DEC-imals and decibels

DEC-imals and decibels

The clamour of preserving dividends vs buy backs at DEC

Dear reader,

My article DEC-laration on buy backs is showing its age.

It was written at a time of “old money” i.e. pre the 20X consolidation and at a share price of £13.00 a share.

Today we are in different times so let’s refresh the model…. at the risk of throwing the cat among the pigeons.

The thesis of the model is that if we buy back shares then a few things happen. First of all, some of the funds which leave the company are retained by the company. The reduced outflows benefit shareholders since the retained assets are greater. But also the effect of fewer shareholders mean your relative ownership increases. Like a timeshare where you get more days per year - think of buy backs like that.

If we look at the progress to date we can see as of Friday 2nd Feb 788,761 shares have been bought back since the beginning of the programme. The $2.7m of dividends not distributed means each share is worth 16c more per year in terms of assets.

To arrive at “adj. shareholder funds” I used the H1 2023 shareholder equity and added back the long term liability of Derivatives to arrive to $1,291,202,000. ($1.3bn approx). I explain in DEC-the-halls why IFRS9 means it must be included for statutory purposes. But for fair analysis it’s fair to remove the possible future P&L cost of derivatives because we aren’t also factoring in the corresponding 8 years of future income either (the gas sales that are set at “guaranteed minimum prices).

The $11m reduction in shareholder funds is because buy backs reduce the assets in the company (they pay to buy and cancel the shares).

Bear in mind reader, too, that the Q4 Trading update confirms $233m of debt has been reduced. So potentially shareholder funds are +£233m i.e. $1,525,091,000 or some proportion of that $233m. But for simplicity, today, let’s assume shareholder equity didn’t change. That’s a Brucey Bonus to look forward to in the annual report. ;)

The value per share of $26.80 is what the accounts say is the value of your proportion of DEC per share. That’s excluding an approximate 25% of the ARO plugging costs at $25k per well. That equates to $3.50 of assets per share, offset against the ARO liability. If (as some Woke Commentators like to claim) shareholders intended to “do a runner” then you actually have $30.30 per share. But DEC is doing the right thing, so $26.80 is all you get, shareholder reader.

It’s also excluding the $5.9bn of PV10 discounted future earnings and cash flow I estimate in DEC-iding 2024 strategy. That my dear reader using simple maths is $123.49 share, less a further $10.50/share of ARO, assuming no doing a runner and DEC carries out its legal responsibility to plug fully-depleted wells. A “mere” $112.99 per share extra.

Any decision to exit in a harrumph would forego $26.80 + $112.99 / 1.27 = £110 a share. So the market price is at a 91.6% discount to current and theoretical future NAV. Or £21.10 today and a 56% discount to NAV today (based on H1 2023) to keep it here and now.

The Immediate Future - the existing authority

The existing authority of 90.5m shares (old money) is 4.525m now. Let’s assume those can bought back at £9.25 average in the coming months.

The effect is very positive as can be seen. Each DEC-hand stands to see a 5.25% increase to the assets they hold per share, worth £1.11 per share once the existing buy back is complete.

The controversy - and allure - of buy backs

In DEC-iding 2024 strategy yesterday only 16% want to prioritise buy backs (colourfully named Chuck landlubber Shorters overboard) and 35% believe Rusty has the right strategy (which includes buy backs).

So 51% directly or indrectly want buy backs (albeit there is a strong voice to preserve dividends). I do not take a stance between these two approaches reader, merely seek to explore the facts. Both have merits.

84% don’t want what I’m modelling next. Fair enough.

The point of this article is to explore what would happen if the dividend was paused in 2024, and if the price crashed as a result as has been mooted by some readers. Or if due to further price crashes, Rusty decides enough is enough and declared the price so attractive that dividends are cancelled - so the value of the entire 2024 dividend should be purposed for buy backs.

Under this scenario I’m also assuming no particular focus on other objectives such as further acquisitions or paying down debt. So I’m not saying this is what will happen, I’m imagining what could happen.

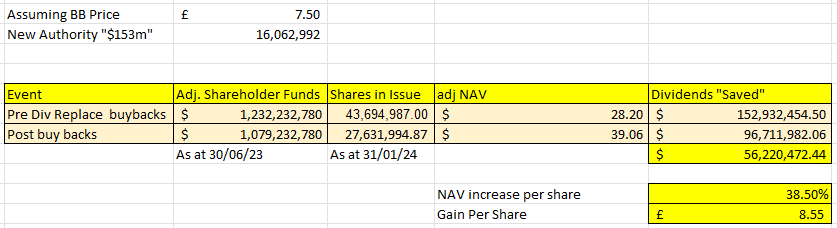

Assuming “the price would crash” as predicted anti-BB readers, meant a 15%-30% drop in price from £9.25 and therefore buy backs could occur at an average £7.50, and the authorisation amount was the value of dividends which following the immediate future were $153m. That $153m would equate to over 16m shares bought back leaving just 27.6m shares in issue and benefit shareholders by 38.5%. (that’s before any 2024 profits of course)

Now of course the extent to which the price crashed would depend on a number of things. The FY2023 results for one. If I’m right about the NAV being above $1.2bn, do you actually want to sell shares at an even steeper discount to their value? Would people ditch DEC in great volume? I assume some would, but would others buy in to replace them.

Also if dividends pause they can also resume. In fact if DEC-hands knew there were resuming dividends in 2025 after a year of buy backs would they sell?

Let’s run with the theory and see the results.

Wow. If dividends resumed at $153m in 2025, theoretically that could mean affording a dividend of $4.85 a share by restoring the current $3.50 per share per annum dividend + 38.5%. On a £7.50 share price that’s a stonking 51% dividend!

38.5%? C’mon, Please be realistic!

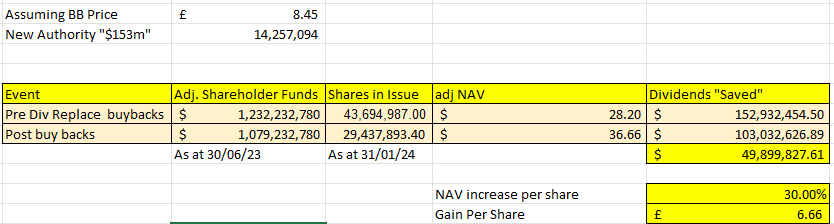

Ok, ok, let’s assume the price doesn’t crash. But the dividend is paused and buy backs occur. This time the improvement to NAV is less pronounced but still it’s substantial.

About a third of shares are bought back, and a 24.77% increase is achieved. Now the sharp eyed among you might say ah, hah, but my dividend of 30% (less if you bought at higher prices) is more than 24.77%. Don’t forget a dividend is every year so that’s 24.77% per year, not one off. But you could argue you use your dividends to invest and grow those funds (e.g. buy more DEC shares), so the recurring nature of dividends is irrelevant.

If you thought that reader, good point. That was my thought on this too. So is below £8.45 a share the point at which Rusty says enough is enough. Until then the focus is acquisition and efficiency?

A penultimate thought

The ABS loans mandate a maxium 2.5X adj.EBITDA/debt. This is a constraint to buy backs. If you are buying back, your net debt is increasing (you’re using your cash). Assuming adj.EBITDA remains constant then the year end 2.4X only needs to tip a little to breach. Now, there is $200m liquidity which I don’t believe is factored in to the 2023 trading statement calculations.

Taking $540m adjusted EBITDA and 2.4X cover suggests debt is at $1.296bn at year end. Therefore less $200m repayment/working capital (RNS 04/01/24) drops the ratio to 2.03X ($1.096bn/$0.54bn) in early 2024.

0.47X head room theoretically allows $254m of buy backs - well above $153m. But 0.1X head room doesn’t. But there are many moving parts including whether 2024 earnings change, acquisitions occur, and other factors.

Conclusion

This article seeks to show the value which might accrue from buy backs. However I hold a sympathy for those dependent on dividends, those who feel maintaining dividends is a great way to (quite literally) make the shorters pay, and also that the dividend itself is extremely attractive.

A focus on buy backs isn’t the top voted approach, but it would be interesting to take a further poll to ask whether your opinion has changed as a result of this article. I’m not expecting it has - but let’s see.

This is not advice

Oak

I appreciate the analysis (along with all the others you’ve done on DEC) and it’s very informative. But (you guessed one was coming) it’s based on numbers and logic whereas many investors do not seem to use logic but rather emotion and sentiment. Confidence in DEC seems to be shaky and the shorters keep chipping away and if the dividend were cancelled I genuinely think it would be a bloodbath. They could shout promises of a dividend resumption until blue in the face but they would be drowned out with the shorters screaming we told you so. Who knows how low it could go and I’m not clear what the impact is on the company itself, if any. I would guess though that a competitor might look at picking up a bargain?

As I mentioned elsewhere I prefer stability but whatever they do I would hope that they provide a very very clearly articulated strategy outlining what they are doing and why. They need to up their PR game as even institutions lose patience eventually and will look to exit

Blackrock reporting 5.5% position as of December 31. Likely reason for today move.