Ding dong! News from BELL

Ding dong! News from BELL

Positive updates on a number of levels

As was expected, approval in Singapore is rapidly unlocking other Asian territories. But today’s news is spectacular. China. Bell is now licenced to sell X-Plor (via its Innomax JV) in China. The recent news about Singapore’s approval was forecast to unlock other territories - and the lock just went click. I expect we’ll see other SE Asia territories following like Thailand and the Phillipines.

Upside

China

with a market with 100m COPD sufferers. Hong Kong and Singapore are exciting too. Hong Kong was covered in BELL-Kong and yes there were only 0.2m COPD sufferers but Hong Kong alone is worth an estimated £75m in future profits to BELL and at no direct cost since Innomax build and BELL gets a licence fee and revenue share. But China is 500X the opportunity. The big one. A $1bn market just for COPD and just for Asia alone. Worldwide, part of a $34bn oxygen therapy market. Talks have already begun with several distributors.

Exclusive

Into a market where we learn today some US channel distributors are planning to ONLY sell BELL products - because they are the only ones which make sense. They can get maximum coverage (subsidy) from Medicare. They cost less, weigh less, and provide better control and functionality. They are also more suited to rentals where filters can be swapped out to the same machine rather than having to replace entire machines. That’s a key advantage when you’re selling to equipment rental/leasing companies.

Higher Revenue

Did you spot the $3,000 for Discov-R price point reader? This was previously a $2,500 price point. So the product is so strong its price is being lifted by 20%. There was some suggestion previously that a higher price might be achieved but this confirms it.

Cash Positive

Confirmation of Runway - BELL confirms the TMTA cash and recent fund raise takes it through to cash positivity. This was forecast by the Oak Bloke in BELL-under, but the expectation is confirmed in the RNS. So much for those who predicted it would run out of options - and cash.

The fundraising has actually raised net asset value to shareholders - as I explain in BELL-longing together.

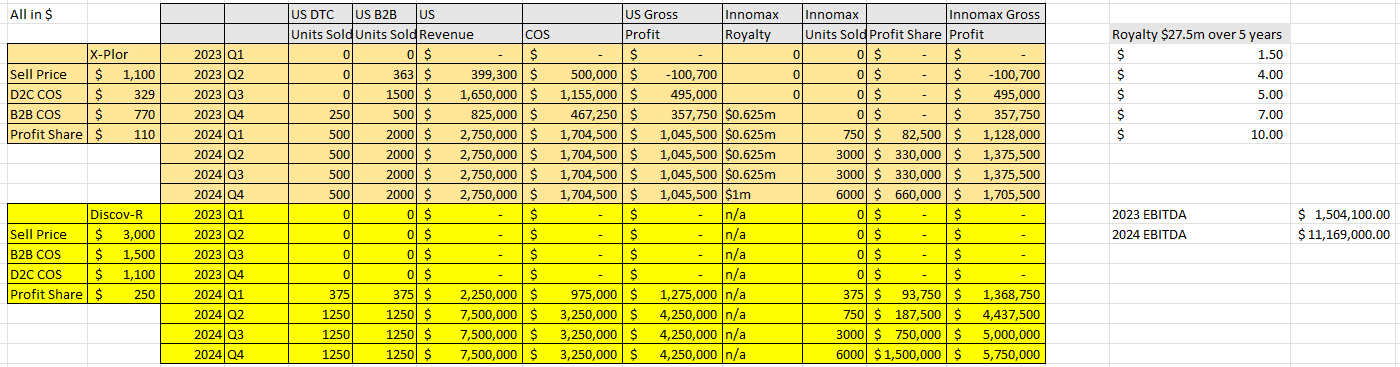

In the charts below I’ve now accounted for the revised cash flow of operations, and the TMTA cash in Q1 2024 but other assumptions remain the same.

Lower Cost

Replacing polymer with a metal sieve will improve margins by 50%! That’s phenomenally good!! Reaction from the market? Zero.

Estimates from Dowgate previously put the margin per Discov-R unit at $800 ($2500 sell price and $1700 cost of sale) so improved margins of 50% at a higher $3,000 sell price I’m assuming is just a $200 per unit reduction for B2B (i.e. $1500 cost of sale on a $3k Discov-R price). I’m going to use a $400 cost of sale discount for D2C consumers. The reason for this is that we know in today’s RNS that gross margin on D2C sales to X-Plor customers is ABOVE 70%. Dowgate tell us $1100 selling price and $770 cost of sale. So I’m assuming $400 of the $770 is the distributor’s cut, to arrive at “above 70% margin”.

Bad news?

Adjusted EBITDA was forecast at -£6.5m in 2023 by Dowgate turning positive £1.5m in 2024.

Today we learn it will be “slightly below”. So -£7m perhaps. So -£3m occurred in H1 so adjusted EBITDA will be about -£4m in H2. All in all, given the investment and progress I’m happy to forgive a -£0.5m miss. In the bigger scheme of things it simply won’t matter.

Forecast Changes

The impact on sales from today’s RNS is to push all Discov-R sales back a quarter - including the ramp up timings, but to offset that US sales are calculated at higher margins.

The Gross Profit from the above sales flow into the “GP Activities” column below.

I’ve also pushed back the timing of investing and w/c changes a quarter - since the launch of Discov-R is delayed. But look at how the cash begins to generate in 2024! BELL should be able to surprise to the upside in 2024, in my opinion. I don’t consider my forecast to be particularly aggressive - and sits below Dowgate’s.

Remember too, reader, its market price is barely above its estimated Net Asset Value (20.1p NAV vs 22p ask).

And finally - that this isn’t a static product picture in 2024 either - there are exciting plans to capitalise on extending sales to its growing customer base and further meet their needs. I explore this in my previous article BELL-issimo

Bell - you’ll not be surprised to learn - is one of my Oak Bloke Top 20 for 2024. This will be a list provided for entertainment and is not a recommendation.

This is not advice.

Oak