LL Flooring Holdings, Inc.’s (LL) Wide Deal Spread:

LL Flooring Holdings, Inc.’s (LL) Wide Deal Spread:

A Tale of Legacy Issues, Questionable Management, and Uncertain Future

As of 11/27/2023

Close price: $3.29

Highest Cash-out bid Price: $5.85

Upside: +75% if management accepts & locks-in Live Venture Inc. deal

Expiration Date: TBD

Non-binding Acquisition Proposal

LL 0.00%↑ 3 Month Trade Chart

LL Flooring Holdings, Inc. (LL 0.00%↑) has received several bid offerings to be acquired by potential strategic buyers. The initial deal announcement was made earlier this year by the former CEO, Thomas Sullivan, through F9 Investments. Then, a consortium led by Howard Jonas, CEO of IDT Corporation (a bit more on him if interested) came out in support of F9 Investment's $5.76 bid. As you know with any entrenched board and management, inept foot dragging brought us to an unsatisfactory Q3 deteriorating business result leading F9 to subsequently rescind their offer.

After a few weeks, F9 returned with a significantly lower bid of $3.00 per share versus $5.76. The latest 13D filing was released a week ago. There is a chance that the recent market turbulence/sell-off will make the shareholders change their minds. If the deal breaks, the downside would be significant. Oddly, F9’s new lower bid was done only after a new strategic buyer entered after management announced they have initiated a strategic review from the August 2023 Q3 earnings call.

Part of the spread might be explained due in part to investor apathy from management's intentional disregard for updating shareholders about the strategic review they announced three months ago in August 2023.

The main concern is that management remains silent about their announced strategic review process and continue to lack any significant updates or talks between Live Ventures Inc. that could potentially result in the cancellation of yet another buyout offer due to ineptness. The question investors should be asking is what strategy is management employing that would see LL 0.00%↑ stock up +80% in the next year?

Ok let’s allow for management’s argument stating they have a long term strategic plan. So what 3 to 5 year perfect plan does management have that requires shareholders to wait for their total return of +80%? Any plan that management has to see the stock significantly higher and above $5.85 that Live Ventures is offering today to buy the company? The math is very simple and it’s obvious. Charles E Tyson, management and the board want shareholders to make assumptions that their rejections for these buyout offers are about self serving job security than maximizing shareholder value.

Events of Import:

7/5/2017: LL stock closed at $25.40.

‘Serial entrepreneur’ moves on from Lumber Liquidators Thomas Sullivan, the founder and former chairman of Lumber Liquidators, the wood flooring retailer — left the company on Dec. 31 under pressure.

9/5/2019: LL 0.00%↑ stock closed at $11.58.

Lumber Liquidators Soars as Founder Plans Take-Private Bid

Lumber Liquidators' founder Thomas Sullivan is trying to take the company private. He says the company has strayed from its original formula of low overhead and big marketing budgets and is spending money like crazy. Sullivan says he's been approached by private equity about partnering to buy Lumber Liquidators in the past, but he's only now interested because the stock price is down. If a deal doesn't take place, Sullivan says he would push for changes, such as boosting advertising and cutting back on corporate expenses.

9/13/2019: LL closed at $9.77.

Lumber Liquidators tumbles after founder shelves buyout and sells shares for a quick profit The founder had upped his ownership of Lumber by 30%, or 500,000 shares on Sept. 4 through his F9 Investments, saying he wanted to take the company private or be an investor in a sale of Lumber Liquidators to another related company. LL stock close at $9.24

5/26/2023: LL stock closed at $4.46.

Years later F9 Investments returns to offer LL Flooring a $5.76 bid. F9’s actions in 2019 make their bid offer questionable but like Elon Musk and Twitter Inc. acquisition saga why hasn’t management called F9’s bluff. ~ My personal thoughts here.

6/13/2023: LL stock closed at $4.65.

An investment consortium led by Howard Jonas urged LL Flooring Holdings, Inc. Board of Directors to consider F9 bid to acquire the company. The consortium believed the offer was a fair starting point for acquisition discussions and that the Board should’ve engaged with the group and immediately enter into a sale process for the company. The consortium also believed that management change would be necessary for stockholders to benefit from the company's underlying value.

10/12/2023: LL stock closed at $4.00.

Live Ventures Submits Proposal to Acquire LL Flooring for $5.85 Per Share in Cash

10/17/2023: LL stock closed at $3.33.

Bleecker Research Short Report for LL deal. “LL Flooring Holdings (LL): Live Ventures Deal Should Be Treated As Dead On Arrival” The report is noble and has made significant claims why you should not own the stock of LIVE 0.00%↑. But Bleecker’s case for Live Ventures potential acquisition of LL 0.00%↑ is more tenuous.

11/14/2023: LL stock closed at $2.97

LL Flooring Holdings, Inc. LL 0.00%↑

LL Holdings, Inc. formerly known as Lumber Liquidators is a niche retail operation for multiple types of hard surface flooring. 85% of sales are based on sold products flooring products and accessories with the rest of sales reflecting 15% of installation and delivery services.

Activist/Influencing Agents

Jon Issac of Issac Group

HISTORY

In 2008 he shifted his focus to investing in and acquiring companies soon after the Great Recession. In 2011, he acquired a controlling stake in Live Ventures Incorporated (LIVE 0.00%↑), a Nasdaq-listed company that was on the brink of bankruptcy. Under his leadership, Live Ventures has been transformed into a diversified holding company with a portfolio of profitable and growing businesses. Isaac is a visionary leader who has a knack for identifying and capitalizing on undervalued opportunities.

Live Ventures

Thomas Sullivan of F9 Investments

F9 Investments is a private equity firm based in Miami Beach, Florida. They invest in Clean Energy, Direct to Consumer Retail, Commercial and Industrial Real Estate.

Cabinets to Go

Mario Rizzi of Rizzi Capital

Rizzi Capital is a value investing firm that focuses on maximizing returns for its clients. The firm manages a concentrated portfolio of U.S. and Canadian listed small-cap stocks, and takes a long-term approach to investing. Rizzi Capital seeks out companies with slow or steady growth, a dividend yield above 5%, very little debt, profits, and a share price below or very close to book value.

Management Bio:

The firm is founded and operated by Mario Rizzi, a seasoned Montreal, Canada, based activist investor with over 20 years of experience. Rizzi has a proven track record of successfully advocating for minority shareholder interests in notable corporate takeovers and mergers, consistently securing substantial gains for shareholders. His expertise lies in deep value investing, prioritizing Canadian stocks with attractive dividend yields and high book-to-market ratios. While maintaining a concentrated portfolio of typically under five major holdings, Rizzi's investment approach is defensive, prioritizing return of capital over return on capital.

Rizzi's notable investor activist campaigns include the 2009 ClubLink Inc/Tri-White Corp merger and the 2008 Viceroy Homes privatization, both of which resulted in significant value accretion for shareholders. His focus on Floor & Decor Holdings, Inc. (FND 0.00%↑) (**insert backhanded cough to LL management** after leaving his earlier attempts to gain LL 0.00%↑ investor support to no avail) exemplifies his deep value approach. Recognizing FND 0.00%↑'s undervalued assets and untapped potential, Rizzi initiated a campaign to unlock shareholder value.

To further amplify his investment activism efforts, Rizzi established the Lumber Liquidators Value Committee (LLVC), a dedicated platform to advocate for shareholder interests in undervalued companies. The LLVC has garnered recognition for its unwavering commitment to protecting shareholder rights and maximizing shareholder value.

Lumber Liquidators Value Committee (LLVC)

LLVC is Back. It is Time to Remove the Board of Directors.

Chris Drose of Bleecker Street Capital, LLC

Chris Drose launched Bleecker Street Capital, LLC in 2021.

Why This Former Kingsford Analyst Is Launching an Activist Short Fund, Short Selling Woes Be Damned

Chris Drose, a former analyst at short-biased hedge fund Kingsford Capital, is launching a new activist short fund called Bleecker Street Capital this summer, he said in an interview with Institutional Investor.

Bleecker Street Research

October 17, 2023:

Bleecker Research posted a short thesis on LL 0.00%↑ that holds valid facts as to why you should NOT buy LIVE 0.00%↑, the potential acquirer LL. Yet despite the report’s title: LL Flooring Holdings (LL): Live Ventures Deal Should Be Treated As Dead On Arrival

The Main points have tenuous relevance to our current issue at hand being WHO IS GOING TO ACQUIRE $LL? The most relevant point to consider from the report is LIVE 0.00%↑ is already highly levered which would make it difficult for the company to obtain any debt financing to buy the company.

Howard Jonas Led Investor Consortium of IDT Corporation

I provided the link above to hint at the associates likely to be identified as participants in the Howard Jonas consortium.

Why Does LL 0.00%↑have a Wide Deal Spread?

LL Flooring's current predicament can be attributed to a confluence of factors

1. Historical of Operational Struggles

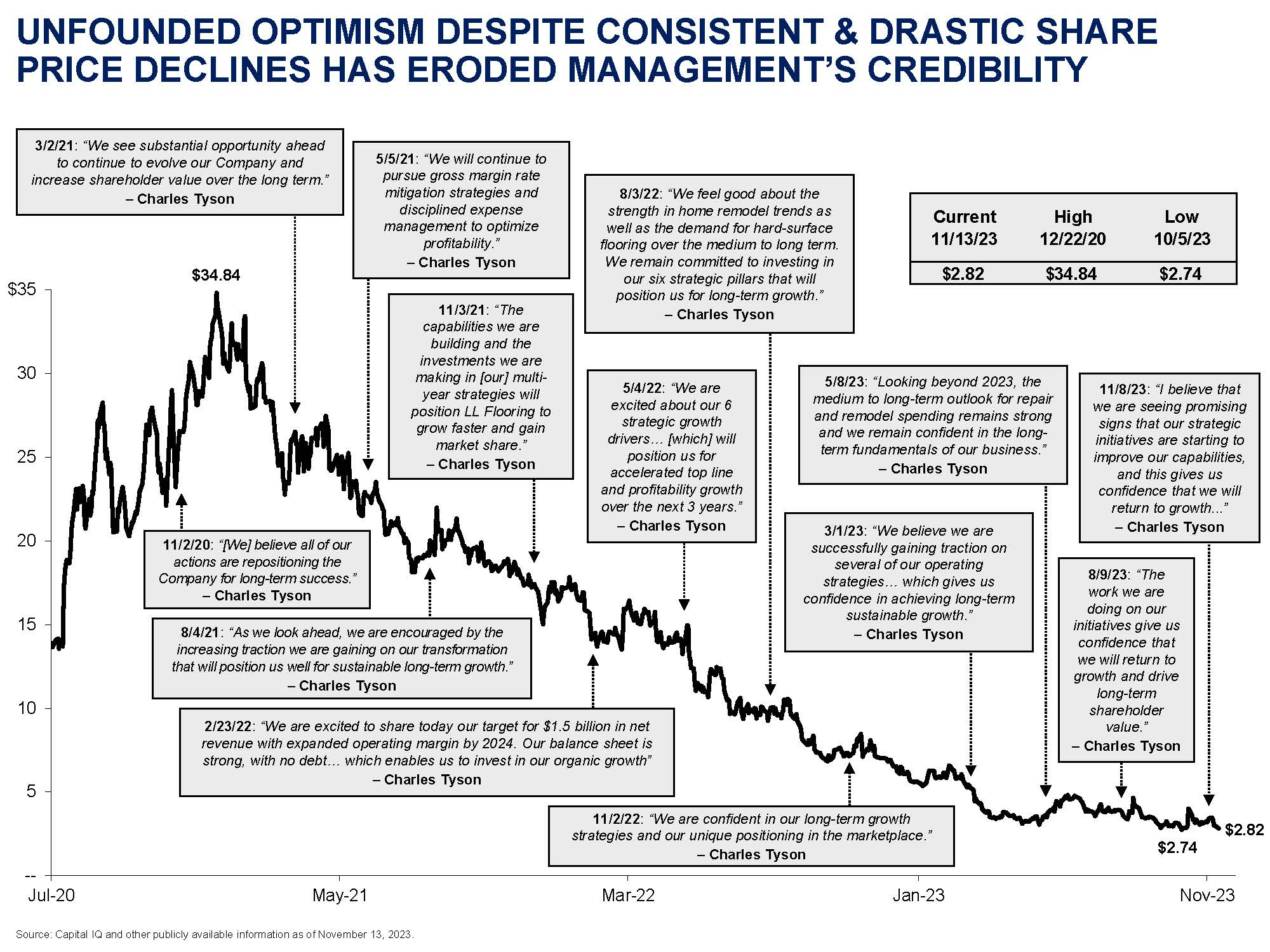

LL Flooring's operating losses that lasted 4 years between 2015 and 2018, stemmed from product issues related to Whitney Tilson's time at Kate Capital, have left a lasting impact on investor confidence. These losses cast doubt on the company's ability to manage its business effectively and generate sustainable profits.

You can read about the whole saga in his short thesis presentation of former Lumber Liquidators and how he made money and likely lost money on his second round of shorting the stock at the time.

2. Failed Acquisition Attempt

In 2019, LL Flooring's board rejected an acquisition offer from Tom Sullivan, the founder of Lumber Liquidators. Their apparent reluctance to pursue other potential deals signal a lack of strategic direction and a potential unwillingness to exit the business. This decision signaled to the market that the company was unwilling to consider strategic alternatives, even in the face of its deteriorating financial performance. This, in turn, widens the deal spread and depresses the stock price.This indecisiveness further clouds the company's future and keeps the deal spread wide..

3. Lack of a Cohesive Turnaround Plan

Despite its recent announcement of an "exploratory strategic review," LL Flooring has yet to present a concrete plan to address its underlying issues and restore profitability. Management has instead relied on shrouded vagueness and false promises veiled in claim of "exploratory strategic review process" This lack of clarity appears to be the modus operandi for LL Flooring’s management team simply because it has worked historically in making unrealistic promises evidenced in other failed activist attempts. And those shareholders have paid for it dearly. If management was emboldened by this before I can only imagine a leader in Charles Tyson’s position saying something as crazy as, “WHAT WILL SHAREHOLDERS DO ABOUT IT ANYWAY!”

Failed Acquisition rescinded letter

10 Year Trading History for LL Flooring

Concluding Implications for the Deal Spread

The combination of these factors has led to a wide deal spread, reflecting the uncertainty surrounding LL Flooring's future. The market is assigning a low probability to a successful acquisition, as evidenced by the significant discount to the highest bid offer of $5.85 per share.

Given scenario:

F9 Investments previously offered $5.76 per share but later offered $3.

Live Ventures, Inc. offered $5.85 per share.

If management doesn't proceed with either buyers, both offers might be rescinded, and the stock likely trades between $2.50 & $2.70.

Success: Deal is completed with LIVE 0.00%↑ at $5.85.

Partial Failure: Management proceeds with F9 Investments deal at $3.00, OR Management does NOT proceed with either buyer causing both offers to be rescinded, and the stock trades down to the expected trading range of $2.50 & $2.70.

Complete Failure: Management doesn't proceed with the buyers, both offers are rescinded, and the stock falls to $2.50 or lower.

Simplifying the probabilities:

Lower Bound of Failure Range = $2.50

Higher Bound of Success Range = $5.85

Calculating the

Implied Probability of Success=

(Current Price minus Lower Bound of Failure Range)

------------------------------------------------------------------

(Higher Bound of Success Range minus Lower Bound of Failure Range) Implied Probability of Success=

3.29-2.50

---------- ≈ 0 .24 ≈ 24%

5.85−2.50Based on the current trading price of $3.29, the implied market probability is approximately 24% for success (management selling the company for $5.85 or higher)

nice formula Implied Probability of Success where did you hear about this?