The Dirt Weekly: August 26, 2022

The Dirt Weekly: August 26, 2022

The Inventory Argument

The Inventory Argument

In the will-they, won’t-they, Ross and Rachel back and forth of the Real Estate analyst world, two camps have formed. One camp is convinced, is completely sure, that there is more housing inventory than anytime in history and that it is all about to come collapsing down (a la 2008). The other camp is convinced, is totally sure, that the the first camp had too many martinis at lunch, that there is still a housing inventory shortage, and there will be for quite some time. Who is right? Who is wrong?

Frankly, I don’t know. There are so many variables at play (location, geography, market demographics, etc) that it hurts my head to try and puzzle it all out. My intuition tells me that, as of today, there are still lots and lots and lots of folks who want a house. Absolute demand is not a problem. But absolute demand (those who want something and would buy it if they could) does not matter. The problem is defining the buyer pool that is both willing and, far more importantly, able to take action. In other words, how large is the pool of potential buyers that can afford a house as of today? Keep in mind the following restrictions: inflation and lagging wages/ salaries, historically high home prices, increasing interest rates, restrictive underwriting standards (as compared to the mid-2000’s). One might throw on top of that people nervous about inflation, the economy, their jobs, politics, etc, etc. With all of those (and many other) factors at play, the market feels and seems like the list of legitimate buyers is a small pool and shrinking by the day. In that sense, I believe that supply and demand are equalizing given the current trend. Stretched further, the trend could eventually lead to supply outpacing demand. In the classical micro-economics rule book, this means that prices will eventually come down. Prices might also just go sideways over a long trend with many small ups and downs in the short term. It is easy for me to imagine a future in which this trend takes place over half a decade or more.

All of those words and hot air feel right. They match the data. I can sell it on the street for a dollar. But things are rarely (if ever) as simple as the Microeconomics 101 textbook led me to believe all those years ago. No, dear reader, no. The road is bumpy. The night is dark and full of terrors.

Trends are real. Economics is culture and culture is feelings and perceptions and those have a momentum of their own. But trends always end. They reverse course. Feelings change. And the reversal tends to be a jolt rather than a smooth glide.

Waiting for Godot and/or a catalyst

The flip side of the above coin is the doomsayers prognostications of the sequel of The Great Recession of 2008 (tentatively titled The Fed Strikes Back). You remember that movie, right? Foreclosures. Short sales. Dented, weather-beaten, and sad For Sale signs and hundreds of unwanted and unloved houses like so many stray dogs in the shelter. Weedy, unkept lawns in sparsely populated yet brand new housing developments. We all remember this. Like in the movie The Big Short: “Oh, it’s just a gulley.”

The catalyst back then was a sudden jump in defaults when the Fed started raising rates. This jump in defaults crushed the Mortgage Backed Securities market which then caused the sudden halt of all lending. Banks were going bankrupt. Companies were going bankrupt. People were going bankrupt. And the lending stopped. Just stopped cold. Like a dumpster-diving raccoon caught in the accusing glare of headlights on high beam. And it all tumbled downhill from there.

It can definitely happen again. And this is regardless of today’s perceived inventory versus overall demand versus legitimate buyer pool arguments. All we need is a big, fat catalyst to stop the party and send everyone scurrying for the door like a frat party raided by the cops. My metric here is layoffs. That is what I look for. If unemployment ticks up (like the Fed wants it to do), if people start losing their jobs en masse, then I think the jig is up. If very large groups of people can no longer afford their mortgage then they will all be forced to sell at the same time. If people stop buying, if your buyer pool shrinks to zero, then it just doesn’t matter how many or few months of inventory there were yesterday. Today will be a new day with a new set of problems. It all just needs a catalyst. But what could that be? What could that be?

Dear reader, I do not know. What I do know is that the Fed has declared war on inflation and over-employment1. They are looking at those numbers like a teenage boy leering out of a second-floor window as the neighbor girl takes in the sun by the pool. And those metrics, the ones that the Fed governers salivate and obsess over, directly effect the housing market.

My bottom line of late is one of complete uncertainty. I have no clue what the government might, could, or would do if some mighty catalyst appears to tip the markets into the sea2. I have no clue if, and am not convinced that the Fed can, wants to, or will, stay any course. We look to them (the government, the Fed, etc) for comfort and succor and guidance. But, dear reader, they are leaves on the wind. They are drunk kids on the backroads in daddy’s new red Mustang. For all the numbers and data and graphs and formulae, they have no clue what to do. What does this mean? Well, it all could go up. It all could go down. It all could go sideways. Your guess is as good as mine. It is already a new day. We already have a new set of problems.

Mr. Mohtashami is in the ‘not enough inventory’ camp:

Mr. McBride is in the ‘too much inventory’ camp:

Interesting note: After I wrote the essay above, I attended a Continuing Education course and came away with the following information (and I was far too lazy to try and work it into the already completed text). The instructor of the course is from Austin. He has been around and practicing real estate for a loooong time. He mentioned the incredible influx of new housing about to hit the Austin area. He expressed his doubts as to Austin’s ability to absorb so much new inventory. So mark him as one more in the too much incoming inventory camp. At least for Austin.

What does all of this mean for land?

I am a land guy so I should keep my eye on the ball, right?

Well…

I pay close attention to the housing market because that market is over $40 trillion3 and about 15% of GDP4. That is… not a small thing. Mortgage Backed Securities (residential conforming) are now the driving factor for most other real estate interest rates. So as you might imagine, when the US housing market coughs, the national economy catches a fever. So the housing market matters more for land than any of us can imagine (or fully and truly comprehend).

I would not try and delude myself nor you, dear reader, and wax prognostic on what the housing market may or may not do to the land markets. I might mention past trends. But those don’t always pan out. Today is a new day. And I am an observer of the here and now. That is all. Here and now land sales in Texas are generally slowing along with the housing market. Explaining why with just a few reasons might make good copy but the truth is that there are thousands of land buyers and sellers each with their own reasons. Some of those reasons might rhyme with something along the lines of interest rates and general market uncertainty (a theme and trend if there ever was one). But there are still willing buyers. There are still willing sellers. The market is changing - transitioning as always - but the land market functions. The rest is guesswork, personal feeing, and individual circumstance. So the big question really is: what do you think? Or, probably better yet, how do you feel?

Texas Land This Week.

The following information comes from LandWatch.com. (Read Data Disclaimer5).

As of August 25, 2022 there were…

13,317 acreage properties listed as Available

1,213 acreage properties Under Contract

8 properties up for auction

Five counties with the most listings:

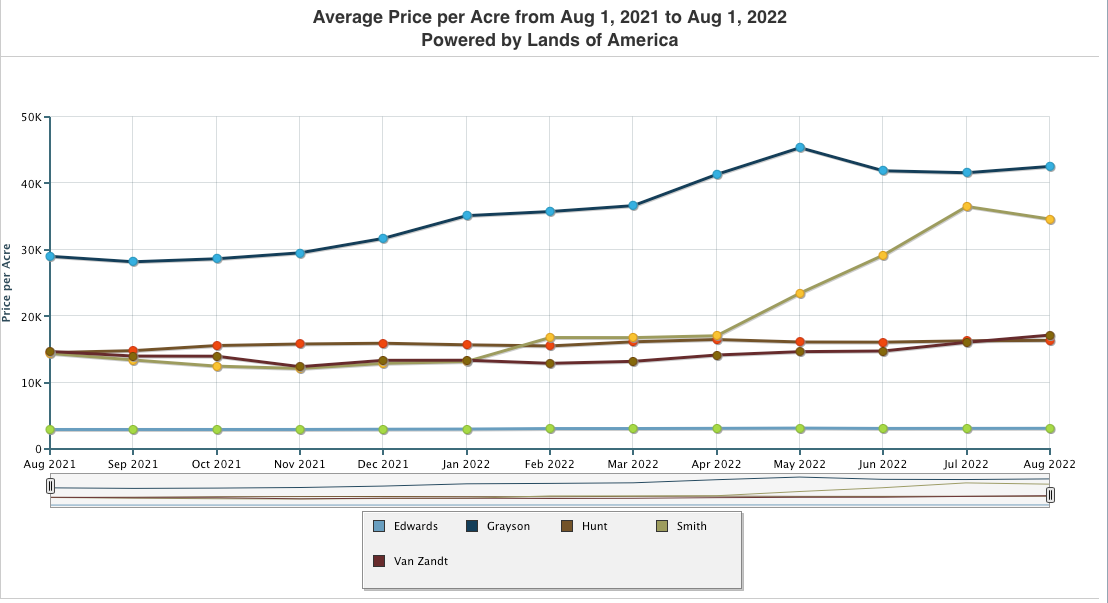

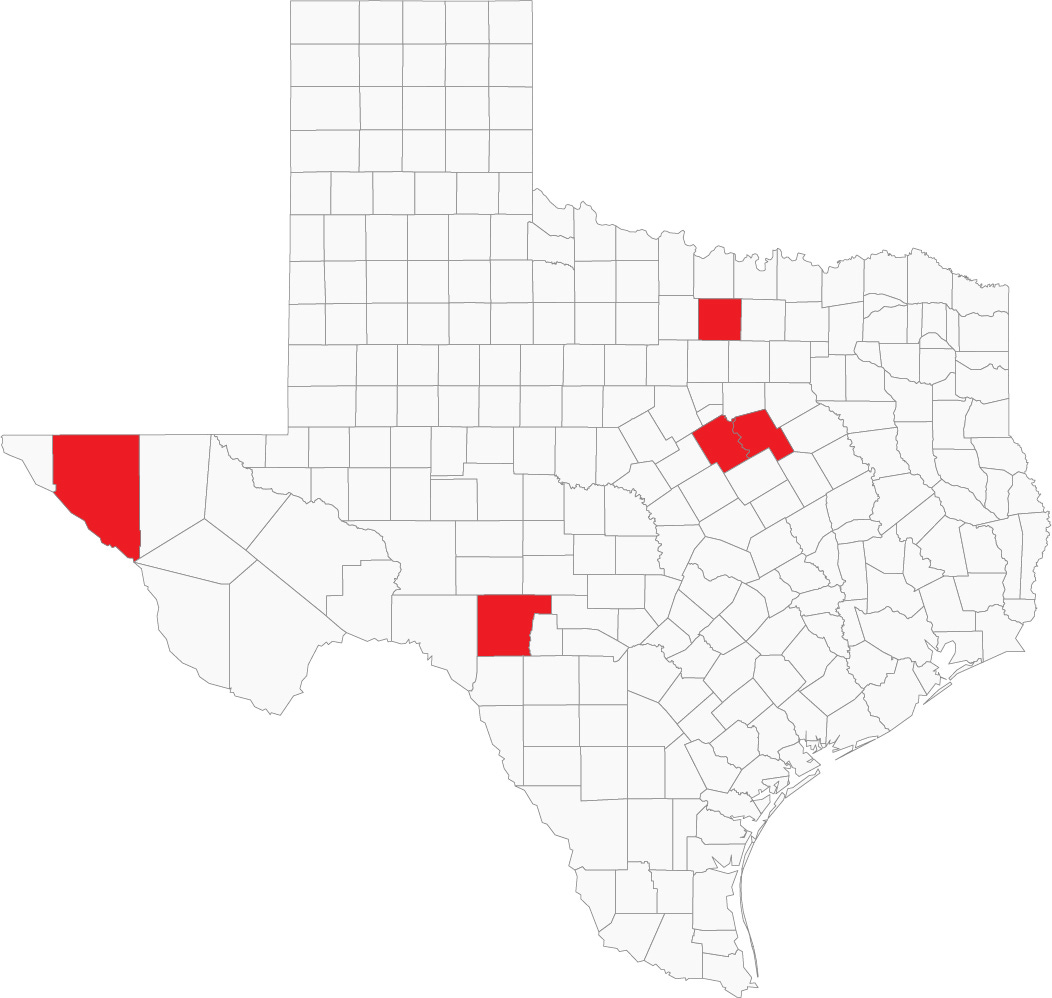

Grayson County - Texoma Region (277 listings)

Hunt County - Dallas Prairie Region (255 listings)

Smith County - Piney Woods North Region (226 listings)

Edwards County - Edwards Plateau West Region (218 listings)

Van Zandt County - Dallas Prairie Region (205 new listings)

Price per acre trends for these five counties:

For the last 7 days there were…

633 new properties listed

12 new properties under contract

2 properties identified as Sold

Five counties with the most listings in the last 7 days:

Bosque County - Blacklands North Region (17 new listings)

Wise County - Fort Worth Prairie Region (15 new listings)

Hill County - Blacklands North Region (15 new listings)

Edwards County - Edwards Plateau West Region (15 new listings)

Hudspeth County - Trans Pecos Region (14 new listings)

Price Trends for these five counties:

News from the Front.

I had an opportunity to attend the Texas Alliance of Land Brokers (TALB) monthly luncheon and meeting this week and caught up with Brokers/ Agents from a wide swath of Texas. One experienced broker from Dripping Springs who practices in the Hill Country area told me that he felt that land markets were still very active. Another from South Texas who specializes in game properties told me that things are definitely slowing down in his neck of the woods. My beautiful and very gifted wife is an agent with Keller Williams and that massive organization is preparing their agents for a coming buyer’s market on the residential side (see news below).

Important News.

Interest Rates (Compliments of the Mortgage News Daily app for iOS and my iPhone).

Financial Markets (compliments of the MarketWatch app for iOS and my iPhone).

UST 2’s and 10’s… yep, still inverted.

The Dirt Recommends.

The Wise Landowner will make themselves very familiar with the concept of Eminent Domain. For many, it may seem like so much dry mumbo-jumbo but that attitude will change very quickly when you get that notice of condemnation in the mail. I am a big consumer of podcasts and find the Ag Law in the Field podcast by Tiffany Lashmet to be very informative. Listen to this episode to get caught up on the latest Supreme Court Case on Eminent Domain. Then listen to all the others for a rich education in all things Ag Law.

Also from Tiffany Lashmet, et al and the folks at the King Ranch Institute for Ranch Management is this very informative Primer on Carbon Credits. The Wise Landowner and Wise Land Professional need to be versed on this emerging market and emerging opportunity.

Where I get my information:

An analyst’s analysis is only as good as the information they possess. As the old programming saying goes: garbage in-garbage out. The following is a list of my sources…

I follow a bunch of smart people on Twitter. A sample is represented above. You may also follow me on Twitter:

The Amazing Realtors with the Grand Land Company

LandWatch.com and LandsofTexas.com

MarketWatch App (market quotes and data)

FRED: Federal Reserve Economic Data, Federal Reserve Bank of St. Louis

North Texas Real Estate Information System and Heartland Realtors

Houston Association of Realtors

If only JM Keynes were alive to see this! For the confused: John Maynard Keynes is an historical economic figure who, during the Great Depression, advocated government intervention on a mass scale to increase interest rates and employment.

In March of 2020, I felt that COVID was The Big One to end all housing as we knew it. I felt sure that the housing market, that all real estate, was going to tank like nothing we had ever seen before. I had no clue, could not even conceive, that the government would take the actions that it did. But it did. And now the seal is broken. The gloves are off. It’s as if the umpire is now a part of the game. A new dimension. A new input. Something new to consider. They will definitely do it again. How, when, why? I’ve no clue.

Here is an article from Zillow for reference. It gives a more exact figure but I just said ‘over $40T’ because, well, prices went up a little in 2021: https://www.zillow.com/research/us-housing-market-total-value-2021-30615/

Here is an article from the Congressional Research Service as reference. It is also from 2021 and so the numbers are no doubt already larger. The point remains the same: housing is a substantial chunk of GDP. https://sgp.fas.org/crs/misc/IF11327.pdf

Data Disclaimer: The information is based on properties that are greater than 10 acres and which I refer to as ‘acreage properties’. This information is single source. Which means that this is NOT an exhaustive list of all properties available and sold everywhere in the Great State of Texas. Texas is a non-disclosure state and is therefore a Dark Market. This means that there are a great deal of data that are hidden, dispersed, not allowed to be shared publicly, or just plain unavailable. The following information is for reference and entertainment purposes only.