Crack open the KAV-a?

Crack open the KAV-a?

Small wins could add up for Kavango

Dear reader,

Ben Turney must have tuned in to a few episodes of Juan Ibarra and Freddy Dodge checking the tailings.

Doing so it seems he’s found gold.

I see a small win of 6,000 Ozs indicated just from the Nara tailings for Kavango at around 0.6g/tonne.

Assuming the current price of $2,125 and an AISC $800 (it’s been mined just needs processing) that’s a quick, cheeky $8m profit. Less the $4m to buy Nara (they have a 2 year option), which PureBond the HNW Family Office backing KAV are presumably happy to front the cash.

So a PBT of $4m for a company whose market cap is £9m and whose share was decimated following several Botswana drills chasing Copper/Nickel/PGM targets which sadly did not result in success.

It’s interesting that PureBond bought in to KAV and own a controlling 52% but paid a 66% premium to the market price back when KAV looked ready to simply go bust. The share dropped to 0.6p - would PureBond pull out? No. “We shook on 1p a share so 1p it is” they apparently said. You don’t see that kind of honour very often. Perhaps they saw the sad, slumped shoulders of the KAV crew, but reviewed their work, saw the quality and thought we need to incentivise these lads - after all Ben Turney had poured 6 figures into KAV. Rich miners are usually shrewd folk, you know.

Today’s small win isn’t that significant although it potentially provides a year’s cash flow and sustainability/dilution is the bug bear of investing in juniors isn’t it?

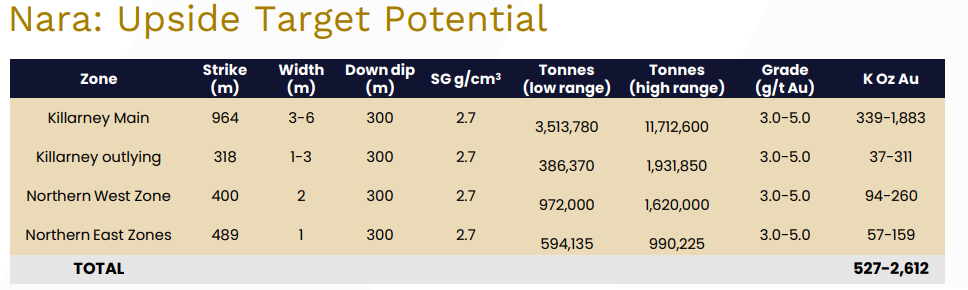

Nara is one of 3 claims in Zim(babwe). Hillside and Leopard too which you can read about in the KAV presentation. It augers well that there’s nearly a gram of gold in the tailings. The investment thesis is that in 1982 Zim produced as much gold as Oz. Then Mugabe happened. The Zim economy went to pieces and gold mining with it - apart from “Artisans” scraping with picks - and they’ve been doing so Turney tells us. The scrape marks show us exactly where to drill. Now, over 40 years later a post-Mugabe world it slowly re-opening to foreign investment. KAV reckon there could be 1Moz just at Nara, or possibly as much as 2.6Moz (see Page 16 of their deck). Other Zim mines like Caledonia historically have produced at $1000 AISC and operated successfully, so the prospect of 1Moz at a $1150 margin if it could happen would be an extremely tasty $1.15bn PBT.

A lot of purple ore bodies remain unmined (dotted lines are mine shafts).

But Kav has disappointed before, so it’s one to carefully consider. But given record gold prices, and the fact that there’s tangible gold, does that change things?

Meanwhile KAV still holds vast areas of Botswana’s Kalahari Copper Belt, Sutrure Zone, and Ditau. In the KCB its Australian neighbours (everybody needs good neiggghbours) have doubled in price over the past year and are working the copper very successfully. CEO Ben Turney now lives in Zim and is “on the ground” so could this time be different? This time there’s quantifiable metal and not just ground-breaking (so to speak) Geo-Phys interpretations of a magnetic resonance nearly a Km underground. That gives me some reason to pause and reconsider.

This is not advice.

Oak

Have been in KAV 3 years and this is the first tangible piece of shareholder value so great news. Well written article.

What is the source of "2.6m oz"? When the Nara option was announced the estimate was 500koz, more recently they talked about potentially 1m oz. KAV are conducting IP & drilling imminent. So intrigued to understand more about 2.6m because if it turned out to be true then KAV could easily be worth +20p/share