for leakage

Positives of offset-based credits:

Providing capital to remove existing high-carbon-emitting, positive NPV projects and assets from the market:

a. Examples:

i. Forcing the early retirement of a hydrocarbon-fueled power plant, the remaining NPV of the plant at the time of early retirement is funded through the issuance

ii. Funding the repair or replacement of high-emitting infrastructure

Creating a funding conduit for low or no carbon-based products

a. Examples are ubiquitous: From CPG products such as soap to durable goods such as vehicles

Removals:

Carbon credits based on a “Removal” are providing capital for the removal of CO2 from the atmosphere, either through a natural approach, such as planting trees, or through a physical (mechanical / chemical) process, Carbon dioxide capture and sequestration (CCS). The theoretical value of the credit should be the cost of removing a ton of carbon from the atmosphere.

The intrinsic value of these removals should be the following, assuming no friction (Txn Fees / Middlemen):

Pitfalls of removal-based credits:

Like “offsets”, credits sold from a removal project may be coming from an existing asset, such as an existing forest or wetland, while the removal of carbon may not be questionable, whether the removal provides additionality might be uncertain (Did the credit fund an actual reduction or just provide a subsidy to an existing project?)

Removal costs vary considerably, so theoretical prices per ton can vary considerably based on type and vintage (year of credit creation). The wide-ranging cost per credit may create perverse incentives towards focusing on lower cost solutions

Carbon Storage for natural and physical solutions have known leakages [e.g. trees can burn, and physical carbon storage can leak (pipes, tanks, geological structures)]

Accurate Cost of Capital or Discount Rate, accurately reflecting the size, geographical and geopolitical risks

Positives of removal-based credits:

Provide Capital allocation to high cost, high risk, but potentially scalable removal methods (will dive deeper into this in a later article.)

Removal-Based Credits are arguably the “real” credits; certain investors, marketplaces and buyers are not interested in offsets due to a potential lack of additionality and don’t want to allocate capital unless they have a high conviction the credit will remove carbon from the atmosphere

While the methods and means of offsetting and removal continue to grow, understanding whether a credit is worth purchasing requires significant diligence, we will continue to explore many of these different ideas in future pieces (and videos).

Sources: