Economic & Housing Update Jan 27, 2023

Economic & Housing Update Jan 27, 2023

Stronger than expected housing data as inflation and rates ease meet a slowing economy

Summary:

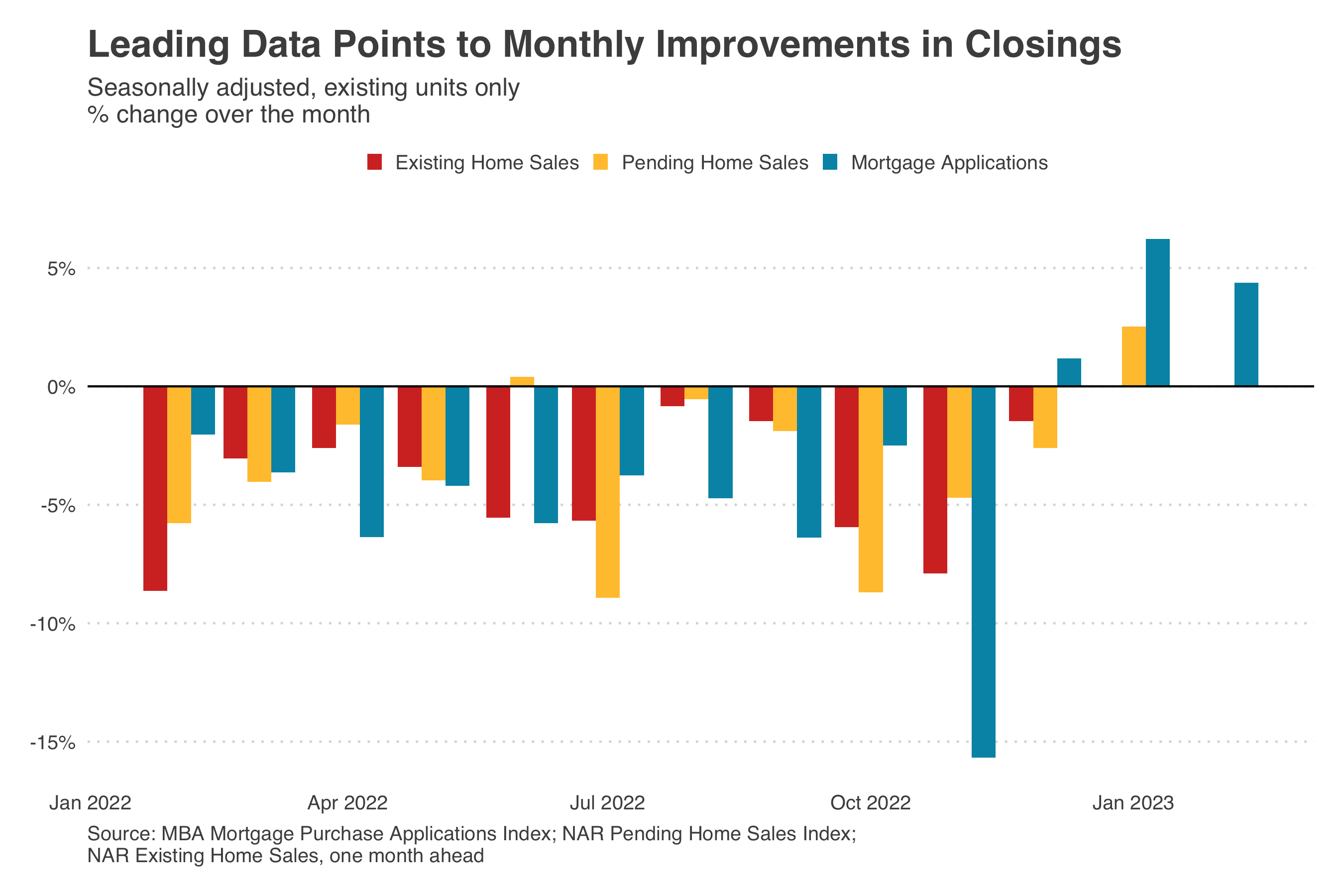

Mortgage rates ticked down to 6.13% to their lowest level since last September as MBA’s Purchase Index continued to increase another 3.4%. The index is 28% above November’s trough.

Pending home sales unexpectedly rose 2.5% month-over-month in December of 2022, the first rise since May, and beating market forecasts of a 0.9% drop. Meanwhile, pending sales of new single family houses also increased 2.3% in December. However, new permits for single-family homes continued to decline 6.4% last month.

Economic growth slowed to 2.9% (annualized) at the end of last year (Q4), but at a rate far from recessionary alongside 3.5% unemployment. However, consumer spending pulled back in December pointing to much slower growth to start 2023. The Fed’s preferred gauge of inflation shows further cooling in December as well to 4.4%.

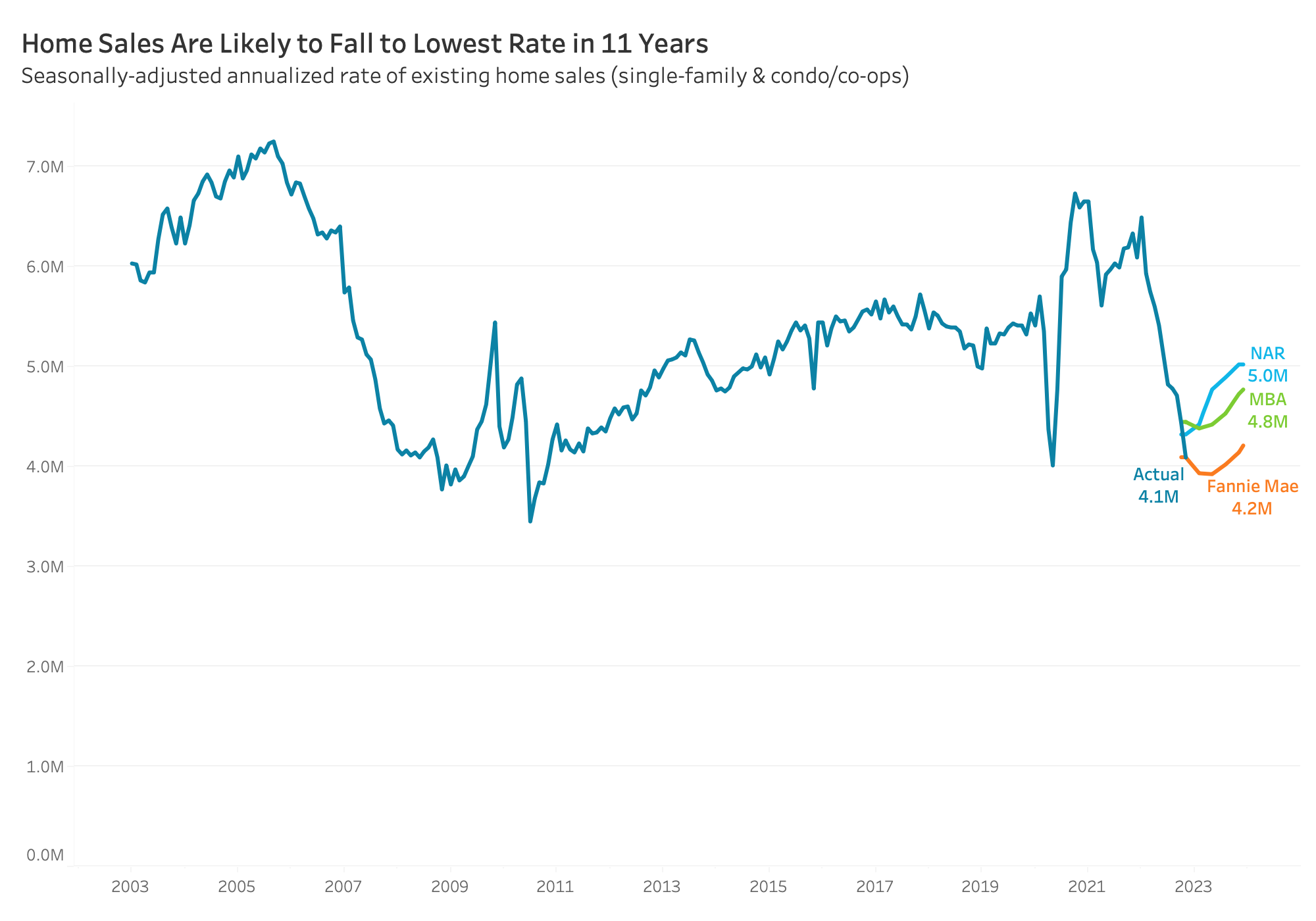

Mortgage rates continue to tick down this week, which further fueled the rebound in housing activity—most notably that mortgage applications are now up 28% from their November trough. Similarly, NAR’s pending home sales data today increased 2.5% in December—well above the expected 1% decline and predicted by Redfin’s pending sales data earlier in the week. November’s contracts were revised up as well bringing December to a 4% bump over the original release. Together, these data points indicate future increases in NAR’s existing home sales for both January and February by a few percentage points (see chart below). Although December 2022’s home sales were 38% below January’s, it most likely marks the bottom at 4 million existing home sales.

The housing market’s improvement builds upon the moderation in mortgage rates over the past few months. So why have mortgage rates been declining? There are a few reasons for this, but two of the biggest drivers are slowing economic growth/recession fears and better than expected progress on inflation. This week we learned that the economy grew by 2.9% in Q4 last year. This was not only faster than expected, but a far cry from a recession. However, GDP growth is slowing and monthly consumer spending data shows a turning point throughout the quarter. The economy is now expected to slow to less than 1% in Q1 of this year and recession risks are still present despite an extremely tight labor market—jobless claims hit a four month low this week.

Inflation has also continued to show strong progress. Of the several measures of inflation, the Fed’s preferred gauge of inflation (core PCE) shows further cooling in December as well to 4.4%, though still well above their target of 2% (see chart below). The FOMC will meet next week to certainly (99% odds) hike the Federal Funds Rate another 25 basis points to 4.5% - 4.75%. Hopefully, they confirm one final 25 basis point hike in March expected (or a 1 in 6 chance they pause). If inflation continues to moderate at this pace or recession flags begin to emerge, then there could be more movement down in mortgage rates.

New housing data:

The MBA Purchase Index continued to increase another 3.4% to 205.4 in the week ending January 20, 2023—to the highest level since August 10 as mortgage rates fell for the 3rd week as well to the lowest rate since September. The unadjusted Purchase Index was still 39 percent lower than the same week one year ago. The adjustable-rate mortgage (ARM) share of activity decreased to 6.5 percent of total applications as the rate on an ARM increased to 5.44, narrowing the spread against the 30-year fixed rate.

Mortgage rates ticked down to 6.13%, their lowest level since last September, which will continue to support a recovery in housing demand. Their 95 basis point decline since November’s peak is the fastest pace of decline since January 2009.

Building permits fell 1.0 percent from a month earlier to a seasonally adjusted annual rate of 1.337 million in December 2022, revised data showed. It was the third consecutive monthly decline in permits. Single-family authorizations declined 6.4 percent to a rate of 731 thousand, the lowest since April 2020, while the volatile multi-segment rose 6.3 percent to 606 thousand.

Sales of new single family houses increased 2.3% month-over-month to a seasonally adjusted annualized rate of 616K in December of 2022, the highest value in four months, compared to market forecasts of 617K. Sales soared in the Midwest (35.2% to 73K) and the South (6.5% to 392K) but fell in Northeast (-19.4% to 29K) and the West (-15.3% to 122K). The median price of new houses sold was $442,100 while the average sales price was $528,400. There were 461,000 houses left to sell, the same as in November corresponding to 9 months of supply at the current sales rate. Considering full 2022, an estimated 644K new homes were sold, 16.4% below the 2021 figure of 771K, and the lowest levels in four years, due to rising mortgage rates.

Pending home sales unexpectedly rose 2.5% month-over-month in December of 2022, the first rise since May, and beating market forecasts of a 0.9% drop. November estimates revised up as well, so December was 4% above the original November estimate. Sales were up in the South (6.1%) and the West (6.4%) but fell in the Northeast (-6.5%) and Midwest (-0.3%). Still, year-on-year, pending home sales sank 33.8%. “This recent low point in home sales activity is likely over. Mortgage rates are the dominant factor driving home sales, and recent declines in rates are clearly helping to stabilize the market. The new normal for mortgage rates will likely be in the 5.5% to 6.5% range”, said NAR Chief Economist Lawrence Yun.

New economic data:

The number of Americans filing new claims for unemployment benefits fell by 6,000 from the previous week to 186,000 on the week ending January 14th, the lowest in four months and well below market expectations of 205,000. The 4-week moving average, which removes week-to-week volatility, fell by 9,250 (4.5%) to 197,500. Continuing claims ticked up further to 1675 thousand in the week ending January 14, 2022.

The US economy (GDP) expanded an annualized 2.9% in Q4 2022, slowing from a 3.2% jump in Q3, but beating forecasts of 2.6%. Consumer spending rose 2.1%. Spending on goods jumped 1.1% (led by motor vehicles) and spending on services slowed (2.6% vs 3.7%), with health care, housing and utilities, and personal care services leading the rise. Meanwhile, private inventories added 1.46 pp to the growth, after a drop in the previous two quarters. On the other hand, the contribution from net trade declined (0.56 pp vs 2.86 pp in Q3), as exports fell 1.3% and imports went down 4.6%. Residential investment continued to contract (-26.7% vs -27.1%), led by new single-family construction and brokers' commissions. Considering full 2022, the GDP expanded 2.1%.

Personal income went up 0.2 percent from a month earlier in December of 2022, following a downwardly revised 0.3 percent increase in November and in line with market expectations. It was the smallest gain since April. The increase primarily reflected increases in compensation and proprietors' income. The increase in compensation reflected increases in private wages and salaries in both services-producing industries and goods-producing industries. The increase in proprietors' income reflected an increase in nonfarm income that was partly offset by a decrease in farm income.

Personal spending dropped 0.2% month-over-month in December of 2022, worse than market forecasts of a 0.1% fall, and following a revised 0.1% decline in November. High-interest rates and rise in inflation levels started to impact consumer behavior. Spending fell on goods, namely gasoline and motor vehicles and parts and services, mainly housing, air transportation and health care. Adjusted for inflation, personal spending dropped 0.3%.

The core PCE annual rate, which is the Federal Reserve’s preferred gauge of inflation, fell to an over one-year low of 4.4% in December of 2022 from 4.7% in the prior month, in line with market forecasts. Core PCE prices went up by 0.3% month-over-month in December of 2022. Meanwhile, the headline index edged up 0.1% last month, the same as in November. In the 12 months through December, the index increased by 5.0%, the least since September of 2021, and below 5.5% in November.

The University of Michigan consumer sentiment was revised higher to 64.9 in January of 2023, the highest since April, from a preliminary of 64.6. The gauge for expectations was revised higher to 62.7 from 62 while the current conditions subindex was revised lower to 68.4 from 68.6. Meanwhile, inflation expectations for the year were revised lower to 3.9% from 4% in the preliminary estimate and the 5-year outlook was revised lower to 2.9% from 3%. Their data also pointed to the worst conditions for buying a home in more than four decades.

Have a great weekend,

Taylor Marr