POW-er rangers

POW-er rangers

What does the Power Metal year end update tell us?

POW reports its year ending 30/09/2023 yesterday.

A relatively small loss on operations (-£1.3m) from expenses (-£2.8m) and we know post period fundraising (£1.3m) has brought more funds in and gains in the year covered (+£1.5m).

The update gave me a chance to update my cornucopia tracker - see below. An interesting detail I decided to add was planned listings. Working through the report there are 4 further IPOs are planned.

Planned IPOs

1.“UEE”

UEE or Uranium Energy Exploration Plc - this will comprise of 19 properties and 1000km2 of which 10 properties have been explored, and the 19th (comprising 31km2) was staked a few days ago at a cost of just C$1,800! This will either IPO or a trade sale is possible with several interested parties. The est. fair value is said by analysts to be £12.5m yet is in the NAV at £0.35m.

2.“FDR”

This new deal comprises several Australian copper/gold prospective grounds with some rare earths and further uranium thrown in. In the books at £1.7m with fair value at £2.5m.

3.”ION”

Ion Battery comprises three assets. A lithium asset called North Wind where assay results are pending, authier north another lithium asset of 560 hectares. Third, there’s a 4,222 hectare Graphite project in Canada. Combined they are in the book at £0.25m, with fair value at £0.5m

4.”NHM”

New Horizon Metals is 20% held by POW and is working towards an ASX listing. This is another Uranium and Gold project.

Publicly Listed

GMET - The publicy listed holding at 30/09/23 was £7.1m but post period there is a £1.4m gain.

POW hold 1,749,378 warrants to acquire new GMET ordinary shares at an exercise price of 10.75p per share and with an expiry date of 10 May 2024, and a further 1,749,378 warrants at an exercise price of 17.5p per share and with an expiry date of 10 May 2025. So that would boost the shareholding by just over 1.5% (from 61.03% to 62.57%)

FDR - valued at £1.1m but post period the shares have fallen so a £0.3m loss (despite positive news which I covered in my article POW WOW.

So POW is on a 26% premium to what appear to be mispriced assets. Or a 41% discount to estimated fair value. But even at that price, it doesn’t reflect the progress at each asset nor the pending results and updates.

For example, it was salutory to see GMET at 30/09/22 was “worth” £4.9m in the accounts 30/09/22. Yet today the same assets are “worth” £13.9m as is seen above in GMET’s mar cap. (market capitalisation). It is certainly the case that GMET has made progress, but the unlisted assets are better valued now that it is publicly listed than when it was a privately held asset.

When there’s 4 more IPOs planned will we see the same? If so there’s a prospective pro-rated £10m gain - let alone any news flow…. and there’s plenty more of that to come.

Additionally…

Saudi Projects 2024 and beyond (more to follow Sean tells us)

Molopo Farms - Nickel/PGM drilling underway targeting the highest conductor

Tati Gold - detailed soil samples being taken to analyse the breadth, size and orientation of the target zone.

A final thought

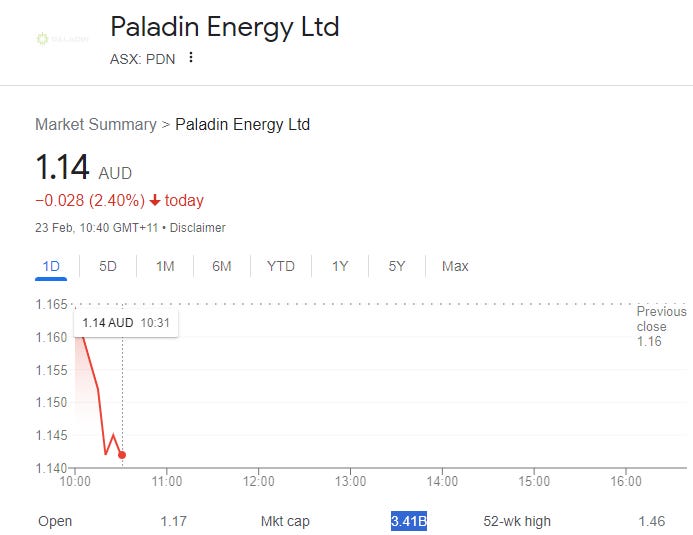

What is a Uranium mine worth anyway? Well If we look at ASX-listed Paladin as an example these are imminently recommencing production. They have a JORC resource of 77m lbs of U3O8.

Paladin’s market cap is A$3.4bn or £1.75bn and around £0.25bn of investment/equity so £1.5bn net for a 77m lb resource of about 2,500ppm. So far POW has soil samples and rock grab samples of up to 1,120ppm across numerous of its 19 projects. But what lies beneath?

Bear in mind too, reader that Paladin bought this mine for £7.7k!

Rossing - is nearby to Paladin’s Namibian mine. This similar sized mine Rossing is worth about £200m and generates a net profit each year of £35m

Eagle-eyed readers will suddenly realise they’ve heard of Rossing before. POW believe 1 of their 19 projects bears geological similarities…..

And at another of POW’s 19 uranium projects, Badger Lake, POW sees similarities to a 257m Lbs deposit called Arrow…..

19 shots at goal, just for the uranium goal and any one of these could be a worth a billion. Such potential should get peoples’ geiger counters clicking at or after the UEE IPO. And that’s just one metal in the cornucopia of POW’s metals.

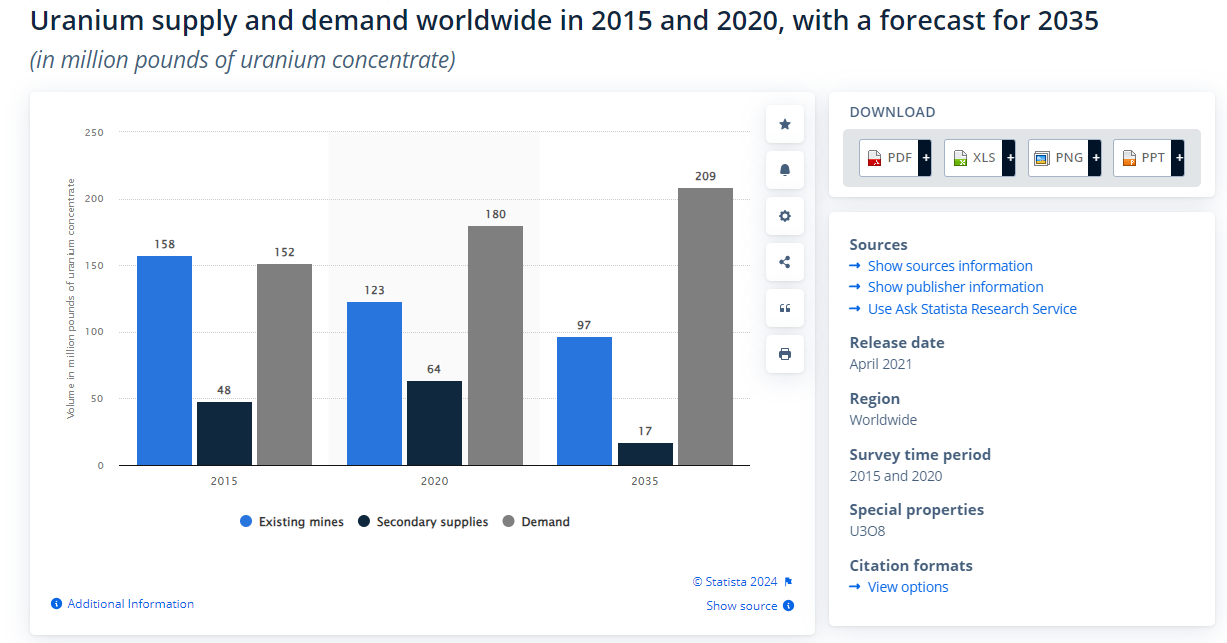

But Uranium is in demand - and that demand is growing. This podcast 20 countries including Ghana who are tripling their investment into nuclear energy as part of Net Zero plans. Forecast demand dwarves supply. Music to an investor’s ears.

This is not advice

Oak

The GSAe acquisition looks interesting. Never heard of the company but the TiO2 technology could be very lucrative. I am sure Sean has checked it out. Looks like lots of upside for a very small wager. I wonder if Sean is heading to Tronox Yanbu?

POW is like buying a 10 year in the money call option on the global mining industry at a fabulous discount!