Are Personal Finance Gurus Unintentionally Giving You Bad Advice?

Are Personal Finance Gurus Unintentionally Giving You Bad Advice?

Ranking 10 of the biggest personal finance YouTubers using economics

According to a 2022 journal article, most advice given by personal finance gurus isn’t supported by any economic theory. This means that what you’ve been taught about how much you should save, where you should invest, or how you should repay debt might be based more on vibes than actual economic principles.

James Choi, the author of the paper, and a Professor of Finance at Yale, analyzed the advice provided by 50 of the most popular personal finance books, including Robert Kiyosaki’s Rich Dad Poor Dad, and Dave Ramsey’s Total Money Makeover.

But who reads books anymore? For those of you who don’t know what a book is, a book is like an audio-book but it’s written down instead of spoken.

So, instead, I decided to compare the recommendations from academic economists against the videos from 10 of the most popular personal finance YouTubers, like Graham Stephan, Andrei Jikh, and Nate O’Brien.

And the results were… interesting.

Here’s how this works: To grade the YouTubers, I created a marking criterion of 13 key recommendations, which broadly cover savings, investing and debt repayment. For each recommendation, I’ll award 1 mark if their videos match the advice of economists, half a mark if they’re sorta in the right area, and 0 marks if they’re completely off.

If any YouTuber doesn’t talk about one of the recommendations, we’ll skip them and each YouTuber’s final mark will be what they scored as a percentage of how many recommendations they provided. If the scores are tied, the YouTuber with more recommendations has the advantage.

Here’s an example.

Links to all sources: https://pastebin.com/F9byu4er

Hopefully this is made clear but this isn’t meant to be a hit piece on any of the YouTubers, I just think it would be interesting to analyze the information millions of people receive against academic principles that might not be as well known.

We hear so much about economists giving advice on the broader economy so why don’t we include economists in personal finance conversations? I’ll expand on this more at the end.

One more thing before I begin, I’ll be referring to the information provided by the YouTubers as ‘videos’, rather than ‘advice’, since, as you know, adding #notfinancialadvice to a video means their financial advice isn’t really financial advice.

Which reminds me, this post is also #notfinancialadvice.

So with that being said, how much of your income should you save every month?

Savings & Consumption

Optimal Savings Rate

Generally, the YouTube videos say that you should save a percentage of your income every month, ranging from 10% to as high as 40%. The number isn’t too important here, the key idea is that you should always be saving something, as much as possible, and as quickly as possible.

This is for several reasons - the most common being to abuse the power of compound interest, the eighth wonder of the world, so you have enough money to spend during retirement. Another reason is to instill discipline, so that you don’t spend money on unnecessary things.

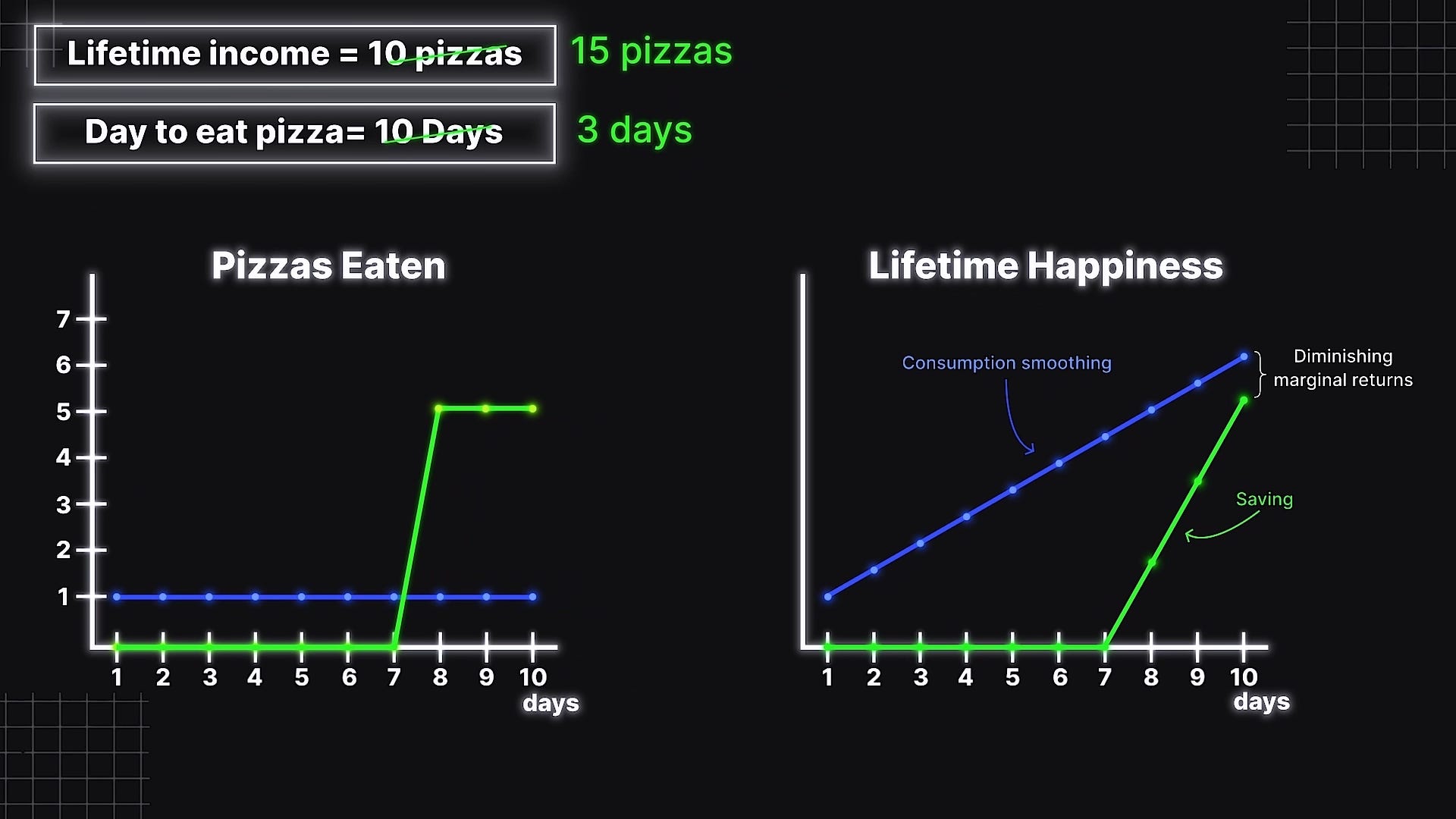

When it comes to economists, they don’t actually recommend an optimal savings rate like 10% or 20%. They don’t even recommend looking at how much to save but rather how much to consume. The optimal savings rate is just the difference between how much you earn and your optimal consumption.

Economists look at consumption because of the law of diminishing marginal returns, which is the idea that you receive less joy from something the more you consume it. The first slice of pizza is more enjoyable than the second, which is more enjoyable than the third and so on.

Let’s look at how this applies to saving money over a person’s life - Imagine we had money to buy 10 slices of pizza over a 10 day lifespan.

If we wanted to avoid triggering diminishing marginal returns, economists recommend spreading out the consumption over time, which is known as consumption smoothing.

If we instead saved our money until the final 3 days, and even if compound interest grows the 10 pizza slices into 15 pizza slices, our overall happiness in life wouldn’t be as high as when we smoothed our consumption.

But that’s just pizza, how does this apply to a person’s life?

Well, generally speaking, a person’s income with respect to their age is hump shaped - they earn little in their first 2 decades of life, earn most of their money between 20 and 65, and back to not earning much once they retire.

Combine this curve with a flat consumption curve that represents consumption smoothing, and we get what is called the Life-Cycle Hypothesis.

What we can see from this model is that in a person’s early life, they should have negative or low savings, in their middle life, they should positive savings, and at retirement, they should have negative savings again.

Early negative savings usually represents loans, particularly student loans, and borrowing from parents and other sources.

Okay, now back to the YouTubers.

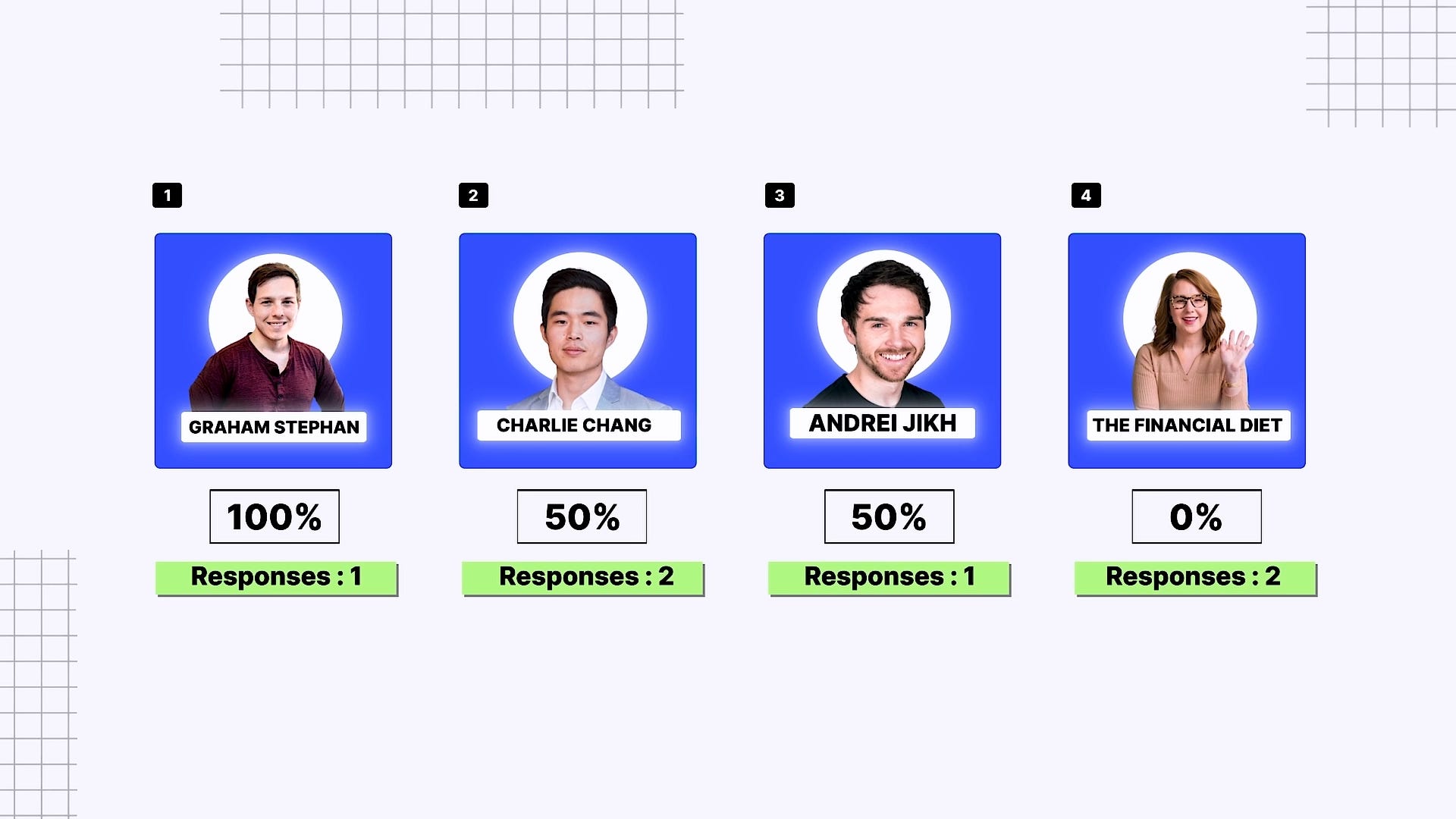

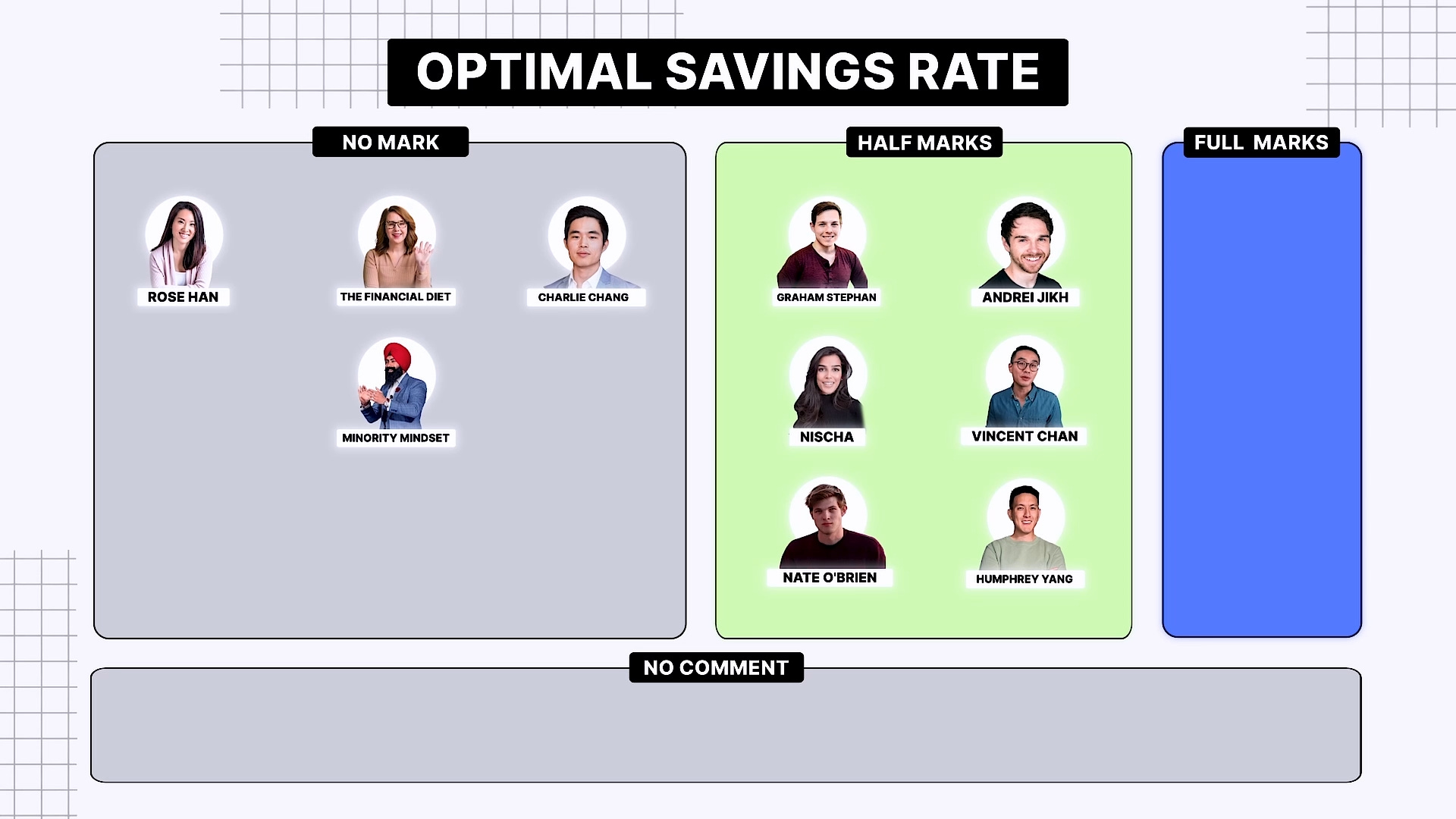

None of the 10 YouTubers explicitly mentioned consumption smoothing as the optimal savings rate so no one gets full marks.

That being said, Graham Stephan, Nate O’Brien and Andrei Jikh advocate for increasing your savings rate if your income increases, which is pretty consistent with consumption smoothing.

Nischa mentions that you shouldn’t save too much when you’re young and to borrow from your future self to grow your skill set, Humphrey Yang says your savings rate depends on your goals, and Vincent Chan has mentioned that how much you save depends on personal factors.

So they all get half a mark, and everyone else gets a 0.

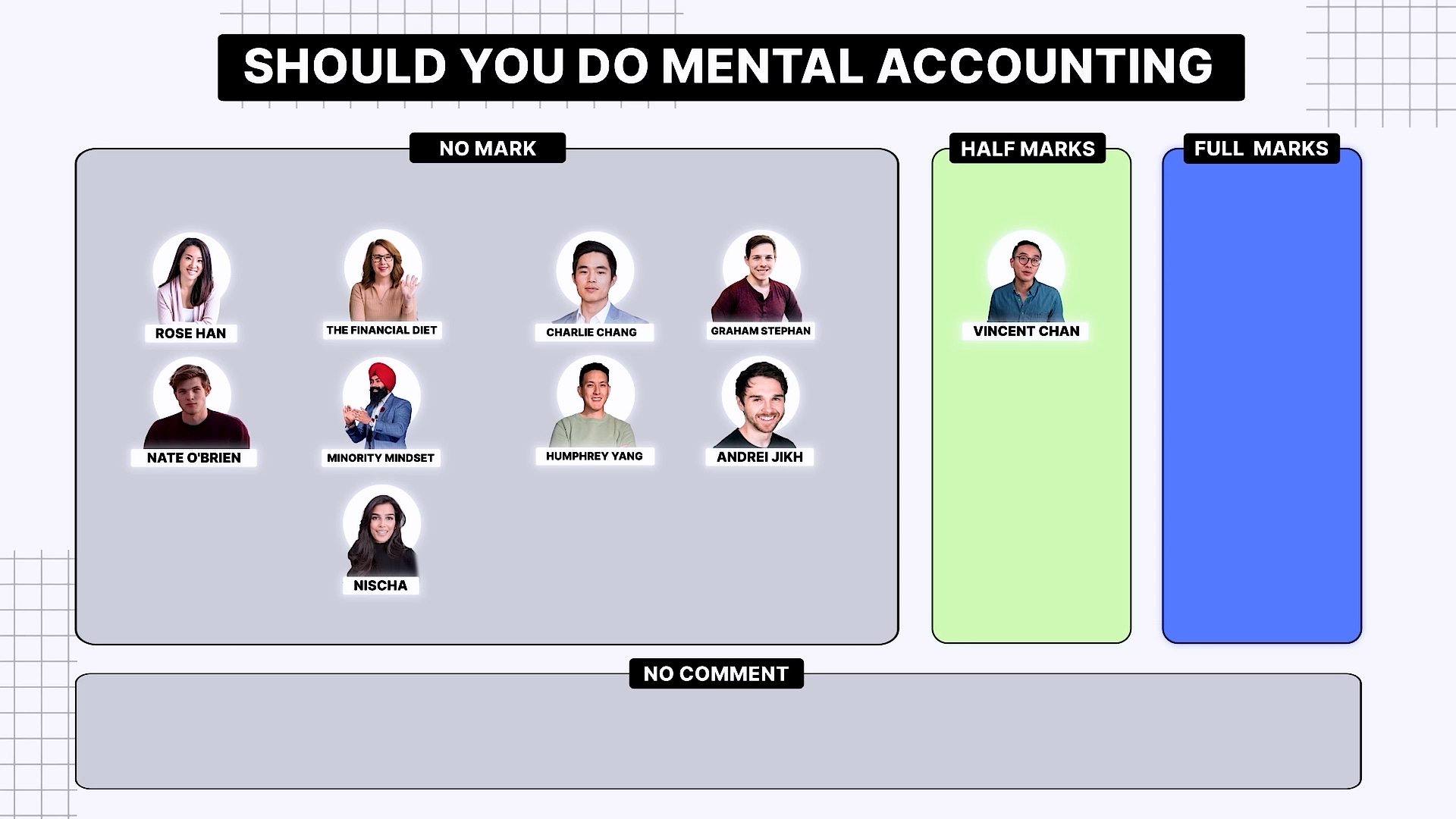

Moving onto the next recommendation, should you categorize your expenses, or do what economists call mental accounting?

Should you categorize your money?

No, according to economists, the answer is no.

Money is fungible. In other words, money is money, is money.

Mental accounting is a model developed by Nobel winning behavioural economist, Richard Thaler. It’s what people do when they mentally split their money into different categories, like saving for a home, or for a holiday, or when they split their expenses into clothing, gas, or food. Does this sound like something you do right now?

The problem with mental accounting is that it can result in people demonstrating greater loss aversion for certain mental accounts, resulting in cognitive bias that incentivizes systematic departures from consumer rationality.

And how do I know this? Well, Wikipedia.

But in layman’s terms, creating arbitrary barriers that only exist in your brain, and not your wallet, could lead to situations where you are making life worse than it needs to be.

Let’s look at a simple example where you budget $100 for gas and $100 for food.

Let’s say at the end of the month, you’ve spent $80 on gas and $100 on food. If you’re out of food and you’re hungry, rationally speaking, you should spend $20 on food. If you instead follow the budget, you’re not allowed to spend any money on food. However, you are allowed to freely spend $20 on gas as it’ll fit perfectly in your budget and, unless you’re Immortan Joe, that’s probably not going to give you any happiness.

At the end of the day, your wallet doesn’t care where the $20 goes to, only that it’s gone, so might as well spend it on what provides you the most happiness.

Looking at the YouTubers, all 10 have videos that say you should budget money into mental accounts, so they all get 0.

Interestingly, Vincent Chan calls out mental accounting as a psychological flaw but later in the same video, he recommends budgeting money into mental accounts… so half a mark for him, I guess.

Annuitize wealth in retirement

And in the last recommendation of savings, economists recommend annuitizing your wealth during retirement. This means buying life annuities to pay you a fixed amount every period as a way to not outlive your savings.

In Choi’s paper, only 4 out of the 50 finance books talk about life annuities and it’s a similar story here. As far as I researched, no YouTuber recommended for or against life annuities during retirement, so they all get a pass here.

Maybe it’s a topic for Graham Stephan’s next video, or maybe he’ll talk about it if the life annuity market crashes.

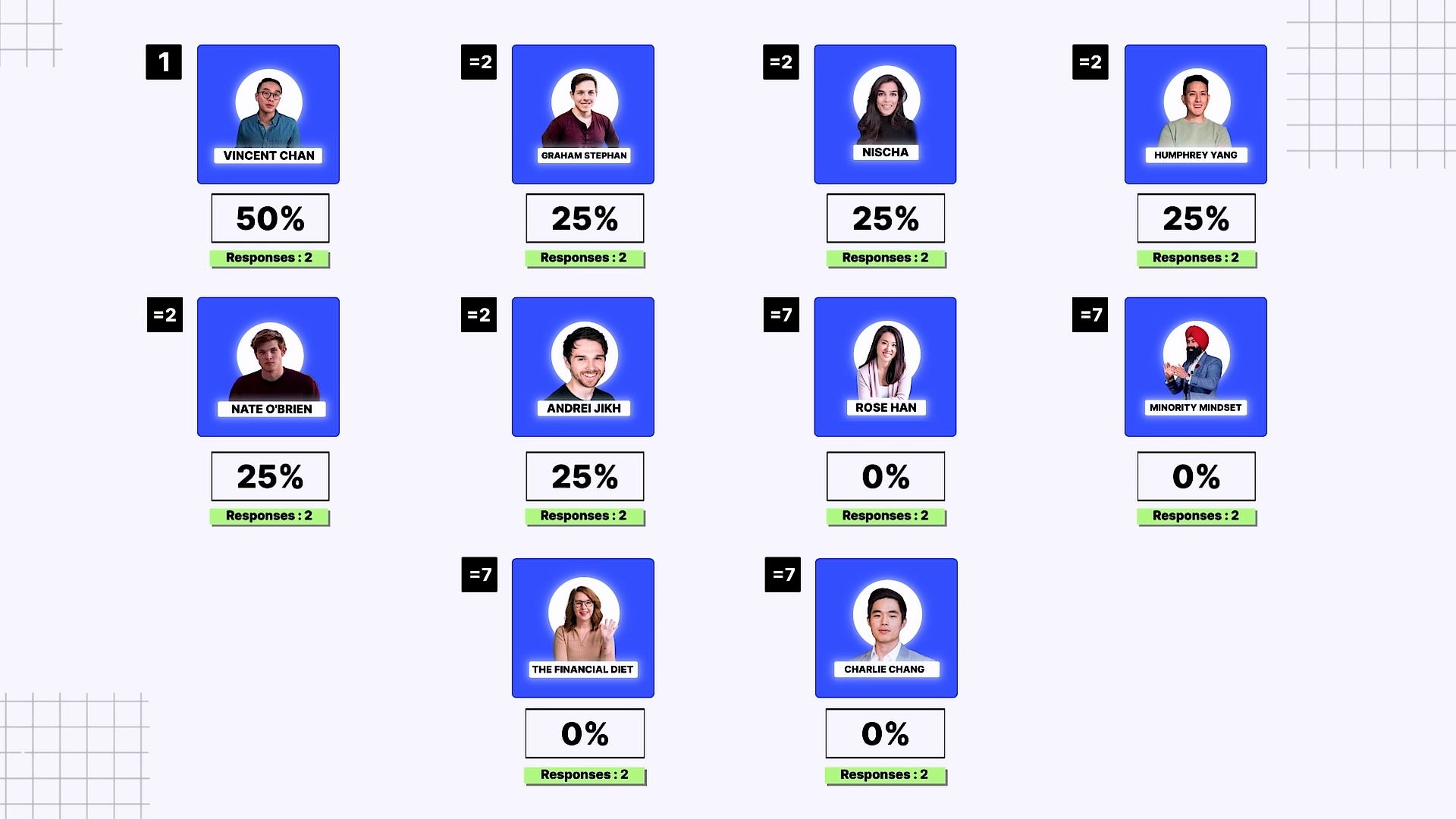

To wrap up savings, Vincent Chan is leading with 50%, followed by Graham Stephan, Nischa, Humphrey Yang, Nate O’Brien, and Andrei Jikh, all with 25%.

Now, onto where to invest your money.

Investing

Investing Near-Term Consumption, Equity Allocation & Why

To kick off this category, we have 3 investment recommendations that are related to each other: how to invest short-term spending, how many shares you should own over your life, and why.

In terms of investing short-term spending, all the YouTubers say to keep emergency funds in a high-interest savings account, so that it is easily accessible and is earning interest, rather than lose value to inflation.

Andrei Jikh mentioned that he kept his emergency savings in BlockFi to earn 8.5% compound interest. Yeah, for some reason I don’t think he’s doing that anymore.

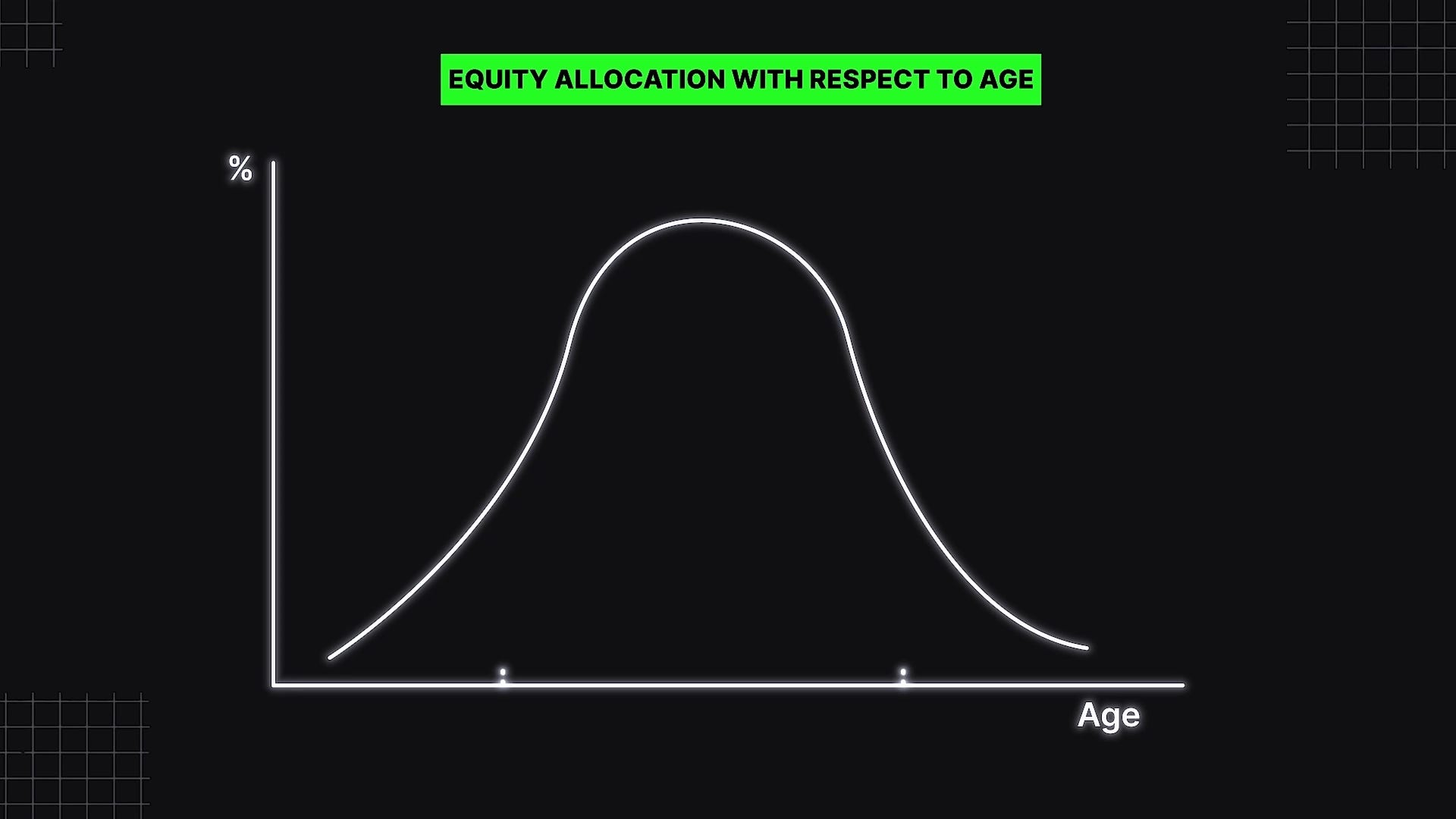

When it comes to how much equities should make up a person’s portfolio, most recommended it to be hump-shaped with respect to age - that is, a low amount of equities in early life, a high amount in middle life, and lower towards retirement.

Kinda like income in the Life-Cycle Hypothesis.

The reason for this shape was fairly consistent among the YouTubers. Young people have a lot of short-term spending requirements, and need to build up an emergency fund, so their equity allocation will be low. Once they are older they should start investing in equities for those sweet stock market gains. When they start to approach retirement, a large chunk of equities should be swapped out for bonds.

In particular, Andrei Jikh mentions a common rule to calculate how much to invest in shares “you can take 110 and subtract your age”, Rose Han says to “own your age in bonds.”

All the YouTubers that advocate for the hump shape mention a common reasoning; young people should buy more equities because they can afford to take risks.

Graham Stephan, Rose Han, Humphrey Yang, and The Financial Diet all say stocks display mean reversion, or in their words, stocks will always go back up after a dip, so investors with long investment horizons, ie young people, should buy equities.

Bonds offer less volatility, so they are appropriate for someone approaching retirement.

In Choi’s paper, other reasons listed by finance authors for why younger people should invest more in stocks include stocks being less likely to under-perform bonds, stocks being less likely to have a negative return as the investment horizon grows, and stocks growing because the economy grows.

When it comes to academic economists, they also recommend that money needed for short-term spending to be invested in short-term, liquid assets, so everyone gets 1 mark.

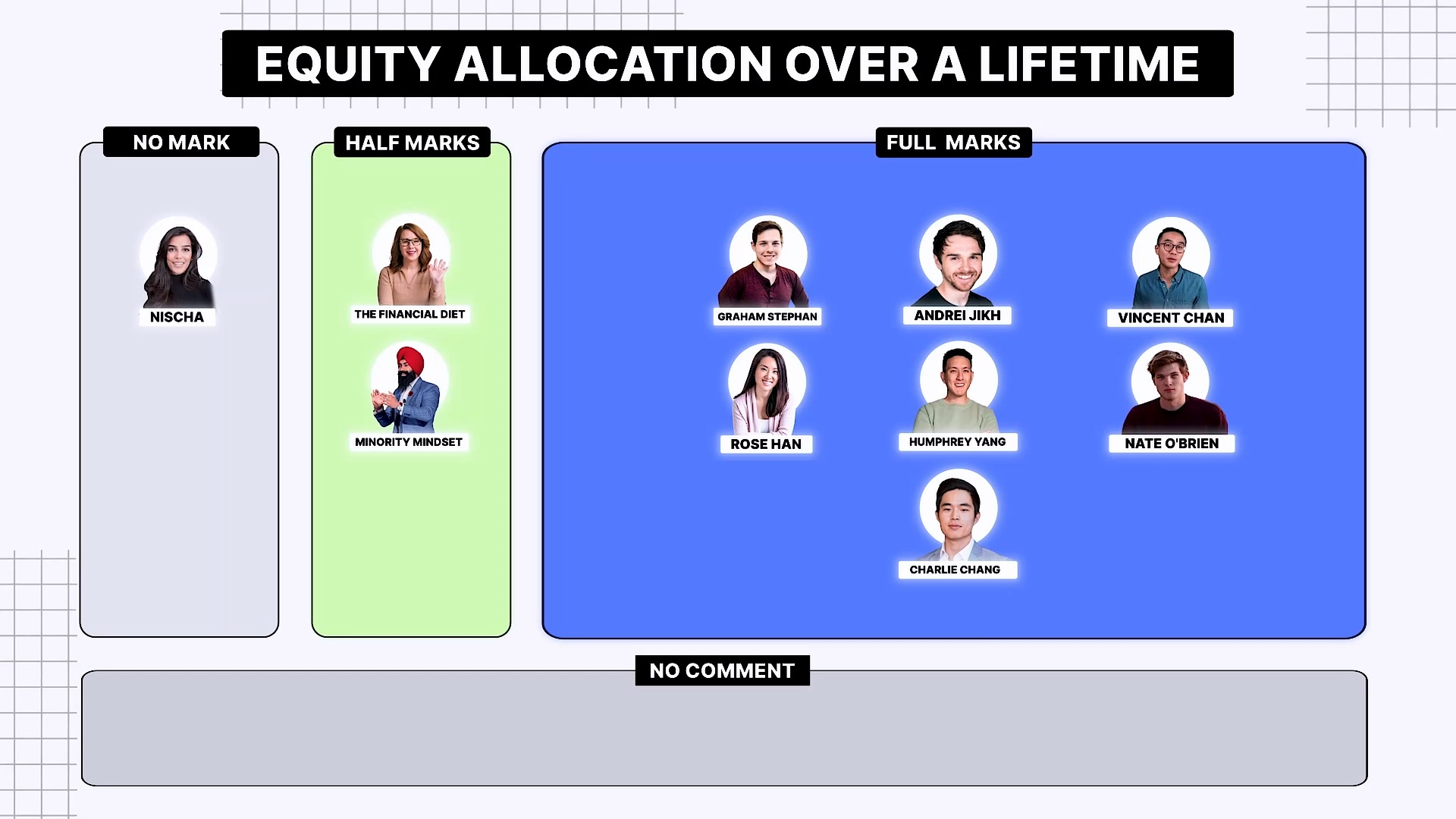

Economists also recommend a hump shaped equity allocation, so Graham Stephan, Andrei Jikh, Vincent Chan, Rose Han, Humphrey Yang, Nate O’Brien, and Charlie Chang get a point here.

The Financial Diet and Minority Mindset describe an equity style that is consistent with a hump shape without calling it a hump shape, so they get half a mark.

Nischa is the only YouTuber to not have an equity allocation that varies, although I suspect it is because her channel is relatively new so she might not have gotten around to it.

When it comes to the reasoning for this hump shape, economists actually disagree with what the reasoning provided by the YouTubers, so no one gets a mark here.

Rather than looking at the expected return of assets like the YouTubers did, economists look at their variance.

Just a quick warning, this section is pretty technical and I am not paid enough to simplify it.

Assuming stocks are identically and independently distributed, stocks outperform bonds as the investment horizon increases, but this is offset by the variance of cumulative stock returns also increasing.

Assuming constant relative risk aversion utility and no labour income, Samuelson and Merton find in their 1969 papers that the optimal equity allocation doesn’t vary with the investment horizon.

And yeah, I know, economists and their assumptions, am I right?

But bear with me, I promise we are getting somewhere.

In their 1997 book, The Econometrics of Financial Markets, Campbell, Lo, and MacKinlay conclude that there is little evidence of the mean reversion of long-horizon returns described by the YouTubers, where low recent stock market returns unconditionally predict high future returns.

However, Cochrane finds in his 2009 book, Asset Pricing: Revised Edition, that if low stock market returns lower the price-dividend ratio because they aren’t accompanied by a drop in dividends, they do forecast higher returns.

And Barberis finds in his 2000 paper that if we take into account today’s price-dividend ratio and expectations of how it will evolve in the future, the conditional annualized variance of cumulative log stock market returns declines with investment horizon.

And Choi says conditional variances are the theoretically relevant factor for investment decisions, and he believes most financial economists agree with Barberis’ findings.

So, all of that is to say, longer-term investors should hold more stock than short-term investors.

My goodness, no wonder people would rather listen to YouTubers than economists.

I actually skipped a lot more to make this section more bearable, so make sure to check out his paper if you want to read into the optimal equity allocation some more.

But that was just equities, how about the bond allocation of people approaching retirement? Okay, this one’s more interesting, at least in my opinion.

Bonds are assets that pay a fixed amount every period. Similarly, a person’s full-time salary is a fixed amount paid every period. So, a young person implicitly has a fixed-income asset with hundreds of incoming future payments, their career.

As someone ages, the number of incoming future payments decreases, so to replace this fixed income, a person should invest in bonds.

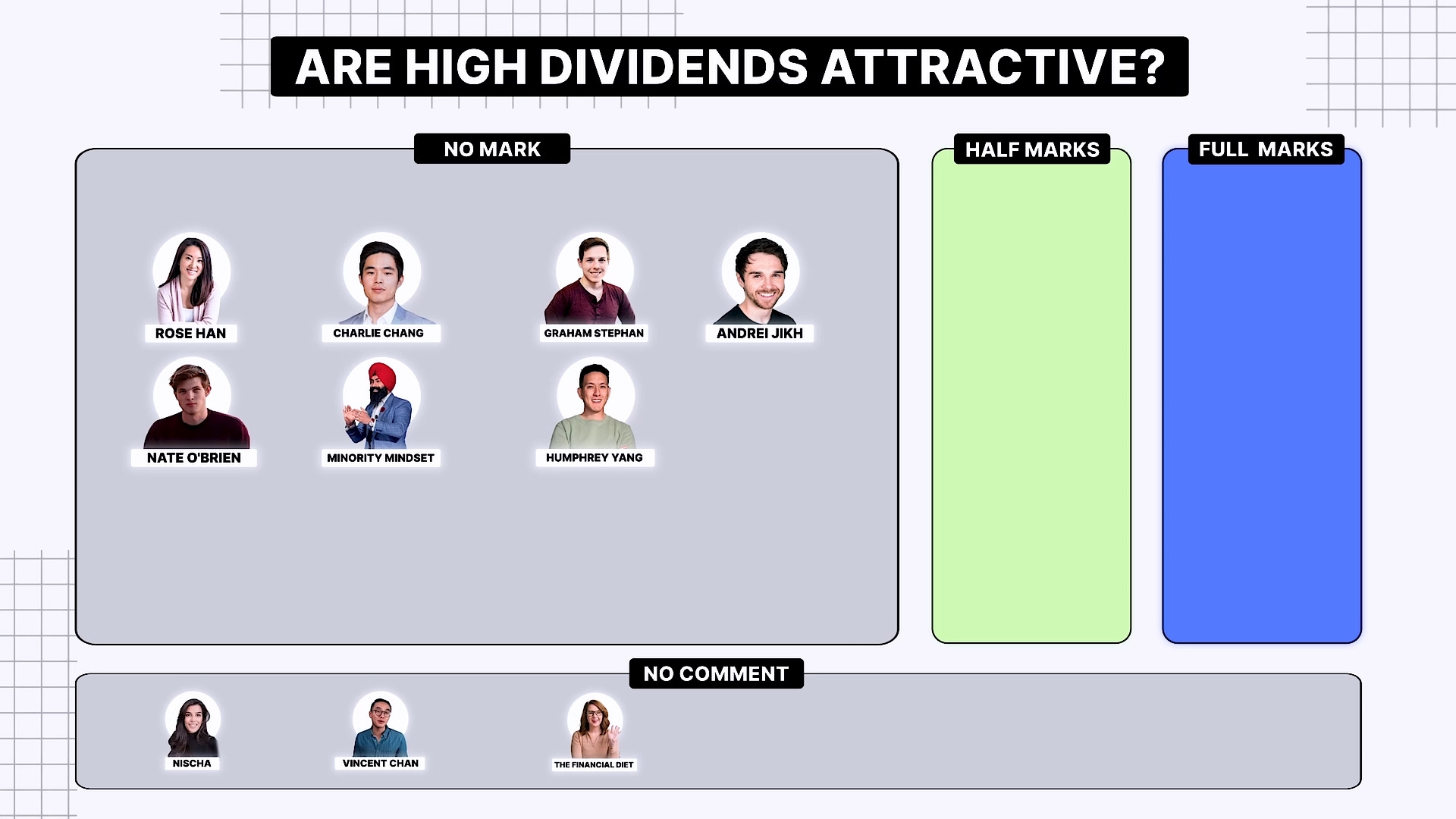

Now that we know the optimal equity allocation for investors, what should they invest in? Should they seek high dividend paying stocks?

Dividend Stocks

Economists aren’t fans of dividends when valuing shares.

In 1961, Miller and Modigliani showed that, in a friction-less market with no taxes, how much a firm pays out in dividends is irrelevant in its valuation. Ben Felix provides a good summation on the dividend irrelevance theory in this tweet.

And yeah, again, I know, economists and their assumptions, am I right?

Well, in the real world, dividends are taxed worse than capital gains in the US. At least that’s what Choi says. I don’t know, I don’t live in the US.

So dividends as a source of income doesn’t really make sense.

Graham Stephan, Andrei Jikh, Nate O’Brien, Rose Han, Minority Mindset, Humphrey Yang, and Charlie Chang all have videos describing how they earn passive income through dividends so they all get 0 marks.

Everyone else gets a pass since they don’t recommend or not recommend dividends.

What about equity style recommendations, like value stocks or small cap stocks?

Value Stocks And Small Cap Stocks

Value stocks are stocks which have relatively low prices compared to their fundamentals. Small cap stocks are stocks with small caps.

Value stocks have historically had higher returns than their counterparts, growth stocks. Similarly, small cap stocks have historically had higher returns than large cap stocks.

Sounds like value stocks and small cap stocks are attractive, right?

But the current academic literature is unsure whether these return differences are due to mispricing or rational compensation for risk that is not captured by their market beta.

If that didn’t make sense to you, basically, the conclusion from economists is that value stocks and small cap stocks may or may not be attractive.

Andrei Jikh, Vincent Chan, Nate O’Brien, Minority Mindset, Humphrey Yang, and Charlie Chang all get half a mark here for recommending value stocks.

So high dividends aren’t attractive, value stocks and small cap stocks may or may not be attractive - what should investors invest in?

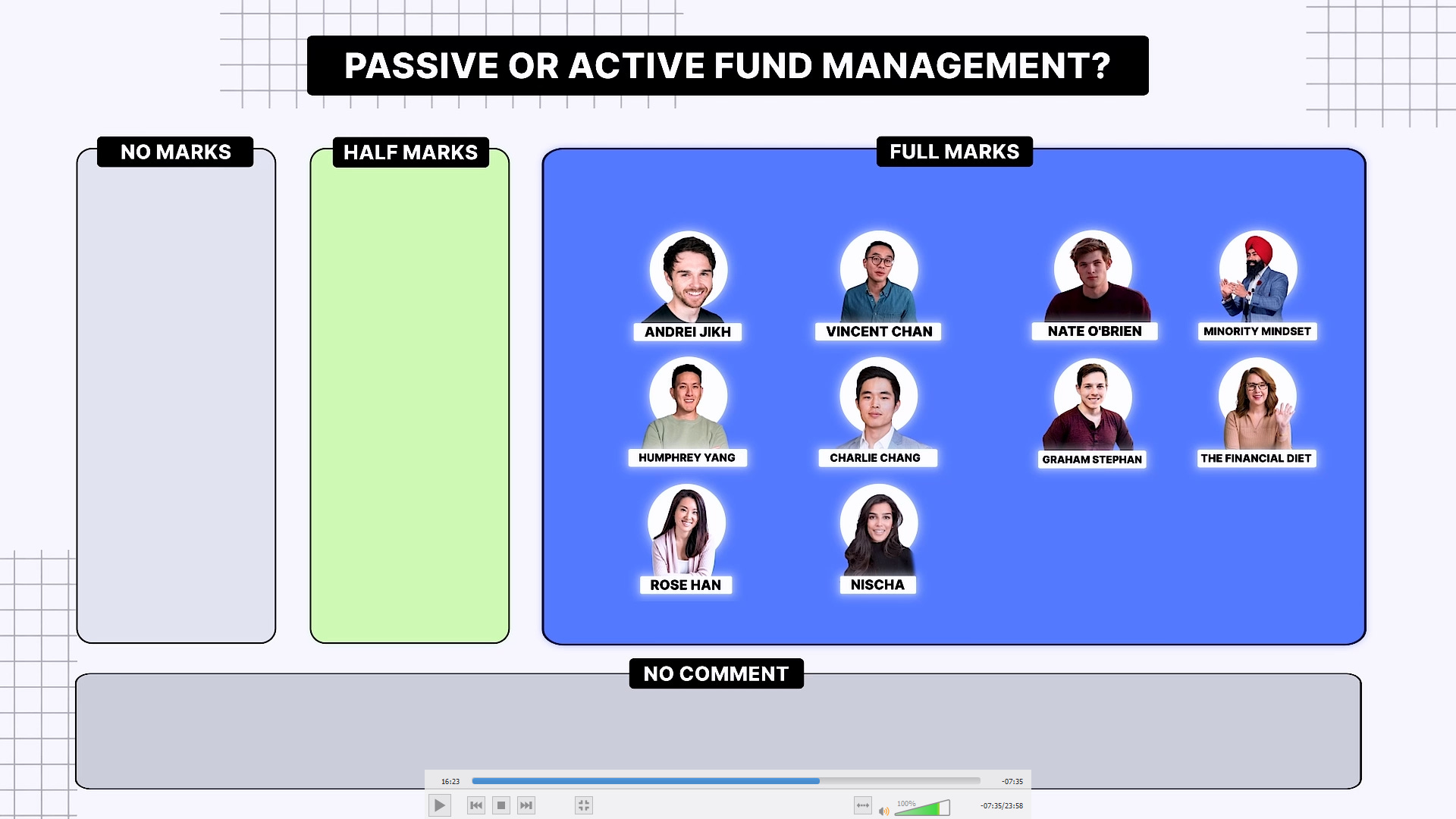

Passive Index Funds

All the YouTubers recommend that investors should passively invest in index funds rather than pursue active fund management, which is the same as economists, so full marks for all the YouTubers here!

YouTubers and economists agree, the average active fund underperforms the average passive fund, by 0.67 per cent per year according to French.

Choi believes the widely public, easy to understand, and straightforward calculations of the statistics of average fund performance leads to economists and personal finance gurus to massively agree here.

But there are a ton of index funds to choose from. Which do the YouTubers say to invest in? All of them recommend an S&P500 index fund.

International Diversification

When discussing adding international stocks to their portfolio, most YouTubers recommend keeping most, if not all of their investments domestically.

Nate O’Brien recommends investing domestically since there’s an information gap when it comes to other countries.

Humphrey Yang says there are currency considerations and is worried about less developed countries with potentially overbearing governments.

Vincent Chan recommends not investing internationally at all, since US companies already have international exposure and we live in a global economy.

Economists recommend holding international stocks in proportion with their global market cap weight. Assuming friction-less markets with homogenous investors, this is the optimal choice for investors.

Besides the theory, academic literature rejects many of the claims of the YouTubers.

Perold and Shulman found that currency risk can be hedged away at a negligible cost in major currencies.

Lewis finds that the correlation between multinationals and their own stock markets is high, so trying to gain international diversification from investing in US companies with international exposure is limited.

French and Poterba find that the perceived foreign risk due to low information quality necessary to rationalize the observed level of home bias is too large to be plausible.

Looking at the leader board now that we’re finished with investing, Vincent Chan is in first place with 56.25%, and Andrei Jikh, Nate O’Brien and Humphrey Yang are tied second with 44.44%.

Now, onto the last category, which is debt repayment.

Debt Repayment

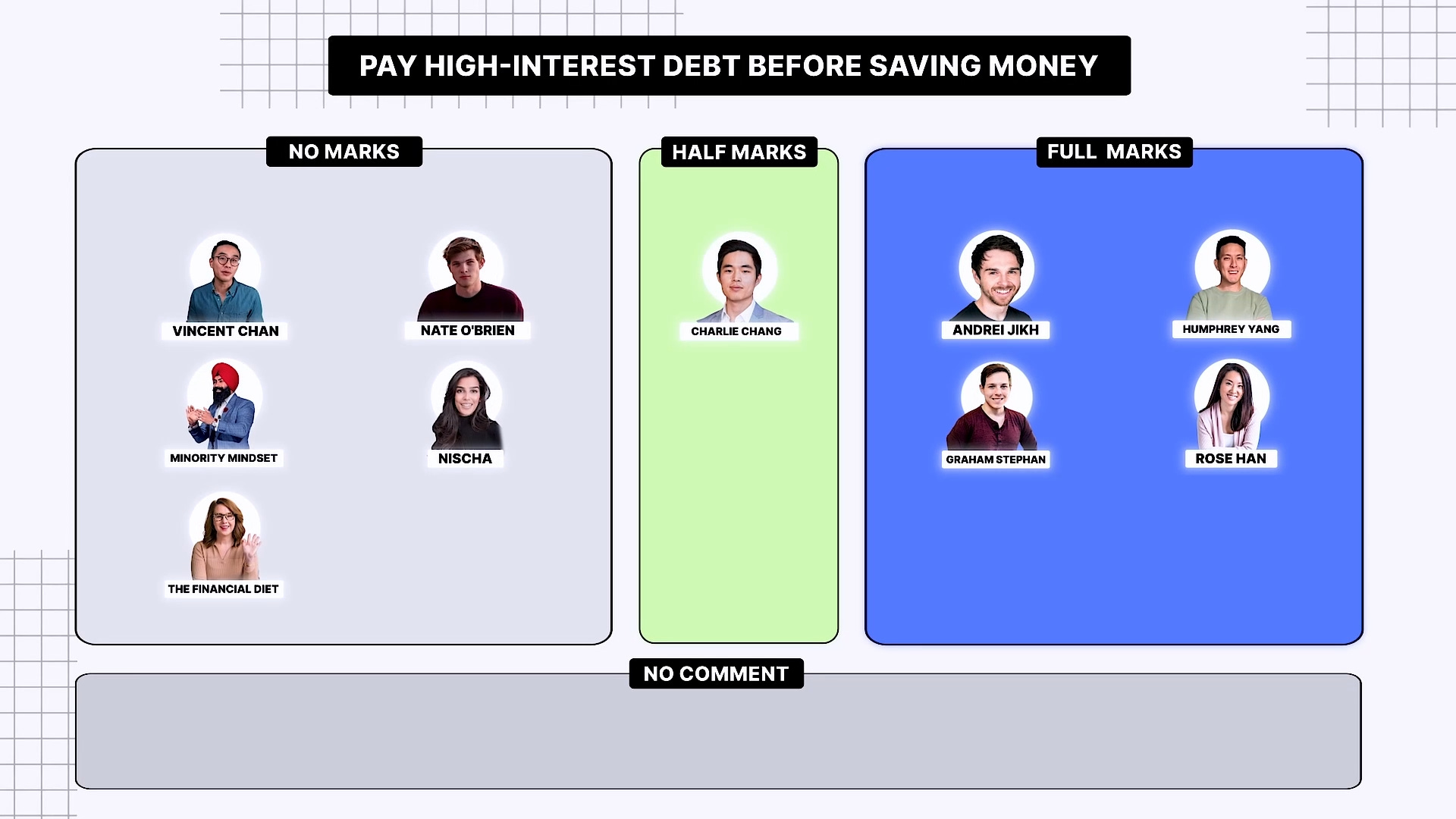

Should you co-hold high-interest debt and low-interest assets?

This one was more divisive than I thought.

Graham Stephan, Humphrey Yang, Andrei Jikh and Rose Han all recommended paying off high-interest debt before building up an emergency fund. Everyone else suggested building up an emergency fund before paying off high-interest debt.

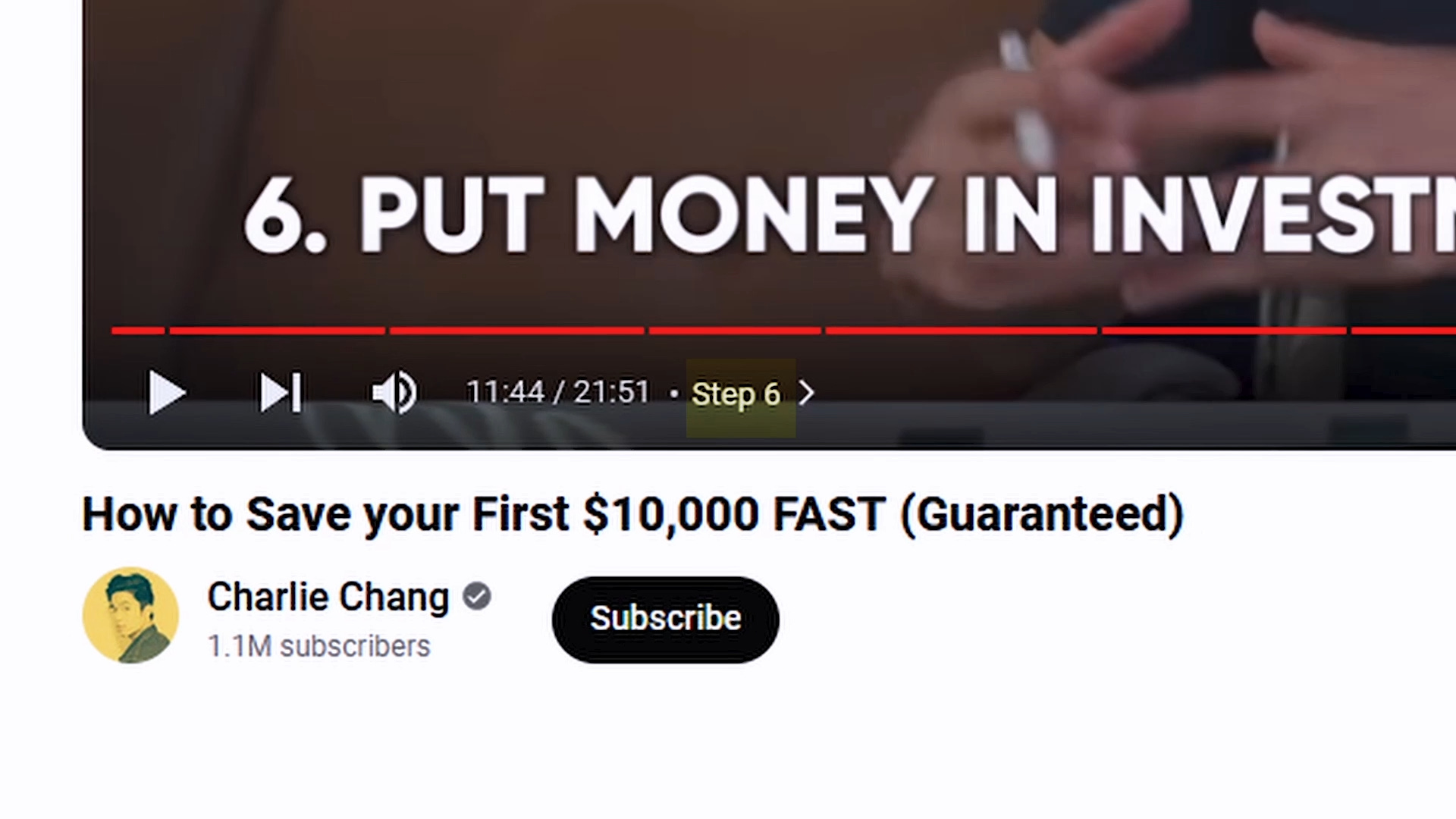

Very strangely, Charlie Chang recommends paying off high-interest debt before investing in this video on how to save $10,000 fast, guaranteed.

However, he puts it all the way at the back, at step 9.

This is weird because in step 6 of how to save $10,000 fast, guaranteed, his recommendation is to put money into investments that you don’t touch.

And I don’t know about you but that’s pretty contradictory to me… so, half a mark for him here?

When it comes to economists, they recommend paying off high-interest debt first due to the high discrepancies in interest rates in credit cards and savings accounts.

But how should someone pay off their debt?

How to pay off debt?

According to the YouTubers, there are 2 methods to pay down your debt - the avalanche method and the debt snowball method.

The debt snowball method was popularised by Dave Ramsey. Here’s Dave to explain it.

The debt avalanche method is when you order your debts in terms of their interest rates and prioritize those debts.

Mathematically, the debt avalanche method is the method that will save you the most money so economists prefer this method.

Nischa and Charlie Chang get full marks as they recommend prioritizing high-interest debt. Everyone else gets half a mark since they recommend both the debt snowball or debt avalanche.

Fixed rate or adjustable rate mortgage

And lastly we have what to choose for your home mortgage: a fixed rate or an adjustable rate.

Only 2 YouTubers uploaded videos on this topic and they both had completely different recommendations.

Graham Stephan recommended, unless you know what you’re doing, you should stick to fixed rates.

Minority Mindset mentions that, if interest rates were tending downwards you should go with adjustable rates, otherwise choose fixed rates if interest rates are already low.

Economists, specifically Campbell and Cocco, agree with Minority Mindset’s approach of choosing adjustable unless interest rates are currently low.

Guran, Krishnamurthy, and McQuade found that adjustable rates are better than fixed rates for economic stability since short-term interest rates tend to fall more than long-term rates during recessions.

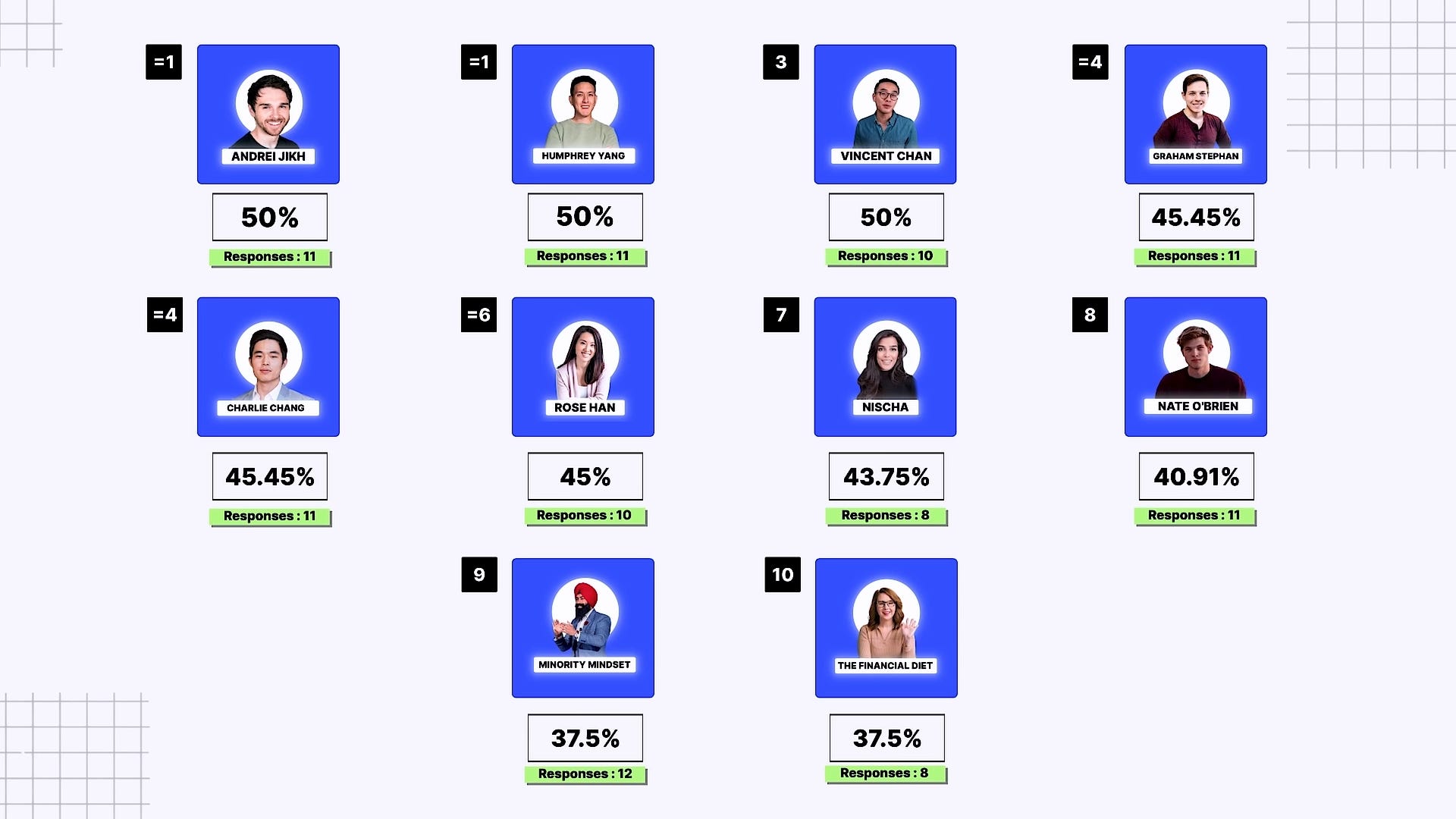

Final results

So with all the recommendations complete, Andrei Jikh and Humphrey Yang are the winners, both scoring 50% and answering 11 recommendations. In third place is Vincent Chan, also scoring 50%, and answering 10 recommendations.

Taking a look at the final results, all the YouTubers scored pretty poorly - so I think it’s safe to say that all the popular advice you hear online from finance gurus is terrible and they’re all bad people for giving you bad advice. Thanks, bye!

Does it really matter?

Ok, in all seriousness, it’s never that straight forward. I honestly think this is the most important part of the post, so if you’ve stuck around until now, thanks!

So the advice given by the YouTubers is quite different to the advice of academic economists but does it really matter? Who said economists are right? I think Choi puts it best in his conclusion: “Popular financial advice can deviate from normative economic theory because of fallacies.”

Put it this way, if economists were to write a research paper about smoking, one of the suggestions they would provide on how to quit smoking will probably be something like: “A rational person will look inwards and realize that smoking is causing harm to their body, and therefore they will stop smoking.”

And there lies the problem, a key assumption in a lot of economic models is a rational person, and we all know how much economists love assumptions.

In the consumption smoothing recommendation, economists recommend people to start saving after years of negative savings as young adults, as if it’s easy as flicking a switch. Saving as much as you can to instill a sense of discipline, like the YouTubers suggest may be a valid option to suggest.

In the no mental accounting recommendation, Choi points out a study that suggests that mental accounting increases motivation to save. I budget my money into different accounts just for some peace of mind to know that I have enough money to pay for certain things.

In the equity allocation recommendation, can you imagine someone trying to explain to an audience of millions that their equity share should depend on how quickly marginal utility diminishes and how much stock returns covary with marginal utility? Simple and easy to understand rules like “age in bonds” would travel much further.

And lastly, in the no debt snowball recommendation, Dave Ramsey knows it’s the mathematically sub-optimal option. However, the psychological benefit it provides isn’t measured by economists at all. And according to some YouTube comments, it’s a technique that really works.

So, yeah, finance YouTubers often provide different advice than academic economists but maybe that’s not a bad thing.

Here’s Choi again: “Popular advice may be more practically useful to the ordinary individual. Developing normative economic models with [human] features, rather than ceding [personal finance advice] to non-economists, may be a fruitful direction for future research.”