Is ANIC in a pickle?

Is ANIC in a pickle?

Understanding Year End Accounts for 30/06/23

Good evening reader

You will be pleased to learn today’s picture is not anything horrific. Nor will an alien bury itself in your abdomen if you spill the contents. It’s simply a kombucha fermentation. A very healthy type of tea, which is very good for your digestion. The Oak Bloke regularly buries his roots into a good Kombucha.

Kombucha is not actually a line of business that ANIC gets involved in but the closest “fermentation” picture I could find.

On to ANIC. I had a bit of a challenge getting my head around the net asset value. The challenge was/is that ANIC’s auditors included Blue Nalu’s Series B investment dated 15/09/23 into the Year End Results 30/06/23.

This chart is the product of hours of work and I believe this chart accurately reflects the Year End Fair Value plus all the CY2023 H2 movements and gains. I’ve then used cash as at 30/09/23 less the £700k and £577.5k post period investments to estimate current cash.

The result? A pleasing NAV of just over 18.1p. A discount to today’s ask price of 11.5p of 36.5% (Bear in mind too ANIC has increased 17.2% since the Oak Bloke Tipped it for his 2024 Top 20)

I’ve previously covered the investment thesis in ANIC are you ok Part 1 in ANIC Are you Ok Part 2

One of the best single articles I have read so far is this piece in the NY Times. I’d strongly recommend reading this - it provides the best picture of the state of play for this interesting food technology play.

Updates and Change

Let’s talk about the bad and the ugly - there’s not much.

Ohayo Valley:

What wasn’t entirely clear in the annual report was the fate of its holding poor old Ohayo Valley. It’s precision fermentation Wagyu burgers sounded delicious. The Wagyu web site is still operational but it has been erased from Agronomics with no RNS to explain. So I’ve written it down to zero.

Rebellyous:

Poor rebellyous was also missed from Anic’s pie chart but explains why the pie chart at the bottom of the Chairman statement adds up to one number and the balance sheet itself is £237k greater. Whoops!

Rebellyous is alive and kickin’!

Blue Nalu: (Bad and Good)

I got very perturbed when the 30/06/23 accounts were released because its NAV was much higher (about £11m) more than expected. While a NAV rise is very welcome I couldn’t work out how it had increased. What date the pie chart related to? The later 30/09/23 ANIC valuation was lower so it appeared ANIC’s NAV had dropped quarter to quarter. No! It was clarified to me that the Blue Nalu gain (RNS 15/09/23) has (for whatever reason) been included in the Year End Accounts (30/06/23).

The blue fin tuna business is also alive and kicking, to my great joy. I included it in my “bad and ugly” but it is also “good”. A gain of over £7m. As I explored in my earlier article going after high end foods which are ESG toxic (due to its critically endangered status), seems a hugely sensible approach.

I would love that one day they could produce animal-free Shark Fins and Pangolin Meat via cellular agriculture in due course to cater for the, how can I say, some of the other controversial eating practices of East Asia.

The GOOD

Formo

These produce animal-free Cheese products, particularly.

Their Formo web site is clearly wacky but the idea isn’t. In fact University of Bath research (5k sample) shows 78% would want to eat animal-free cheese. Ciao, cow, indeed!

9m tonnes of cheese are consumed each year in Europe. At an average £10/Kg for cheese that’s a £90 bn/year market. Formo want 10% of the action by 2030. If they can (and there’s the twin challenge of demand and of supply - more on that later), that’s a £900m turnover business. Let’s say even an 8% net margin and you have a £72m profit and at 15 times earnings that is a Unicorn (A £1bn business).

Formo raised $50m in 2021 and production they say is “imminent” in 2024. Production means 50,000 litre vats producing a curd after which the usual cheese-making process continues.

Dairy drives 18% of greenhouse gases and precision fermentation reduces that by over 95%. At which COP conference in the future will they tackle the moo moos and charge a methane tax? It’s pointless bleating on about aspects like oil in the north sea, when energy production and transport emissions are dropping - farming emissions simply aren’t. Instead more and more people want meat and cheese.

I included this as “good” because ANIC have tripled their money with Formo (on an unrealised basis)

Solar Foods

Solar Foods. Imagine you could make protein. Not from animals. Not from plants.

From Microbes, using Electricity - renewable, of course - and carbon dioxide.

Agronomics held its 5.8% holding at book value (€6 million) based on its Series A/pre-Series B participation in Solar Foods, at a €103 million valuation.

In November a Series B round revalued Solar Foods at €178 million in a Series B oversubscribed upround.

Again ANIC have more than tripled their money.

-

What is Solein from Solar Foods

The process takes a single microbe, one of the billion different ones found in nature, and grows it by fermenting it, which is also called a bioprocess. They feed the microbe like you would feed a plant, but instead of watering and fertilising it, Solar Foods uses air and electricity. With its current process, this is 20x more efficient than photosynthesis (and 200 times more than meat).

By using fermentation to grow protein, the bioprocess of its first protein product Solein® may not be traditional, but it is natural. And the best part? It won’t run out.

Imagine what the production economics will be for something which 200 times more efficient to produce than meat? Could this be a holy grail for feeding the world in the future?

SuperMeat

This time it’s chicken. What strikes me here is a couple of simple truths. Slaughter is a pretty horrific process to be fair. I watched a programme about Bernard Matthews recently where bits of the plastic machinery but breaking off and going into the Turkey… and slime and cross contamination. Ugh. Horrific.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

So is that not a major selling point of precision fermentation?

Elimination of slaughter removes a major point of contamination, resulting in fresh poultry with longer shelf life and no need for use of antibiotics.

Supermeat have raised $15m (14th largest company by fundraise) and have a commercialisation agremeent with a £26bn Swiss retailer Migros. They begin selling next year (2025)

Supermeat also have researched and found the majority of Chefs are keen to introduced animal-free meat.

Meat worldwide is a $1.3tn market and 30% will be animal-free by 2040 they suggest. So a $360bn market. If Supermeat can capture even 0.2% of that market that’s a $720m turnover business perhaps generating a £50m profit, and would be valued in the hundreds of millions.

The problem of supply

My unending optimism must be tempered not just by market demand but also by science. The science of supply. The practicality of growing supply, and producing at an acceptable price point. Some ANIC holdings report a reduction of cost in the magnitude of 88x but more must be done.

If you look at capacity in 2024 (the green at the bottom of my presumably animal-free glass of milk) and even look at demand growth in the coming year we can build it but the demand will come too fast!

(Thank you to Dazzle in the comments who shared this great insight)

Taking Formo is it realistic to grow to address 10% of the European cheese market by 2030? If they build a 600,000-liter facility, producing 0.1kg of cheese per litre, and run the process weekly, their annual output would be (365/7)×600,000×0.1=3,100 tonnes. This represents only 0.03% of the European cheese market. Achieving their goal would require approximately 30,000 times more production capacity. Where would this substantial increase come from?

That facility could cost about £40m to build (using Liberation Labs), so £2m a year depreciation, plus running costs. 3,100 tonnes of cheese at £10/Kilo is £31m revenue. So the profitability is there, depending on running costs. But to supply 10% of European cheese requires a cool £1.2tn. With yield, scale and process improvements I expect this number can be reduced but the sheer scale of money needed would be on a par with the green energy revolution. And the opportunity is colossal.

Remember both animal-free and green energy roughly progress us the same amount to net zero. Can we do one without the other, reader?

If only there was a picks and shovels provider of facilities?……

Liberation Labs

For my final deep dive let’s address that and how the above companies ferment. This last one is a “picks and shovels play” if you will. A contract manufacturer.

How does it work? So you need cells so from the target foodstuff so beef, tuna, chicken, milk etc. This is called “the media”. You need sugar, but you also need the vat or the biotechnology reactor.

If Precision Fermentation is going to explode as is thought you need to cope with that “gold rush”. Liberation Labs (LL) say current contract manufacturing facilities are unsuited and expensive. They are built 60-80 years ago and aimed at producing antibiotics and chemicals.

LL provides the means to biomanufacture and to ferment.

ANIC own 37.4% of LL currently but a Series A $40m funding round will complete in Q1 2024. This is part of a production facility build in Indiana, part supported by the US government and begins to address the capacity challenge which will hold back the growth of precision fermentation at scale. Scale being a 600,000 litre facility and this will be built by the end of 2024.

This is another holding which has tripled in value.

Valuation

The tripling of several holdings as far as I can see is based on tangible progress both technological and commercial. This isn’t some finger in the air, random reval.

It’s sobering that the “future” of this stuff is much more near term than perhaps people realise for animal-free animal products. 2024 and 2025 are going to see huge progress.

Another aspect is the regulatory approval. But the number #1 and #2 funded companies (both non-Agronomics companies - Upside foods and Eat Just (did somebody say…… Eat Just?) who already have all three FDA approvals. The key point to take from that animal-free chicken nugget is that it is far easier for others to follow including all of ANIC’s holdings. The FDA are the toughest - so regulatory approval elsewhere in the world is generally easier.

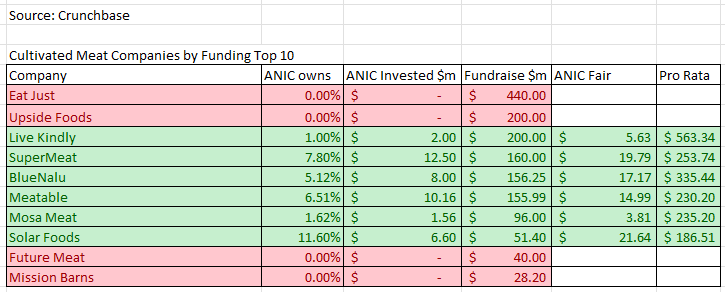

So let’s do a worldwide Top 10. This is (to the best of my knowledge and as at 6th January 2024) the top 10 alt-meat backed ventures.

Anic invest in the joint second #2 to the #8 largest. But if I apply the latet fair value the pro rata value emerges.

ANIC appears to have a stake in the five most valuable precision fermentation businesses in the world

I’ve made no attempt to find what the non-ANIC companies fair value is. If theirs are correspondingly higher I wouldn’t be surprised…. but when you look at ANIC this way then my musings on these growing into one or more Unicorns isn’t that wacko…. they’re already well on their way!

Conclusion.

There remain challenges ahead. Cost. Scale. The inevitable franken-meat objection.

But the advantages of animal-free are compelling: Environmental, Tax, ESG, Simple Economics, Sanitation, Health….. the tailwinds are such that one can imagine the world changing far faster towards this faster than the 30% animal-free meat forecast by 2040. But what if the pace of change were far more comprehensive - say 90%? If scale drives cost reduction (I’m thinking of 200x more efficient has to eventually make this cheaper than traditional farming) doesn’t that simply end farming except for hard core enthusiasts?

It’s fair to say not all holdings will succeed, but even one holding succeeding and thriving to grow to a unicorn could cover the £111m buy price - and then some. But the range and breadth in terms of product, geography as well as picks and shovels investments are impressive.

Also how targetting the thin edge by choosing higher price products like blue fin tuna can drive adoption to other species of endangered fish and it grows from there.

ANIC regularly issues positive RNS updates and news. I’m glad I’ve been able to reconcile its final accounts for FY2023 and eradicate the “unknown NAV” so now have a forecast NAV which is (I believe) fairly accurate and reflects progress since June 2023.

This is not advice.

Have a good weekend

Oak

Rebellyous Foods expect to be profitable this year - they not only provide their own plant based chicken but also supply processing facilities and tech to other plant based food companies.

To find out more and to keep updated on all things cultivated meat - including Agronomics companies follow my youtube podcasts issued weekly. https://www.youtube.com/@FutureofFoods

Thanks so much for this detailed analysis. Much appreciated!

I'm wondering about the long-term strategy of ANIC.

What happens if one of the companies in the current portfolio becomes the market leader in the next decades. Will ANIC hold their shares of this company or will they sell it. And what would be the impact on the ANIC shareholders?